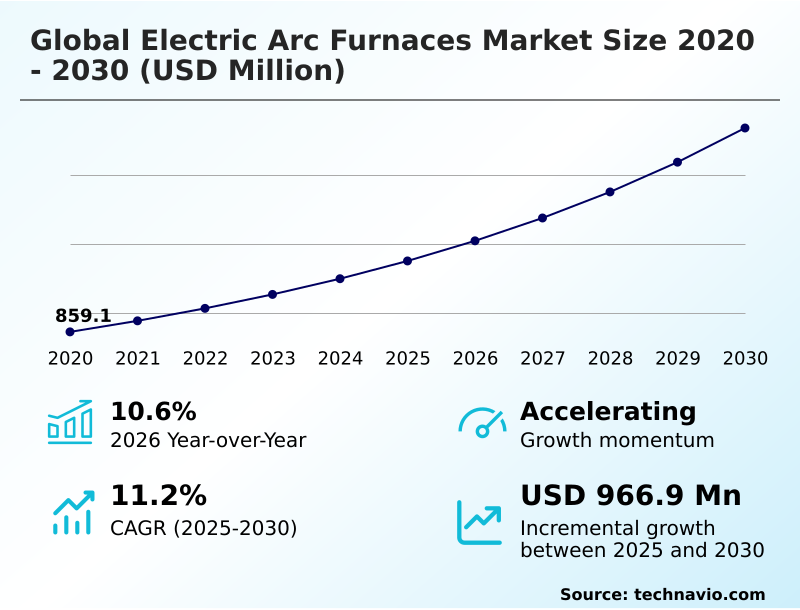

Electric Arc Furnaces Market Size 2026-2030

The electric arc furnaces market size is valued to increase by USD 966.9 million, at a CAGR of 11.2% from 2025 to 2030. Decarbonization in steel production and imperative for industrial decarbonization will drive the electric arc furnaces market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 67.1% growth during the forecast period.

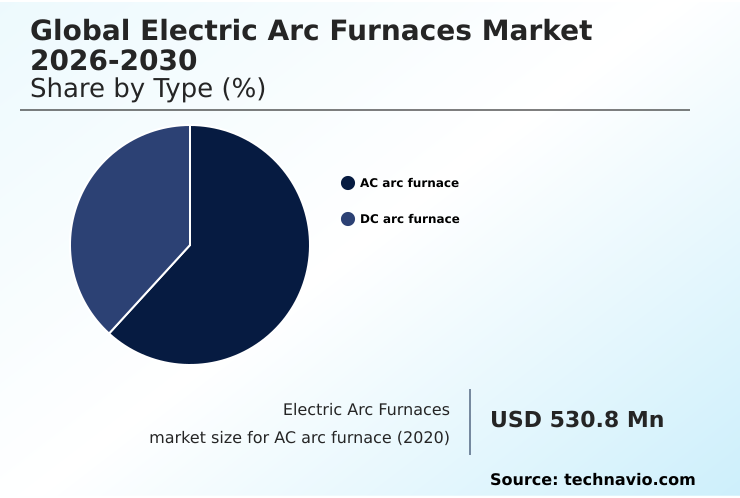

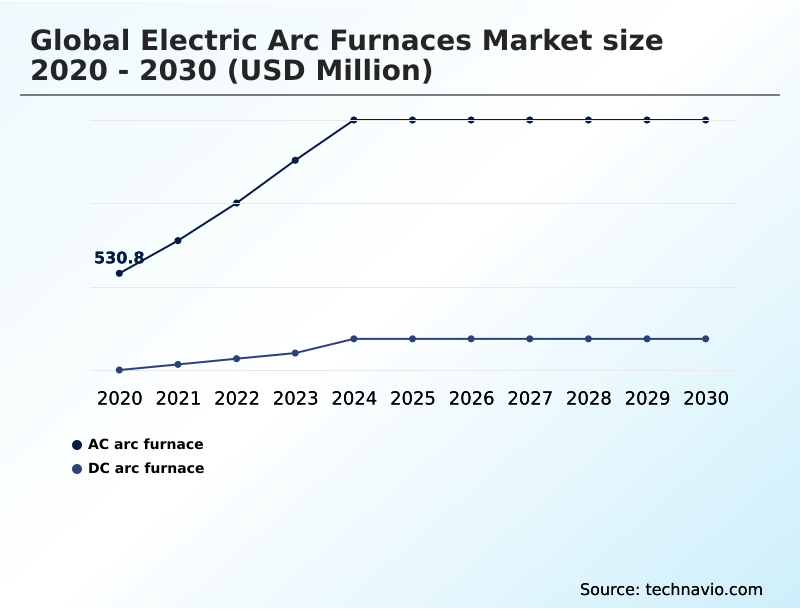

- By Type - AC arc furnace segment was valued at USD 852.1 million in 2024

- By Product - 100 to 200 tons segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1.48 billion

