Retail Digital Signage Market Size 2026-2030

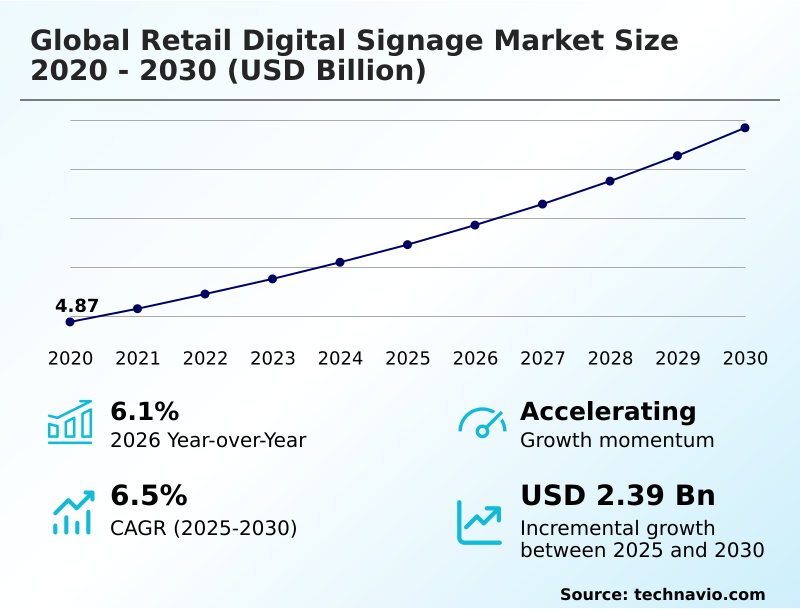

The retail digital signage market size is valued to increase by USD 2.39 billion, at a CAGR of 6.5% from 2025 to 2030. Advancement of omnichannel strategy through phygital integration will drive the retail digital signage market.

Major Market Trends & Insights

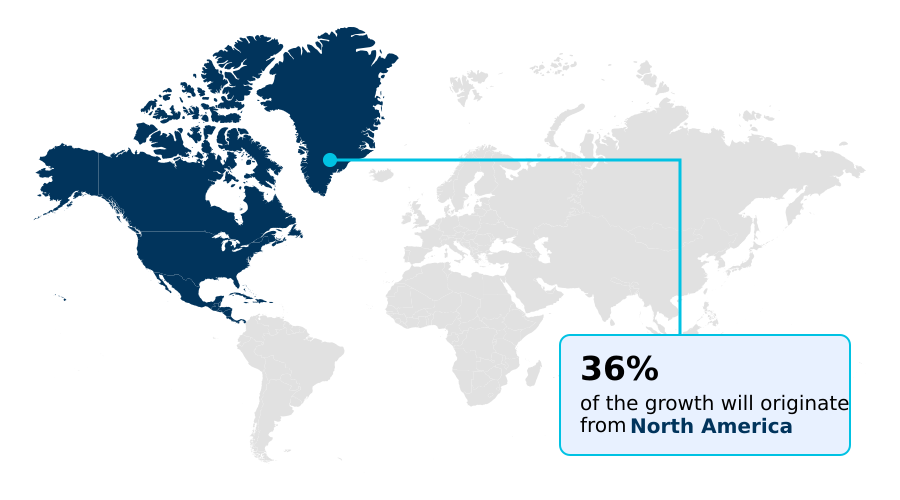

- North America dominated the market and accounted for a 36.2% growth during the forecast period.

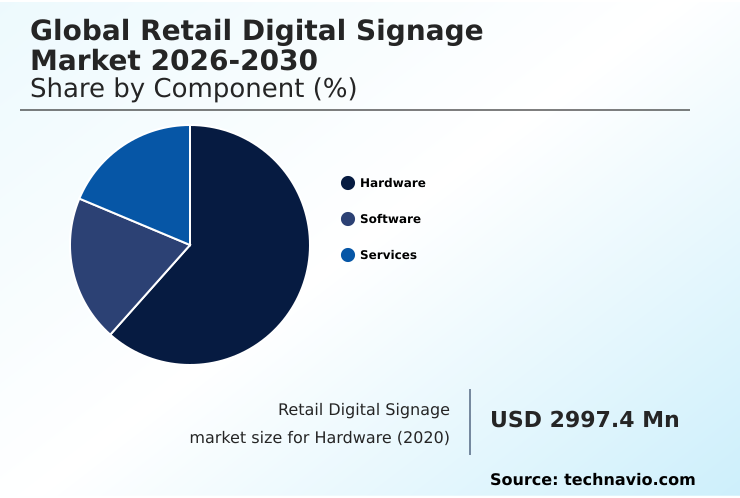

- By Component - Hardware segment was valued at USD 3.64 billion in 2024

- By Product Type - Standalone displays segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.98 billion

- Market Future Opportunities: USD 2.39 billion

- CAGR from 2025 to 2030 : 6.5%

Market Summary

- The Retail Digital Signage Market is undergoing a significant transformation, moving beyond simple electronic displays to become a cornerstone of modern phygital retail. This evolution is driven by the need to create immersive brand experiences and bridge the gap between digital and physical commerce.

- Key technologies such as AI and computer vision are integrated into interactive kiosks and displays, enabling retailers to gather real-time analytics on consumer behavior for hyper-personalization of content.

- For instance, a fashion retailer can use augmented reality mirrors for virtual try-on services, enhancing the in-store experience while collecting data on popular items, which can optimize inventory management by up to 20%. However, the high initial cost of ultra-high-definition displays and the complexities of data privacy regulations present significant challenges.

- The successful implementation of centralized content management systems is crucial for deploying cohesive omnichannel strategies, ensuring brand consistency and operational efficiency across all customer touchpoints, from wayfinding to checkout. This dynamic landscape demands a strategic balance between technological innovation and sustainable business practices.

What will be the Size of the Retail Digital Signage Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Retail Digital Signage Market Segmented?

The retail digital signage industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

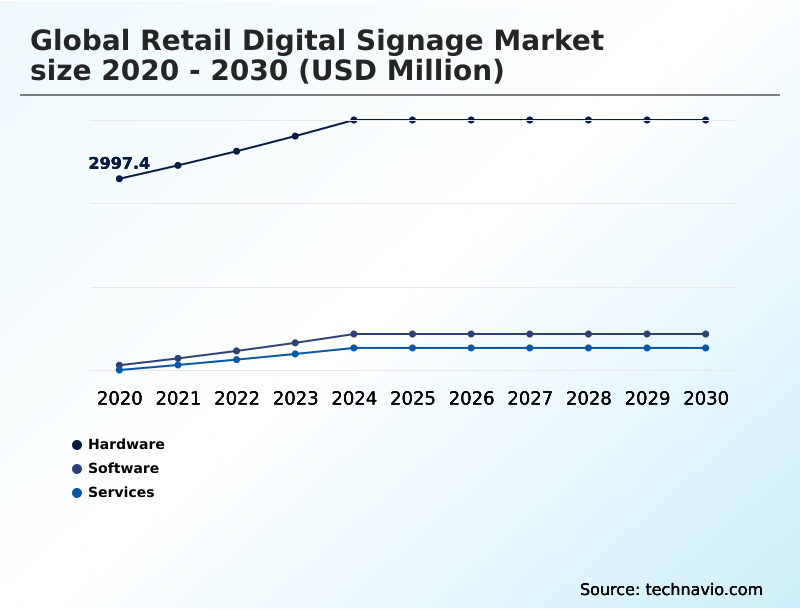

- Component

- Hardware

- Software

- Services

- Product type

- Standalone displays

- Video walls

- Digital menu boards

- Interactive kiosks

- Others

- End-user

- Hypermarkets and supermarkets

- Specialty stores

- Department stores

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Japan

- Europe

- UK

- Germany

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The hardware segment, including ultra-high-definition displays and media players, forms the physical backbone of retail visual communication. Development focuses on visual fidelity and durability, with micro-LED technology enabling seamless, customizable video walls. This technology is critical for omnichannel integration.

The segment also encompasses infrastructure like mounting solutions and connectivity for operational stability. Systems utilizing proximity detection and ambient light sensors can optimize performance and reduce energy consumption by up to 15%.

Innovations like transparent screens, which blend physical products with digital information, are creating layered sensory experiences, moving beyond passive display to active engagement points.

