Power Semiconductor Market Size 2026-2030

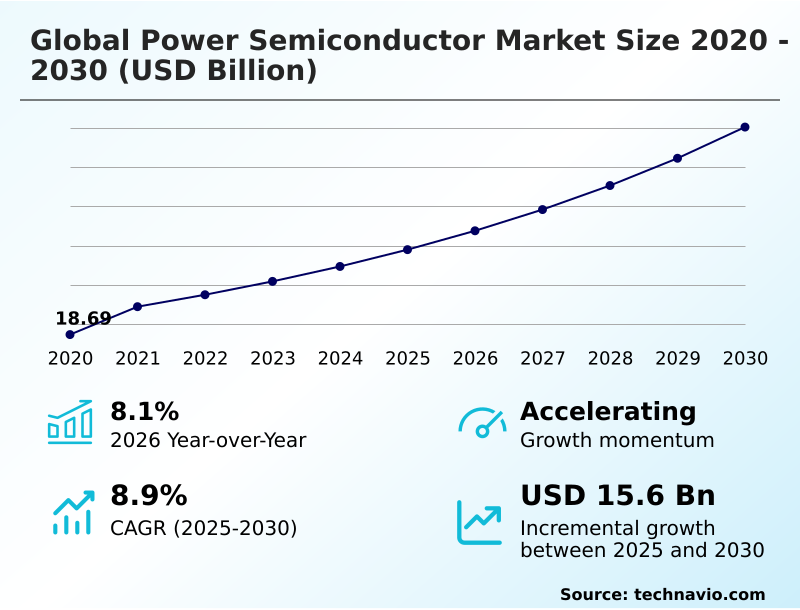

The Power Semiconductor Market size was valued at USD 29.50 billion in 2025, growing at a CAGR of 8.9% during the forecast period 2026-2030.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 59.1% growth during the forecast period.

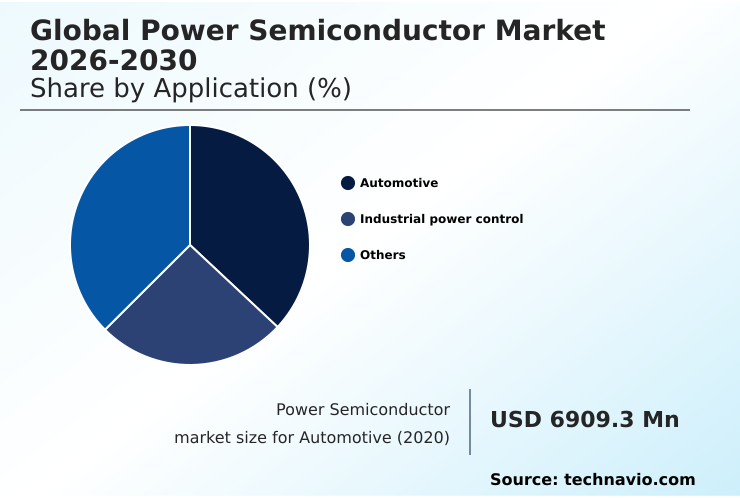

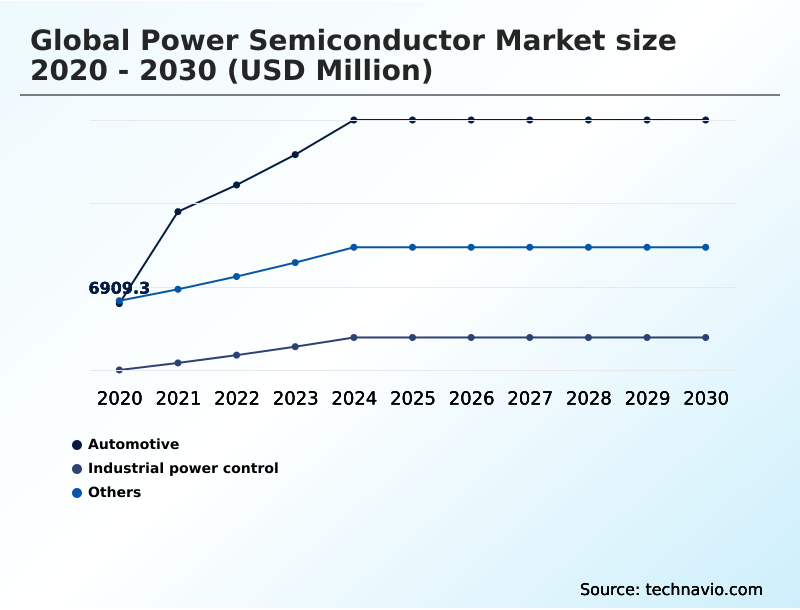

- By Application - Automotive segment was valued at USD 12.82 billion in 2024

- By Material - Silicon segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 26.41 billion

