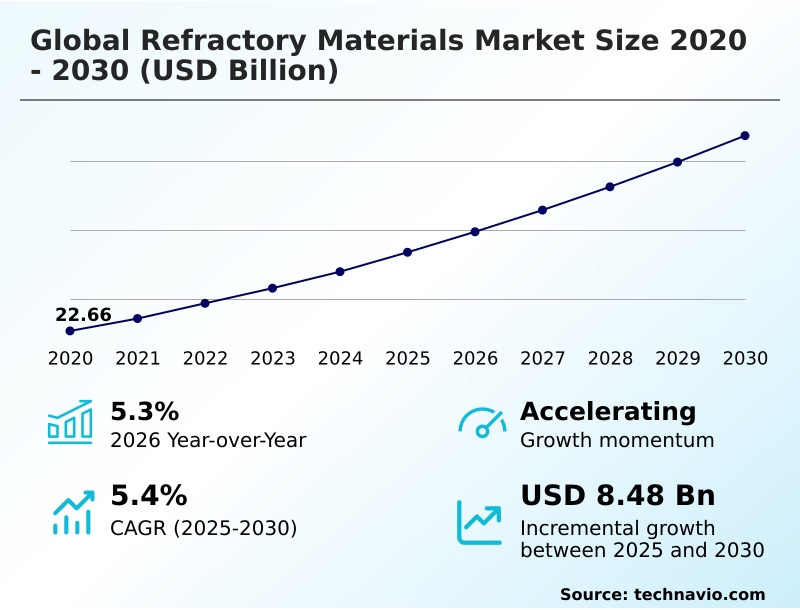

Refractory Materials Market Size 2026-2030

The refractory materials market size is valued to increase by USD 8.48 billion, at a CAGR of 5.4% from 2025 to 2030. Sustained global demand and capacity expansion in core end-use industries will drive the refractory materials market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 68.3% growth during the forecast period.

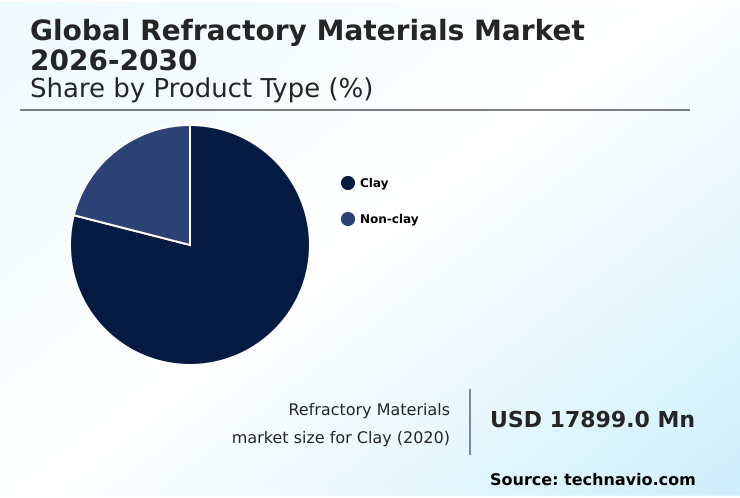

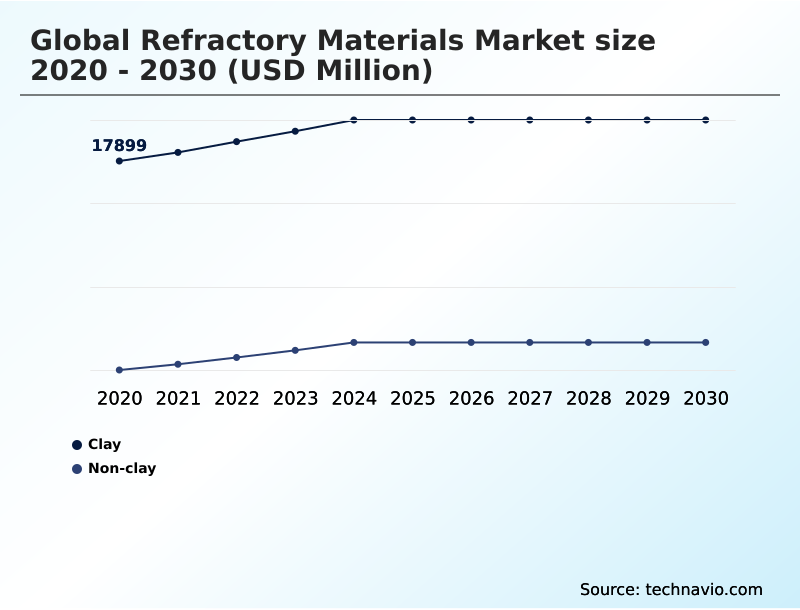

- By Product Type - Clay segment was valued at USD 20.48 billion in 2024

- By Type - Shaped segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 14.20 billion

