Silicon Carbide (sic) Market Size 2026-2030

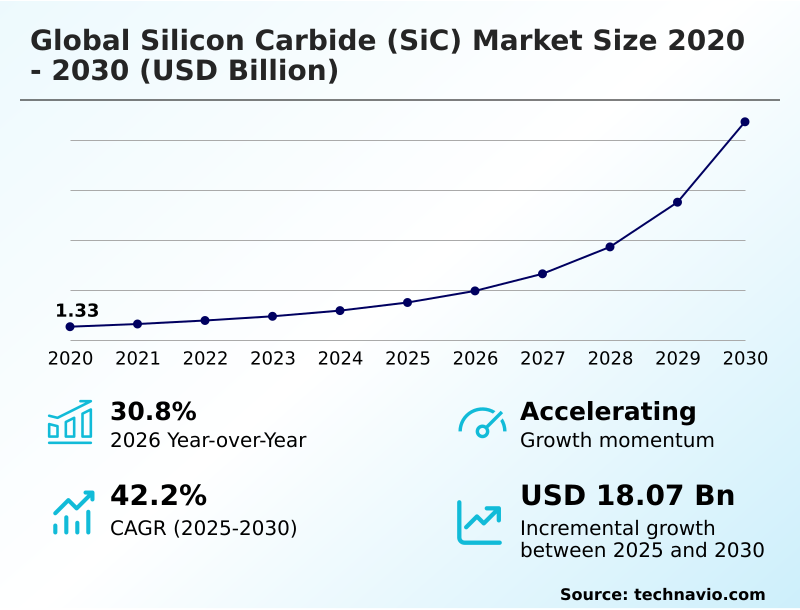

The silicon carbide (sic) market size is valued to increase by USD 18.07 billion, at a CAGR of 42.2% from 2025 to 2030. Transition toward eight-inch wafer manufacturing for economies of scale will drive the silicon carbide (sic) market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 53.4% growth during the forecast period.

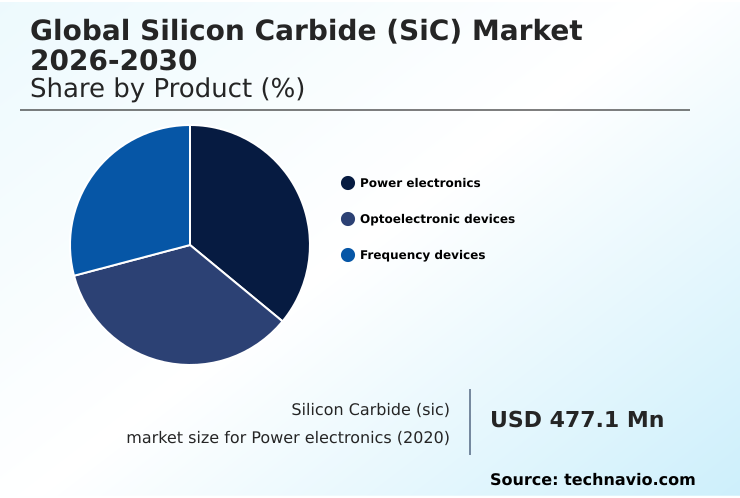

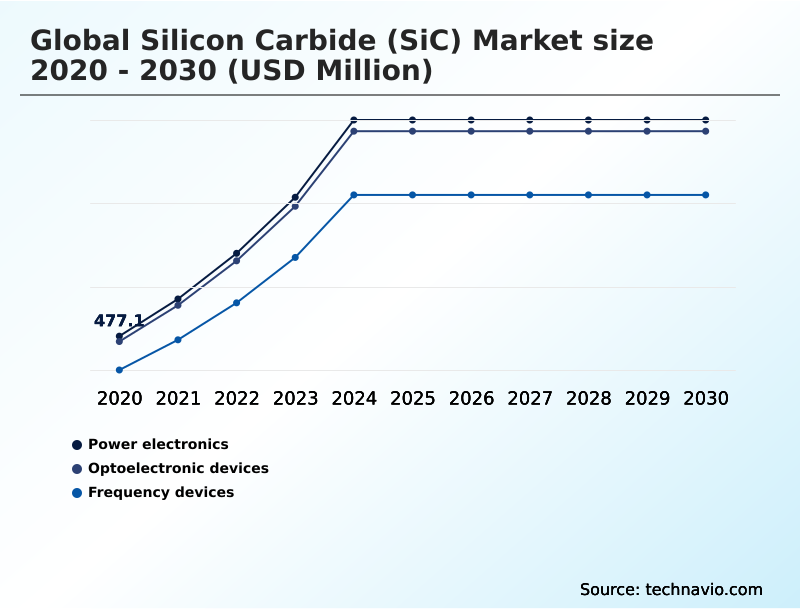

- By Product - Power electronics segment was valued at USD 1.06 billion in 2024

- By Application - Automotive segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 20.50 billion