These advancements in e-paper displays and holographic displays redefine the in-store experience, supporting sophisticated phygital retail experience initiatives.

The Hardware segment was valued at USD 3.64 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 36.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Retail Digital Signage Market Demand is Rising in North America Request Free Sample

North America leads the retail digital signage market, accounting for 36.2% of the incremental growth, driven by mature infrastructure and high adoption of programmatic advertising and sophisticated IoT ecosystems.

APAC follows closely, representing 32.34% of the opportunity, with rapid urbanization and a focus on experiential retail utilizing 3D anamorphic displays.

Europe, contributing 22.62%, is heavily influenced by stringent regulations, prioritizing sustainable and privacy-compliant solutions like e-paper displays and cloud-based architectures. A key driver in this region is the need for omnichannel strategy.

The Middle East and Africa and South America show steady growth, focusing on modernizing retail formats and implementing foundational technologies like quick response codes for omnichannel integration.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the future of retail requires a deep understanding of the strategic implications behind emerging display technologies. A core consideration is the impact of AI on retail digital signage personalization, which moves beyond generic advertising to deliver tailored content that can significantly lift conversion rates.

- Concurrently, businesses must perform a rigorous cost-benefit analysis of electronic shelf labels vs paper, weighing the upfront investment against long-term operational savings and dynamic pricing capabilities, which can outperform static models by a significant margin. Success also hinges on optimizing retail store layout with digital wayfinding, as effective navigation reduces shopper friction and increases time spent in high-margin areas.

- Furthermore, integrating digital signage with point-of-sale systems is no longer optional; it is essential for real-time inventory accuracy and a seamless omnichannel experience. Finally, addressing the privacy challenges of computer vision in retail analytics is paramount.

- Retailers must adopt privacy-by-design principles to build consumer trust, as failure to do so can undermine the entire data-driven strategy and lead to regulatory penalties. These elements collectively shape a complex but opportunity-rich environment for forward-thinking retailers.

What are the key market drivers leading to the rise in the adoption of Retail Digital Signage Industry?

- The advancement of omnichannel strategies through phygital integration, which synchronizes the physical and digital consumer journey, is a key market driver.

- The need for a seamless phygital retail experience is a primary driver, with retailers using centralized content management systems to synchronize online and in-store promotions. This omnichannel approach is critical for brand consistency.

- The evolution of display technologies, including high-efficiency transparent OLED panels and advanced gesture control, enhances visual quality and interactivity. AI integration transforms passive signs into intelligent agents for targeted content.

- Furthermore, the push for operational efficiency and sustainability makes digital shelf-edge labels a logical solution, reducing paper waste and enabling dynamic pricing that can boost margin control by 2-4%.

- The phygital experience relies on these advanced media players and IoT ecosystems.

What are the market trends shaping the Retail Digital Signage Industry?

- The proliferation of artificial intelligence and real-time consumer analytics is a primary market trend, driving the shift from static advertising to dynamic, data-responsive content.

- The global retail digital signage market is increasingly defined by the integration of artificial intelligence and real-time data processing. This trend is particularly dominant in North America and APAC, where technologies like computer vision and machine learning transform displays into intelligent observers.

- Such systems facilitate hyper-personalization by adjusting content based on viewer demographics, with early adopters reporting engagement increases of over 25%. Sustainability is also a key focus, with new hardware like transparent OLED panels designed for lower energy use, reducing operational costs by up to 80% in some cases through the adoption of technologies like contactless interaction technologies and facial recognition.

What challenges does the Retail Digital Signage Industry face during its growth?

- Significant financial barriers to entry and high long-term operational expenses present a key challenge impacting broader industry adoption and growth.

- Substantial initial investment for ultra-high-definition displays and interactive kiosks remains a primary hurdle. Ongoing operational expenses, including software licensing and energy consumption, further compound the financial burden. Data privacy regulations, such as GDPR, create complexity for systems using biometric-enabled advertising and require significant investment in compliant edge computing solutions to anonymize data.

- A German pilot program was suspended due to insufficient consent methods, highlighting the difficulty in balancing personalization with privacy. Hardware interoperability and fragmented content management systems also create significant technical challenges, increasing long-term operational costs and hindering seamless integration with existing retail systems like POS databases, a core component of phygital.

