US Robotic Prosthetics Market Size 2024-2028

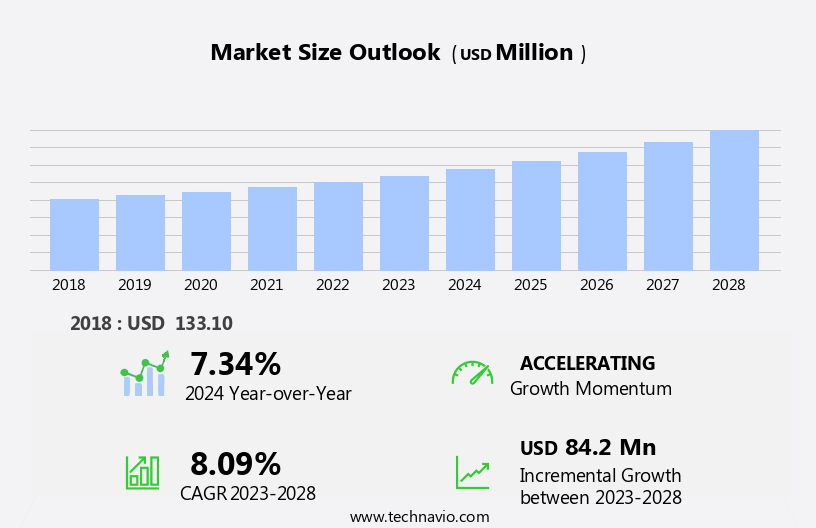

The US robotic prosthetics market size is forecast to increase by USD 84.2 million, at a CAGR of 8.09% between 2023 and 2028.

- The Robotic Prosthetics Market in the US is witnessing significant growth, driven by the expanding target population and the relentless pursuit to restore personal mobility and independence for amputees. The market is fueled by an increasing number of technological advances and Research and Development activities, which continue to revolutionize the field of prosthetics. However, the high cost of prosthetic solutionsremains a formidable challenge, limiting accessibility for many potential users. Companies seeking to capitalize on market opportunities must navigate this financial barrier by exploring cost-effective solutions, collaborations, and innovative business models.

- Additionally, staying abreast of the latest technological developments and regulatory landscape is crucial for maintaining a competitive edge. The robust growth potential in this market is underpinned by the unmet needs of the growing amputee population and the ongoing technological innovations, offering ample opportunities for companies to make a meaningful impact.

What will be the size of the US Robotic Prosthetics Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

- The robotic prosthetics market in the US is witnessing significant advancements, particularly in the areas of upper and lower limb prosthetics. Personalized prosthetic fitting, achieved through gait analysis algorithms and muscle activation patterns, is becoming increasingly important for enhancing patient comfort and functionality. Neural interface technology and haptic feedback systems are revolutionizing the field, enabling more natural interaction between the user and the prosthetic limb. Advanced prosthetic materials, such as biocompatible coatings and wearable sensor networks, are improving prosthetic durability and enabling more precise prosthetic limb alignment. Robotic hand dexterity and robotic arm design are also seeing improvements through actuator control systems and prosthetic joint articulation.

- Kinematic analysis software and biomechanical modeling are essential tools for optimizing control algorithm design and surgical implantation techniques. Prosthetic rehabilitation protocols are being enhanced through user feedback mechanisms, motion capture technology, and EMG signal amplification. Prosthetic weight distribution and wearable sensor networks are crucial for understanding the user's needs and preferences. Prosthetic socket design and prosthetic durability testing are ongoing areas of research to ensure optimal performance and user satisfaction. Haptic feedback systems and prosthetic power sources are also gaining attention, with a focus on creating more energy-efficient and user-friendly solutions. The market is expected to continue evolving, driven by technological innovations and growing demand for advanced prosthetic solutions.

