Satellite Manufacturing And Launch Market Size 2024-2028

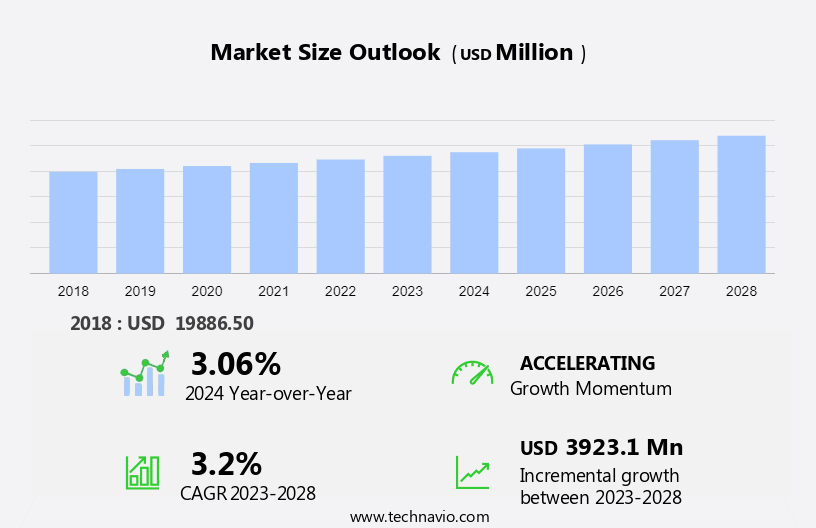

The satellite manufacturing and launch market size is forecast to increase by USD 3.92 billion at a CAGR of 3.2% between 2023 and 2028.

- The reduction in associative launch costs is the key driver of the satellite manufacturing and launch market, as lower costs have made space access more affordable for a wider range of organizations, including commercial entities and smaller nations. This has resulted in a surge in satellite launches for various purposes, from communications to earth observation. An emerging trend in the market is the rise in satellite-aided warfare.

- With increasing reliance on space-based technologies for military operations, satellites are playing a crucial role in intelligence gathering, communication, and navigation. This growing dependence on space assets is driving further investment and innovation in satellite manufacturing and launch services

- Satellite intelligence services, satellite mission technology, GPS, satellite data transmission, and tactical communication systems are integral components of this market. Another trend influencing the market is the rise in satellite-aided warfare, as governments and militaries increasingly rely on satellite technology for surveillance, communication, military communication, and navigation.

What will be the Size of the Satellite Manufacturing And Launch Market During the Forecast Period?

- The market encompasses the production and deployment of satellites for various applications, including communications, earth observation, military and government uses, and internet and telecommunications. Key players in this industry include satellite manufacturers producing satellites for geostationary orbit (GEO) and low earth orbit (LEO), catering to the needs of military surveillance, government agencies, defense forces, and space warfare.

- Commercial entities also contribute significantly, providing satellite-based solutions for tactical communication systems, tactical data links, and satellite-based internet (Satcom). C4ISR integration, UAVs, and space observation further expand the market's scope. The industry is characterized by continuous innovation, with a focus on miniaturization, cost reduction, and enhanced performance to meet evolving customer requirements.

How is this Satellite Manufacturing And Launch Industry segmented and which is the largest segment?

The satellite manufacturing and launch industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Communication satellite

- Military surveillance

- Earth observation satellite

- Navigation satellite

- Others

- Product

- Satellite launch

- Launch services

- End User

- Commercial

- Military

- Geography

- North America

- Canada

- US

- Europe

- Germany

- UK

- APAC

- China

- South America

- Middle East and Africa

- North America

By Application Insights

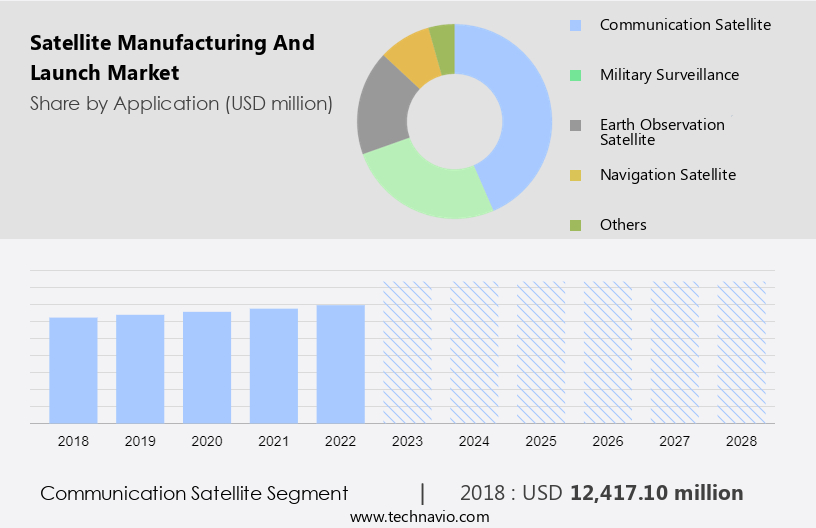

- The communication satellite segment is estimated to witness significant growth during the forecast period.