Exclusive Technavio Analysis on Customer Landscape

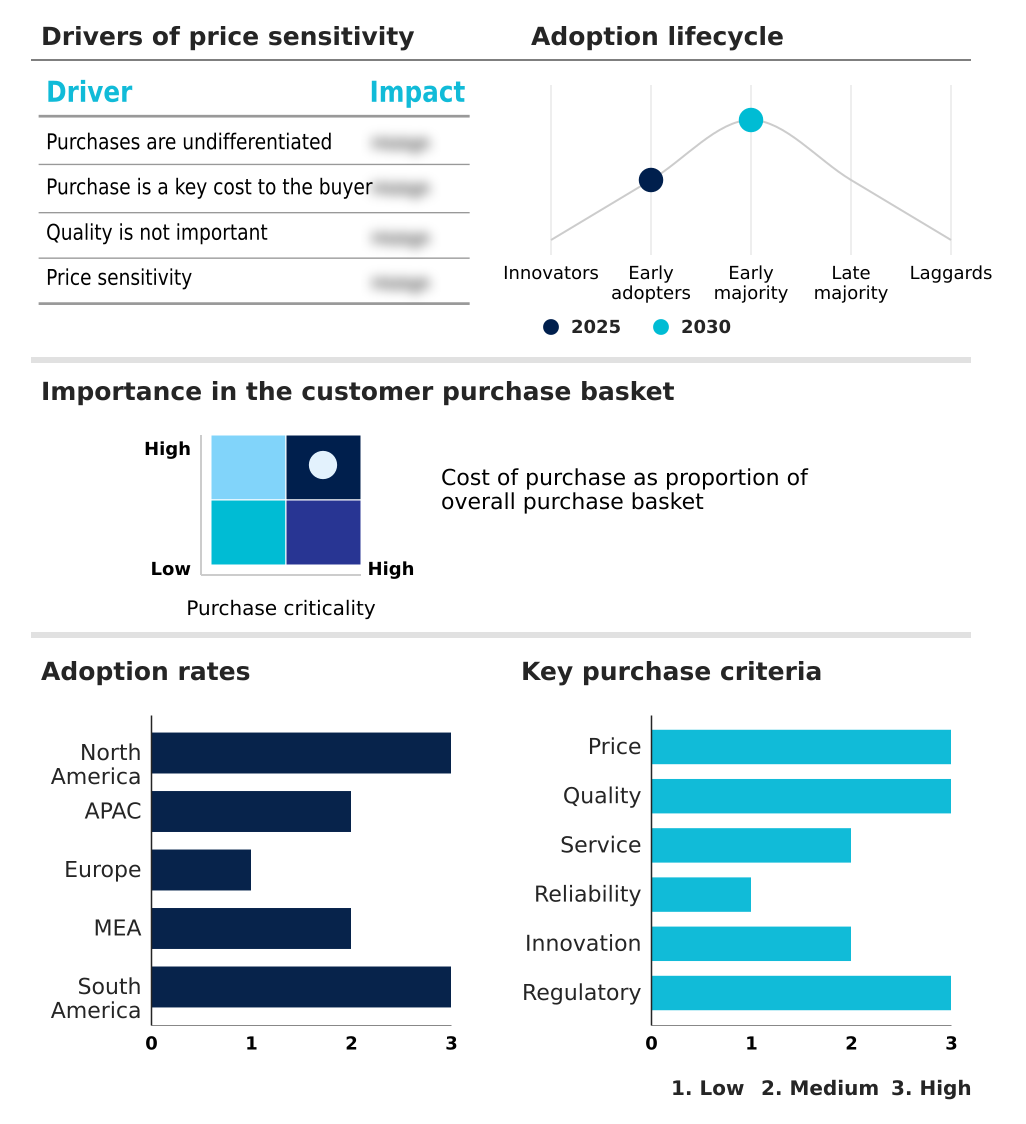

The retail digital signage market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the retail digital signage market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Retail Digital Signage Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, retail digital signage market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Acer Inc. - Provides a portfolio of professional displays including large-format, 4K, and interactive video walls designed for retail visualization.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Acer Inc.