- Market Future Opportunities: USD 18.07 billion

- CAGR from 2025 to 2030 : 42.2%

Market Summary

- The Silicon Carbide (SiC) market is undergoing a pivotal transformation, fundamentally reshaping power management across multiple industries. This shift is characterized by the replacement of traditional silicon with advanced wide-bandgap semiconductor materials to meet the escalating demands for higher energy efficiency, power density, and thermal performance.

- Key applications in electric vehicles, such as traction inverters and onboard chargers, leverage SiC's capabilities to extend driving range and accelerate charging times. Similarly, the renewable energy sector utilizes SiC-based photovoltaic inverters for more effective energy harvesting.

- A critical operational consideration for businesses is supply chain resilience; for example, an automotive original equipment manufacturer must secure a stable substrate supply of high-quality SiC wafers to avoid production delays. This involves navigating challenges in crystal growth and wafer fabrication, where the transition to 200mm wafer production is crucial for achieving economies of scale.

- The inherent material properties of SiC enable the development of more compact and efficient power modules, driving innovation in industrial automation and electrical grid modernization.

What will be the Size of the Silicon Carbide (sic) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Silicon Carbide (sic) Market Segmented?

The silicon carbide (sic) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Power electronics

- Optoelectronic devices

- Frequency devices

- Application

- Automotive

- Energy and power

- Aerospace and defense

- Data and communication devices

- Others

- Device

- SiC discrete device

- SiC module

- Measurement

- Up to 150mm

- Greater than 150mm

- Geography

- APAC

- China

- Japan

- South Korea

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Product Insights

The power electronics segment is estimated to witness significant growth during the forecast period.

The power electronics segment is pivotal, driven by the need for enhanced energy conversion efficiency. This involves the use of wide-bandgap semiconductor devices like MOSFETs and Schottky barrier diodes, which offer superior performance over silicon, particularly in high-voltage architecture.

These components are critical for automotive traction inverters and photovoltaic inverters, where they enable greater driving ranges and improved energy harvesting. The focus is on reducing switching losses and improving power density.

For instance, optimized integrated gate drivers can lead to a 12% improvement in energy throughput.

The ongoing shift toward advanced ceramic materials and better heat dissipation techniques is also central to this segment, ensuring reliability in demanding industrial automation and high-performance computing environments.

The Power electronics segment was valued at USD 1.06 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 53.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Silicon Carbide (sic) Market Demand is Rising in APAC Get Free Sample

The geographic landscape is dominated by APAC, which is projected to account for over 53% of the incremental market expansion, significantly outpacing North America's 16% share.

This growth is fueled by massive investments in semiconductor manufacturing and the region's central role in the electric vehicle supply chain. China, in particular, drives demand for traction inverters and power modules.

In contrast, North America and Europe focus on high-value applications and technological innovation, including electrical grid modernization and advanced R&D in wafer fabrication.

The emphasis in these regions is on enhancing substrate supply security and improving yield improvement in 200mm wafer production, which is critical for maintaining a competitive edge in the global power semiconductor race.

This regional dynamic highlights a global market structured around high-volume production in one area and specialized, high-performance development in others.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic evaluation of silicon carbide vs gallium nitride applications is a central theme, as enterprises determine the optimal technology for their specific needs. For high-voltage, high-power systems like electric vehicle powertrains, the power density advantages of SiC are clear, making it the preferred choice.

- The cost-benefit of SiC inverters becomes particularly compelling when considering long-term operational savings from enhanced efficiency. However, a primary hurdle remains: the challenges in large-diameter SiC crystal growth, which directly impact manufacturing costs and scalability. Consequently, a great deal of focus is on improving yield in 200mm SiC wafers to make the technology more accessible.

