Structural Insulated Panels Market Size 2026-2030

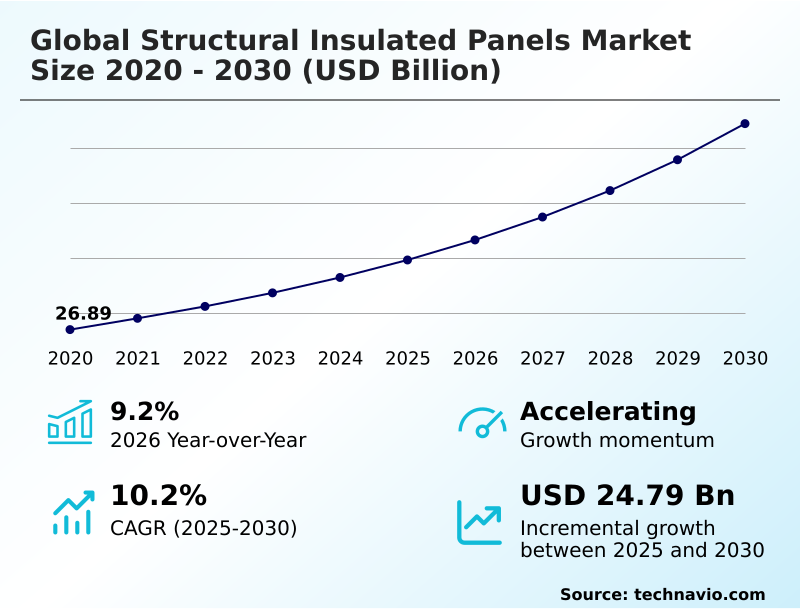

The structural insulated panels market size is valued to increase by USD 24.79 billion, at a CAGR of 10.2% from 2025 to 2030. Rising demand for green building construction materials will drive the structural insulated panels market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 36.3% growth during the forecast period.

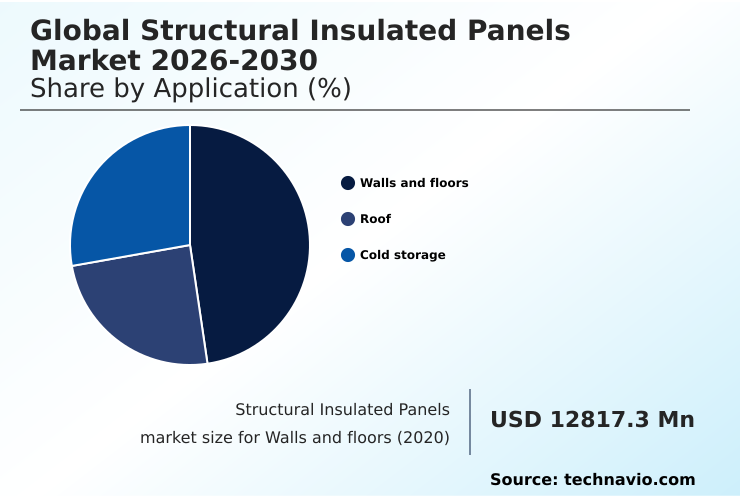

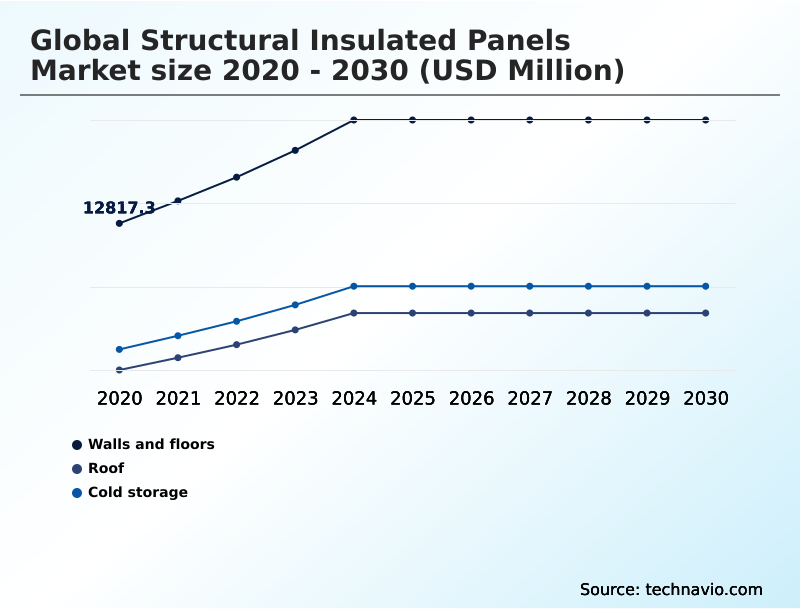

- By Application - Walls and floors segment was valued at USD 17.20 billion in 2024

- By Product - Polystyrene segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 37.45 billion

- Market Future Opportunities: USD 24.79 billion

- CAGR from 2025 to 2030 : 10.2%

Market Summary

- The structural insulated panels market is advancing beyond niche applications into the mainstream of residential and light commercial construction. This evolution is driven by a convergence of factors, primarily the urgent need for more energy-efficient buildings to meet tightening regulations and sustainability goals. These systems offer a compelling solution by combining structural support and insulation into a single, factory-produced component.

- For instance, a residential developer facing skilled labor shortages and tight deadlines can utilize panelized construction to erect building envelopes in a fraction of the time required for traditional methods, substantially reducing on-site labor costs and build cycles. This efficiency is critical in addressing housing deficits. However, the market is not without its complexities.

- The reliance on raw materials like oriented strand board and foam insulation exposes manufacturers and builders to price volatility, impacting project budgets and cost competitiveness against conventional construction techniques.

- Furthermore, market penetration is contingent on overcoming builder inertia and investing in training for proper installation to ensure the high-performance benefits, such as superior airtightness and thermal consistency, are fully realized in practice, preventing performance gaps.

What will be the Size of the Structural Insulated Panels Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Structural Insulated Panels Market Segmented?

The structural insulated panels industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Walls and floors

- Cold storage

- Roof

- Product

- Polystyrene

- Polyurethane

- Glass wool

- Others

- End-user

- Residential

- Commercial

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Application Insights

The walls and floors segment is estimated to witness significant growth during the forecast period.

The walls and floors segment is the cornerstone of the structural insulated panel system market, driven by the need for a whole-building system approach to construction.

These prefabricated construction components are essential for creating a high-performance building envelope, directly addressing the construction labor shortage by simplifying on-site work. Demand is accelerating due to stringent energy code compliance and the pursuit of green building certifications.

By integrating structure and insulation, typically with an expanded polystyrene foam core, these panels facilitate accelerated building timelines.

This integrated design approach achieves superior airtightness, with performance tests showing a reduction in air leakage by over 50% compared to traditional framing, fundamentally improving a building's energy consumption profile.

The Walls and floors segment was valued at USD 17.20 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 36.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Structural Insulated Panels Market Demand is Rising in APAC Get Free Sample

The market's geographic landscape is characterized by mature adoption in North America and rapid expansion in the APAC region, which is projected to contribute over 36% of the market's incremental growth.

In North America, stringent building airtightness standards and the prevalence of custom home prefabrication drive demand. Here, resilient construction methods are gaining traction, with systems using oriented strand board facings demonstrating superior performance in extreme weather.

The focus is on achieving superior thermal performance and reduced thermal bridging. In contrast, growth in APAC is fueled by new construction in light commercial applications and the build-out of the cold storage facility insulation infrastructure.

Across all regions, the ability of these systems to enable reduced jobsite waste, often by more than 40%, appeals to sustainability-focused projects.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- A critical consideration for builders and architects is a detailed structural panel r-value comparison, as this metric directly influences a building's long-term energy performance and suitability for specific climate zones. The decision often involves a trade-off analysis of the cost of sip panels vs stick frame construction.

- While initial material expenses for panels may be higher, project managers find that total installed costs can be competitive due to significantly reduced labor hours and faster enclosure times, sometimes shortening schedules by over 30%.

- The benefits of polyurethane foam insulation, including its higher r-value per inch and excellent moisture resistance, make it a preferred choice for high-performance projects, particularly when using sips for net zero homes. However, this choice must be balanced against fire resistance ratings for sips, which are crucial for meeting building codes and ensuring occupant safety.

- For specialized applications, understanding moisture management in sip walls is paramount to guarantee the long-term durability and structural integrity of the building envelope. This is especially true for sip construction for cold climates, where managing condensation and thermal breaks is essential to prevent moisture-related issues and maintain performance throughout the building's lifecycle.

What are the key market drivers leading to the rise in the adoption of Structural Insulated Panels Industry?

- The increasing demand for green building materials is a key driver for market growth, fueled by global sustainability initiatives and stricter energy efficiency regulations.

- Market growth is fundamentally driven by the global push for building energy efficiency. These systems, which act as load-bearing structural elements, are integral to designs for eco-friendly building solutions.

- The off-site manufacturing process allows for the use of advanced insulation materials and ensures consistent quality, which is difficult to replicate with site-built methods. This prefabrication into modular building components directly addresses demands for faster, more predictable construction cycles.

- Furthermore, rigorous structural integrity testing confirms their resilience, making them suitable for climate zone-specific design challenges.

- As regulations tighten, the ability of insulated roofing systems and wall assemblies to meet and exceed thermal performance requirements, improving a building's energy efficiency by over 50%, makes them an increasingly essential construction technology.

What are the market trends shaping the Structural Insulated Panels Industry?

