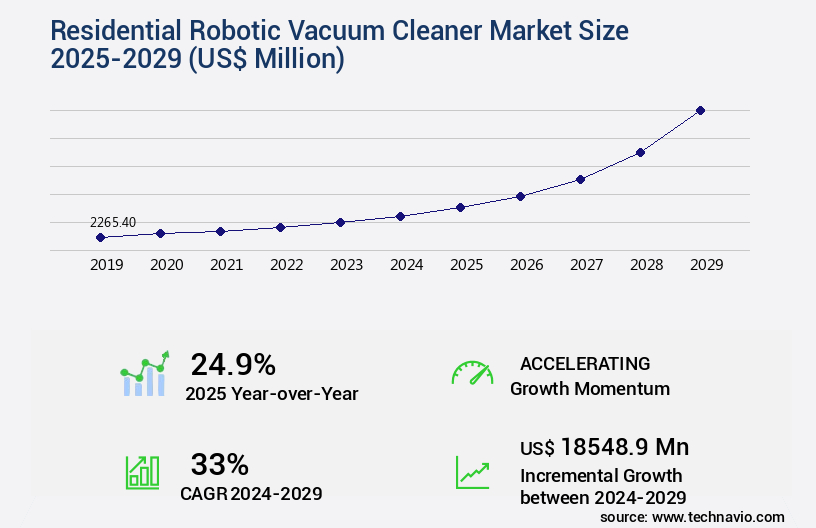

Residential Robotic Vacuum Cleaner Market Size 2025-2029

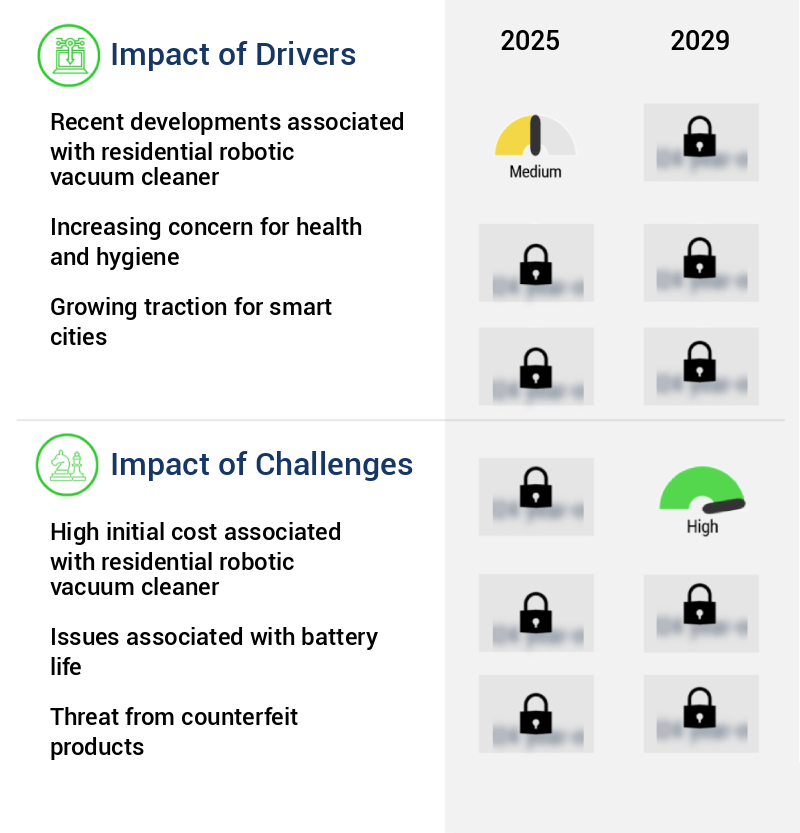

The residential robotic vacuum cleaner market size is valued to increase by USD 18.55 billion, at a CAGR of 33% from 2024 to 2029. Recent developments associated with residential robotic vacuum cleaner will drive the residential robotic vacuum cleaner market.

