Roofing Insulation Adhesives Market Size 2026-2030

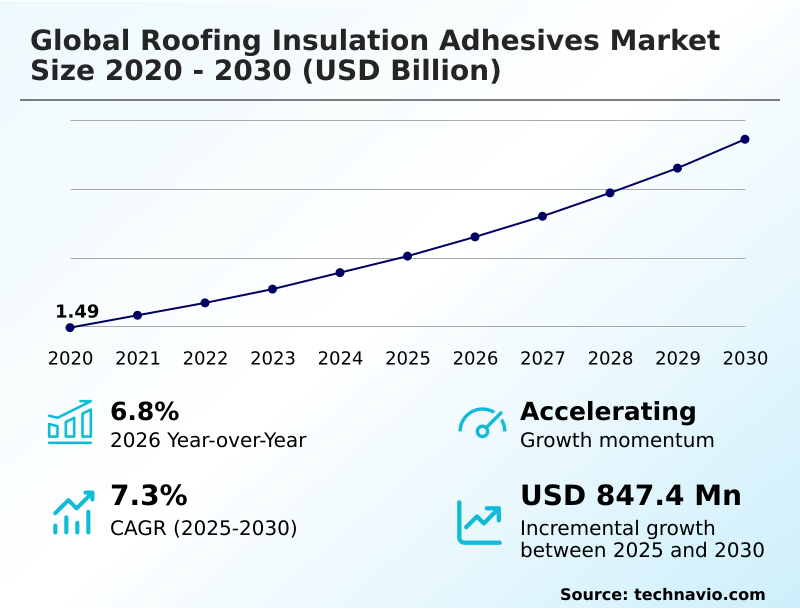

The roofing insulation adhesives market size is valued to increase by USD 847.4 million, at a CAGR of 7.3% from 2025 to 2030. Stringent energy efficiency mandates and decarbonization of building stock will drive the roofing insulation adhesives market.

Major Market Trends & Insights

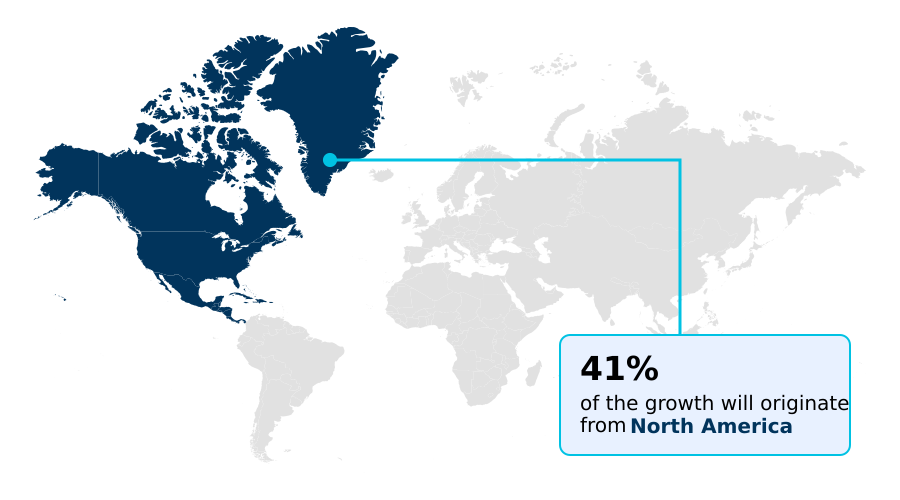

- North America dominated the market and accounted for a 41.1% growth during the forecast period.