- The increasing market preference for lightweight and durable panels is a significant emerging trend. This shift is driven by the demand for materials that offer both structural integrity and ease of installation.

- A key trend is the growing sophistication of panel technology, emphasizing a systems-based approach rooted in building envelope science. Manufacturers are innovating with advanced engineered wood products and laminated composite structure designs to enhance performance. The adoption of closed-cell insulation foam is becoming more widespread, valued for its superior moisture resistance and a higher r-value insulation measurement.

- This aligns with passive house design principles, which demand exceptional airtightness and thermal control. For builders, the primary benefit is on-site assembly efficiency, with prefabricated systems reducing construction schedules by up to 30%. This speed, combined with long-term operational savings from reduced energy consumption, presents a compelling financial case for both residential and commercial projects.

What challenges does the Structural Insulated Panels Industry face during its growth?

- High material costs represent a key challenge, potentially hindering market growth by affecting the overall affordability of projects utilizing these advanced panels.

- The primary market challenge revolves around material cost volatility and specification complexity. While panelized building systems are key to net-zero energy construction, the fluctuating price of polyurethane foam insulation and structural sheathing materials can complicate project budgeting. Ensuring proper vapor barrier integration and selecting appropriate moisture-resistant panels are critical technical hurdles that require specialized knowledge, impacting adoption rates.

- Furthermore, meeting fire-resistant panel core specifications adds a layer of regulatory complexity and cost. A comprehensive life cycle cost analysis is often necessary to justify the upfront investment, as decision-makers must balance initial expenses against long-term energy savings and contributions to healthy indoor air quality. The panel's compressive strength rating also needs to be carefully matched to application-specific loads.

