Rubber Processing Chemicals Market Size 2025-2029

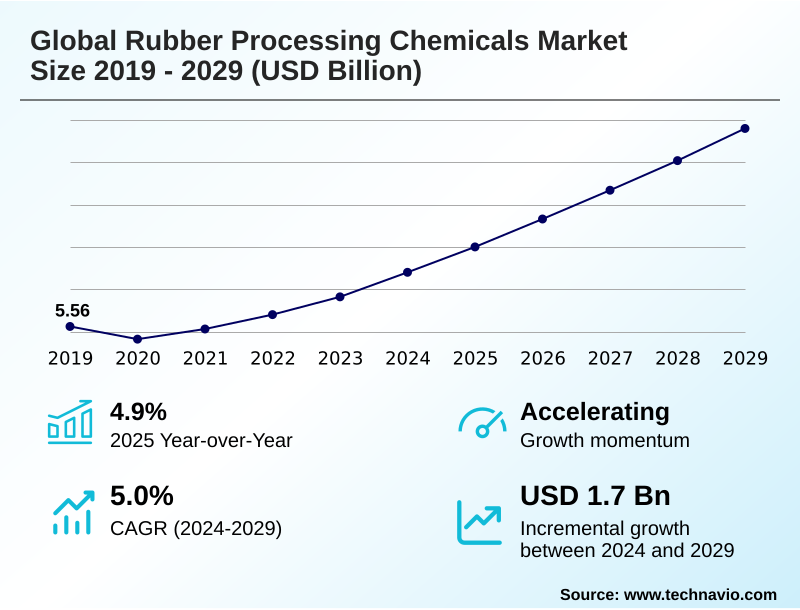

The rubber processing chemicals market size is valued to increase by USD 1.70 billion, at a CAGR of 5% from 2024 to 2029. Robust automotive sector growth and electric vehicle transition will drive the rubber processing chemicals market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 42% growth during the forecast period.

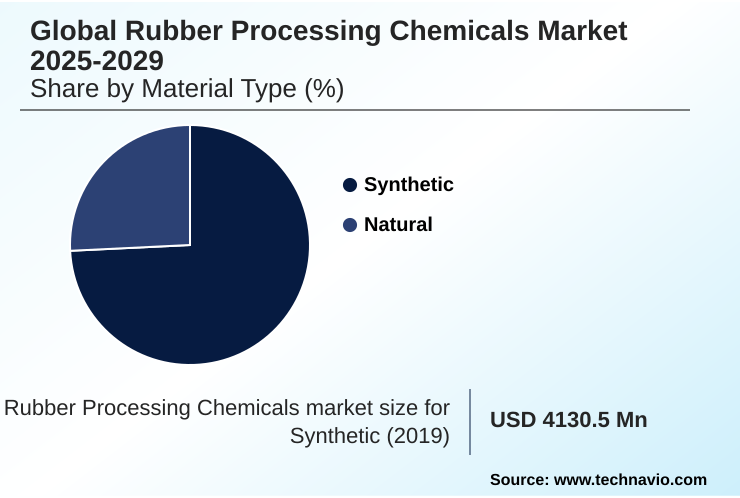

- By Material Type - Synthetic segment was valued at USD 4.46 billion in 2023

- By Type - Tire segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 2.34 billion

- Market Future Opportunities: USD 1.70 billion

- CAGR from 2024 to 2029 : 5%

Market Summary

- The rubber processing chemicals market is integral to manufacturing durable rubber products, where additives enhance material properties for demanding applications. Key drivers include sustained growth in the automotive sector, propelled by the transition to electric vehicles which require high-performance tires with unique characteristics like superior wear resistance and low rolling resistance.

- This shift drives demand for advanced vulcanization accelerators and silane coupling agents. A significant trend is the industry-wide pivot to sustainability, compelled by stringent regulations and corporate esg mandates.

- For instance, a tire manufacturer aiming to incorporate 30% recycled content into a new product line must reformulate its compounds, using specialized processing aids and devulcanizing agents to ensure performance parity with virgin materials. This scenario highlights the market's evolution, balancing innovation against challenges like raw material price volatility and the high cost-of-compliance.

What will be the Size of the Rubber Processing Chemicals Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Rubber Processing Chemicals Market Segmented?