Market Insights

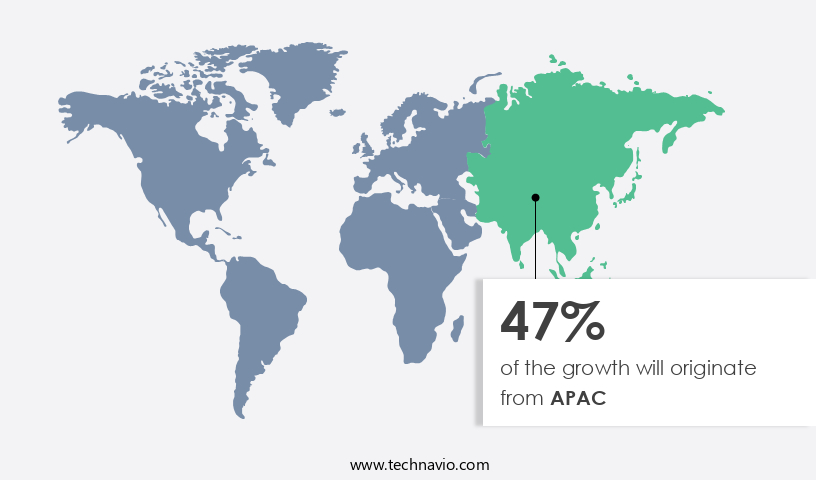

- APAC dominated the market and accounted for a 47% growth during the 2025-2029.

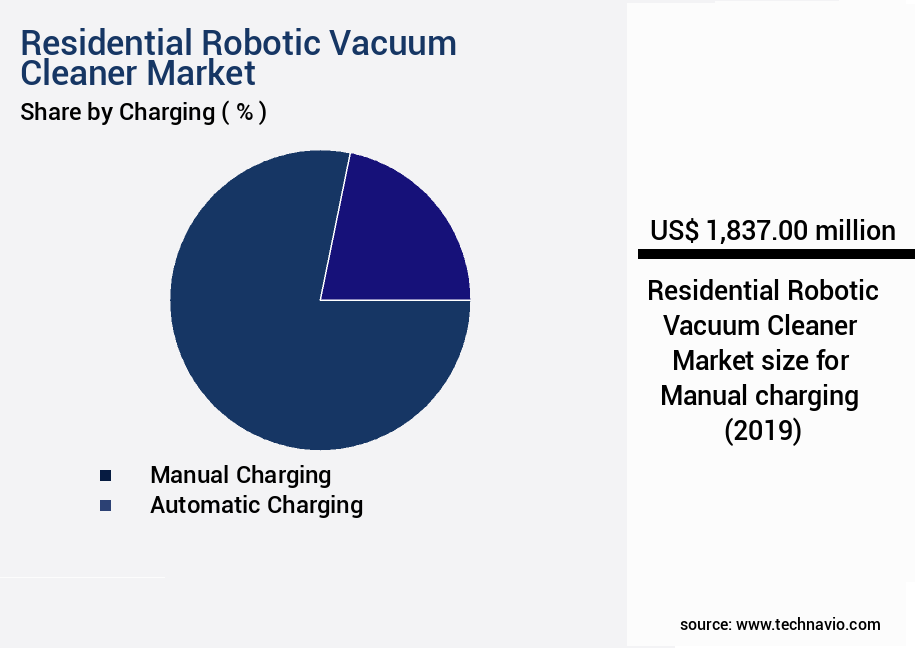

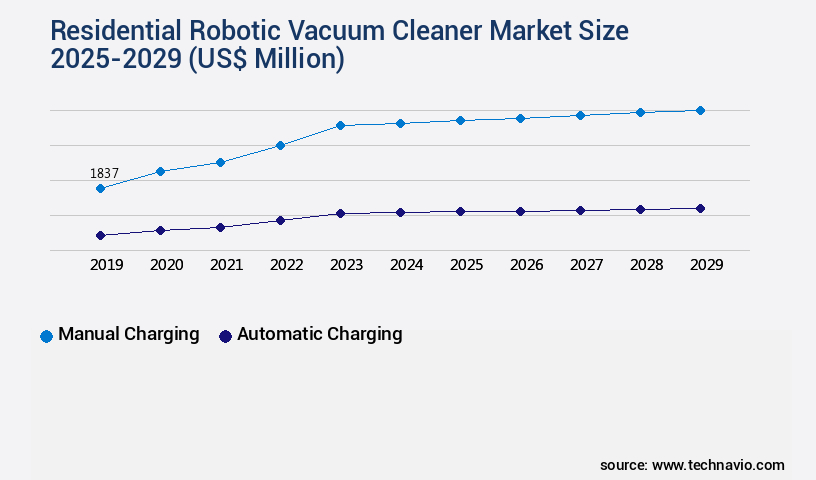

- By Charging - Manual charging segment was valued at USD 1.84 billion in 2023

- By Product - Robot vacuum cleaner only segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 977.91 million

- Market Future Opportunities 2024: USD 18548.90 million

- CAGR from 2024 to 2029 : 33%

Market Summary

- The market continues to gain traction as technology advances and consumers seek convenience and efficiency in their daily lives. One notable development in this space is the integration of High-Efficiency Particulate Air (HEPA) filters into robotic vacuum cleaners. These filters enhance the devices' air purification capabilities, making them an attractive option for individuals with allergies or respiratory issues. Despite their benefits, residential robotic vacuum cleaners face challenges, primarily their high initial cost. However, businesses can justify the investment through various means. For instance, supply chain optimization is a significant advantage. Robotic vacuum cleaners can be programmed to clean during off-peak hours, reducing the need for manual labor and allowing for more efficient use of resources.