- Market Future Opportunities: USD 966.9 million

- CAGR from 2025 to 2030 : 11.2%

Market Summary

- The electric arc furnaces market is undergoing a significant transformation, driven by the steel industry's pivot toward sustainability and enhanced operational efficiency. This shift is characterized by a move away from carbon-intensive production methods in favor of technologies with a lower environmental footprint and greater feedstock flexibility.

- The increasing emphasis on decarbonization has emerged as a primary catalyst, compelling steelmakers to adopt cleaner production technologies like electric arc furnaces, which are central to the industry's circular economy ambitions. These furnaces primarily use recycled steel scrap, reducing reliance on virgin raw materials and associated carbon emissions.

- The economic advantages, including the use of cost-effective scrap, further bolster market appeal. A key business scenario involves steel producers leveraging the modular nature of EAF plants for scalable production, allowing them to dynamically respond to fluctuating market demands and optimize output.

- For instance, an operator might adjust production schedules to capitalize on off-peak electricity prices, a level of agility not possible with traditional furnaces. However, the market is not without challenges, such as the availability of high-quality scrap and the need for significant capital investment.

- The strategic decisions of key stakeholders are reshaping the competitive landscape and signaling the future direction of steelmaking.

What will be the Size of the Electric Arc Furnaces Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Electric Arc Furnaces Market Segmented?

The electric arc furnaces industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- AC arc furnace

- DC arc furnace

- Product

- 100 to 200 tons

- 200 to 300 tons

- More than 300 tons

- Upto 100 tons

- Application

- Ferrous metals

- Non-ferrous metals

- Geography

- APAC

- China

- India

- Japan

- Europe

- Germany

- Italy

- UK

- North America

- US

- Canada

- Mexico

- Middle East and Africa

- Saudi Arabia

- South Africa

- UAE

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- APAC

By Type Insights

The ac arc furnace segment is estimated to witness significant growth during the forecast period.

The AC arc furnace segment remains relevant for specific applications within the global electric arc furnaces market 2026-2030, largely due to lower initial capital expenditure for EAF compared to more advanced alternatives.

This makes it a viable choice for brownfield steel plant modernization projects where existing infrastructure, including high-power transformers and transformer vaults, is already configured for AC operation.

However, the technology faces challenges from higher minimill operational costs, notably increased consumption of graphite electrodes, which can be over 50% higher than in DC systems.

The significant electrical disturbance it creates often necessitates expensive flicker compensation equipment like a static var compensator.

This lack of eaf operational flexibility and higher energy consumption reduction potential in other systems tempers growth prospects, positioning it for niche replacement rather than new large-scale greenfield projects.

The AC arc furnace segment was valued at USD 852.1 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 67.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Electric Arc Furnaces Market Demand is Rising in APAC Get Free Sample

The geographic landscape is characterized by dual dynamics: massive capacity expansion in APAC, which accounts for over 67% of incremental growth, and strategic decarbonization projects in Europe and North America.

In developing regions, investment focuses on building new direct current arc furnace facilities to meet rising demand for construction materials.

In contrast, mature markets are driven by steel plant modernization, replacing aging assets with efficient furnaces capable of producing advanced steel grades and high-quality flat products. These upgrades can reduce tap-to-tap times by up to 15%, significantly boosting productivity.

Advanced eaf maintenance strategies and off-gas analysis are critical for optimizing metallic yield across all regions, while specialized applications like non-ferrous metal recycling using submerged arc furnace technology are also gaining traction.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the electric arc furnaces market involves a complex assessment of multiple operational and financial variables. A primary consideration is the ongoing debate regarding ac vs dc electric arc furnace efficiency, where the lower electrode consumption of DC systems is weighed against the higher capital cost.

