Personal Mobility Devices Market Size 2024-2028

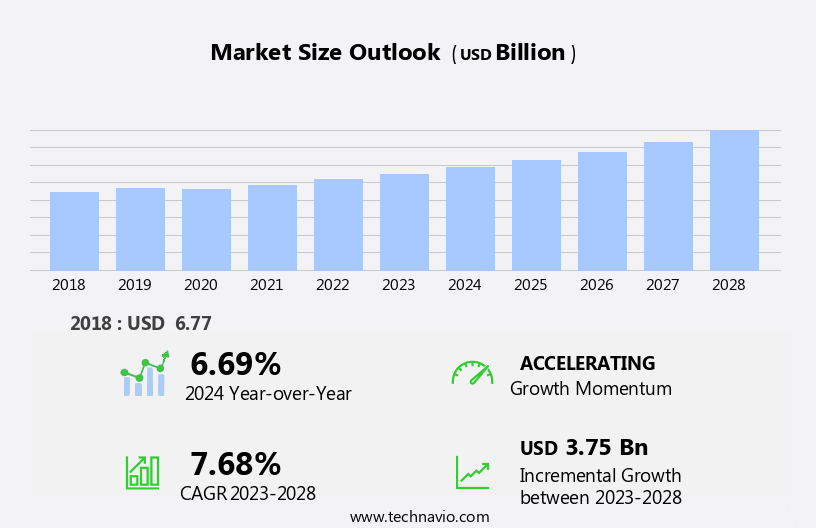

The personal mobility devices market size is forecast to increase by USD 3.75 billion, at a CAGR of 7.68% between 2023 and 2028.

- The market is experiencing significant growth, driven by the increasing number of orthopedic and neurological disorders that necessitate the use of these devices. This trend is expected to continue as the global population ages and the prevalence of chronic conditions increases. Another key driver is the automation of manually operated personal mobility devices, which enhances user experience and convenience. However, the high cost associated with these devices poses a significant challenge for both manufacturers and consumers. Despite this, opportunities exist for companies to differentiate themselves through innovative product design, affordable pricing strategies, and partnerships with healthcare providers and insurers.

- Additionally, the integration of advanced technologies, such as artificial intelligence and IoT, can add value to personal mobility devices, creating new revenue streams and enhancing user experience. Companies must navigate these opportunities and challenges effectively to capitalize on the market's potential and meet the evolving needs of their customer base.

What will be the Size of the Personal Mobility Devices Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, with innovations in user interface design, charging time optimization, and speedometer accuracy driving advancements in various sectors. Devices now integrate regenerative braking systems and hill climbing assist, ensuring optimal energy efficiency and enhanced performance. Tire pressure monitoring and segway balancing algorithms provide improved stability and safety, while cruise control functions offer a smoother riding experience. Ergonomic handlebar designs and three-wheeled scooter designs cater to diverse user needs, and wheelchair accessibility features expand the market's reach. Maximum speed control and folding mechanism designs enable easy transportation, while hoverboard stability control and electric motor efficiency optimize user experience.

Lithium-ion battery life and anti-theft systems address concerns, and suspension system performance and power assist systems cater to diverse user requirements. Ongoing advancements in battery thermal management and GPS tracking systems further enhance the functionality of these devices. The market's dynamics continue to unfold, with continuous innovation shaping the future of personal mobility solutions.

How is this Personal Mobility Devices Industry segmented?

