Sandwich Panels Market Size 2024-2028

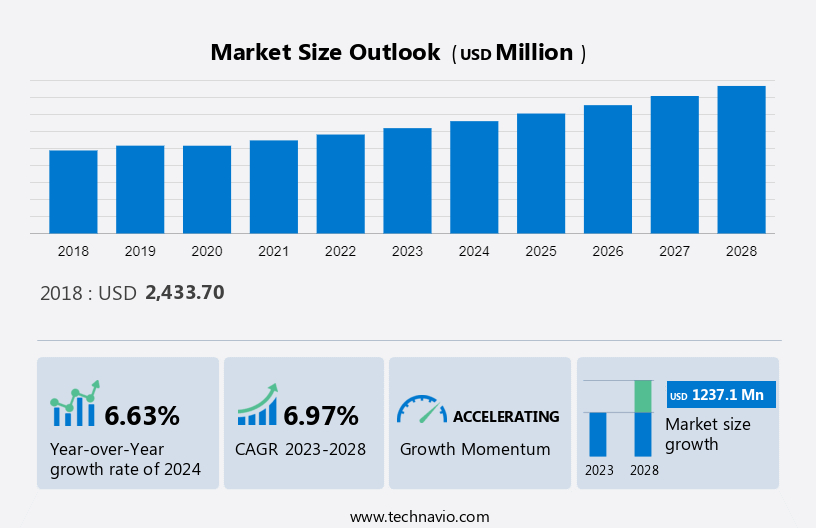

The sandwich panels market size is forecast to increase by USD 1.23 billion at a CAGR of 6.97% between 2023 and 2028. Market growth is propelled by various factors, notably the benefits offered by sandwich panels, such as enhanced insulation and structural strength. These panels cater to the rising demand for energy-efficient buildings, aligning with sustainability goals and reducing operational costs. Additionally, the expanding construction industry plays a pivotal role, driving the adoption of innovative building materials like sandwich panels. Their versatility and ease of installation make them a preferred choice for modern construction projects. As the focus on eco-friendly and cost-effective solutions intensifies, sandwich panels continue to gain traction, contributing significantly to the growth and development of the construction sector while meeting evolving market demands.

What will be the Size of the Market During the Forecast Period?

To learn more about this report, View Report Sample

Market Dynamics and Customer Landscape

The Market is driven by rising demand from the food and beverage sector and chemical sector for energy-efficient, insulated, and durable construction materials. Trends include the integration of high-performance materials like composite materials to meet stringent standards while reducing carbon footprints. Challenges such as labor shortages and economic uncertainties impact market growth and recovery efforts. However, advancements in advanced interiors and structural insulated panels cater to the industrial segment, especially in warehouses and cold storage facilities, emphasizing energy-saving materials and cold storage technology. Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Key Market Driver

The several advantages of sandwich panels are the key factors driving the growth of the global market. There are several advantages of using sandwich panels that are driving their demand, such as the fast and easy installation, perfect thermal insulation, and provides the aesthetic appearance of the buildings. In a fast and easy installation process, contrary to conventional systems, continuous-line manufactured sandwich panels come in fully compatible, ready-to-assemble pieces, and it is also prepared in the required dimensions, insulation types, and colors based on the structure of your facility.

Moreover, these have been thermally insulated to ensure that your structure will be sturdy and long-lasting by preventing issues like mold and humidity brought on by heat movements and condensation. The thickness of the insulation used in it varies depending on the structure's ability to support its weight, the climate in the area, the building's intended use, and the thermal insulation value. It provides aesthetic appearances to the buildings, and the end-users can make a variety of designs with sandwich panels because they can be employed in internal portions as well. Such factors are expected to fuel the growth of the global market during the forecast period.

Significant Market Trends

An increase in demand for sandwich panels in cold storage is the primary trend in the global market growth. They are becoming an increasingly popular solution for refrigeration applications as demand has steadily increased in recent years. This is mainly due to the many advantages these panels offer, making them an excellent choice for cold store owners. One of the main factors driving the demand for these for refrigeration is their excellent insulation capacity. A sandwich panel consists of two outer layers of metal or other material with insulations sandwiched between them. This design minimizes heat transfer between the inside and outside of the unit, keeping the temperature inside stable. This is important for refrigerated warehouses where products need to be kept at specific temperatures to prevent spoilage and maintain quality.