- ASUSTeK Computer Inc.

- AUO Corp.

- Barco NV

- Christie Digital Systems Inc.

- Dell Technologies Inc.

- Elo Touch Solutions Inc.

- HP Inc.

- Koninklijke Philips NV

- Leyard International.

- LG Electronics Inc.

- Mitsubishi Electric Corp.

- NEC Corp.

- Panasonic Holdings Corp.

- Planar Systems Inc.

- Samsung Electronics Co. Ltd.

- Sharp Corp.

- Sony Group Corp.

- Toshiba Corp.

- ViewSonic Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Retail digital signage market

- In August 2025, a prominent North American department store chain deployed a system that synchronized mobile shopping carts with in-store interactive kiosks across its flagship locations.

- In May 2025, a leading global technology firm headquartered in Seoul launched a suite of signage solutions that utilized edge computing to analyze customer demographics without storing personal information.

- In March 2025, Target Corporation implemented a comprehensive network of AI-powered interactive kiosks across three hundred US locations to provide personalized product recommendations.

- In November 2025, Adidas introduced a proprietary Scan-and-Sync interactive display system in its flagship stores in London and Paris, allowing shoppers to synchronize mobile profiles with large-format wall displays.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Retail Digital Signage Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 316 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.5% |

| Market growth 2026-2030 | USD 2392.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.1% |

| Key countries | US, Canada, Mexico, China, India, Japan, South Korea, Australia, Indonesia, UK, Germany, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The retail digital signage market is defined by its role as the central nervous system for the modern phygital retail experience. Its continuous evolution is marked by the convergence of advanced hardware and intelligent software. The adoption of micro-LED technology and transparent OLED panels, managed through centralized content management systems, allows for unprecedented visual storytelling.

- Core to this is omnichannel integration, ensuring a seamless customer journey. Boardroom decisions are increasingly influenced by the need to balance innovation with regulatory compliance; for example, the use of facial recognition for hyper-personalization must navigate stringent data privacy laws, impacting technology budgets and vendor selection.

- Systems leveraging edge computing to process analytics locally can reduce data transmission costs by over 40% while enhancing security. This ecosystem, which includes interactive kiosks, programmatic advertising, and digital shelf-edge labels, is no longer a peripheral marketing tool but a critical operational asset driving both sales and efficiency through contactless interaction technologies, augmented reality mirrors, and e-paper displays.

What are the Key Data Covered in this Retail Digital Signage Market Research and Growth Report?

-

What is the expected growth of the Retail Digital Signage Market between 2026 and 2030?

-

USD 2.39 billion, at a CAGR of 6.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware, Software, and Services), Product Type (Standalone displays, Video walls, Digital menu boards, Interactive kiosks, and Others), End-user (Hypermarkets and supermarkets, Specialty stores, Department stores, and Others) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Advancement of omnichannel strategy through phygital integration, Financial barriers to entry and long-term operational expenses

-

-

Who are the major players in the Retail Digital Signage Market?

-

Acer Inc., ASUSTeK Computer Inc., AUO Corp., Barco NV, Christie Digital Systems Inc., Dell Technologies Inc., Elo Touch Solutions Inc., HP Inc., Koninklijke Philips NV, Leyard International., LG Electronics Inc., Mitsubishi Electric Corp., NEC Corp., Panasonic Holdings Corp., Planar Systems Inc., Samsung Electronics Co. Ltd., Sharp Corp., Sony Group Corp., Toshiba Corp. and ViewSonic Corp.

-

Market Research Insights

- The retail digital signage market is shaped by the pursuit of operational efficiency and enhanced customer engagement. Retailers are adopting dynamic pricing strategies, which can adjust in real-time, improving pricing accuracy by over 99% compared to manual methods. The implementation of predictive maintenance protocols on display networks reduces hardware downtime by as much as 30%, safeguarding brand image.

- The shift to software-as-a-service models lowers initial capital expenditure, making advanced content management accessible to more businesses. This phygital retail approach, which includes endless aisle browsing and gamified shopping experiences, is critical for creating a compelling in-store experience.

We can help! Our analysts can customize this retail digital signage market research report to meet your requirements.

RIA -

RIA -