The personal mobility devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

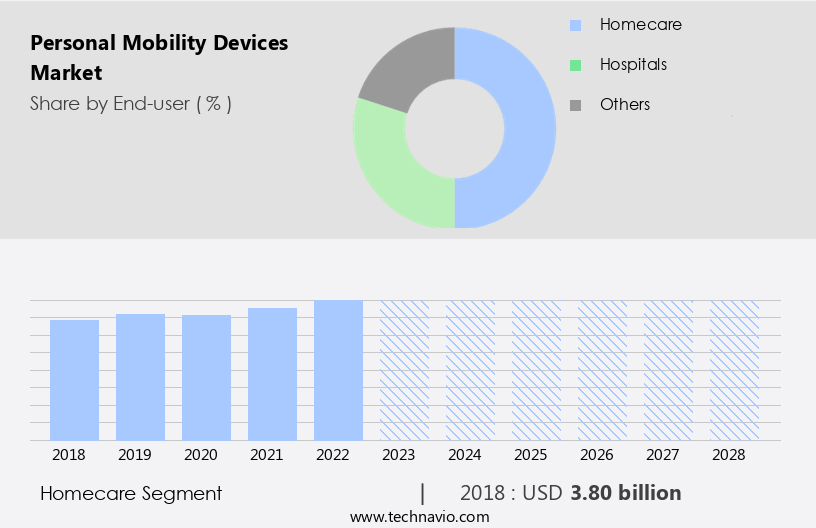

- End-user

- Homecare

- Hospitals

- Others

- Product

- Wheelchairs

- Walking aids

- Scooters and others

- Geography

- North America

- US

- Europe

- France

- Germany

- APAC

- China

- India

- Rest of World (ROW)

- North America

By End-user Insights

The homecare segment is estimated to witness significant growth during the forecast period.

The market in homecare settings is experiencing significant growth due to an aging population and the rising prevalence of chronic health conditions. Advanced technologies such as regenerative braking systems, hill climbing assist, and tire pressure monitoring are enhancing the functionality and safety of mobility aids like wheelchairs, rollators, and mobility scooters. The Segway balancing algorithm and cruise control function offer users greater mobility and convenience, while ergonomic handlebar designs improve comfort and ease of use. Three-wheeled scooter designs provide better maneuverability, and wheelchair accessibility features cater to individuals with specific needs. User weight limits and frame material strength ensure durability, while lightweight chassis designs and battery thermal management systems extend the device's lifespan.

User interface designs optimize charging time, and speedometer accuracy and maximum speed control offer users greater control. Folding mechanism designs and hoverboard stability control make transportation and storage more convenient, and anti-theft systems provide peace of mind. Suspension system performance and power assist systems improve mobility, and lithium-ion battery life and scooter braking systems ensure reliable operation. GPS tracking systems offer added security and convenience for users. In-home care is increasingly focusing on enabling individuals to maintain their independence and improve their quality of life, making personal mobility devices an essential component of this trend.

The Homecare segment was valued at USD 3.80 billion in 2018 and showed a gradual increase during the forecast period.

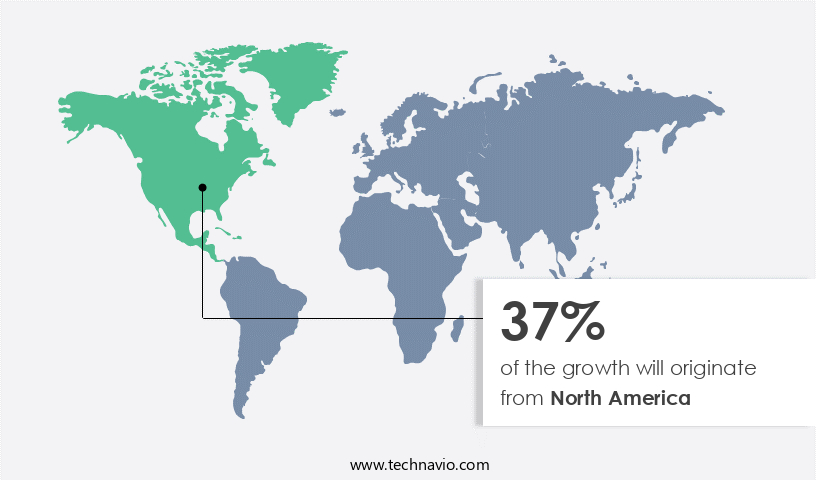

Regional Analysis

North America is estimated to contribute 37% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the dynamic US market for personal mobility devices, several advanced features are gaining traction. Regenerative braking systems are increasingly being integrated to enhance energy efficiency and extend battery life. Hill climbing assist technology aids users in navigating steep inclines with ease, while tire pressure monitoring ensures optimal performance and safety. The Segway balancing algorithm and cruise control function offer a smooth riding experience, and ergonomic handlebar designs cater to user comfort. Three-wheeled scooter designs provide agility and maneuverability, making them popular among users. Wheelchair accessibility features are crucial for individuals with mobility limitations, expanding the market's reach.

User weight limits vary among devices, necessitating robust frame material strength and lightweight chassis designs. Battery thermal management is essential for maintaining optimal battery performance and longevity. User interface designs prioritize simplicity and ease of use, while charging time optimization and speedometer accuracy ensure convenience. Maximum speed control and folding mechanism designs cater to diverse user needs. Hoverboard stability control and electric motor efficiency are key considerations for balanced and efficient operation. Anti-theft systems offer peace of mind, and suspension system performance enhances user comfort. Power assist systems cater to users with varying energy requirements, and lithium-ion battery life determines the overall value proposition.

Scooter braking systems are crucial for safe stopping, and GPS tracking systems provide added security and convenience. The market's evolution reflects the growing demand for innovative, efficient, and accessible mobility solutions.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market encompasses a wide range of technologies and solutions designed to enhance the mobility of individuals with various physical limitations or disabilities. Focusing on this market's evolving nature, these devices offer innovative solutions through methods such as advanced battery technology and lightweight materials. With considerations like user-friendly designs and customizable features becoming increasingly important, the market is a significant area of growth. Key applications of personal mobility devices include power chairs, scooters, and wheelchairs. Power chairs, for instance, provide users with the ability to maneuver around their environment with ease, allowing them to maintain independence and mobility. Scooters, another essential mobility device, offer a more portable solution for individuals who require assistance with longer distances. Lastly, wheelchairs continue to be a vital component of personal mobility devices, with advancements in materials and design making them more comfortable and functional. Through methods such as market segmentation and trend analysis, the market is being studied extensively to understand its various aspects. Key areas involve demographic trends, technological advancements, and regulatory requirements. Demographic trends, including an aging population and an increase in individuals with disabilities, are driving demand for personal mobility devices. Technological advancements, such as the integration of smart technology and telehealth capabilities, are enhancing the functionality and convenience of these devices. Regulatory requirements, on the other hand, ensure the safety and accessibility of personal mobility devices for all users. In conclusion, the market is a dynamic and growing industry that offers innovative solutions for individuals with mobility limitations. By focusing on user needs, technological advancements, and regulatory requirements, this market is poised for continued growth and development.

What are the key market drivers leading to the rise in the adoption of Personal Mobility Devices Industry?

- The prevalence of orthopedic and neurologic disorders serves as the primary growth factor for the market, as the increasing incidence and prevalence of these conditions drive demand for effective treatments and interventions.

- The market is experiencing significant growth due to the increasing prevalence of orthopedic and neurological conditions. These conditions, including rheumatoid arthritis, knee problems, and hip arthritis, necessitate the use of mobility devices such as wheelchairs and scooters for patients to move around independently. Factors such as medical emergencies, long-term and short-term disabilities, and the rising number of surgical procedures further fuel market growth. Advanced features, such as regenerative braking systems, hill climbing assist, tire pressure monitoring, segway balancing algorithms, cruise control functions, and ergonomic handlebar designs, enhance the user experience and convenience. These features cater to the needs of an aging population, who are more susceptible to conditions affecting mobility.

- The market is poised for continued growth, driven by the increasing demand for mobility solutions to address various medical conditions and enable greater independence for individuals.

What are the market trends shaping the Personal Mobility Devices Industry?

- The automation of manually operated personal mobility products is an emerging market trend. This shift towards automated technology aims to enhance the user experience and increase efficiency in personal mobility solutions.

- Personal mobility devices, including three-wheeled scooters and wheelchairs, have gained significant traction in recent years due to their accessibility features and user-friendly design. These devices offer increased mobility for individuals with mobility challenges, enabling them to move around with ease and independence. Smart technology has played a crucial role in the evolution of personal mobility devices. For instance, electric wheelchairs and smart wheelchair systems can be controlled via mobile apps or Bluetooth devices, offering users greater convenience and autonomy. The US and Canadian markets have shown a strong adoption rate for these devices due to their high disposable income and healthcare spending.

- Frame material strength and lightweight chassis design are essential considerations in the development of personal mobility devices, ensuring durability and ease of use. Moreover, battery thermal management is a critical aspect of these devices' design, ensuring optimal performance and longevity. As the market continues to grow, research and development efforts are focused on enhancing user experience, safety, and functionality. Personal mobility devices have become indispensable tools for improving the lives of individuals with mobility challenges. With ongoing advancements in technology and design, these devices will continue to offer innovative solutions for enhancing mobility and independence.

What challenges does the Personal Mobility Devices Industry face during its growth?

- The high cost of personal mobility devices poses a significant challenge to the industry's growth trajectory.

- The market faces challenges due to the high cost of advanced technologies and limited government reimbursements. These factors hinder the market's growth, making these devices inaccessible for many users. The average cost of electric wheelchairs ranges from USD1,350 to USD1,700. To address these issues, manufacturers focus on user interface design, charging time optimization, speedometer accuracy, maximum speed control, folding mechanism design, and hoverboard stability control.

- These features aim to enhance the user experience while ensuring safety and efficiency. Despite the challenges, the market continues to evolve, driven by technological advancements and the increasing demand for personal mobility solutions.

Exclusive Customer Landscape

The personal mobility devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the personal mobility devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, personal mobility devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Comfort Orthopedic Co. Ltd. - This company specializes in providing mobility solutions through innovative devices, including the LY EW402 U and LY EW402 PLUS medium mobility scooters.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Comfort Orthopedic Co. Ltd.

- ComfyGO Inc.

- GF Health Products Inc.

- Golden Technologies

- Hoveround Corp.

- Invacare Corp.

- Karma Medical Products Co. Ltd.

- LEVO AG

- Matsunaga Manufactory Co. Ltd.

- Medical Depot Inc.

- MEYRA GROUP

- Ottobock SE and Co. KGaA

- Permobil AB

- Pride Mobility Products Corp.

- Roma Medical

- Sunrise Medical LLC

- Tzora Active Systems Ltd.

- Vermeiren Group

- WHILL Inc.

- YATTLL Industry Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Personal Mobility Devices Market

- In January 2024, Whiz Mobility, a leading Personal Mobility Devices (PMD) manufacturer, launched its new product line, the WhizGo X, featuring advanced AI navigation and longer battery life, at the Consumer Electronics Show (CES) in Las Vegas (Whiz Mobility Press Release, 2024).

- In March 2024, Medtronic, a global healthcare solutions company, and Segway, a renowned PMD manufacturer, announced a strategic partnership to integrate Segway's mobility devices with Medtronic's healthcare technology, aiming to enhance mobility solutions for elderly and disabled individuals (Medtronic Press Release, 2024).

- In May 2024, Hovertrax, a US-based PMD manufacturer, raised USD50 million in a Series C funding round led by Daimler AG and LG Chem, to expand its production capacity and invest in research and development (Hovertrax Press Release, 2024).

- In February 2025, the European Union (EU) passed the 'European Accessibility Act,' mandating accessibility features in various products, including PMDs, to improve accessibility for people with disabilities (European Parliament Press Release, 2025).

Research Analyst Overview

- The market is witnessing significant advancements, with key players focusing on enhancing product lifecycle management and manufacturing process efficiency. Remote diagnostics capabilities are becoming essential for identifying and addressing maintenance issues promptly, reducing downtime and costs. Range extender technology is a notable trend, extending the devices' operational range, catering to the evolving user needs. Durability testing standards and component reliability testing are crucial for ensuring product longevity and dependability. Advanced safety features are gaining traction, prioritizing user experience (UX) and environmental impact assessment. Material selection criteria are increasingly centered around sustainability and eco-friendliness, aligning with supply chain sustainability initiatives.

- Brushless DC motors and energy consumption metrics are critical factors influencing the market dynamics. Manufacturers are investing in manufacturing process improvements to optimize energy efficiency and reduce production costs. Mobility aid regulations and accessibility compliance standards continue to shape the market landscape, with ride-sharing programs emerging as a potential growth area. In the realm of product development, user experience (UX) is a primary consideration, with manufacturers focusing on integrating advanced safety features and seamless connectivity solutions. Environmental impact assessment and mobility aid regulations are shaping the design for assembly processes, ensuring compliance and sustainability. Component reliability testing and maintenance cost analysis are essential aspects of the market, with manufacturers continually striving to improve product durability and minimize long-term maintenance costs.

- Overall, the market is characterized by a focus on innovation, efficiency, and sustainability, with key players addressing the evolving needs and expectations of end-users.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Personal Mobility Devices Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

150 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.68% |

|

Market growth 2024-2028 |

USD 3.75 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.69 |

|

Key countries |

US, Germany, France, China, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Personal Mobility Devices Market Research and Growth Report?

- CAGR of the Personal Mobility Devices industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the personal mobility devices market growth of industry companies

We can help! Our analysts can customize this personal mobility devices market research report to meet your requirements.

RIA -

RIA -