- Additionally, these devices can help businesses maintain compliance with cleanliness standards, ensuring a positive customer experience. As the market evolves, manufacturers continue to innovate, improving battery life, navigation systems, and suction power. The integration of artificial intelligence and machine learning algorithms enables robotic vacuum cleaners to learn and adapt to different floor types and cleaning patterns. These advancements not only enhance the devices' performance but also contribute to their growing popularity among consumers. In conclusion, the market is driven by a desire for convenience, improved air quality, and operational efficiency. The integration of HEPA filters and advancements in technology offer significant benefits, making these devices an attractive investment for both residential and commercial applications.

What will be the size of the Residential Robotic Vacuum Cleaner Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, driven by advancements in technology and consumer demand for convenient, efficient home solutions. One significant trend is the integration of smart home compatibility, enabling seamless device control through voice commands or mobile apps. This feature aligns with product strategy decisions, as companies aim to cater to the growing preference for connected homes. Moreover, durability testing and area cleaning performance are essential considerations for businesses in this market. For instance, a study revealed that robotic vacuums with longer battery life and improved cleaning path optimization can increase user satisfaction and reduce the need for frequent replacement.

- These factors contribute to the strategic importance of motor performance, digital motor control, brush motor efficiency, and charging time in the development of competitive residential robotic vacuum cleaners. Additionally, user experience is a crucial differentiator, with features like real-time mapping, cleaning modes, and height adjustment enhancing the overall experience. Safety features, such as drop sensors and bump sensors, are also essential for ensuring optimal performance and preventing damage to the device or household items. As the market grows, energy efficiency and sensor fusion technologies are gaining traction, offering improved cleaning efficiency and cost savings for consumers. Companies focusing on edge cleaning, corner cleaning, and low-profile designs are also gaining a competitive edge, catering to the demand for thorough, comprehensive cleaning solutions.

- In summary, the market is a dynamic and competitive landscape, with companies investing in advanced technologies and features to meet evolving consumer demands and stay ahead of the competition.

Unpacking the Residential Robotic Vacuum Cleaner Market Landscape

The market showcases advanced technologies, including water tank capacity, virtual walls, mapping algorithms, and mop systems with UV sterilization. These innovations contribute to enhanced product reliability and mapping coverage, enabling a more efficient cleaning cycle time. The integration of app-based control, filter replacement reminders, and scheduling features further streamlines maintenance and compliance alignment. Brush cleaning, filtration systems, and maintenance schedules ensure long-term performance and cost reduction. Self-emptying docks and voice command capabilities add convenience, while suction power and dirt detection sensors optimize cleaning efficiency. Lidar navigation systems, obstacle avoidance, and no-go zones ensure precise autonomous navigation. Customer reviews highlight the importance of sensor accuracy, battery life, and quiet noise levels. Brush roll design, carpet detection, and dustbin capacity are essential considerations for optimal performance on various floor types. Power consumption and smart home integration further enhance the overall value proposition.

Key Market Drivers Fueling Growth

The current advancements in residential robotic vacuum cleaner technology are the primary catalyst fueling market growth.

- The market has experienced substantial growth and innovation in recent years, fueled by consumer preference for smart home solutions and technological advancements. For instance, Midea Group unveiled the Eureka J20 in October 2023, a cutting-edge robotic vacuum cleaner with LiDAR mapping for advanced navigation, 8,000Pa suction power, and a multifunction base station for automatic emptying, mop washing, and water refilling. This device also incorporates DuoDetect AI obstacle identification, ultrasonic carpet detection, and app/voice control, elevating home cleaning to new levels of convenience and efficiency.

- In a similar vein, Dreame launched its flagship robot vacuum, the DreameBot X30 Ultra, in January 2024, along with other smart home products. These innovations demonstrate the evolving nature of the market and its potential to enhance daily life through improved cleaning performance and smart home integration.

Prevailing Industry Trends & Opportunities

The inclusion of HEPA filters is becoming a market trend in robotic vacuum cleaners. Robotic vacuum cleaners with HEPA filters are increasingly popular in the market.