How is this market segmented?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Orthotic and prosthetic clinics

- Hospitals

- Specialty orthopedic centers

- Product

- Lower limb robotic prosthetics

- Upper limb robotic prosthetics

- Geography

- North America

- US

- North America

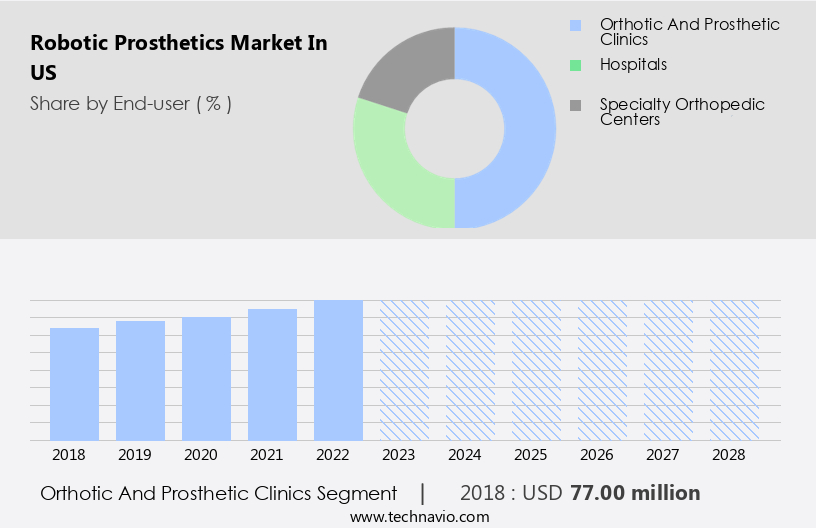

By End-user Insights

The orthotic and prosthetic clinics segment is estimated to witness significant growth during the forecast period.

In the realm of orthotic and prosthetic solutions, advanced technologies are revolutionizing the industry to enhance functionality and patient comfort. Biocompatible coatings ensure the durability and longevity of prosthetics, while haptic feedback systems provide a more natural sensation for users. Prosthetic power sources have evolved to include lightweight, rechargeable batteries, and bio-integrated sensors enable real-time monitoring of patient movement and vital signs. Myoelectric signal processing and pattern recognition software facilitate intuitive control, and gait analysis algorithms optimize walking patterns. Actuator control systems enable precise joint articulation, and wearable sensor networks provide continuous data for prosthetic rehabilitation protocols.

Robotic hand dexterity and personalized prosthetic fitting have improved, allowing for greater functionality and comfort. Surgical implantation techniques, such as osseointegration, have advanced to provide more stable and secure attachments. Advanced prosthetic materials, including lightweight alloys and high-strength polymers, have reduced the weight of prosthetics, making them easier to use. Control algorithm optimization and neural interface technology have enabled more natural and intuitive control, while user feedback mechanisms provide real-time adjustments for improved performance. Prosthetic joint articulation has been enhanced through kinematic analysis software and motion capture technology, resulting in more fluid and lifelike movements.

In the realm of upper and lower limb prosthetics, robotic arm design and socket design have advanced to provide greater functionality and comfort, while prosthetic limb alignment and rehabilitation protocols have been optimized to improve patient outcomes.

The Orthotic and prosthetic clinics segment was valued at USD 77.00 million in 2018 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the US Robotic Prosthetics Market drivers leading to the rise in adoption of the Industry?

- The market's expansion is primarily fueled by the increasing target population and the focus on enabling mobility and independence for amputees.

- The demand for robotic prosthetics in the US is driven by the rising number of individuals requiring artificial limbs due to various reasons. Trauma cases and accidents are significant contributors, as well as the increasing prevalence of diabetes and congenital diseases. Each year, approximately 1,500 babies are born with upper limb reductions, and 750 babies are born with lower limb reductions in the US. This equates to four out of 10,000 babies born with upper limb reductions and two out of 10,000 babies born with lower limb reductions.

- The advancement of technology has led to the development of kinematic analysis software, enabling more precise and personalized prosthetic solutions.

What are the US Robotic Prosthetics Market trends shaping the Industry?

- The trend in the market is characterized by an escalating number of technological advances and Research and Development activities. This upward trajectory in innovation is a mandatory and significant aspect of modern business dynamics.

- Robotic prosthetics have advanced significantly, offering amputees improved mobility and reduced risk of falls. Powered prostheses, driven by innovations such as lithium-ion batteries, brushless electric motors with rare earth magnets, miniaturized sensors integrated into semiconductor chips, and low-power computer chips, replicate natural limb movements. These technological advancements are the result of extensive research and development efforts. Biocompatible coatings ensure a harmonious interaction between the prosthetic and the body, while haptic feedback systems provide a sense of touch. Prosthetic power sources and bio-integrated sensors, along with myoelectric signal processing, contribute to the overall functionality and durability of these devices.