- Market Future Opportunities: USD 8.48 billion

- CAGR from 2025 to 2030 : 5.4%

Market Summary

- The refractory materials market is integral to high-temperature industrial processes, providing critical thermal containment for sectors like steel, cement, and glass. Market dynamics are shaped by a persistent need for operational efficiency, driving a transition from commodity products to high-performance, engineered solutions.

- A key trend is the move toward materials that support industrial decarbonization, such as linings for electric arc furnaces and hydrogen-based production units, which demand enhanced chemical and thermal resistance. Concurrently, the industry grapples with volatile raw material supply chains and the challenge of developing longer-lasting products that inherently slow replacement cycles.

- For instance, a steel manufacturer might implement a new monolithic lining that extends campaign life by 15%, reducing annual maintenance costs but also lowering the frequency of refractory purchases.

- This scenario highlights the market's shift toward value-based partnerships, where suppliers provide integrated solutions, including predictive maintenance and recycling services, to align with customer goals of maximizing uptime and minimizing total cost of ownership. Digitalization, through sensor-embedded refractories and AI-driven wear modeling, further accelerates this transformation from a material supplier to a technology and service provider.

What will be the Size of the Refractory Materials Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Refractory Materials Market Segmented?

The refractory materials industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product type

- Clay

- Non-clay

- Type

- Shaped

- Monolithic

- Application

- Iron and steel

- Non-metallic materials

- Non-ferrous metals

- Others

- Geography

- APAC

- China

- India

- Japan

- Europe

- Germany

- France

- UK

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Product Type Insights

The clay segment is estimated to witness significant growth during the forecast period.

The clay-based segment, built on aluminosilicate systems, remains foundational in high-temperature industries. While evolving, its market position is sustained by cost-effectiveness and raw material availability.

Innovation focuses on developing high-alumina compositions and advanced chemically bonded refractories to enhance performance in demanding applications like anode baking furnace linings.

This includes non-wetting alumina castables engineered for superior corundum growth prevention and low thermal mass refractories that directly contribute to embodied carbon reduction. The core objective is optimizing thermal containment design to improve efficiency and extend service life.

For instance, new formulations demonstrate improved refractory wear rate predictability, a critical factor for industries where lining performance must align with strict production schedules and refractory compatibility with green hydrogen is a growing concern.

The Clay segment was valued at USD 20.48 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 68.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Refractory Materials Market Demand is Rising in APAC Get Free Sample

The geographic landscape is dominated by APAC, which accounts for over 68% of the incremental growth, driven by massive industrial expansion. This region’s demand for fused-cast refractories and magnesia-spinel bricks is fueled by new steel and cement capacity.

In contrast, Europe and North America focus on technological upgrades, with a strong emphasis on green steel production and materials for clinker-free cement kilns.

This drives adoption of specialized products like high-purity fused silica for glass and ultra-low cement castables with superior alkali attack resistance. The market shift includes a focus on end-of-life material management and detailed structural integrity assessment to optimize performance.

Specialized submerged entry nozzles remain critical for advanced steelmaking globally.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global refractory materials market is undergoing a significant transformation, moving beyond traditional supply models to address complex industrial challenges. There is a growing demand for refractory materials for hydrogen DRI, as steelmakers pivot to greener production methods. This requires materials with unique chemical resistance.

- Similarly, the need for high-purity refractories for glass melting remains critical to prevent product contamination and ensure long furnace campaigns. In steelmaking, monolithic linings for steel ladles are gaining preference over bricks due to faster installation and repair, while refractory performance in EAF steelmaking is a key focus area driving innovation in magnesia-carbon products.

- For the energy sector, insulating materials for petrochemical reformers are essential for thermal efficiency. The move to refractory solutions for alternative fuels in cement kilns presents new challenges for material durability. Emerging applications include advanced ceramics for energy storage and wear resistant linings for cement kilns designed for longer life.

- The market is also seeing specialized demand for non-wetting castables for aluminum smelting and specialized refractories for copper smelting. Technology is a key enabler, with predictive analytics for refractory wear and robotic gunning for furnace repair becoming standard. Sustainability is driving interest in recycled content in refractory bricks and low-carbon binders for castables.