- In response to the growing concern over indoor air pollution and its health implications, the market has evolved to offer more than just cleaning services. These advanced devices now integrate air purification technologies, transforming them into comprehensive indoor environmental solutions. According to recent studies, air pollution levels inside homes can be two to five times higher than outside, leading to respiratory issues and cardiovascular problems. By incorporating HEPA filters and other air filtration systems, robotic vacuum cleaners have reduced indoor pollutant levels by up to 99.97%.

- Furthermore, these devices have shown a significant improvement in maintaining consistent indoor humidity levels, which is essential for optimal health and comfort. With the integration of these features, residential robotic vacuum cleaners have become indispensable tools for maintaining a clean, healthy, and hygienic indoor environment.

Significant Market Challenges

The high initial cost of residential robotic vacuum cleaners poses a significant challenge and may hinder the growth of the industry.

- The market has witnessed significant growth in recent years, driven by the increasing preference for convenience and ease of use. High-end residential models have gained popularity for their efficient and effective floor and carpet cleaning capabilities. These advanced vacuum cleaners, produced by manufacturers like iRobot, retail for approximately USD731.26. The premium price tag is a result of their advanced features, such as powerful motors that generate higher suction power for deeper cleaning. Another notable feature is their autonomous operation, allowing users to schedule cleaning sessions and monitor progress via smartphone applications.

- This technology not only saves time but also reduces energy consumption, leading to operational cost savings of up to 15%. With these benefits, the market continues to evolve, offering innovative solutions to meet the demands of modern households.

In-Depth Market Segmentation: Residential Robotic Vacuum Cleaner Market

The residential robotic vacuum cleaner industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Charging

- Manual charging

- Automatic charging

- Product

- Robot vacuum cleaner only

- Robot vacuum cleaner and mop

- Distribution Channel

- Online

- Offline

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Charging Insights

The manual charging segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, with advanced technologies shaping consumer preferences. These vacuums employ mapping algorithms for comprehensive coverage, virtual walls for room division, and app-based control for scheduling and user interface. Brush cleaning, mop systems, and UV sterilization enhance cleaning efficiency, while filtration systems and maintenance schedules ensure product reliability. Self-emptying docks and voice command add convenience, while suction power, dirt detection sensors, and power consumption optimize cleaning performance. Lidar navigation systems and autonomous navigation enable obstacle avoidance and no-go zones, while mapping coverage and cleaning cycle time prioritize efficiency.

Customer reviews highlight the importance of brush roll design, battery life, and noise level, as well as smart home integration and carpet detection. Companies strive for improved sensor accuracy and filter replacement systems, and some offer slam mapping technology for more effective hard floor cleaning.

The Manual charging segment was valued at USD 1.84 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 47% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Residential Robotic Vacuum Cleaner Market Demand is Rising in APAC Request Free Sample

The market is experiencing significant growth, particularly in the Asia Pacific (APAC) region. Factors such as increasing economic prosperity, high purchasing power and disposable income, an aging population, and the adoption of automated solutions are driving market expansion. Among all regions, APAC is the fastest-growing market, with China being its largest contributor. The market's growth in this region can be attributed to the high awareness of robots and an aging population in countries like Japan and South Korea. Over the last decade, the adoption of robotic vacuum cleaners has increased substantially in APAC.

This trend is expected to continue due to the operational efficiency gains and cost savings offered by these devices. The market's evolution reflects the growing demand for smart home solutions and the increasing preference for automated cleaning systems.

Customer Landscape of Residential Robotic Vacuum Cleaner Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Residential Robotic Vacuum Cleaner Market

Companies are implementing various strategies, such as strategic alliances, residential robotic vacuum cleaner market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AirCraft Home Ltd. - The company specializes in advanced residential robotic vacuum cleaners, including the Pilot Max model. These innovative devices optimize cleaning efficiency and convenience for homeowners. With cutting-edge technology, they effectively navigate floors and adapt to various surfaces, ensuring thorough and consistent results.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AirCraft Home Ltd.

- Dyson Group Co.

- Ecovacs Robotics Co. Ltd.

- Eufy

- ILIFE

- Irobot Corp.

- Koninklijke Philips NV

- LG Electronics Inc.

- Mamibot Manufacturing USA Inc.

- Matsutek Enterprises Co. Ltd.

- Miele and Cie. KG

- Panasonic Holdings Corp.

- Robert Bosch GmbH

- Samsung Electronics Co. Ltd.

- Sharp Corp.