- The impact of scrap quality on eaf operation is another critical factor, compelling producers to invest in technologies for reducing eaf electrode consumption or to refine their eaf process control for specialty steels. Many are now using direct reduced iron in electric arc furnaces to dilute contaminants and improve final product quality.

- A thorough cost-benefit analysis of eaf conversion from older technologies must account for future environmental regulations for eaf dust disposal, which can significantly influence long-term operational expenses. Optimizing eaf tap to tap time through automation and robotics in eaf operations is a key focus for enhancing throughput.

- Similarly, innovations in eaf refractory materials can extend campaign life by more than double the duration of conventional linings, directly impacting maintenance budgets. The role of eafs in green steel production is central to corporate strategy, driving investment in energy saving technologies for electric arc furnaces.

- Even for applications like eaf for non-ferrous metal smelting, the goals of improving metallic yield in electric steelmaking and feedstock flexibility in electric arc furnaces remain paramount.

- Other considerations include managing power grid flicker from ac arc furnaces, challenges of high-capacity electric arc furnaces, seamless eaf integration with continuous casting, the overall capital investment for minimill construction, and specific eaf application in steel foundries.

What are the key market drivers leading to the rise in the adoption of Electric Arc Furnaces Industry?

- The imperative for industrial decarbonization, particularly within steel production, is a key driver for the market.

- The imperative for industrial decarbonization is the primary driver propelling the market toward green steel production.

- The electric arc furnace is central to this shift, supporting a circular economy model by using steel recycling technology to create new products from scrap.

- This process, especially when enhanced with scrap preheating systems and oxy-fuel burners, significantly improves eaf environmental performance. Compared to traditional methods, the EAF route reduces the eaf carbon footprint by up to 75%.

- Furthermore, this technology provides a clear pathway for decarburization, aligning with stringent emissions targets.

- Effective hazardous waste management through advanced eaf dust treatment techniques further solidifies the EAF's role as the preferred technology for sustainable steelmaking, making it a cornerstone of green steel pathways.

What are the market trends shaping the Electric Arc Furnaces Industry?

- A growing emphasis on circular economy principles is a key market trend. This is coupled with enhanced scrap metal availability, which supports the expansion of recycling-based steel production.

- The integration of steel industry 4.0 and smart furnace technologies is fundamentally redefining operational efficiency. Advanced furnace automation systems and sophisticated electrode regulation enable ultra high power operation while optimizing power consumption. Through predictive maintenance in EAF, operators can increase furnace availability by up to 15%.

- Digital twin simulation allows for the risk-free testing of new process parameters for specialty alloy production, while robotic sampling enhances safety and consistency. This data-driven approach, powered by advanced process control, improves key metrics, with some facilities reporting eaf productivity improvements of over 10% by minimizing unplanned downtime and enhancing the lifespan of components like water-cooled panels.

What challenges does the Electric Arc Furnaces Industry face during its growth?

- The high initial capital investment required for new facilities presents a formidable barrier to market entry and is a key challenge affecting industry growth.

- Raw material price volatility and inconsistent eaf feedstock quality present significant operational challenges. Price swings in scrap can alter production costs by over 20% in a single quarter, impacting profitability. The presence of undesirable tramp elements necessitates sophisticated scrap yard processing using sensor-based sorting or blending with premium alternative iron units like direct reduced iron and hot briquetted iron.

- Additionally, the high capital expenditure for EAF installations, including the refractory lined vessel and ancillary systems like a ladle furnace and continuous casting equipment, creates a formidable barrier to entry. These upfront costs, coupled with ongoing regulatory compliance costs for operations, require careful financial planning and risk management.