The communication satellite sector holds a substantial share in the market. Communication satellites are engineered to deliver various communication services such as television broadcasting, telephone networks, internet connectivity, and data transmission. In the realm of satellite manufacturing and launch, communication satellites entail the development, production, and deployment of satellites that facilitate long-distance communication worldwide. These satellites are usually positioned in geostationary orbit (GEO) or medium earth orbit (MEO) to ensure consistent coverage and communication services. The demand for communication satellites is fueled by the escalating requirement for dependable and superior communication services, including voice, data, and multimedia transmissions.

Key players in the communication satellite market offer a wide range of solutions, including satellite broadcasting, telemetry broadcasting, satellite navigation, orbital launch services, and small satellites. The integration of satellite technology into military and government applications, such as C4ISR (Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance), tactical communication systems, tactical data links, SATCOM, and UAVs, further accelerates market growth. Additionally, satellite technology is crucial in weather forecasting, internet services, navigation, satellite data transmission, and space observation. Satellite manufacturing companies provide essential components such as propulsion hardware, solar arrays, and electric, gas-based, or liquid-fuel launch systems to ensure the successful deployment of satellites into orbit.

Get a glance at the Satellite Manufacturing And Launch Industry report of share of various segments Request Free Sample

The communication satellite segment was valued at USD 12.42 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

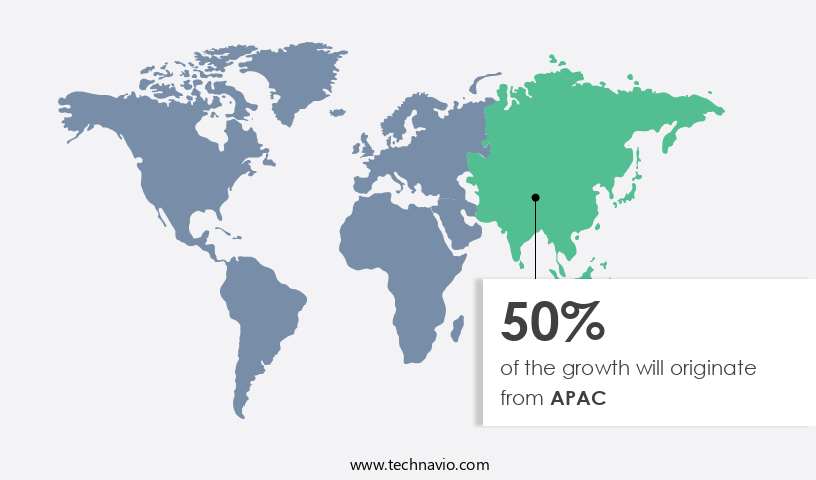

- APAC is estimated to contribute 50% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The North American market is a significant and thriving sector In the global industry. With the presence of major players In the US and Canada, this region holds a substantial market share. Advanced technological capabilities, a strong aerospace industry, and extensive infrastructure contribute to its growth. The market is driven by the increasing demand for satellite communication, remote sensing applications, and national security requirements. North America leads in satellite technology advancements, making it a key player In the global market. The regional market is expected to continue expanding due to these factors.

Market Dynamics

Our satellite manufacturing and launch market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Satellite Manufacturing And Launch Industry?

Reduction in associative launch cost is the key driver of the market.

- The market encompasses the production and deployment of satellites for various applications, including military surveillance, communications, and earth observation. Government agencies and defense forces rely on satellite technology for space warfare, C4ISR integration, and tactical communication systems. Satellite manufacturers produce satellites for internet and telecommunications, GPS, satellite data transmission, and weather forecast. Launch systems, including rockets and launch assembly systems, play a crucial role in satellite deployment. Propulsion hardware, such as solar array (electric or gas-based) and liquid fuel, significantly impacts satellite performance. Satellite payloads, which include satellite communication, satellite broadcasting, telemetry broadcasting, remote sensing, satellite navigation, and orbital launch, are essential components.

- Small satellites have gained popularity due to their cost-effectiveness and versatility. Companies specializing in satellite manufacturing offer innovative solutions to reduce the associated costs of satellite systems. For instance, Rocket Lab, an American company, has developed the Electron rocket, which is expected to decrease the cost and time required to launch satellites into geostationary orbit (GEO) or low Earth orbit (LEO). This investment in research and development (R&D) is crucial for enhancing satellite technology and meeting the evolving needs of the military, government, and commercial sectors.

What are the market trends shaping the Satellite Manufacturing And Launch Industry?

The rise in satellite-aided warfare is the upcoming market trend.