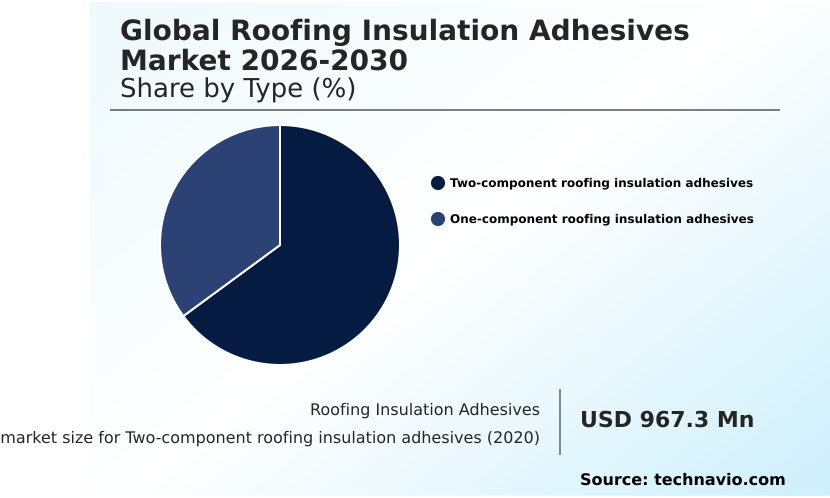

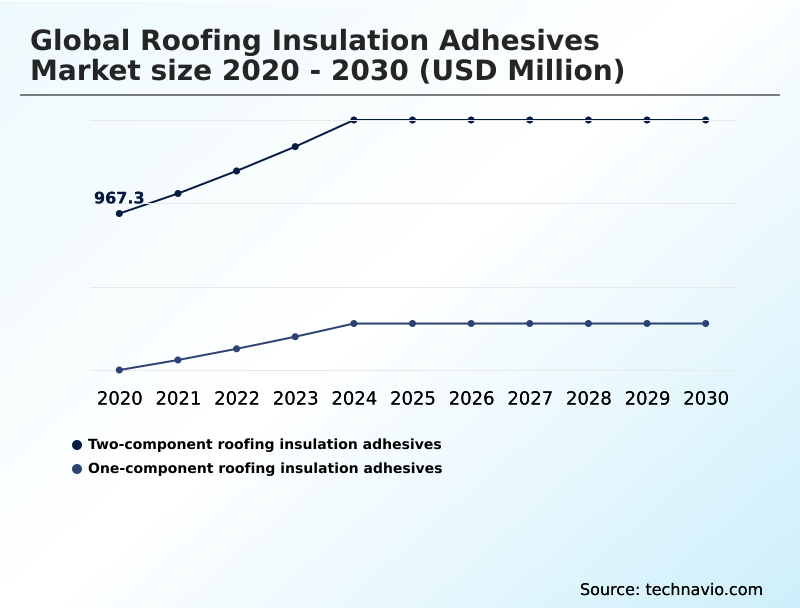

- By Type - Two-component roofing insulation adhesives segment was valued at USD 1.23 billion in 2024

- By End-user - Non-residential segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1.37 billion

- Market Future Opportunities: USD 847.4 million

- CAGR from 2025 to 2030 : 7.3%

Market Summary

- The roofing insulation adhesives market is undergoing a significant transformation, driven by the convergence of stringent energy efficiency regulations and advancements in chemical formulations. A key application is securing insulation without mechanical fasteners, which is crucial for thermal bridge elimination to maximize a building's energy performance. This method is increasingly specified in designs targeting building decarbonization mandates.

- The industry is responding with a range of products, including low-rise polyurethane foam and moisture-curing polymers, which offer enhanced performance characteristics. A major trend is the shift toward low-VOC formulations and cold-applied liquid resins to improve job site safety enhancement and meet green building standards.

- For instance, a contractor working on a hospital renovation must select a solvent-free polymer adhesive to avoid disrupting indoor air quality, a decision that balances compliance, performance, and operational continuity.

- However, challenges such as raw material price volatility and a persistent skilled labor shortage impact project costs and timelines, pushing manufacturers toward developing more efficient canister-based delivery systems and products with wider application windows.

What will be the Size of the Roofing Insulation Adhesives Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Roofing Insulation Adhesives Market Segmented?

The roofing insulation adhesives industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Two-component roofing insulation adhesives

- One-component roofing insulation adhesives

- End-user

- Non-residential

- Residential

- Distribution channel

- Indirect sales

- Direct sales

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Type Insights

The two-component roofing insulation adhesives segment is estimated to witness significant growth during the forecast period.

The roofing insulation adhesives market is segmented by product, end-user, and geography. Two-component systems represent a significant segment, valued for their rapid reaction-curing adhesive systems and superior substrate adhesion strength.

These products, often based on two-component polyurethane adhesive technology, are critical for commercial roofing sector projects where wind uplift resistance is paramount. The formulation of these adhesives focuses on building envelope integrity and waterproofing membrane compatibility.

Innovations in canister-based delivery systems address job site safety enhancement and the need for skilled labor shortage solutions.

Contractors in the industrial roofing projects space prefer these systems as they deliver consistent performance, with automated adhesive dispensing improving application efficiency by over 20% compared to manual methods, ensuring compliance with stringent fire safety code compliance.