Exclusive Technavio Analysis on Customer Landscape

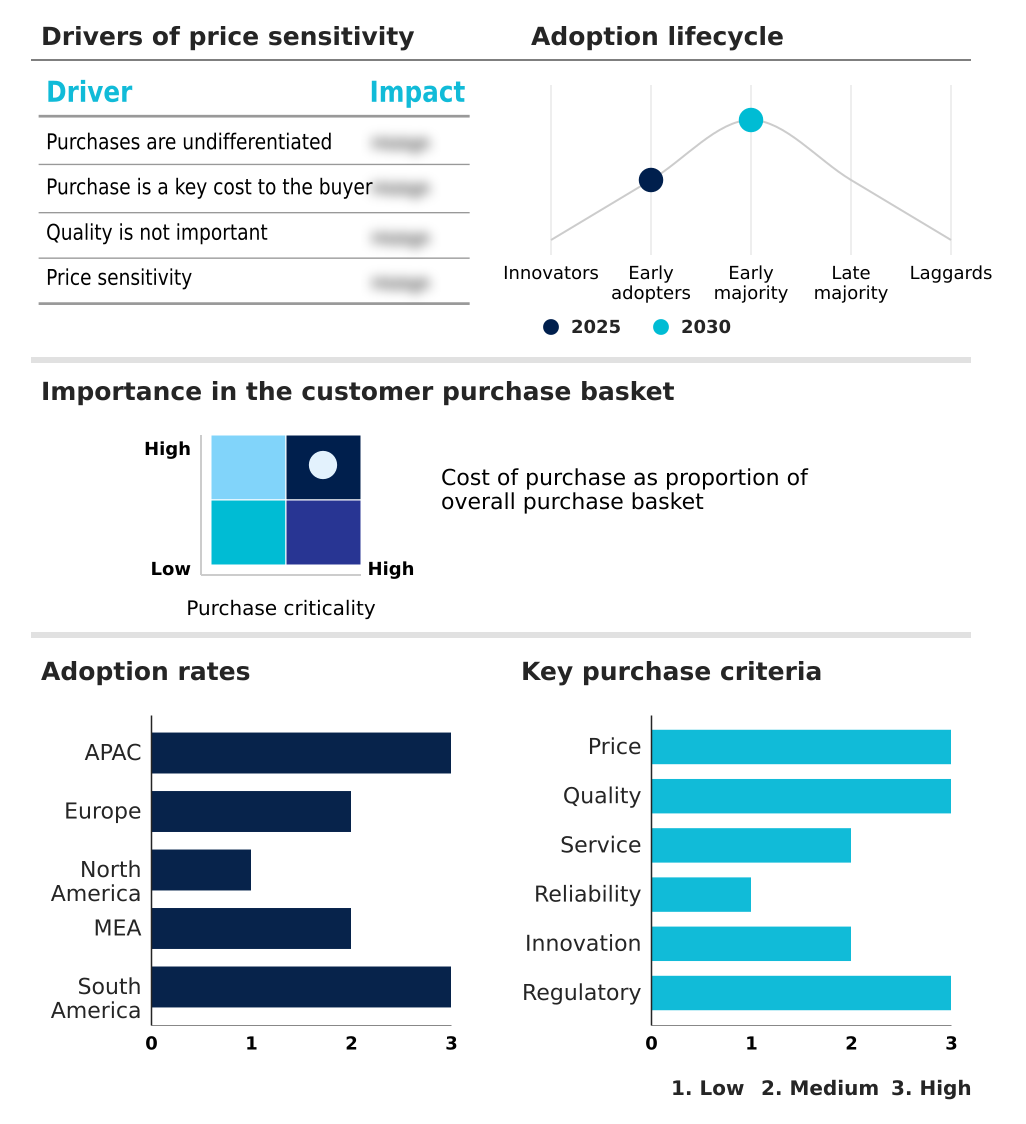

The electric arc furnaces market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the electric arc furnaces market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Electric Arc Furnaces Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, electric arc furnaces market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

CISDI Group Co. Ltd. - Advanced electric arc furnace solutions are enabling steelmakers to process flexible feedstock mixes, aligning with long-term carbon neutrality goals and enhancing operational efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- CISDI Group Co. Ltd.

- Comeca Tecnologie SpA

- Daido Steel Co. Ltd.

- Danieli and C. Officine SpA

- Electrotherm Ltd.

- Epcon Industrial Systems LP

- GHI Smart Furnaces

- INTECO Melting Casting GmbH

- JFE Engineering Corp.

- Mitsubishi Heavy Industries

- Nidec ASI SpA

- Primetals Technologies Ltd.

- Sarralle

- Siemens AG

- SMS group GmbH

- Taoyuan Metallurgical Co. Ltd.

- Tenova SpA

- The Rose Corp.

- Whiting Equipment Canada Inc.