The rubber processing chemicals industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Material type

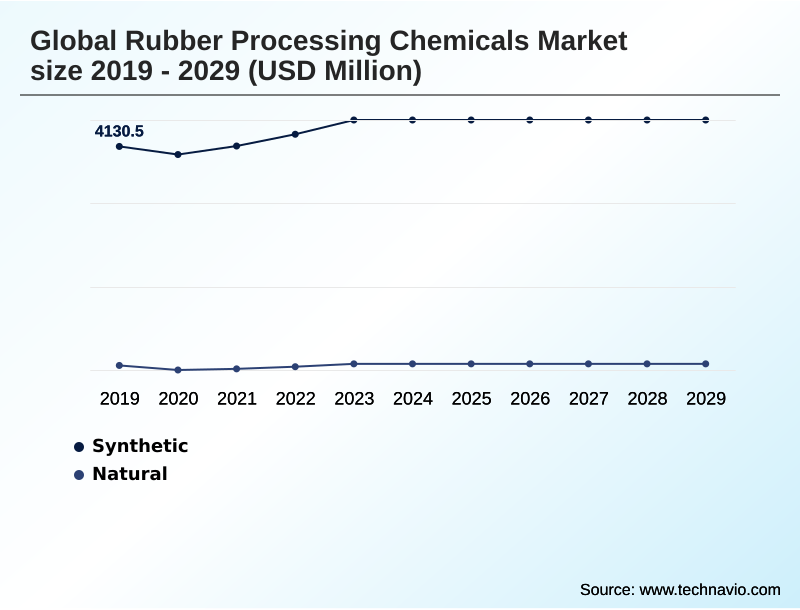

- Synthetic

- Natural

- Type

- Tire

- Non Tire

- Product

- Accelerators

- Anti degradants

- Flame retardants

- Processing aid

- Others

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of World (ROW)

- APAC

By Material Type Insights

The synthetic segment is estimated to witness significant growth during the forecast period.

The market for chemicals used in synthetic rubber is driven by relentless innovation. Tailoring material characteristics for applications where natural rubber is unsuitable is enabled by the strategic use of rubber processing chemicals, including specific vulcanization accelerators and processing aids.

Polymers like SBR and BR require optimized cure package systems to manage the vulcanization process and avoid issues such as the reversion phenomenon.

For EPDM, which is prized for its weathering resistance, a distinct set of antidegradants and antiozonants is essential to prevent flex-cracking fatigue.

The industry is also using material informatics to assess the ecotoxicity profile of new compounds, with some new polymers featuring up to 75% bio-based content, requiring a unique activator complex for effective crosslinking.

The Synthetic segment was valued at USD 4.46 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 42% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Rubber Processing Chemicals Market Demand is Rising in APAC Get Free Sample

The geographic landscape is dominated by the APAC region, which accounts for over 42% of incremental growth opportunities, driven by its manufacturing prowess.

This region is a major consumer of high-volume polymers like styrene-butadiene rubber (sbr) and polybutadiene rubber (br) for the tire industry.

In contrast, mature markets in North America and Europe focus on specialty applications, such as nitrile rubber (nbr) for industrial hoses and ethylene propylene diene monomer (epdm) for automotive seals.

Regulatory pressures concerning chemicals like p-phenylenediamine (ppd) and its derivative 6ppd-quinone are highest in these western regions. Investment in advanced process control systems is helping improve batch-to-batch consistency globally.

The adoption of predictive modeling is also on the rise, while nearshoring strategies aimed at reducing reliance on single-source suppliers of silica fillers can decrease supply chain lead times by up to 20%.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global rubber processing chemicals market 2025-2029 is undergoing a significant transformation, driven by both technological innovation and stringent regulatory pressures. The quest for sustainable antiozonant alternatives to 6ppd has become a top R&D priority, directly linked to the development of high-performance chemicals for ev tires, where balancing durability and efficiency is paramount.

- Digitalization in rubber compound formulation is accelerating this process, enabling faster development of solutions that address the impact of reach on rubber chemicals. This has led to the rapid commercialization of non-nitrosamine generating vulcanization accelerators. A key focus area is reducing rolling resistance with advanced silica fillers, which is impossible without advanced silane coupling agents for synthetic rubber.

- The industry's sustainability goals are further advanced by the use of bio-based processing aids for sustainable rubber and new chemical solutions for devulcanized elastomers. In construction, demand for halogen-free flame retardants for construction is growing. On the factory floor, improving cure characteristics of natural rubber remains a core competency, often achieved with multi-functional additives for process efficiency.

- Companies are also developing specialized processing aids for recycled tire materials. While these innovations drive value, suppliers must also provide cost-effective commodity chemicals for tire manufacturing to remain competitive. Niche growth is found in specialty antidegradants for industrial hoses and high-strength bonding agents for rubber-to-metal applications.

- Strategically, firms are focused on managing raw material price volatility, with some finding that supply chain regionalization in chemical production can reduce exposure by 10% compared to global sourcing models. This involves developing new strategies for navigating complex regulatory frameworks, including understanding the chemical requirements for seismic isolation bearings.

What are the key market drivers leading to the rise in the adoption of Rubber Processing Chemicals Industry?

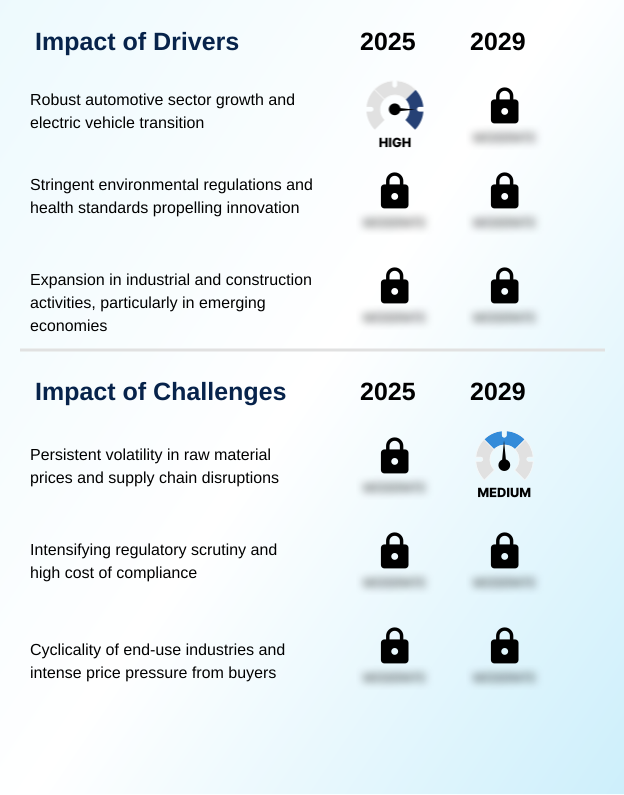

- The market's primary driver is the robust growth of the automotive sector, significantly amplified by the global transition toward electric vehicles.

- The evolution of the automotive industry is a primary market driver, with the transition to EVs creating demand for specialized rubber compounds and the associated chemicals.

- The need for lightweighting components to increase vehicle range by up to 5% fuels innovation in materials that depend on specific bonding agents and blowing agents to reduce weight by 10% without sacrificing performance.

- This trend necessitates advanced cure characteristics and excellent scorch safety during processing. Beyond automotive, expansion in construction drives demand for products like seismic isolation bearings and materials incorporating flame retardants like aluminum trihydrate (ath).

- The use of pre-vulcanization inhibitors is critical in these complex applications. Demand from these diverse sectors provides market stability, balancing the intense buyer bargaining power found in the automotive sphere.

What are the market trends shaping the Rubber Processing Chemicals Industry?

- The market is experiencing a significant trend defined by the accelerating industry-wide shift toward sustainable and green rubber processing chemicals. This movement is driven by corporate ESG mandates and increasing consumer demand for environmentally responsible products.

- A defining trend is the industry-wide pivot to sustainability, driven by corporate esg mandates and the high cost-of-compliance with environmental regulations. This manifests in the adoption of circular economy principles through chemicals that support the use of ground tire rubber (gtr) and devulcanized elastomers, improving material efficiency by over 15%.

- There is a strong push away from traditional petrochemical feedstocks toward bio-based feedstocks to reduce carbon footprints by up to 25%. This shift fuels demand for innovative products like non-nitrosamine generating accelerators and halogen-free flame retardants (hffr).

- The development of multi-functional additives and advanced silane coupling agents that are more sustainable further exemplifies this trend, reshaping supplier-customer dynamics and supply chain visibility.

What challenges does the Rubber Processing Chemicals Industry face during its growth?

- Persistent volatility in raw material prices, coupled with frequent supply chain disruptions, presents a key challenge to the industry's growth trajectory.

- A persistent challenge is economic volatility, which impacts raw material prices derived from petrochemicals, with costs fluctuating over 30% in a single quarter. This complicates forecasting for export-oriented manufacturing. Furthermore, intensifying regulatory scrutiny, such as new rules on non-exhaust particulate emissions, adds significant compliance costs, which can increase overhead by 15%.

- Manufacturers must constantly innovate the polymer matrix to improve wear resistance and rolling resistance while managing these financial pressures. Optimizing the crosslinking reaction to build a robust vulcanizate network and ensuring ideal rheological properties are constant technical hurdles. Poor polymer-filler interaction can undermine performance, making material science expertise critical in this demanding environment.

Exclusive Technavio Analysis on Customer Landscape

The rubber processing chemicals market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the rubber processing chemicals market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Rubber Processing Chemicals Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, rubber processing chemicals market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Akzo Nobel NV - Delivers patented bimodal epoxy technology for advanced chemical-resistant linings, enhancing durability and performance in harsh industrial environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Akzo Nobel NV

- Arkema Group

- BASF SE

- China Petrochemical Corp.

- CHINA SUNSINE LTD.

- Eastman Chemical Co.

- Finorchem Ltd

- Flexsys Inc.

- Kemai Chemical Co. Ltd.