The Two-component roofing insulation adhesives segment was valued at USD 1.23 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 41.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Roofing Insulation Adhesives Market Demand is Rising in North America Request Free Sample

The geographic landscape of the roofing insulation adhesives market is diverse, with mature regions like North America and Europe driven by stringent energy efficiency codes and building stock renovation initiatives.

North America is expected to contribute approximately 41% of the market's incremental growth, fueled by residential refurbishment and commercial projects focused on weather resilience enhancement.

In contrast, the APAC region is characterized by rapid urbanization and new construction, particularly in logistics center construction and industrial sectors. This demand is met with innovations in single-ply roofing systems and EPDM rubber adhesion.

While Europe leads in adopting bio-based adhesive technology and circular economy principles, emerging markets are focused on establishing modern infrastructure.

This regional divergence requires manufacturers to tailor their cold storage facility insulation and data center roofing solutions, creating supply chains that are 15% more complex to manage.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the roofing insulation adhesives market is increasingly focused on specialized applications and advanced material compatibility. The development of adhesives for PVDF coated metal panels has resolved long-standing installation challenges, providing a reliable chemical bonding for kynar coated components without mechanical fasteners.

- In the commercial sector, the specification of high-shear adhesives for solar-ready assemblies is becoming standard practice to support the additional weight and wind loads. For retrofit projects, bonding agents for high-density insulation boards are crucial for upgrading thermal performance. Formulations are also being optimized for specific substrates, such as polyurethane adhesives for concrete roof decks.

- In sensitive environments, the demand for single-component adhesive for occupied buildings is growing due to low-odor properties. For new builds, two-component adhesive for board-to-board application offers rapid curing, while low-temperature curing roofing adhesive formula extends the construction season in colder climates.

- The adoption of root penetration resistant green roof adhesive supports sustainable urban development, and specialized adhesive for external thermal insulation composite systems is key for facade renovations. The complexity of these niche requirements has led to supply chains that are over 20% more intricate than those for commodity construction materials, demanding precise inventory and logistics planning from suppliers.

What are the key market drivers leading to the rise in the adoption of Roofing Insulation Adhesives Industry?

- Stringent energy efficiency mandates and the push for the decarbonization of building stock are key drivers propelling market growth.

- Market growth is fundamentally driven by stringent building decarbonization mandates and the global emphasis on energy efficiency. Regulations now require significant improvements in thermal performance, directly fueling demand for adhesive solutions that facilitate thermal bridge elimination.

- Using adhesives for polyisocyanurate (ISO) insulation and expanded polystyrene (EPS) bonding, instead of mechanical fasteners, can preserve over 95% of an insulation's stated R-value.

- Another major driver is the proliferation of green roofing systems and cool roof adhesion technologies, which require specialized bonding agents for structural integrity.

- Strategic consolidation is also shaping the competitive landscape, enabling firms to expand into high-growth segments like data center roofing and prefabricated housing construction. This allows for the development of integrated solutions that meet new net-zero building envelopes standards.

What are the market trends shaping the Roofing Insulation Adhesives Industry?

- A prominent market trend is the increasing adoption of eco-friendly and low-VOC adhesive formulations. This shift is driven by stringent environmental regulations and rising demand for sustainable building materials.

- Key trends are reshaping the roofing insulation adhesives market, driven by sustainability and efficiency demands. There is a definitive shift toward eco-friendly options, with new bio-based adhesive technology and solvent-free polymer adhesives reducing environmental impact. Modern formulations offer up to 90% lower VOC content compared to legacy products.

- This trend supports the growing adoption of sustainable construction materials and aligns with circular economy principles. Concurrently, the industry is moving toward advanced application methods. The use of cold-applied liquid resins and specialized systems for EPDM rubber adhesion improves job site safety enhancement and performance.

- These innovations can accelerate project timelines by as much as 40%, a critical factor in both commercial roofing sector and residential refurbishment projects, while ensuring durable waterproofing membrane compatibility.

What challenges does the Roofing Insulation Adhesives Industry face during its growth?

- Strict environmental regulations and associated compliance costs present a significant challenge to industry growth.

- The market faces significant operational and regulatory challenges. Raw material volatility, particularly for key inputs like polyols and isocyanates, can increase production costs by over 20% during periods of geopolitical instability. These supply chain disruptions are compounded by logistical hurdles that have increased transit times by up to 30% in some lanes.