Additionally, they are easy and quick to install, which is another reason for their increasing popularity in cold storage. The panels can be cut to fit the specific dimensions of the facility and can be installed rapidly with minimal disruption to the ongoing operations. This can be especially beneficial for facilities that need to start operations quickly or are undergoing renovations or expansions. Moreover, sandwich panels offer an aesthetically pleasing appearance, which can enhance the overall appeal of the facility. Thus, the above-mentioned factors are expected to fuel the growth of the global market during the forecast period.

Major Market Challenge

The volatility of raw material prices is a major challenge to the growth of the global market. The sandwich panel industry faces major challenges due to volatility in raw material prices. This issue has adversely affected the global sandwich panel market in recent years, causing price hikes, production delays, and supply chain disruptions. Key raw materials such as polyurethane, polystyrene, and mineral wool used in sandwich panels are highly dependent on oil prices. Fluctuations in oil prices, therefore, have a direct impact on raw material costs. The oil industry has experienced several ups and downs in recent years, which has caused commodity prices to skyrocket.

Moreover, the uncertainty caused by the volatile prices of raw materials has also affected the production process, leading to delays and supply chain disruptions. Manufacturers can no longer assure timely delivery to clients, who then must bear additional costs such as storage fees or delays in their projects. In addition, the cost of transportation has also increased due to the rise in raw material prices. This has impacted the shipping of sandwich panels across various regions, resulting in higher transportation costs, further contributing to price escalation. Thus, such factors are expected to hinder the growth of the market in focus during the forecast period.

Market Customer Landscape

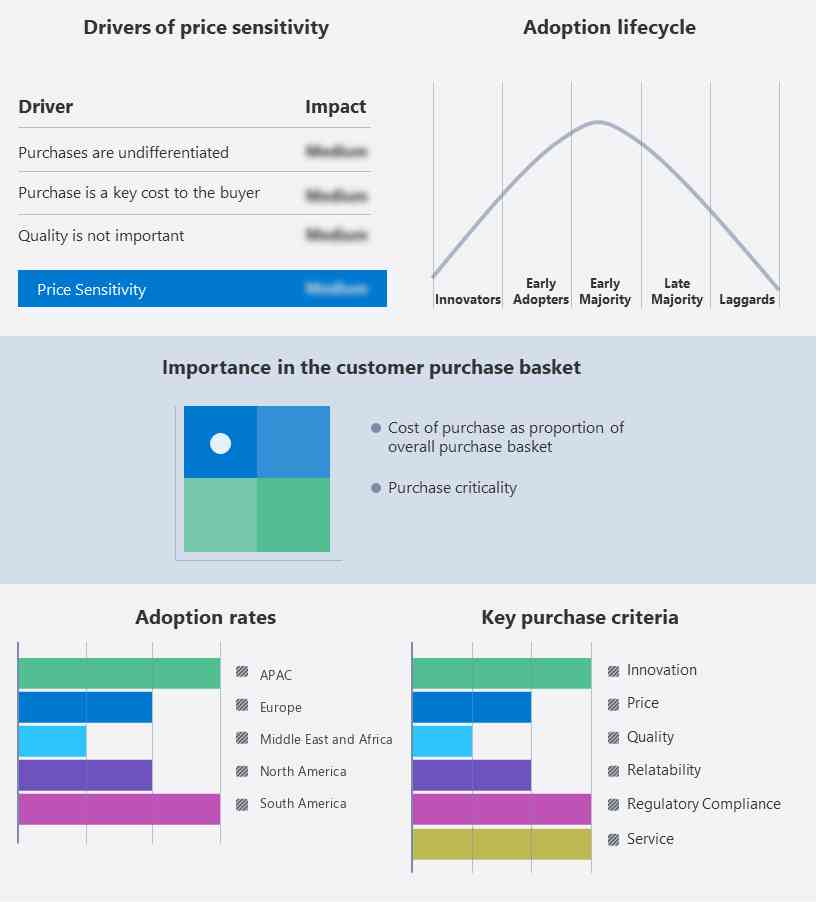

The sandwich panels industry analysis report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Market Customer Landscape

Who are the Major Market Players?

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Italpannelli Srl: The company offers sandwich panels such as PUF, EPS, and insulated. Also, the company offers insulating sandwich panels.

The sandwich panels industry analysis report also includes detailed analyses of the competitive landscape of the market and information about 17 market companies, including:

- Alubel Spa

- ArcelorMittal SA

- ArmaPanel

- Assan Panel A.S

- DANA Group of Companies

- Izopanel sp. z o.o.

- Kingspan Group Plc

- Lattonedil Spa Milan

- Manni Group S.r.l.