- Prosthetic durability testing and socket design, with a focus on weight distribution, further enhance the user experience. These advancements continue to transform the lives of amputees, enabling them to navigate various terrains with greater ease and confidence.

How does US Robotic Prosthetics Market face challenges during its growth?

- The high cost of prosthetics poses a significant challenge to the growth of the prosthetics industry. This issue, which is a major concern for both manufacturers and patients, limits the accessibility and affordability of advanced prosthetic technologies.

- Robotic prosthetics offer advanced functionality and improved user experience compared to conventional prosthetics, yet their higher cost is a significant barrier to adoption. The average price of conventional prosthetics ranges from USD 9,500 to USD 11,500, while advanced myoelectric and microprocessor-controlled (MPC) prosthetics can cost between USD 35,000 and USD 55,000. For instance, the Genium X3 knee, a high-end MPC knee developed by Ottobock, retails around USD 120,000. Similarly, the Michelangelo electronic hand costs approximately USD 60,000. These costs, coupled with insufficient reimbursements, hinder the widespread adoption of robotic prosthetics.

- To address this challenge, ongoing research focuses on enhancing prosthetic rehabilitation protocols, improving actuator control systems, and developing gait analysis algorithms. Additionally, patient comfort features, wearable sensor networks, and upper limb prosthetics with surgical implantation techniques are under investigation to make robotic prosthetics more accessible and affordable.

Exclusive US Robotic Prosthetics Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aether Biomedical sp. z o.o.

- Blatchford Ltd.

- Click Medical LLC

- DEKA Research and Development Corp.

- Fillauer LLC

- Hanger Inc

- HDT Global

- Mobius Bionics LLC

- Ossur hf

- Ottobock SE and Co. KGaA

- Steeper Inc.

- Trulife

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Robotic Prosthetics Market In US

- In January 2024, Boston Scientific Corporation, a leading medical device company, announced the FDA approval of its new REAL Hand Solution robotic prosthetic system. This advanced technology offers improved grip control and dexterity for amputees (Boston Scientific Corporation Press Release, 2024).

- In March 2024, Medtronic plc and Google's Life Sciences division, Verily, entered into a strategic partnership to develop advanced robotic prosthetic limbs. This collaboration aimed to combine Medtronic's expertise in prosthetics with Verily's knowledge in sensor technology and data analytics (Medtronic Press Release, 2024).

- In April 2025, Ossur, a leading provider of prosthetic solutions, raised USD100 million in a Series C funding round. This investment will be used to expand its research and development capabilities, particularly in robotic prosthetics (BusinessWire, 2025).

- In May 2025, the Food and Drug Administration (FDA) granted clearance to Hanger, Inc. For its new myoelectric prosthetic system, the Touch Bionics i-Limb Quantum Revolution. This advanced robotic prosthetic hand offers increased functionality and customization for amputees (Hanger, Inc. Press Release, 2025).

Research Analyst Overview

The robotic prosthetics market in the US continues to evolve, driven by advancements in technology and growing demand for more functional and comfortable solutions. Prosthetic rehabilitation protocols are being refined through the integration of actuator control systems, gait analysis algorithms, and patient comfort features. Seamless integration of wearable sensor networks and upper limb prosthetics enables improved muscle activation patterns and biomechanical modeling. Surgical implantation techniques, such as osseointegration process and personalized prosthetic fitting, are gaining popularity for their ability to enhance durability and patient satisfaction. Advanced prosthetic materials, like biocompatible coatings and lightweight alloys, are being used to enhance the durability and aesthetics of prosthetic limbs.

Robotic hand dexterity is being enhanced through the use of haptic feedback systems and pattern recognition software. Prosthetic power sources, such as rechargeable batteries and fuel cells, are being optimized for improved efficiency and longevity. The ongoing development of control algorithm optimization, neural interface technology, and prosthetic joint articulation is enabling more natural and intuitive prosthetic limb control. Motion capture technology and kinematic analysis software are being used to improve the alignment and functionality of both upper and lower limb prosthetics. The evolving nature of the market is also reflected in the emergence of new applications across various sectors, including military, healthcare, and sports.

The continuous unfolding of market activities and evolving patterns underscores the importance of staying abreast of the latest developments in robotic prosthetics technology.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Robotic Prosthetics Market in US insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

116 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.09% |

|

Market growth 2024-2028 |

USD 84.2 million |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

7.34 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across US

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -