Residential And Commercial Security Market Size 2026-2030

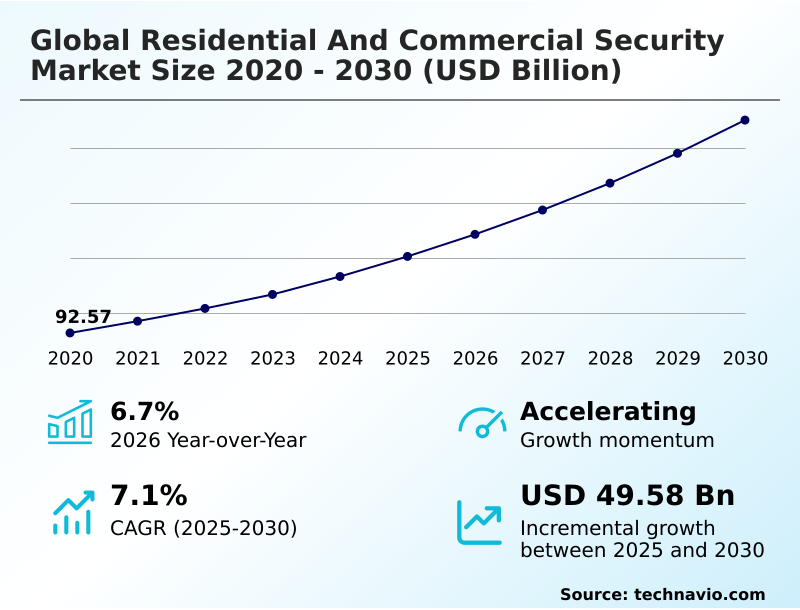

The residential and commercial security market size is valued to increase by USD 49.58 billion, at a CAGR of 7.1% from 2025 to 2030. Rising consumer awareness of fire safety and regulatory compliance mandates will drive the residential and commercial security market.

Major Market Trends & Insights

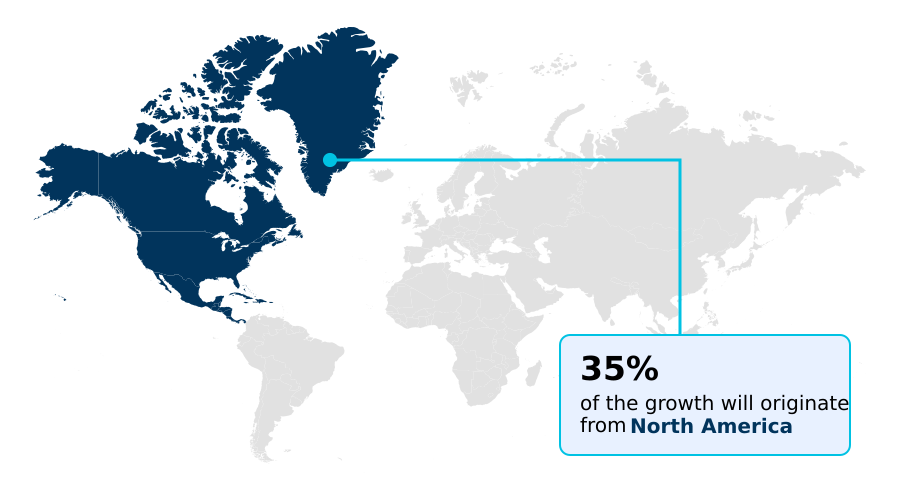

- North America dominated the market and accounted for a 35.4% growth during the forecast period.

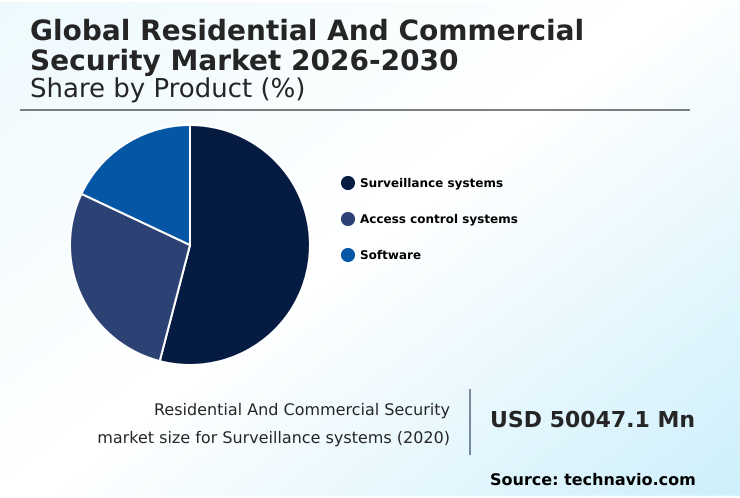

- By Product - Surveillance systems segment was valued at USD 61.30 billion in 2024

- By Technology - Wired systems segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 77.40 billion

- Market Future Opportunities: USD 49.58 billion

- CAGR from 2025 to 2030 : 7.1%

Market Summary

- The residential and commercial security market is undergoing a significant transformation, moving beyond traditional intrusion detection systems to comprehensive, integrated security ecosystems. This evolution is driven by the convergence of physical and digital security, where IP-based surveillance and electronic access control are now standard.

- The adoption of smart home security and smart building technologies is accelerating, with devices like smart video doorbells and mobile credentialing becoming commonplace. A key dynamic is the shift to proactive security postures, enabled by AI-powered video analytics that can identify threats in real time.

- For instance, a retail enterprise can deploy a unified security platform not just for loss prevention strategies but also for business intelligence gathering, analyzing customer traffic to optimize store layouts. However, this increased connectivity introduces significant cybersecurity vulnerabilities, demanding robust network security solutions and encrypted communications to protect against data breaches.

- The market is also seeing a move toward SaaS security models and professional monitoring services that offer recurring revenue models and greater flexibility than managing on-premises hardware, ensuring operational resilience and asset protection.

What will be the Size of the Residential And Commercial Security Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Residential And Commercial Security Market Segmented?

The residential and commercial security industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

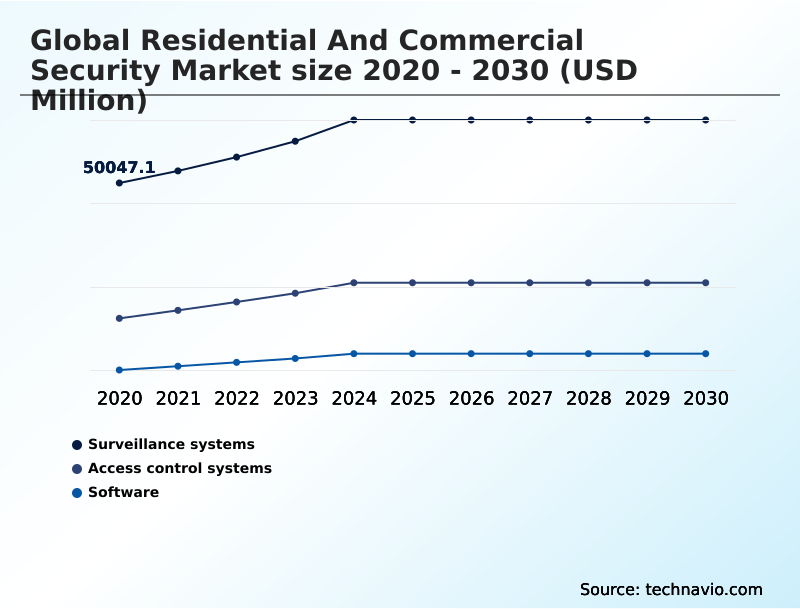

- Product

- Surveillance systems

- Access control systems

- Software

- Technology

- Wired systems

- Wireless systems

- Cloud-based solutions

- AI and analytics

- Type

- New installations

- Retrofit installations

- Portable systems

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Product Insights

The surveillance systems segment is estimated to witness significant growth during the forecast period.

The global residential and commercial security market is segmented by product into surveillance systems, access control systems, and software. The surveillance systems segment is foundational, driven by a persistent need for threat deterrence and post-event investigation.

This segment is defined by a market-wide transition from analog to network-based digital systems, which offer superior image quality and integration potential.

Key trends include the embedding of analytical capabilities, such as motion detection and behavioral analysis, directly into hardware and software, transforming passive video into actionable intelligence.

This shift toward intelligent surveillance, utilizing AI-powered video analytics and video management systems, allows organizations to reduce false alarms by over 45%, enhancing the proactive security posture for both residential and commercial applications and improving overall situational awareness.

The Surveillance systems segment was valued at USD 61.30 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Residential And Commercial Security Market Demand is Rising in North America Get Free Sample

The geographic landscape of the residential and commercial security market is characterized by distinct regional dynamics, with North America and APAC driving a majority of the growth.

North America is projected to contribute over 35% of the market's incremental growth, fueled by high adoption rates of smart home security, smart building technologies, and cloud-based video surveillance. This region's mature market prioritizes technology upgrades and SaaS security models.

In contrast, APAC is the fastest-growing region, with its 7.3% growth rate driven by massive infrastructure development and government-led smart city initiatives. This creates substantial demand for new installations of IP-based surveillance, unified security platforms, and electronic access control systems.

While Europe focuses on regulatory compliance and data privacy regulations, emerging markets in South America and the Middle East prioritize asset protection and operational resilience amid rapid urbanization.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic discourse in the residential and commercial security market increasingly revolves around a few critical technology debates. The benefits of edge computing in surveillance are now widely recognized for enabling faster, localized analytics, which directly addresses the role of AI in reducing security false alarms.

- This is compelling organizations to establish cybersecurity best practices for IP cameras to protect these distributed intelligent nodes. Concurrently, a major operational shift is evident in access control, with many evaluating mobile credentialing versus traditional access cards for enhanced convenience and security.

- The underlying technology is also evolving, with a strong push for open-source protocols for security interoperability to break down proprietary silos. This move is crucial for integrating fire safety with smart security, creating truly unified systems.

- However, the impact of GDPR on video surveillance storage continues to shape cloud architecture and data retention policies, especially when comparing SaaS vs on-premise security software. Businesses are finding that investments in IP-based surveillance for commercial properties yield a significantly higher return when part of a holistic strategy.

- For smaller entities, cloud-based video surveillance for small business offers an accessible entry point. Ultimately, the cost analysis of retrofit security installations versus new builds often favors modern, integrated approaches, especially when considering the long-term value of real-time threat processing with AI analytics and the benefits of unified physical security platforms.

What are the key market drivers leading to the rise in the adoption of Residential And Commercial Security Industry?

- A key market driver is the growing emphasis on fire protection and safety regulations, coupled with rising consumer awareness and compliance mandates.

- The market's expansion is significantly propelled by the increasing penetration of smart home technologies, including user-friendly wireless products and smart video doorbells, which have lowered the barrier to entry for many households.

- Modernization of commercial infrastructure is another key driver, with businesses moving from legacy systems to advanced IP-based surveillance and biometric access control to enable better loss prevention strategies and business intelligence gathering.

- Retailers leveraging security data for operational insights have reported a 5% uplift in efficiency. Furthermore, stringent fire safety regulations and compliance mandates are a fundamental catalyst for growth.

- These regulations, which often require professionally installed fire and life safety monitoring, drive a consistent 15% of new installation projects, ensuring a stable demand for high-quality hardware and professional monitoring in both residential and commercial sectors.

What are the market trends shaping the Residential And Commercial Security Industry?

- The institutionalization of edge computing is a significant trend, enabling real-time threat processing directly within security hardware. This shift allows for faster analysis and response without cloud latency.

- A significant trend reshaping the security market is the institutionalization of edge computing, which facilitates real-time threat processing directly within hardware. This allows systems to analyze data and trigger automated deterrence actions near-instantaneously, a critical capability for commercial facilities that can process threat data up to 95% faster than cloud-dependent models.

- This trend is complemented by the move toward universal interoperability, driven by open-source communication protocols that foster a more competitive and innovative environment. Another dominant trend is the rise of frictionless access control and mobile credentialing, which are becoming standard in modern buildings.

- The adoption of these touchless access technologies eliminates risks associated with physical cards and offers enhanced flexibility through remote system configuration. Adoption has accelerated, reducing physical card management costs by over 50% for many early adopters.

What challenges does the Residential And Commercial Security Industry face during its growth?

- A significant challenge affecting industry growth is the complexity of achieving interoperability and integrating modern security solutions with existing legacy systems.

- A significant challenge involves the complexity of legacy system integration, where connecting modern IP-based surveillance with entrenched analog hardware can increase project timelines by up to 40%. This fragmentation is compounded by a lack of universal interoperability, often forcing users into proprietary ecosystems.

- As the market migrates toward cloud-based management and IoT, it faces escalating cybersecurity vulnerabilities and stringent data privacy regulations. The cost of a single cybersecurity breach on a connected security network now frequently exceeds the initial system investment for small and medium-sized businesses.

- Finally, the prohibitive initial capital expenditure for advanced on-premises hardware and ongoing maintenance serves as a formidable barrier, particularly in emerging markets, inhibiting the transition away from basic security measures.

Exclusive Technavio Analysis on Customer Landscape

The residential and commercial security market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the residential and commercial security market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Residential And Commercial Security Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, residential and commercial security market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alarm.com Holdings Inc. - Delivering integrated, cloud-native platforms for interactive security, video monitoring, and smart automation to residential and commercial markets.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alarm.com Holdings Inc.