- Market Future Opportunities 2025-2030: USD 15.60 billion

- CAGR from 2025 to 2030 : 8.9%

Market Summary

- The power semiconductor market is defined by a rapid innovation cycle, where the demand for higher power density and efficiency leads to continuous material and architectural advancements. For instance, the transition to wide bandgap semiconductors like silicon carbide (SiC) and gallium nitride (GaN) has enabled a 30% reduction in energy loss in certain high-voltage applications compared to traditional silicon.

- A key driver is the global electrification of the automotive sector, which requires robust components like traction inverters and onboard chargers capable of handling high power loads with minimal heat generation. A real-world operational scenario involves supply chain managers for automotive OEMs collaborating with semiconductor fabs to secure long-term contracts for SiC wafers, mitigating production risks.

- Conversely, a significant challenge is the high capital expenditure required for new fabrication facilities, creating a barrier to entry and concentrating production among a few key players. This dynamic underscores the critical balance between technological advancement and manufacturing scalability in the industry.

What will be the Size of the Power Semiconductor Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Power Semiconductor Market Segmented?

The power semiconductor industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Automotive

- Industrial power control

- Others

- Material

- Silicon

- Silicon carbide

- Gallium nitride

- Component

- Discrete

- Module

- Power ICs

- Geography

- APAC

- China

- Japan

- South Korea

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

How is the Power Semiconductor Market Segmented by Application?

The automotive segment is estimated to witness significant growth during the forecast period.

The automotive segment's adoption of advanced power semiconductors has resulted in a 15% improvement in electric vehicle (EV) range due to enhanced power conversion efficiency.

Devices like the silicon carbide MOSFET are integral to this shift, with new traction inverter designs reducing energy losses by over 20% compared to previous silicon-based systems. This enables faster charging and more compact drivetrain components.

The demand for automotive-grade qualification in these components is driven by the need for high reliability in electrified systems and onboard chargers.

As the industry moves towards 800-volt architectures, the role of wide bandgap semiconductors becomes even more critical for managing high-voltage applications and achieving superior fast-switching performance in power supply design.

The Automotive segment was valued at USD 12.82 billion in 2024 and showed a gradual increase during the forecast period.

How demand for the Power Semiconductor market is rising in the leading region?

APAC is estimated to contribute 59.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Power Semiconductor Market demand is rising in APAC Request Free Sample

The geographic landscape of the power semiconductor market is dominated by APAC, which accounts for approximately 59% of the global market, a stark contrast to North America's 13% share.

This dominance is driven by countries like China, Japan, and South Korea, which collectively represent over half of the region's demand, fueled by massive electronics manufacturing and aggressive electric vehicle (EV) production targets.

In contrast, Europe's market, while smaller, is characterized by high-value applications in industrial automation and premium automotive sectors, focusing on automotive-grade qualification.

Regional differences in supply chain localization are notable; APAC benefits from an integrated ecosystem of wafer fabrication and advanced packaging, reducing lead times by up to 20%, whereas North America and Europe are increasingly investing in domestic semiconductor manufacturing to reduce dependency and enhance supply chain resilience for critical energy infrastructure and data center optimization.

What are the key Drivers, Trends, and Challenges in the Power Semiconductor Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the complexities of the power semiconductor market requires a deep understanding of specific use cases and material performance. For instance, evaluating silicon carbide vs gallium nitride for EV applications reveals that SiC is often preferred for high-voltage traction inverters, where its superior thermal conductivity allows for a 10-15% increase in power density over silicon.

- In contrast, GaN excels in high-frequency onboard chargers and DC-DC converters. When considering how to improve power density in data centers, engineers often turn to GaN-based power management ICs, which can operate at higher switching frequencies, reducing the size of passive components by as much as 40%.

- The selection of a power semiconductor for renewable energy inverters depends heavily on the scale of the system; SiC modules are prevalent in utility-scale solar farms, while GaN devices are making inroads in residential microinverters. However, a significant hurdle remains: the challenges in wide bandgap material supply, which can lead to production delays and price volatility.

- To address this, companies are exploring integrated power modules for industrial automation, which offer a pre-validated, reliable solution that simplifies design and sourcing, mitigating some of the supply chain risks associated with discrete components.

What are the key market drivers leading to the rise in the adoption of Power Semiconductor Industry?

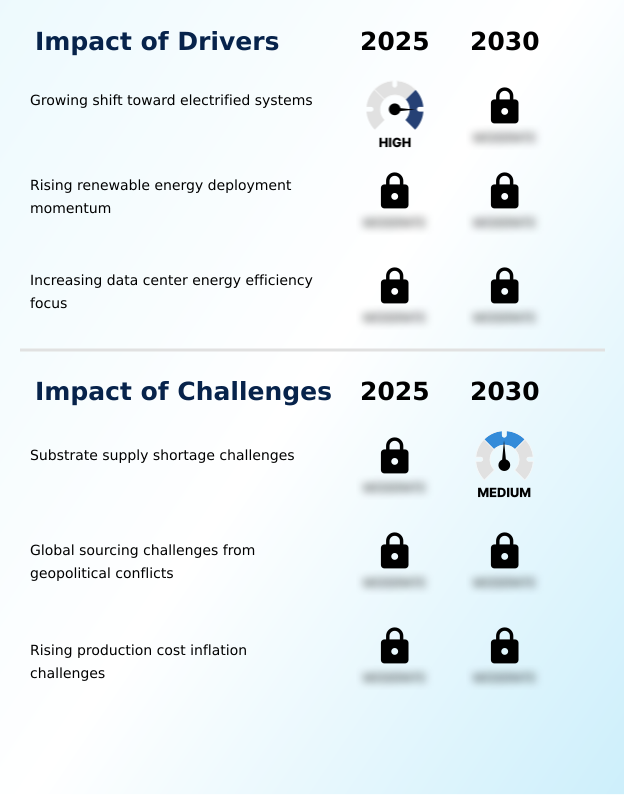

- A primary driver for the market is the growing shift toward electrified systems, which is accelerating transitions across the transportation and energy sectors.

- The escalating demand for electrified systems is a primary driver, with electric vehicle sales increasing over 20% annually, creating a substantial need for advanced power semiconductors.

- This momentum is matched by the rapid renewable energy deployment, where the efficiency of power inverters directly impacts energy yield. High-voltage applications in solar and wind farms benefit significantly from devices that minimize energy loss, improving overall grid synchronization.

- Furthermore, the exponential growth of data center optimization initiatives, driven by AI workloads, necessitates highly efficient power supply design.

- Adopting advanced power management ICs in servers can reduce energy consumption by up to 15%, a critical factor in managing operational costs and achieving sustainability goals within large-scale energy infrastructure.

What are the market trends shaping the Power Semiconductor Industry?

- The market is undergoing a significant transformation driven by the shift toward wide bandgap supremacy. Silicon carbide and gallium nitride materials are establishing dominance by offering exclusive performance advantages in high-efficiency applications.

- A dominant trend in the power semiconductor market is the advancement of wide bandgap semiconductor materials, which offer a 30% increase in power conversion efficiency over traditional silicon. This shift is driven by the adoption of AI-centric power delivery architectures that demand high-frequency operation and superior thermal management solutions.

- For instance, the use of a silicon carbide MOSFET enables systems to handle higher breakdown voltage and junction temperature, reducing system size and cooling requirements. This is particularly critical in applications like electric vehicles, where gallium nitride HEMT devices in onboard chargers contribute to faster charging times.

- The move toward integrated electrification modules, combining functions like circuit protection and fault detection, further exemplifies the trend toward higher power density and system-level optimization.

What challenges does the Power Semiconductor Industry face during its growth?

- A key challenge impacting industry growth is the ongoing substrate supply shortage, stemming from constrained production of high-quality silicon carbide and gallium nitride materials.

- A primary challenge confronting the power semiconductor market is the persistent shortage of high-quality substrates, which has extended lead times for silicon carbide wafers by up to 50% in some cases. This substrate manufacturing bottleneck directly impacts the ability of producers to scale wafer fabrication and meet the surging demand from the automotive and industrial sectors.

- Geopolitical conflicts exacerbate these issues, disrupting global supply chains and leading to semiconductor manufacturing cost inflation, with some input materials seeing price increases of over 25%.

- These global sourcing challenges force companies to invest in supply chain localization and qualify alternative suppliers, adding complexity and cost to their operations and potentially delaying the rollout of next-generation technologies that depend on these advanced materials.