- Other innovations include thermal shock resistant ladle shrouds, lightweight castables for furnace doors, smart refractories with embedded sensors, and chrome-free refractories for cement industry. Ensuring refractory compatibility with green hydrogen and developing high-emissivity coatings for furnace efficiency represent the next frontier.

- Adopting these technologies allows firms to extend maintenance cycles, in some cases doubling the time between major relines compared to legacy systems.

What are the key market drivers leading to the rise in the adoption of Refractory Materials Industry?

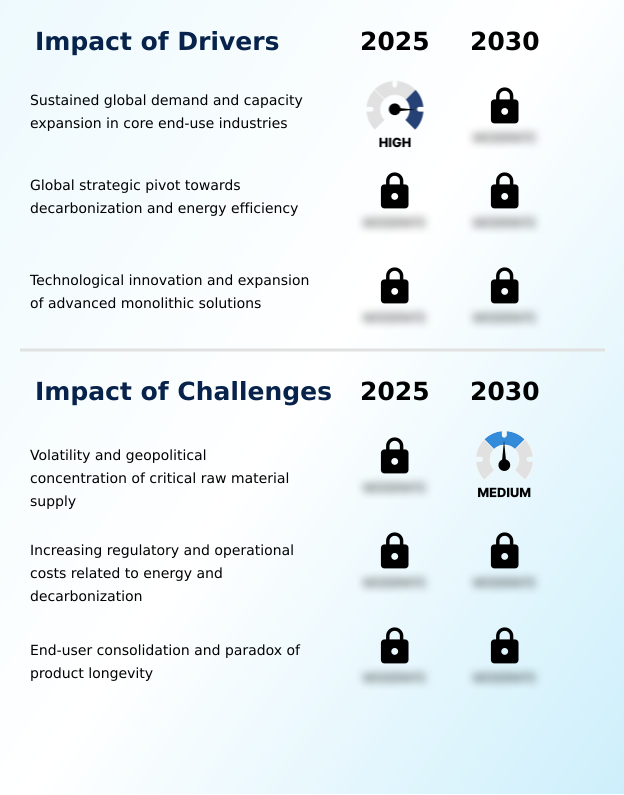

- Sustained global demand and strategic capacity expansion within core end-use industries, including steel and cement, represent the key driver for market growth.

- Sustained industrial output creates a non-negotiable cyclical demand for refractory materials, driving market expansion. The preference is shifting toward advanced solutions that offer superior slag erosion tolerance and operational efficiency.

- The adoption of robotic refractory installation for high-density gunning mixes has reduced application times by up to 40%, enhancing safety and consistency. Innovation in monolithic refractories, such as the non-cement refractory castable, is streamlining repair cycles.

- Furthermore, demand is growing for pre-cast refractory shapes and insulating firebrick based on the traditional alumina-silica system, which are integral to thermal efficiency optimization. This trend is underpinned by enhanced high-temperature process control across end-user industries.

What are the market trends shaping the Refractory Materials Industry?

- The market is defined by an accelerated shift toward digitalization and the integration of smart refractories. This trend is fundamentally reshaping competitive dynamics and value propositions for industrial end-users.

- The refractory materials market is rapidly evolving through digitalization and sustainability mandates. The adoption of smart refractories with embedded sensors is enabling advanced predictive refractory maintenance, improving asset reliability by over 30%. This shift supports the broader push for industrial decarbonization, where material selection is critical. Innovations in microporous insulation and silicon carbide castables are lowering energy consumption.

- At the same time, circular economy principles are driving the development of magnesia-carbon bricks with recycled content, enhancing supply chain resilience. High-performance monolithic refractories are increasingly specified for their superior thermal shock resistance, contributing to a market where technological value and lifecycle performance are paramount.

What challenges does the Refractory Materials Industry face during its growth?

- The volatility and geopolitical concentration inherent in critical raw material supply chains pose a significant structural challenge to the industry's growth and cost stability.

- The market faces significant headwinds from raw material volatility and evolving end-user demands. The supply of critical materials like dead burned magnesia and alumina-zirconia-silica remains geopolitically concentrated, leading to price instability. This affects the cost of high-performance products, including direct-bonded magnesia-chrome bricks and low-carbon resin-bonded mgo-c variants.

- Concurrently, the success of advanced materials is extending furnace campaign life by up to 15%, altering the traditional refractory relining cycle. This paradox challenges revenue models, pushing suppliers toward the cost-per-ton-of-steel model. Technical issues such as molten metal infiltration and hydrogen-induced degradation require constant innovation in calcium aluminate binders to meet new performance thresholds.

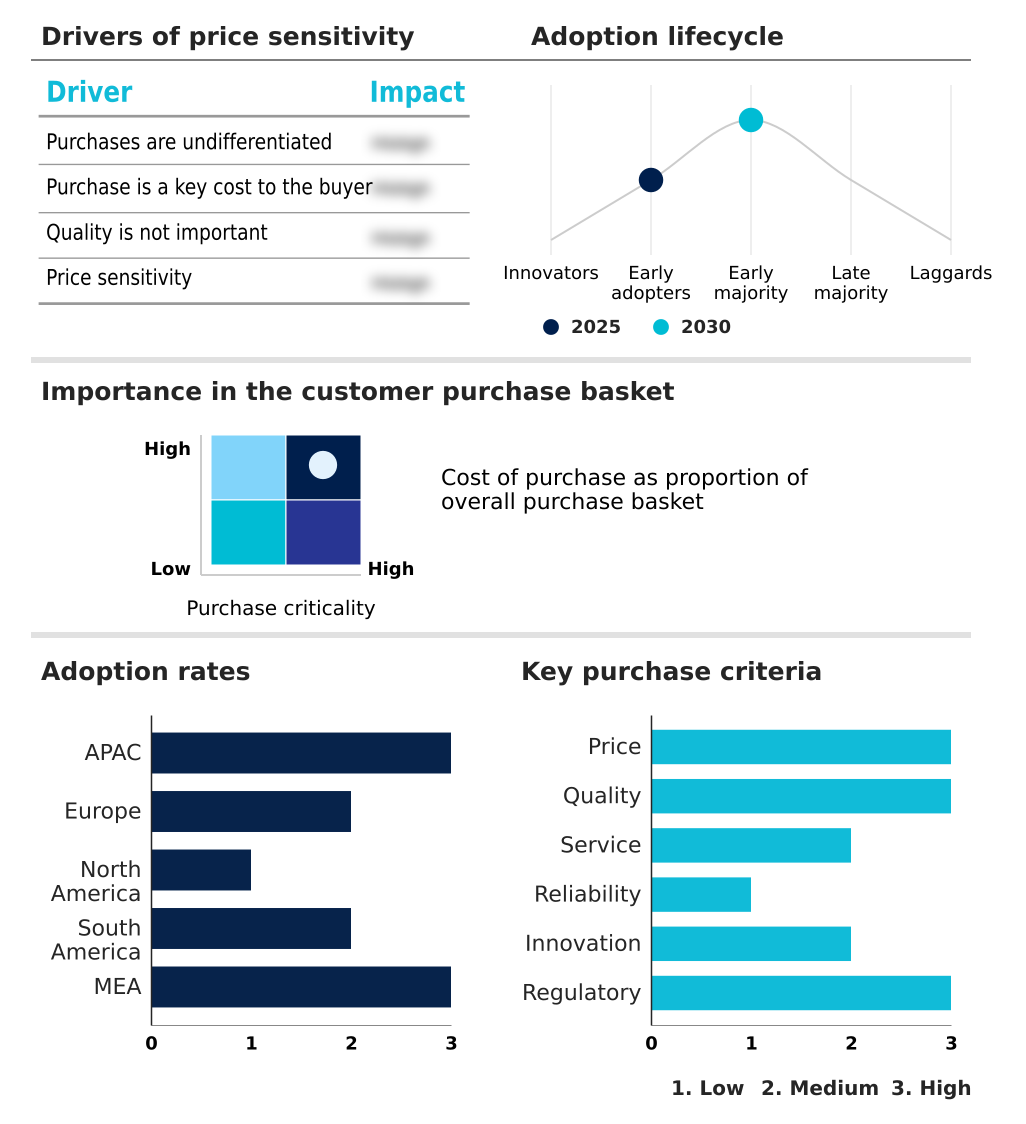

Exclusive Technavio Analysis on Customer Landscape

The refractory materials market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the refractory materials market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Refractory Materials Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, refractory materials market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Carborundum Universal - Offerings include a range of fired, monolithic, and super refractory materials providing high-temperature thermal insulation solutions for critical industrial processes in steel, cement, and glass manufacturing.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Carborundum Universal

- Compagnie de Saint Gobain SA

- Corning Inc.

- HarbisonWalker International

- IFGL Refractories Ltd.

- Imerys S.A.

- INTOCAST AG

- KAEFER SE and Co.

- Krosaki Harima Corp.

- Magnezit Group

- Minerals Technologies Inc.

- Morgan Advanced Materials

- Refratechnik Holding

- RHI Magnesita GmbH

- SCR Sibelco NV

- Shinagawa Refractories.

- Vesuvius Plc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Refractory materials market

- In March, 2025, RHI Magnesita finalized the integration of a newly acquired production facility in South America, strengthening its local presence and service capabilities for the region's steel and mining industries.

- In January, 2025, HarbisonWalker International (HWI) introduced a next-generation non-cement refractory castable with improved flow and shorter curing times, enhancing operational efficiency for steel ladle maintenance.

- In April, 2025, Imerys S.A. announced a breakthrough in high-purity calcium aluminate binder technology, enabling superior strength development in refractory castables at intermediate temperatures to extend service life.

- In May, 2025, Vesuvius Plc announced a strategic partnership with a global artificial intelligence software firm to integrate machine learning into its software for optimizing tundish lining life in continuous casting.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Refractory Materials Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 310 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.4% |

| Market growth 2026-2030 | USD 8484.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.3% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, Germany, France, UK, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The refractory materials market is defined by its critical role in enabling high-temperature industrial manufacturing and its ongoing technological evolution. Demand is increasingly shifting toward advanced materials that offer extended service life and support sustainability goals. The use of sophisticated monolithic refractories, including the non-cement refractory castable and ultra-low cement castables, is rising due to installation flexibility and superior performance.

- Core products like magnesia-carbon bricks and insulating firebrick from the alumina-silica system are being enhanced with new formulations, such as high-alumina compositions and advanced calcium aluminate binders. Specialized applications drive demand for fused-cast refractories, high-purity fused silica, and alumina-zirconia-silica in glassmaking, as well as direct-bonded magnesia-chrome and magnesia-spinel bricks in metallurgy.

- The transition to EAFs and new DRI processes propels innovation in low-carbon resin-bonded mgo-c and chemically bonded refractories. A key boardroom-level consideration is the shift to performance-based contracts, enabled by smart refractories with embedded sensors. This service model, leveraging microporous insulation and pre-cast refractory shapes, allows end-users to achieve verified reductions in energy consumption by up to 10%.

- This evolution demands continuous investment in materials like silicon carbide castables, high-density gunning mixes, and solutions for anode baking furnace linings, moving the industry from a product supplier to a service partner.

What are the Key Data Covered in this Refractory Materials Market Research and Growth Report?

-

What is the expected growth of the Refractory Materials Market between 2026 and 2030?

-

USD 8.48 billion, at a CAGR of 5.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product Type (Clay, Non-clay), Type (Shaped, Monolithic), Application (Iron and steel, Non-metallic materials, Non-ferrous metals, Others) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Sustained global demand and capacity expansion in core end-use industries, Volatility and geopolitical concentration of critical raw material supply

-

-

Who are the major players in the Refractory Materials Market?

-

Carborundum Universal, Compagnie de Saint Gobain SA, Corning Inc., HarbisonWalker International, IFGL Refractories Ltd., Imerys S.A., INTOCAST AG, KAEFER SE and Co., Krosaki Harima Corp., Magnezit Group, Minerals Technologies Inc., Morgan Advanced Materials, Refratechnik Holding, RHI Magnesita GmbH, SCR Sibelco NV, Shinagawa Refractories. and Vesuvius Plc

-

Market Research Insights

- The refractory materials market is characterized by a dynamic shift toward value-added solutions, driven by the need for enhanced thermal efficiency optimization and supply chain resilience. The adoption of circular economy principles is reshaping end-of-life material management, with some producers achieving a 20% reduction in embodied carbon by using innovative binders.

- As industries pursue industrial decarbonization, particularly in green steel production, demand for specialized materials with superior performance is increasing. This move toward high-performance solutions is changing procurement, with a notable shift toward the cost-per-ton-of-steel model that aligns supplier incentives with end-user productivity.

- The focus on extending furnace campaign life and improving predictive refractory maintenance has enabled some operators to reduce unscheduled downtime by over 30%, highlighting the market's transition to a service-oriented and technology-led ecosystem.

We can help! Our analysts can customize this refractory materials market research report to meet your requirements.

RIA -

RIA -