- The market involves the production and deployment of satellites for a wide range of applications, including military surveillance, communications, and Earth observation. Government agencies and defense forces utilize satellites for space warfare, tactical communication systems, and C4ISR (Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance) integration. Satellites provide essential services such as GPS, satellite data transmission, internet and telecommunications, weather forecasts, and navigation. Military satellites are critical for intelligence gathering, global communication, and nuclear threat deterrence. As satellite technology evolves, its use has expanded from defensive to offensive roles. Modern satellite capabilities now allow ground troops to access mission-specific data, enabling more effective strategic planning.

- Soldiers rely on satellites for communication, navigation, targeting, weather prediction, and force protection. Satellite manufacturing companies produce various types of satellites, including communications satellites, satellite intelligence services, and remote sensing satellites. These satellites are launched into geostationary orbit (GEO) or orbital launch systems using rockets and launch assembly systems. Propulsion hardware, such as solar arrays (electric or gas-based), and liquid fuel, are essential components of satellite manufacturing. Satellite communication and broadcasting, telemetry broadcasting, and satellite navigation are integral parts of the market. Small satellites have gained popularity due to their cost-effectiveness and versatility. The infrastructure required for satellite manufacturing and launch is extensive and includes satellite payloads, launch systems, and infrastructure support.

What challenges does the Satellite Manufacturing And Launch Industry face during its growth?

The presence of satellite orbital debris is a key challenge affecting the industry growth.

- The market encompasses various applications, including military surveillance, government agencies, and defense forces, in the realm of space warfare. Satellite manufacturers produce communications satellites for internet and telecommunications, GPS, satellite data transmission, and satellite intelligence services. These satellites are integral to C4ISR integration, tactical communication systems, tactical data links, and SATCOM. The market consists of satellite manufacturing companies specializing in propulsion hardware, solar array, and electric or gas-based systems. Launch systems incorporate rockets and launch assembly systems, while infrastructure includes satellite communication, satellite broadcasting, telemetry broadcasting, remote sensing, satellite navigation, and orbital launch. Small satellites are gaining traction due to their cost-effectiveness and versatility.

- NASA and US DoD collaborate to manage orbital debris, which poses a potential threat to operational satellites. However, the attitude and orbit control system of microsatellites is limited in its ability to avoid large-scale collisions. This necessitates ongoing efforts to mitigate the risks associated with space debris. In summary, the market plays a crucial role in providing essential services for various sectors, including the military and government, while addressing the challenges of space debris and advancing satellite mission technology.

Exclusive Customer Landscape

The satellite manufacturing and launch market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the satellite manufacturing and launch market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, satellite manufacturing and launch market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Airbus SE

- Axelspace Corp.

- Blue Origin Enterprises LP

- GeoOptics Inc.

- Honeywell International Inc.

- Israel Aerospace Industries Ltd.

- Leidos Holdings Inc.

- Lockheed Martin Corp.

- Maxar Technologies Inc.

- Mitsubishi Electric Corp.

- Northrop Grumman Corp.

- OHB SE

- RTX Corp.

- Rocket Lab USA Inc.

- RUAG International Holding Ltd.

- Safran SA

- Sierra Nevada Corp.

- Space Exploration Technologies Corp.

- Thales Group

- The Boeing Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses the production and deployment of artificial satellites for various applications, including communication, earth observation, and space observation. This industry is characterized by continuous advancements in technology, driving the demand for more capable and cost-effective satellites. Satellite manufacturing involves the design, development, and assembly of satellite components, such as propulsion hardware, solar arrays, and communication systems. These components are essential for ensuring the functionality and longevity of satellites in orbit. Electric and gas-based propulsion systems, as well as solar arrays, are commonly used to maintain satellite position and generate power. The launch market is responsible for the transportation of satellites into orbit using various launch systems, including rockets and launch assembly systems.

Moreover, infrastructure development, including the construction of launch pads and support facilities, is also a crucial aspect of the launch market. Communication satellites play a significant role In the market, enabling global connectivity and enabling various industries, including telecommunications and broadcasting, to expand their reach. Telemetry broadcasting, remote sensing, and satellite navigation are other applications that rely on satellites for data transmission and collection. The market is influenced by several factors, including technological advancements, regulatory requirements, and market demand. The increasing adoption of small satellites, which offer cost-effective solutions for various applications, is a notable trend In the industry.

Additionally, the integration of satellite technology into various industries, such as transportation and agriculture, is driving growth In the market. The market is a dynamic and complex industry, requiring significant investment in research and development to stay competitive. Companies in the industry must continuously innovate to meet the evolving needs of their customers and adapt to changing market conditions.

|

Satellite Manufacturing And Launch Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

185 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.2% |

|

Market Growth 2024-2028 |

USD 3.92 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.06 |

|

Key countries |

US, China, Canada, UK, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Satellite Manufacturing And Launch Market Research and Growth Report?

- CAGR of the Satellite Manufacturing And Launch industry during the forecast period

- Detailed information on factors that will drive the Satellite Manufacturing And Launch market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution to the industry in focus on the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the satellite manufacturing and launch market growth of industry companies

We can help! Our analysts can customize this satellite manufacturing and launch market research report to meet your requirements.

RIA -

RIA -