Exclusive Technavio Analysis on Customer Landscape

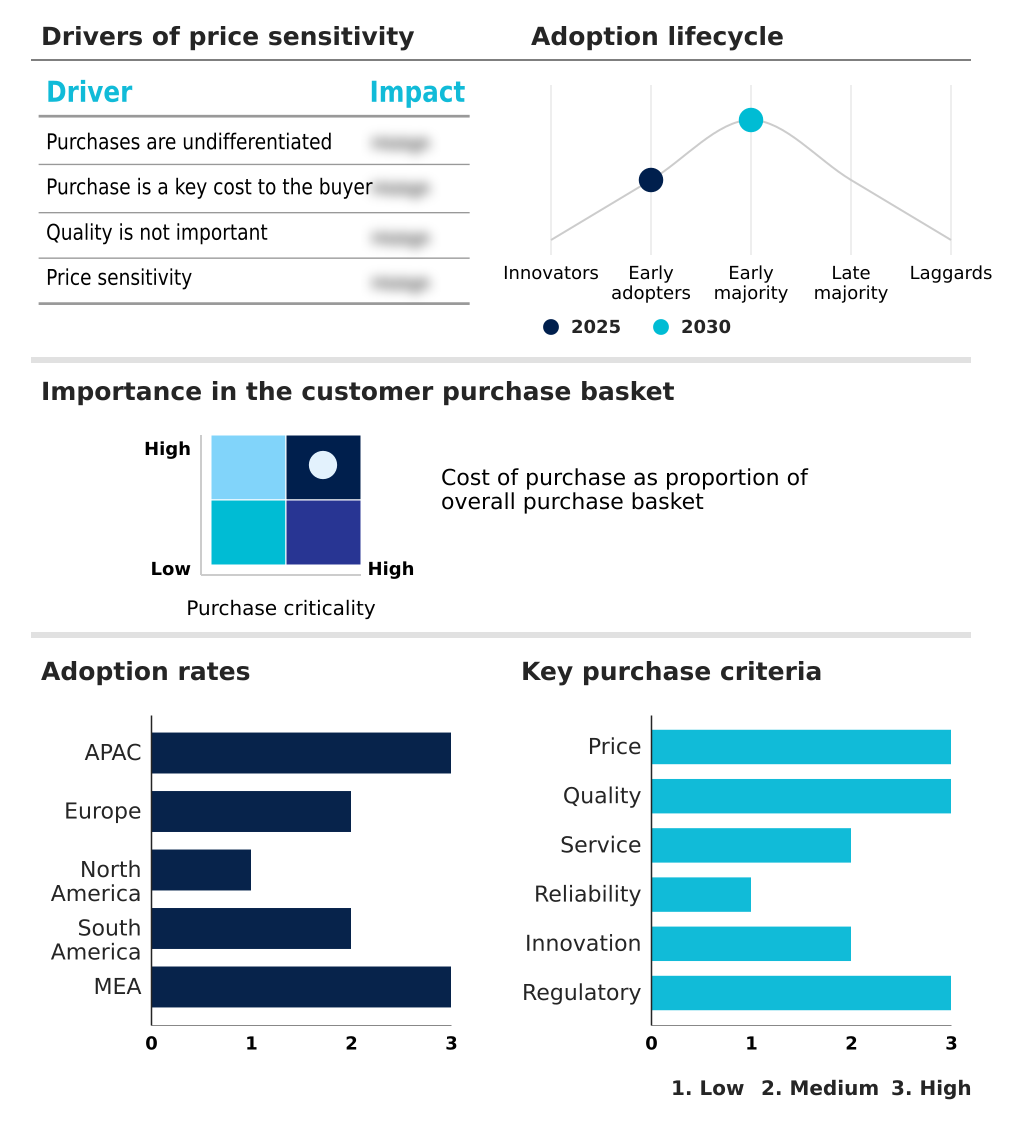

The power semiconductor market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the power semiconductor market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Power Semiconductor Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, power semiconductor market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alpha and Omega Semiconductor - Key offerings include advanced power semiconductors, encompassing silicon carbide (SiC) and gallium nitride (GaN) devices, designed for high-efficiency power conversion and management across multiple industries.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alpha and Omega Semiconductor

- Diodes Inc.

- Fuji Electric Co. Ltd.

- Infineon Technologies AG

- Littelfuse Inc.

- MagnaChip Semiconductor Corp.

- Microchip Technology Inc.

- Mitsubishi Electric Corp.

- Monolithic Power Systems Inc.

- Navitas Semiconductor Inc.

- Nexperia BV

- NXP Semiconductors NV

- ON Semiconductor Corp.

- Renesas Electronics Corp.

- ROHM Co. Ltd.

- Shindengen Electric Co. Ltd.

- STMicroelectronics NV

- Texas Instruments Inc.