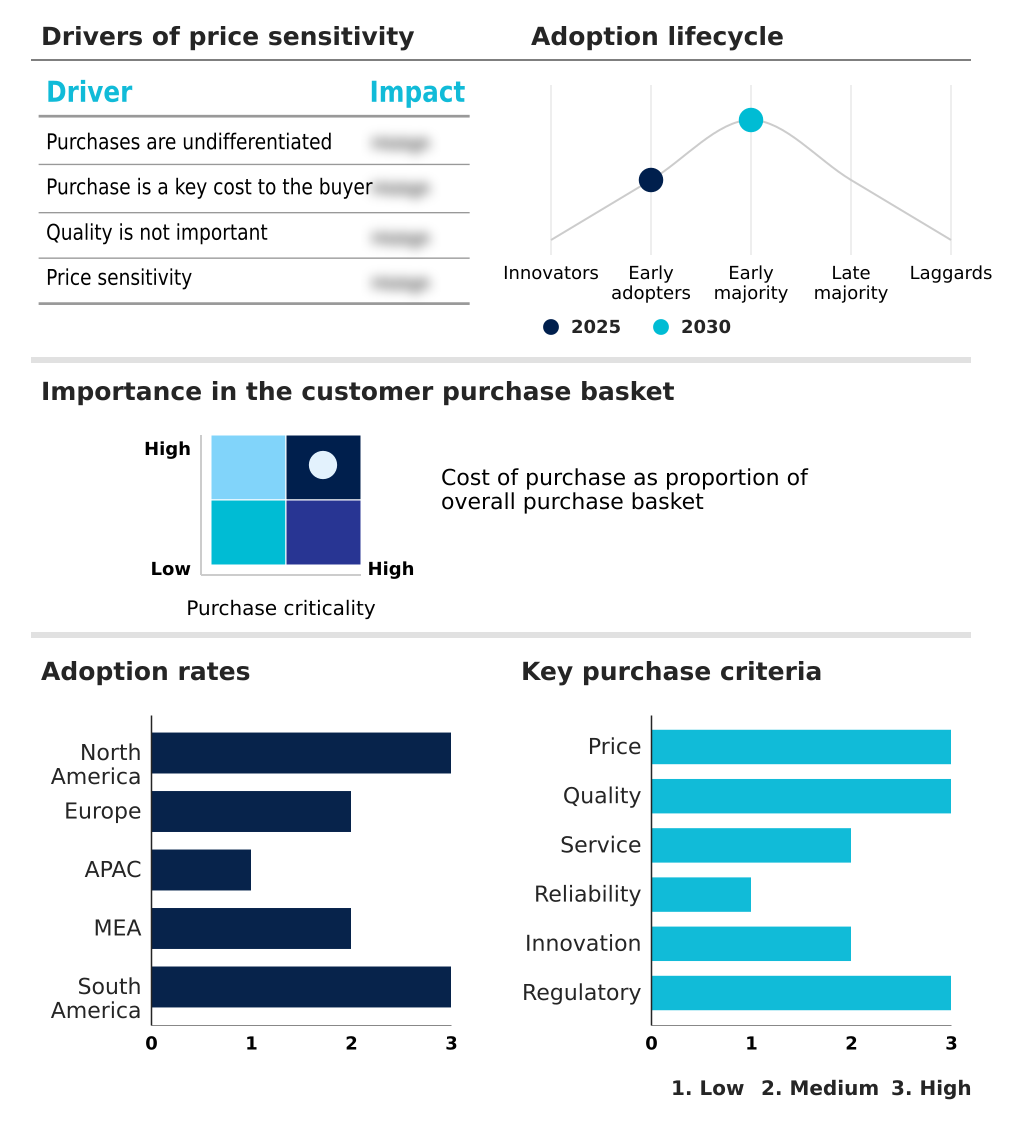

Exclusive Technavio Analysis on Customer Landscape

The structural insulated panels market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the structural insulated panels market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Structural Insulated Panels Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, structural insulated panels market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Acme Panel - Delivers lightweight and durable structural insulated panels engineered for high chemical and biological resistance, meeting advanced construction requirements.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Acme Panel

- All Weather Insulated Panels

- American Insulated Panel

- ArcelorMittal SA

- Balex Metal Sp zoo

- Enercept Inc.

- Extreme Panel Technologies

- Foard Panel

- InGreen Building Systems

- INSULSPAN SIP System

- Isopan Spa

- Kingspan Group Plc

- KPS Global LLC

- Metl Span

- PFB Corp.

- Premier building systems

- RAY-CORE SIPs

- Structural Panels Inc.

- T. Clear Corp.

- ThermaSteel

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Structural insulated panels market

- In November 2024, Kingspan Group Plc announced a strategic partnership with a leading smart home technology firm to embed sensor technology directly into its SIPs for real-time thermal performance monitoring.

- In January 2025, PFB Corp. launched its new 'EcoMax' panel series, featuring a proprietary foam core made from 40% recycled materials and achieving a 15% higher R-value per inch.

- In March 2025, ArcelorMittal SA completed the acquisition of a regional European SIP manufacturer, aiming to integrate steel-faced panels into its portfolio and expand its footprint in the prefabricated building market.

- In May 2025, the California Energy Commission proposed an update to its Title 24 building standards, introducing prescriptive requirements for building envelope airtightness that strongly favor integrated systems like SIPs.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Structural Insulated Panels Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 282 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 10.2% |

| Market growth 2026-2030 | USD 24785.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.2% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The structural insulated panels market is fundamentally reshaping construction paradigms by providing an integrated solution that addresses efficiency, performance, and sustainability. These panelized building systems, typically composed of advanced insulation materials like polyurethane foam insulation and structural sheathing materials, create a high-performance building envelope with superior thermal performance.

- Key to adoption is the off-site manufacturing process, which ensures quality control and enables rapid assembly, a critical advantage for net-zero energy construction projects. Decision-making at the board level now involves evaluating these engineered wood products not just on cost but on their ability to meet evolving building airtightness standards, which can result in energy savings of up to 40%.

- The load-bearing structural elements and laminated composite structure offer design flexibility, while the integration of features like a vapor barrier and the use of moisture-resistant panels ensure durability. A focus on sustainable building materials is driving innovation in fire-resistant panel cores and closed-cell insulation foam.

What are the Key Data Covered in this Structural Insulated Panels Market Research and Growth Report?

-

What is the expected growth of the Structural Insulated Panels Market between 2026 and 2030?

-

USD 24.79 billion, at a CAGR of 10.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Walls and floors, Roof, and Cold storage), Product (Polystyrene, Polyurethane, Glass wool, and Others), End-user (Residential, and Commercial) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Rising demand for green building construction materials, High material costs hinder the market growth

-

-

Who are the major players in the Structural Insulated Panels Market?

-

Acme Panel, All Weather Insulated Panels, American Insulated Panel, ArcelorMittal SA, Balex Metal Sp zoo, Enercept Inc., Extreme Panel Technologies, Foard Panel, InGreen Building Systems, INSULSPAN SIP System, Isopan Spa, Kingspan Group Plc, KPS Global LLC, Metl Span, PFB Corp., Premier building systems, RAY-CORE SIPs, Structural Panels Inc., T. Clear Corp. and ThermaSteel

-

Market Research Insights

- The market is shaped by a dynamic interplay between performance demands and economic realities. The push toward passive house design principles and the need to meet stringent green building certifications are creating significant pull for high-performance systems.

- These solutions address the chronic construction labor shortage by enabling on-site assembly efficiency, which can reduce build times by 20% to 50% compared to traditional framing. This accelerated timeline translates into long-term operational savings for developers through lower financing costs.

- Concurrently, a life cycle cost analysis often reveals the superior value of these systems, despite higher initial material costs, as they contribute to healthier indoor air quality and lower utility expenses over decades.

We can help! Our analysts can customize this structural insulated panels market research report to meet your requirements.

RIA -

RIA -