- Furthermore, the chronic skilled labor shortage remains a primary constraint, with the construction industry facing a deficit of nearly half a million workers, impacting the adoption of advanced two-component polyurethane adhesive systems that require precise application.

- Stricter environmental rules mandating low-VOC formulations and weather resilience enhancement add another layer of complexity, requiring significant R&D investment for compliance and increasing the cost of both logistics center construction and building stock renovation.

Exclusive Technavio Analysis on Customer Landscape

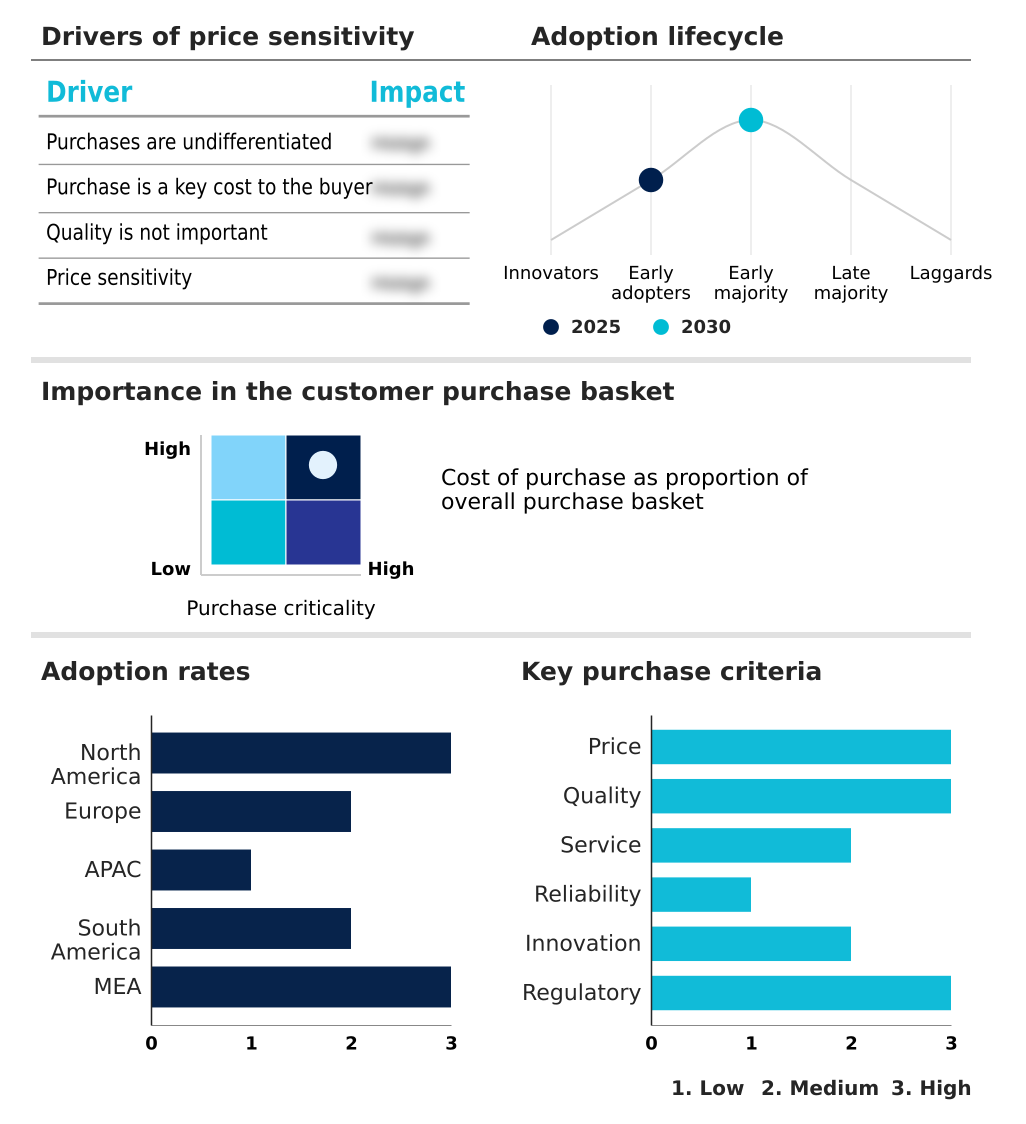

The roofing insulation adhesives market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the roofing insulation adhesives market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Roofing Insulation Adhesives Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, roofing insulation adhesives market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3M Co. - Specialized adhesive technologies address complex bonding challenges in high-performance construction and industrial assemblies.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- ALTENLOH, BRINCK and CO. INC.