- Xiye Metallurgy Technology Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Electric arc furnaces market

- In August 2025, Rayanco announced it is building Saudi Arabia's first electric arc furnace steel billet plant in Dammam, with an initial annual capacity of 150,000 tons and scheduled to start operations in mid-2026.

- In May 2025, ArcelorMittal announced its intention to build a new electric arc furnace in Dunkirk, France, with an estimated investment of $1.2 billion, as a cornerstone of its decarbonization strategy in Europe.

- In April 2025, JFE Steel announced its plan to invest in a new, advanced, and large-scale electric arc furnace at its Kurashiki facility in Japan to produce high-grade steel products for advanced manufacturing sectors.

- In October 2024, SMS group GmbH detailed its contract to supply a 185-ton AC Electric Arc Furnace to Saarstahl in Volklingen, Germany, designed to process a flexible mix of scrap and Cold Direct Reduced Iron.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Electric Arc Furnaces Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 300 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 11.2% |

| Market growth 2026-2030 | USD 966.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 10.6% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, Germany, Russia, Italy, UK, Spain, The Netherlands, US, Canada, Mexico, Saudi Arabia, South Africa, UAE, Israel, Turkey, Argentina, Brazil and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The electric arc furnaces market is defined by relentless technological advancement aimed at maximizing efficiency and sustainability. Central to modern operations is the sophisticated interplay between components like the refractory lined vessel, water-cooled panels, and the single conductive furnace bottom of a direct current arc furnace.

- The goal is to achieve shorter tap-to-tap times and higher metallic yield through precise electrode regulation and optimized power input profiles. A key trend driving boardroom decisions is the push for green steel production, where the circular economy model is realized through the use of feedstocks like direct reduced iron and hot briquetted iron.

- This strategy is not just about emissions; it's about market positioning and ESG compliance. Furnace automation systems, incorporating robotic sampling and advanced process control, are becoming standard. The implementation of digital twin simulation for operator training has been shown to reduce critical process errors by over 25% in initial production runs.

- Technologies such as scrap preheating systems, off-gas analysis, and advanced eaf dust treatment are crucial for minimizing environmental impact and operational costs, while developments in secondary metallurgy and continuous casting ensure final product quality.

What are the Key Data Covered in this Electric Arc Furnaces Market Research and Growth Report?

-

What is the expected growth of the Electric Arc Furnaces Market between 2026 and 2030?

-

USD 966.9 million, at a CAGR of 11.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (AC arc furnace, and DC arc furnace), Product (100 to 200 tons, 200 to 300 tons, More than 300 tons, and Upto 100 tons), Application (Ferrous metals, and Non-ferrous metals) and Geography (APAC, Europe, North America, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Decarbonization in steel production and imperative for industrial decarbonization, High initial capital investment as formidable barrier to market entry

-

-

Who are the major players in the Electric Arc Furnaces Market?

-

CISDI Group Co. Ltd., Comeca Tecnologie SpA, Daido Steel Co. Ltd., Danieli and C. Officine SpA, Electrotherm Ltd., Epcon Industrial Systems LP, GHI Smart Furnaces, INTECO Melting Casting GmbH, JFE Engineering Corp., Mitsubishi Heavy Industries, Nidec ASI SpA, Primetals Technologies Ltd., Sarralle, Siemens AG, SMS group GmbH, Taoyuan Metallurgical Co. Ltd., Tenova SpA, The Rose Corp., Whiting Equipment Canada Inc. and Xiye Metallurgy Technology Co.

-

Market Research Insights

- The electric arc furnaces market is defined by a strategic push toward enhancing eaf productivity improvements and achieving greater eaf operational flexibility. Steelmakers are increasingly adopting advanced systems that improve electric steelmaking efficiency, with some modernizations leading to a 10% reduction in overall energy consumption.

- This focus is driven by the need to mitigate the impact of raw material price volatility and reduce minimill operational costs. Furthermore, adherence to stringent environmental standards necessitates investments that lower the eaf carbon footprint, with advanced technologies now enabling a reduction in specific emissions by over 15%.

- This alignment with regulatory compliance costs and sustainability goals is reshaping investment strategies across the sector, favoring technologies that offer both economic and environmental benefits, thereby supporting long-term steel plant modernization efforts.

We can help! Our analysts can customize this electric arc furnaces market research report to meet your requirements.

RIA -

RIA -