- Effective thermal management in SiC power modules is another critical area, as it dictates device longevity and performance, with advancements in this area directly correlating to a vehicle's reliability. The impact of SiC on EV charging speed is profound, with 800-volt systems enabling ultra-fast charging capabilities that reduce consumer range anxiety.

- As the industry matures, SiC for renewable energy grid integration is set to expand, driven by the need for more efficient and resilient power grids. For mission-critical sectors, the role of SiC in aerospace power systems highlights its robustness. Meanwhile, the growing energy demands of hyperscale facilities make SiC in high-power AI data centers a non-negotiable path toward sustainability.

- All these applications hinge on stringent reliability testing for automotive SiC modules and robust SiC supply chain risk mitigation strategies to ensure market stability.

What are the key market drivers leading to the rise in the adoption of Silicon Carbide (sic) Industry?

- The transition toward eight-inch wafer manufacturing to achieve economies of scale is a key driver for the market, aiming to reduce costs and increase throughput.

- A primary driver is the industry's aggressive push toward 200mm wafer production, which is essential for achieving economies of scale and reducing the per-die cost of power modules.

- This transition enables manufacturers to meet the escalating demand from the automotive sector for affordable traction inverters.

- The shift to an 800-volt electrical architecture in new electric vehicles mandates the use of SiC MOSFETs to achieve faster charging and extended range, with some platforms realizing a 10% gain in overall powertrain efficiency.

- This automotive-led demand is bolstered by requirements from smart grid infrastructure, where SiC's ability to handle high voltages improves grid stability and performance.

- The continuous refinement of wafer fabrication and epitaxial growth processes is critical to lowering costs and accelerating the displacement of silicon.

What are the market trends shaping the Silicon Carbide (sic) Industry?

- A significant market trend is the surge in advanced power architectures for AI data centers. This is driving demand for high-efficiency power management solutions capable of handling increased power densities.

- Market trends are increasingly shaped by the electrification of heavy industry and the rise of high-density power architectures for AI data centers. The transition to high-voltage architecture in industrial automation and mining machinery is driving demand for robust power semiconductor devices capable of operating in harsh environments.

- This trend is complemented by the surge in high-performance computing, where SiC-based power supply units offer superior energy conversion efficiency, reducing operational costs. For example, data centers adopting these technologies have reported up to a 20% reduction in cooling energy consumption. The focus on developing advanced ceramic materials and improving heat dissipation allows for more compact and reliable systems.

- These developments are paving the way for wider adoption in solid-state transformers and other grid-scale energy storage applications.

What challenges does the Silicon Carbide (sic) Industry face during its growth?

- Manufacturing complexity and yield limitations associated with large-diameter wafers present a key challenge to industry growth, impacting production costs and scalability.

- A significant challenge remains the manufacturing complexity and low yield rates associated with large-diameter wafer fabrication. The inherent difficulty in the crystal growth of SiC leads to a higher incidence of micropipe defects and basal plane dislocations, which limits the usable die per wafer and keeps costs high.

- This issue is particularly acute in the transition to 200mm substrates, where process stability issues can lead to yield rates for automotive-grade devices remaining below 60%. Furthermore, the supply chain is vulnerable due to the geographic concentration of high-purity raw material suppliers and the long lead times for specialized equipment like ion implantation tools.

- These factors create a structural bottleneck that can slow the adoption of SiC in more cost-sensitive industrial motor drives and consumer applications.

Exclusive Technavio Analysis on Customer Landscape

The silicon carbide (sic) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the silicon carbide (sic) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Silicon Carbide (sic) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, silicon carbide (sic) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AGSCO Corp. - Key offerings include high-performance silicon carbide abrasives and advanced materials engineered for industrial surface treatment and finishing applications, enhancing durability and precision.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AGSCO Corp.

- Asuzac Fine Ceramics Co Ltd

- CeramTec GmbH

- Compagnie de Saint Gobain SA

- CoorsTek Inc.

- Dow Chemical Co.

- ESD SIC bv

- ESK SiC GmbH

- Hongwu International Group Ltd.

- Imerys S.A.

- Infineon Technologies AG

- Kyocera Corp.

- Mersen Corporate Services SAS

- Miller and Co.