- Apollo Roofing Solutions Ltd.

- Arkema Group

- BASF SE

- Dow Chemical Co.

- DuPont de Nemours Inc.

- GAF Materials LLC

- H.B. Fuller Co.

- Henkel AG and Co. KGaA

- Huntsman International LLC

- IKO Industries Ltd.

- Johns Manville Corp.

- Mapei SpA

- OMG Inc.

- Paramelt Rmc BV

- Sika AG

- Tremco CPG Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Roofing insulation adhesives market

- In August 2024, Sika Roofing announced the launch of SikaFast 3341, a specialized adhesive engineered to bond to PVDF resin-based metal coatings, addressing a significant challenge in the industry.

- In November 2024, Holcim acquired OX Engineered Products, a provider of wall insulation and sheathing solutions, to expand its building envelope division and offer more integrated energy efficiency systems.

- In December 2024, H.B. Fuller Co. divested its flooring business to Pacific Avenue Capital Partners, leading to a reorganization of its construction segments into a new global business unit named Building Adhesive Solutions.

- In March 2025, Sika acquired Cromar Building Products, a UK-based provider of roofing and waterproofing systems, to strengthen its distribution channels and better serve the renovation sector in Europe.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Roofing Insulation Adhesives Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 290 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.3% |

| Market growth 2026-2030 | USD 847.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.8% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, Indonesia, South Korea, Australia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The roofing insulation adhesives market is defined by a strategic shift towards high-performance bonding solutions that address critical industry challenges. Boardroom decisions are now heavily influenced by the need to balance regulatory pressures, such as fire safety code compliance and low-VOC formulations, with operational efficiency. The core technology revolves around achieving superior substrate adhesion strength and ensuring building envelope integrity.

- Innovations in two-component polyurethane adhesive and moisture-curing polymers are central to this, enabling effective TPO membrane adhesion and PVC roofing chemical bonding. The push for thermal bridge elimination has made products like low-rise polyurethane foam essential for polyisocyanurate (ISO) insulation and expanded polystyrene (EPS) bonding.

- Advanced reaction-curing adhesive systems have demonstrated the ability to reduce installation labor by up to 30%, a compelling metric for an industry grappling with labor shortages. This evolution underscores a move away from commoditized products toward specialized chemistries that offer guaranteed performance in critical applications like vapor retarder bonding and structural deck preservation, shaping long-term product strategy and investment.

What are the Key Data Covered in this Roofing Insulation Adhesives Market Research and Growth Report?

-

What is the expected growth of the Roofing Insulation Adhesives Market between 2026 and 2030?

-

USD 847.4 million, at a CAGR of 7.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Two-component roofing insulation adhesives, and One-component roofing insulation adhesives), End-user (Non-residential, and Residential), Distribution Channel (Indirect sales, and Direct sales) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Stringent energy efficiency mandates and decarbonization of building stock, Strict environmental regulations and compliance costs

-

-

Who are the major players in the Roofing Insulation Adhesives Market?

-

3M Co., ALTENLOH, BRINCK and CO. INC., Apollo Roofing Solutions Ltd., Arkema Group, BASF SE, Dow Chemical Co., DuPont de Nemours Inc., GAF Materials LLC, H.B. Fuller Co., Henkel AG and Co. KGaA, Huntsman International LLC, IKO Industries Ltd., Johns Manville Corp., Mapei SpA, OMG Inc., Paramelt Rmc BV, Sika AG and Tremco CPG Inc.

-

Market Research Insights

- The dynamics of the roofing insulation adhesives market are shaped by a strategic focus on performance and efficiency. The adoption of advanced cold-applied adhesives is accelerating, with some systems reducing installation time by over 30% compared to traditional hot-mop methods, directly addressing the industry's skilled labor shortage. This shift supports job site safety enhancement and allows for year-round construction.

- Concurrently, the proliferation of green roofing systems and sustainable construction materials is driving demand for specialized formulations. Adhesives used in these assemblies deliver up to 25% greater shear strength to support vegetative loads while ensuring waterproofing membrane compatibility. This focus on specialized, high-performance bonding solutions underscores the market's response to modern architectural and environmental demands.

We can help! Our analysts can customize this roofing insulation adhesives market research report to meet your requirements.

RIA -

RIA -