- Kumho Petrochemical Co. Ltd.

- Lanxess AG

- NOCIL Ltd.

- R.T. Vanderbilt Holding Co. Inc.

- Sennics Co Ltd.

- Huatai Chemical Co Ltd.

- Solvay SA

- Sumitomo Chemicals

- Willing Materials Co Ltd.

- Zhedongxlangzhu Co Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Rubber processing chemicals market

- In August, 2024, GreenChem Innovations acquired BioFormulate Solutions, a specialist in bio-based processing aids derived from plant oils, for USD 75 million to bolster its sustainable chemicals portfolio.

- In November, 2024, EuroChem Advanced Materials launched its new line of 'NitroSafe' vulcanization accelerators, becoming the first major producer to offer a complete portfolio of non-nitrosamine generating alternatives compliant with upcoming EU regulations.

- In February, 2025, OmniPlast Technologies announced a strategic partnership with DataChem AI to integrate a predictive modeling platform into its R&D process, aiming to reduce new rubber compound development time by 40%.

- In May, 2025, AsiaChem Group broke ground on a new USD 200 million manufacturing facility in Mexico to produce high-performance antidegradants and specialty chemicals for the growing North American electric vehicle tire market.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Rubber Processing Chemicals Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 295 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5% |

| Market growth 2025-2029 | USD 1702.4 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 4.9% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, Saudi Arabia, South Africa, UAE, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The rubber processing chemicals market is defined by its role in transforming raw natural rubber and synthetic rubber into high-performance materials. The vulcanization process relies on a complex interplay of vulcanization accelerators, antidegradants, and processing aids to build a robust vulcanizate network.

- Key polymers like styrene-butadiene rubber (sbr), polybutadiene rubber (br), and nitrile rubber (nbr) require specific formulations to optimize cure characteristics. For instance, achieving ideal scorch safety and rheological properties is critical.

- A boardroom-level focus on sustainability is reshaping portfolios, driving investment in non-nitrosamine generating alternatives and bio-based feedstocks to mitigate risks associated with chemicals like p-phenylenediamine (ppd) and its derivative, 6ppd-quinone. Innovations in ethylene propylene diene monomer (epdm) compounds demand superior antiozonants.

- The push for EV efficiency has intensified focus on reducing rolling resistance and improving wear resistance, dependent on the polymer-filler interaction between silica fillers and the polymer matrix, facilitated by silane coupling agents. This has led to a 15% improvement in tread life for some premium tire lines.

- The industry is also developing halogen-free flame retardants (hffr) such as aluminum trihydrate (ath) and magnesium dihydroxide (mdh), alongside specialized bonding agents, blowing agents, and pre-vulcanization inhibitors. This includes multi-functional additives that enhance the crosslinking reaction and facilitate use of ground tire rubber (gtr) and devulcanized elastomers.

What are the Key Data Covered in this Rubber Processing Chemicals Market Research and Growth Report?

-

What is the expected growth of the Rubber Processing Chemicals Market between 2025 and 2029?

-

USD 1.70 billion, at a CAGR of 5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Material Type (Synthetic, and Natural), Type (Tire, and Non Tire), Product (Accelerators, Anti degradants, Flame retardants, Processing aid, and Others) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Robust automotive sector growth and electric vehicle transition, Persistent volatility in raw material prices and supply chain disruptions

-

-

Who are the major players in the Rubber Processing Chemicals Market?

-

Akzo Nobel NV, Arkema Group, BASF SE, China Petrochemical Corp., CHINA SUNSINE LTD., Eastman Chemical Co., Finorchem Ltd, Flexsys Inc., Kemai Chemical Co. Ltd., Kumho Petrochemical Co. Ltd., Lanxess AG, NOCIL Ltd., R.T. Vanderbilt Holding Co. Inc., Sennics Co Ltd., Huatai Chemical Co Ltd., Solvay SA, Sumitomo Chemicals, Willing Materials Co Ltd. and Zhedongxlangzhu Co Ltd.

-

Market Research Insights

- Market dynamics are increasingly shaped by strategic responses to economic volatility and a focus on operational excellence. Companies are leveraging advanced supply chain visibility tools to mitigate the impact of fluctuating petrochemical feedstocks, with leading firms reducing logistical delays by over 15%. The high buyer bargaining power of major tire manufacturers necessitates a focus on value, not just cost.

- Adherence to stringent standards, such as tire labeling regulation, drives innovation in high-purity chemicals. This push for performance is balanced by a nearshoring trend aimed at improving just-in-time delivery capabilities, which has proven to cut inventory carrying costs by up to 20% in certain supply chains. Navigating this landscape requires balancing price sensitivity with the high cost-of-compliance.

We can help! Our analysts can customize this rubber processing chemicals market research report to meet your requirements.

RIA -

RIA -