- Morgan Advanced Materials

- Murugappa Group

- ON Semiconductor Corp.

- SNAM Abrasives Pvt. Ltd.

- Tokai Carbon Co. Ltd.

- Xiamen Powerway Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Silicon carbide (sic) market

- In March 2025, Infineon Technologies AG initiated the volume ramp-up of its 200mm silicon carbide wafer production at its new facility in Kulim, Malaysia, to meet the surging demand from the automotive sector.

- In January 2025, Wolfspeed Inc. launched a new top-side cooled power module package specifically designed to meet the extreme thermal demands of high-density AI server architectures, enhancing power delivery efficiency.

- In November 2024, a major joint venture in China announced it had entered the risk production stage for 8-inch automotive-grade SiC wafers, aiming to resolve long-term reliability issues before initiating full-scale manufacturing.

- In September 2024, onsemi launched a new series of intelligent power modules incorporating proprietary SiC MOSFETs, targeting high-efficiency three-phase industrial motor drives and renewable energy systems.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Silicon Carbide (sic) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 322 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 42.2% |

| Market growth 2026-2030 | USD 18069.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 30.8% |

| Key countries | China, Japan, South Korea, India, Australia, Indonesia, US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Silicon Carbide (SiC) market's trajectory is defined by the industry-wide strategic shift toward 200mm wafer production, a move critical for reducing the per-die cost and scaling output for mass-market applications. This transition is a key boardroom topic, influencing capital expenditure decisions and long-term supply agreements.

- Mastering the complexities of crystal growth and epitaxial growth on larger substrates is now the primary benchmark for technological leadership. Companies are focused on yield improvement to make high-performance discrete components and power modules more economically viable.

- The adoption of SiC is driven by its superior thermal management and energy conversion efficiency, which are indispensable for next-generation electric vehicles and electrical grid modernization. For instance, the use of SiC in high-voltage architecture allows for system designs that are over 20% more compact than their silicon-based predecessors.

- The success of this wide-bandgap semiconductor technology hinges on securing a resilient substrate supply and advancing semiconductor manufacturing processes to meet the demands of high-frequency devices and power electronics.

What are the Key Data Covered in this Silicon Carbide (sic) Market Research and Growth Report?

-

What is the expected growth of the Silicon Carbide (sic) Market between 2026 and 2030?

-

USD 18.07 billion, at a CAGR of 42.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Power electronics, Optoelectronic devices, and Frequency devices), Application (Automotive, Energy and power, Aerospace and defense, Data and communication devices, and Others), Device (SiC discrete device, and SiC module), Measurement (Up to 150mm, and Greater than 150mm) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Transition toward eight-inch wafer manufacturing for economies of scale, Manufacturing complexity and yield limitations in large-diameter wafers

-

-

Who are the major players in the Silicon Carbide (sic) Market?

-

AGSCO Corp., Asuzac Fine Ceramics Co Ltd, CeramTec GmbH, Compagnie de Saint Gobain SA, CoorsTek Inc., Dow Chemical Co., ESD SIC bv, ESK SiC GmbH, Hongwu International Group Ltd., Imerys S.A., Infineon Technologies AG, Kyocera Corp., Mersen Corporate Services SAS, Miller and Co., Morgan Advanced Materials, Murugappa Group, ON Semiconductor Corp., SNAM Abrasives Pvt. Ltd., Tokai Carbon Co. Ltd. and Xiamen Powerway Co. Ltd.

-

Market Research Insights

- The market's dynamics are shaped by a strategic push toward high-efficiency power conversion, where the adoption of trench MOSFETs has resulted in a 30% reduction in on-resistance compared to previous generations. This enhancement is critical for applications in industrial motor drives and high-performance computing, where minimizing energy loss is paramount.

- The successful implementation of physical vapor transport techniques has improved wafer quality, leading to a 15% increase in device reliability under high-stress conditions. Innovations in packaging, such as silver sintering, improve heat dissipation, allowing power supply units to operate at higher capacities without thermal degradation.

- As a result, systems utilizing advanced SiC components demonstrate a significant improvement in overall power density, enabling more compact and lightweight designs for applications ranging from onboard chargers to smart grid infrastructure, with some systems achieving a 40% smaller footprint.

We can help! Our analysts can customize this silicon carbide (sic) market research report to meet your requirements.

RIA -

RIA -