- Metecno Group

- Nucor Corp.

- Panel Tech International LLC

- Romakowski GmbH and Co. KG

- Sika AG

- Sintex Plastics Technology Ltd.

- SSAB AB

Qualitative and quantitative market growth and forecasting analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. In market growth analysis, data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Segmentation

The market is a crucial player in the construction sector, offering innovative solutions driven by composite materials and high-performance materials. With a focus on energy efficiency and insulation, these panels are highly sought-after in sectors like the food and beverage industry and the chemical sector. They play a vital role in industrial buildings, warehouses, and cold storage facilities, catering to the rising demand for energy-saving materials and sustainable construction practices. One of the key advantages of sandwich panels is their durability coupled with being lightweight, making them ideal for applications in advanced interiors and structural insulated panels. They contribute significantly to reducing carbon footprints in the built environment while offering exceptional insulation properties.

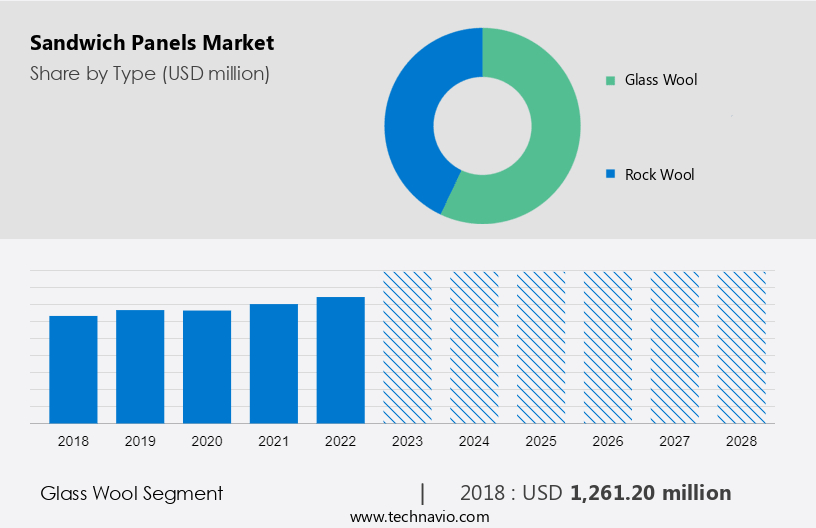

By Type

The market share growth by the glass wool segment will be significant during the forecast period. Glass wool is a popular insulation material used in sandwich panels around the world. Sandwich panels are composite structures consisting of two thin, strong face sheets and a core material that provides insulation and rigidity.

Get a glance at the market contribution of various segments View the PDF Sample

The glass wool segment was valued at USD 1.26 billion in 2018. Glasswool-based sandwich panels are widely used in residential, commercial, and industrial building construction, as well as refrigeration and refrigeration applications. Glass wool-based sandwich panels are known for their excellent insulating properties and low thermal conductivity materials that help reduce heat loss and improve energy efficiency, making them ideal for use in buildings in the colder regions of the world.

By Region

For more insights on the market share of various regions Download PDF Sample now!

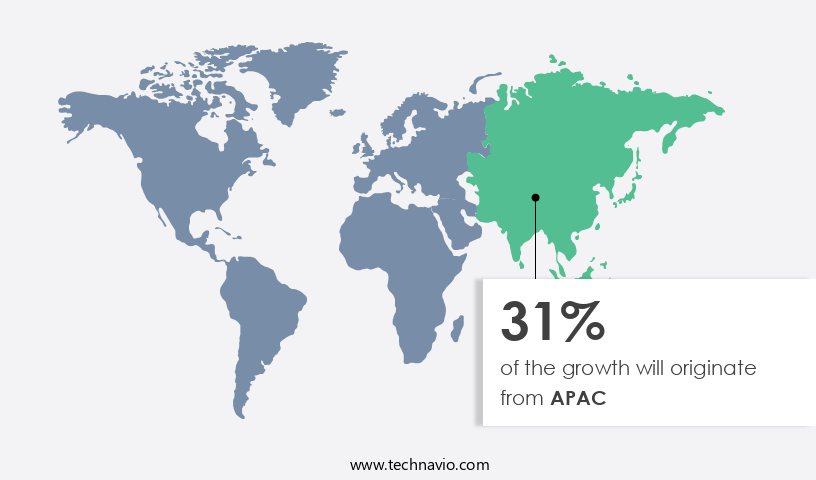

APAC is estimated to contribute 31% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. The growing demand for energy-efficient construction materials and the increasing focus on sustainable building practices are major factors driving the demand for sandwich panels in the APAC region. This is due to the rising disposable income and changing lifestyle of consumers in the region have led to a surge in demand for residential and commercial buildings, thereby driving the demand for sandwich panels. Moreover, the APAC region is witnessing a shift towards green building practices, which emphasizes the use of energy-efficient and sustainable materials. With their superior insulating properties and durability, sandwich panels are increasingly favored over traditional building materials, such as brick and cement. Such factors will accelerate the market growth during the forecast period.