- Allegion Public Ltd. Co.

- Arlo Technologies Inc.

- ASSA ABLOY AB

- Brivo Inc.

- Dahua Technology Co. Ltd.

- Gallagher Group Ltd.

- Genetec Inc.

- Hangzhou Hikvision Digital

- Hanwha Vision Co. Ltd.

- Honeywell International Inc.

- i PRO Co. Ltd.

- Johnson Controls International

- Motorola Solutions Inc.

- Napco Security Technologies Inc.

- Resideo Technologies Inc.

- Robert Bosch GmbH

- Securitas AB

- Siemens AG

- Verkada Inc.

- VIVOTEK Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Residential and commercial security market

- In May 2025, ASSA ABLOY AB completed its acquisition of the Hardware and Home Improvement division from Spectrum Brands, a strategic move to significantly expand its portfolio of residential locks and smart home access solutions.

- In February 2025, Honeywell International Inc. finalized its acquisition of Carrier Global's Access Solutions business, integrating several prominent security and access control brands under its unified cloud platform to strengthen its building technologies segment.

- In January 2025, Johnson Controls International acquired Webeasy, a specialist in building automation and IoT solutions, to enhance its proprietary smart building control systems and further integrate security with overall facility management.

- In November 2024, Motorola Solutions Inc. acquired Blue Eye, an AI-powered remote video monitoring company, to bolster its command center software ecosystem with intelligent, real-time threat detection and response orchestration capabilities.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Residential And Commercial Security Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.1% |

| Market growth 2026-2030 | USD 49580.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.7% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The residential and commercial security market is defined by its transition toward intelligent and interconnected systems. The core of this evolution lies in the adoption of unified security platforms that merge previously disparate functions like IP-based surveillance, biometric access control, and fire and life safety monitoring.

- This integration is powered by AI-powered video analytics and sophisticated command and control software, shifting the industry from a reactive to a proactive security posture. The deployment of edge computing is accelerating this trend by enabling real-time analysis directly on devices like network cameras.

- A key boardroom consideration is the investment in cybersecurity for these newly connected physical security systems, as each device represents a potential network vulnerability. Organizations that leverage advanced video verification and video management systems have demonstrated the ability to reduce incident investigation times by as much as 60%.

- This technological shift is also reshaping business models, with a clear migration from reliance on on-premises hardware to scalable SaaS security models and remote monitoring services that provide continuous value and system oversight.

What are the Key Data Covered in this Residential And Commercial Security Market Research and Growth Report?

-

What is the expected growth of the Residential And Commercial Security Market between 2026 and 2030?

-

USD 49.58 billion, at a CAGR of 7.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Surveillance systems, Access control systems, and Software), Technology (Wired systems, Wireless systems, Cloud-based solutions, and AI and analytics), Type (New installations, Retrofit installations, and Portable systems) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Rising consumer awareness of fire safety and regulatory compliance mandates, Heightened interoperability obstacles and legacy system integration

-

-

Who are the major players in the Residential And Commercial Security Market?

-

Alarm.com Holdings Inc., Allegion Public Ltd. Co., Arlo Technologies Inc., ASSA ABLOY AB, Brivo Inc., Dahua Technology Co. Ltd., Gallagher Group Ltd., Genetec Inc., Hangzhou Hikvision Digital, Hanwha Vision Co. Ltd., Honeywell International Inc., i PRO Co. Ltd., Johnson Controls International, Motorola Solutions Inc., Napco Security Technologies Inc., Resideo Technologies Inc., Robert Bosch GmbH, Securitas AB, Siemens AG, Verkada Inc. and VIVOTEK Inc.

-

Market Research Insights

- The market's dynamic is increasingly shaped by a shift toward service-based, recurring revenue models and the strategic adoption of open-source communication protocols. These protocols have been shown to reduce integration costs by up to 25%, fostering universal interoperability and allowing end-users to build more flexible integrated security ecosystems.

- The focus on proactive security postures, supported by real-time threat processing, is delivering measurable results; firms adopting these advanced frameworks report up to a 40% faster response to critical incidents.

- This evolution is compelling providers to move beyond hardware sales and focus on delivering value through centralized cloud management, remote system configuration, and advanced video analytics software, ensuring sustained operational resilience for clients.

We can help! Our analysts can customize this residential and commercial security market research report to meet your requirements.

RIA -

RIA -