- Vishay Intertechnology Inc.

- Wolfspeed Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the semiconductor materials and equipment industry, the push for domestic semiconductor fabrication capabilities, supported by government initiatives, is altering global supply chains for power semiconductors, encouraging supply chain localization and investments in new wafer fabrication plants to mitigate geopolitical risks and ensure a stable supply for energy infrastructure.

- A significant trend is the accelerated development and investment in 300-millimeter wafer processing lines, which increases manufacturing yields by over 25% per wafer. This directly impacts the power semiconductor market by lowering the unit cost of high-volume devices and supporting the scaling of advanced packaging for consumer electronics.

- The adoption of advanced packaging technologies, such as system-in-package (SiP) designs, is enabling higher levels of integration. This allows power semiconductor manufacturers to create more compact and efficient modules that combine power, control, and protection functions, a key requirement for industrial electrification.

- Stricter environmental regulations on industrial emissions and energy consumption are driving demand for high-efficiency power semiconductors. The need for variable frequency drives and smart grid technology in industrial settings creates a pull for devices that minimize energy loss, with new standards mandating efficiency improvements of at least 10% in motor control systems.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Power Semiconductor Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 303 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.9% |

| Market growth 2026-2030 | USD 15596.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.1% |

| Key countries | China, Japan, South Korea, India, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The power semiconductor market ecosystem is a highly integrated network where raw material suppliers of silicon, silicon carbide, and gallium nitride provide the foundation for device manufacturing. Specialized equipment providers supply the tools for wafer fabrication, a segment that commands over 40% of the total capital expenditure in the industry.

- Manufacturers, including integrated device makers and foundries, design and produce components ranging from discrete devices to complex power modules. These products are then distributed through direct sales channels and global distributors to end-users in the automotive, industrial, and consumer electronics sectors.

- Regulatory bodies and industry consortia establish the standards for performance and reliability, such as automotive-grade qualification, which ensures devices can withstand harsh operating conditions. The entire value chain is supported by R&D entities and software firms that provide the intellectual property and design tools necessary for continuous innovation, with R&D investments often exceeding 15% of revenue for leading firms.

What are the Key Data Covered in this Power Semiconductor Market Research and Growth Report?

-

What is the expected growth of the Power Semiconductor Market between 2026 and 2030?

-

The Power Semiconductor Market is expected to grow by USD 15.60 billion during 2026-2030, registering a CAGR of 8.9%. Year-over-year growth in 2026 is estimated at 8.1%%. This acceleration is shaped by growing shift toward electrified systems, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Automotive, Industrial power control, and Others), Material (Silicon, Silicon carbide, and Gallium nitride), Component (Discrete, Module, and Power ICs) and Geography (APAC, Europe, North America, South America, Middle East and Africa). Among these, the Automotive segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers APAC, Europe, North America, South America and Middle East and Africa. APAC is estimated to contribute 59.1% to market growth during the forecast period. Country-level analysis includes China, Japan, South Korea, India, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is growing shift toward electrified systems, which is accelerating investment and industry demand. The main challenge is substrate supply shortage challenges, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Power Semiconductor Market?

-

Key vendors include Alpha and Omega Semiconductor, Diodes Inc., Fuji Electric Co. Ltd., Infineon Technologies AG, Littelfuse Inc., MagnaChip Semiconductor Corp., Microchip Technology Inc., Mitsubishi Electric Corp., Monolithic Power Systems Inc., Navitas Semiconductor Inc., Nexperia BV, NXP Semiconductors NV, ON Semiconductor Corp., Renesas Electronics Corp., ROHM Co. Ltd., Shindengen Electric Co. Ltd., STMicroelectronics NV, Texas Instruments Inc., Vishay Intertechnology Inc. and Wolfspeed Inc.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape of the power semiconductor market is intensely dynamic, with the top five vendors accounting for over 60% of market share. Companies are aggressively investing in wide bandgap materials to capture growth in high-demand sectors. For instance, Infineon Technologies AG is expanding its manufacturing for power supplies to support AI data centers and renewable energy, while Wolfspeed Inc.

- focuses on 300-millimeter silicon carbide technology to enhance thermal and electrical performance. These strategic moves are a direct response to the escalating demand for high-efficiency power conversion in electric vehicles and data center infrastructure.

- This innovation push is not without obstacles; ongoing substrate supply shortages present a significant challenge, forcing companies to implement dual-sourcing strategies and invest in research for alternative materials to maintain production continuity.

We can help! Our analysts can customize this power semiconductor market research report to meet your requirements.

RIA -

RIA -