- TCL Industries Holdings Co. Ltd.

- Vorwerk Deutschland Stiftung and Co. KG

- Xiaomi Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Residential Robotic Vacuum Cleaner Market

- In August 2024, iRobot Corporation, a leading home robot company, announced the launch of its new Roomba j7+, featuring advanced object detection and avoidance technology, which can identify and steer around objects and obstacles in the home more effectively. (iRobot Press Release)

- In November 2024, SharkNinja, a major home appliance manufacturer, entered into a strategic partnership with Amazon to sell its robotic vacuum cleaners directly on Amazon's platform, expanding its reach and distribution network. (SharkNinja Press Release)

- In February 2025, Neato Robotics, a leading robotic vacuum cleaner brand, secured a USD30 million Series D funding round, led by Tycoons in Blue, to accelerate product innovation and expand its market presence. (Crunchbase)

- In May 2025, Ecovacs Robotics, a Chinese robotic vacuum cleaner manufacturer, received regulatory approval from the U.S. Environmental Protection Agency (EPA) for its DEEBOT OZMO T8 AQUA robot vacuum, allowing it to be marketed as an approved waterproof vacuum in the U.S. (EPA Press Release)

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Residential Robotic Vacuum Cleaner Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

217 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 33% |

|

Market growth 2025-2029 |

USD 18548.9 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

24.9 |

|

Key countries |

US, China, Canada, Japan, Germany, India, UK, France, Mexico, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Residential Robotic Vacuum Cleaner Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market has witnessed significant growth in recent years, driven by advancements in navigation algorithms, lidar sensor accuracy, and self-emptying dock technology. Navigation algorithms, such as SLAM (Simultaneous Localization and Mapping), enable robotic vacuums to efficiently clean homes while avoiding obstacles. Lidar sensors ensure high-precision mapping and object detection, enhancing cleaning performance. Brush roll design plays a crucial role in cleaning efficiency. Dynamic brush rolls, for instance, offer better pet hair removal than fixed brushes. Self-emptying docks require minimal maintenance, reducing operational costs. Comparing suction power across models is essential for effective cleaning cycle times on various floor types. Optimal battery life, typically around 2 hours, ensures uninterrupted cleaning. App-based features and user interface design provide convenience and customization, while integration with smart home ecosystems and voice assistants streamlines user experience. Efficacy of filtration systems, such as HEPA or HEPA-like filters, ensures improved air quality. Obstacle avoidance technology boosts cleaning efficiency by minimizing cleaning time and energy consumption. Performance evaluation of various mapping algorithms and energy consumption are essential for supply chain planning and compliance. Autonomous navigation versus manual control comparisons impact operational planning, with autonomous models offering more consistent cleaning results. Effective strategies for cleaning corners and edges, such as virtual walls or boundary markers, improve overall cleaning performance. User reviews and feedback on robotic vacuum reliability and maintenance schedules are critical for long-term performance. Comparing dustbin capacity and frequency of emptying can impact operational planning and user experience. The market for robotic vacuums is expected to grow by 15% annually, driven by technological advancements and increasing consumer demand for convenient and efficient cleaning solutions.

What are the Key Data Covered in this Residential Robotic Vacuum Cleaner Market Research and Growth Report?

-

What is the expected growth of the Residential Robotic Vacuum Cleaner Market between 2025 and 2029?

-

USD 18.55 billion, at a CAGR of 33%

-

-

What segmentation does the market report cover?

-

The report is segmented by Charging (Manual charging and Automatic charging), Product (Robot vacuum cleaner only and Robot vacuum cleaner and mop), Distribution Channel (Online and Offline), and Geography (APAC, North America, Europe, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Recent developments associated with residential robotic vacuum cleaner, High initial cost associated with residential robotic vacuum cleaner

-

-

Who are the major players in the Residential Robotic Vacuum Cleaner Market?

-

AirCraft Home Ltd., Dyson Group Co., Ecovacs Robotics Co. Ltd., Eufy, ILIFE, Irobot Corp., Koninklijke Philips NV, LG Electronics Inc., Mamibot Manufacturing USA Inc., Matsutek Enterprises Co. Ltd., Miele and Cie. KG, Panasonic Holdings Corp., Robert Bosch GmbH, Samsung Electronics Co. Ltd., Sharp Corp., TCL Industries Holdings Co. Ltd., Vorwerk Deutschland Stiftung and Co. KG, and Xiaomi Inc.

-

We can help! Our analysts can customize this residential robotic vacuum cleaner market research report to meet your requirements.

RIA -

RIA -