Segment Overview

The market research report provides comprehensive data (region wise segment analysis), with forecasts and estimates in "USD Billion" for the period 2024 to 2028, as well as historical data from 2018 to 2022 for the following segments.

- Type Outlook

- Glass wool

- Rock wool

- Application Outlook

- Commercial

- Residential

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- U.K.

- Germany

- France

- Rest of Europe

- APAC

- China

- India

- South America

- Chile

- Argentina

- Brazil

- Middle East & Africa

- Saudi Arabia

- South Africa

- Rest of the Middle East & Africa

- North America

You may also interested in the below market reports

-

Structural Insulated Panels Market: by Application, Product, and Geography - Forecast and Analysis

-

Composite Insulated Panels Market: by Product and Geography - Forecast and Analysis

-

Aluminum Composite Panels Market: by Type, End-user and Geography - Forecast and Analysis

Market Analyst Overview

The Market is influenced by a range of factors shaping modern construction practices. Composite materials are at the forefront, offering lightweight solutions ideal for addressing labor shortages and boosting industrialization efforts. Amid economic uncertainties, the market emphasizes energy-saving materials like structural insulated panels and solar panels, catering to non-residential applications such as industrial buildings, cold storage facilities, and institutional buildings. Moreover, these panels excel in fire performance and are favored in the non-residential sector by entities like retail food chains, multinational companies, and warehouses due to their contribution to reducing carbon footprints. They enhance the shelf life of agricultural produce, seafood, and frozen food, which is critical in industries like food and beverage and cold chain.

Furthermore, their application extends to chemical, medical, and pharmaceutical sectors, ensuring optimal storage conditions for photographic film, chemicals, and pharmaceutical drugs. Key players like GIC, DLF, and Wiskind drive market recovery and promote high-performance materials for finished construction and advanced interiors. The cold storage technology segment benefits significantly, meeting the stringent requirements of cold chain industries while advancing sustainability goals and adapting to evolving market demands.

Furthermore, the Market is a dynamic sector driven by diverse industries and factors. Utilizing materials like steel and aluminum, these panels offer exceptional structural integrity and thermal insulation, making them popular in residential buildings, warehouses, and cold storage facilities across the globe. Their versatility extends to applications in the food and beverage, chemical, and medical sectors, ensuring optimal conditions for pharmaceutical items and perishable goods. Investments and funds play a crucial role in driving market growth, supporting innovation, and technological advancements in cladding material application. The market's performance is closely tied to economic indicators such as GDP, reflecting the demand for sustainable and efficient construction solutions in the industrial segment and beyond.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

156 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.97% |

|

Market growth 2024-2028 |

USD 1.23 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.63 |

|

Regional analysis |

APAC, North America, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 31% |

|

Key countries |

US, China, India, Germany, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Alfa Peb Ltd., Alubel Spa, ArcelorMittal SA, ArmaPanel, Assan Panel A.S, DANA Group of Companies, Italpannelli Srl, Izopanel sp. z o.o., Kingspan Group Plc, Lattonedil Spa Milan, Manni Group S.r.l., Metecno Group, Nucor Corp., Panel Tech International LLC, PortaFab Corp., Romakowski GmbH and Co. KG, Sika AG, Sintex Plastics Technology Ltd., SSAB AB, Tata Sons Pvt. Ltd., and Technical Supplies and Service Co. LLC |

|

Market dynamics |

Parent market analysis, Market Forecasting, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, Market growth and Forecasting, COVID 19 impact and recovery analysis and future consumer dynamics, Market condition analysis for market forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting of the market between 2024 and 2028

- Precise estimation of the size of the market size and its contribution to the parent market

- Accurate predictions about upcoming market trends and analysis and changes in consumer behavior

- Growth of the market industry across Europe, North America, APAC, South America, and Middle East and Africa

- Thorough market growth analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive market analysis and report on the factors that will challenge the market research and growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -