Silicon Metal Market Size 2026-2030

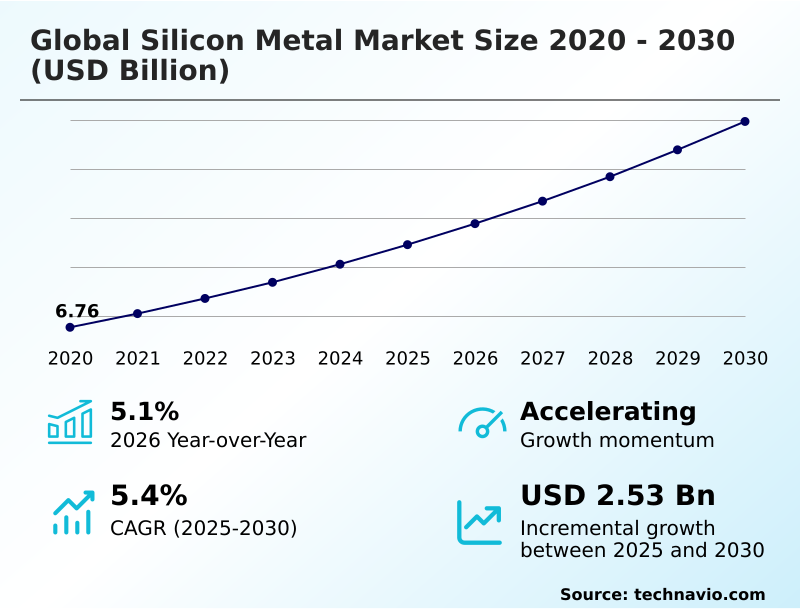

The silicon metal market size is valued to increase by USD 2.53 billion, at a CAGR of 5.4% from 2025 to 2030. Surge in aluminum alloy demand for automotive lightweighting will drive the silicon metal market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 41.9% growth during the forecast period.

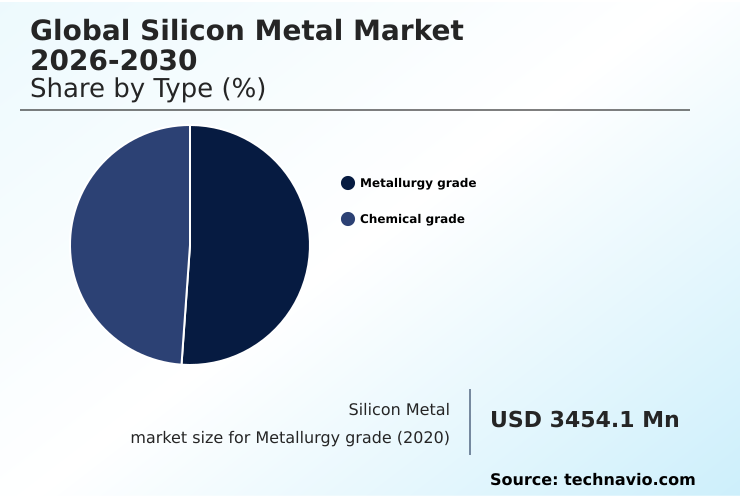

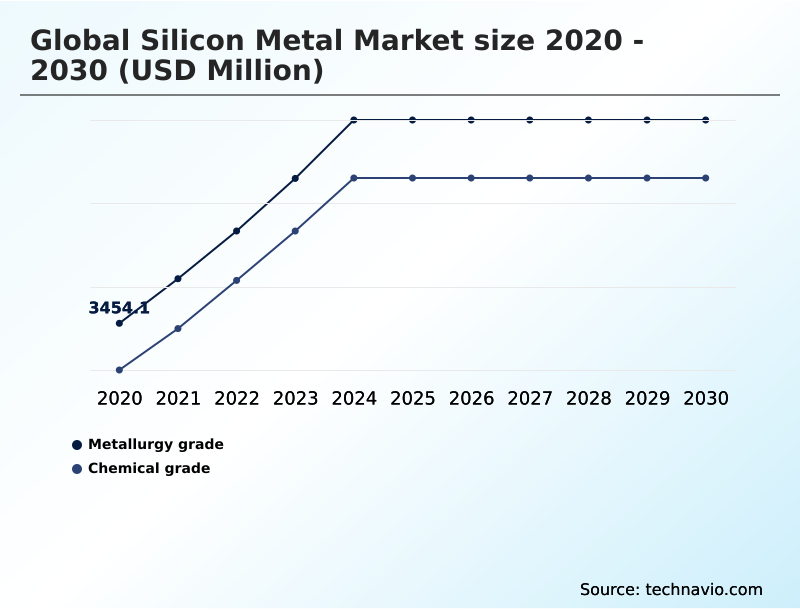

- By Type - Metallurgy grade segment was valued at USD 4.12 billion in 2024

- By Application - Aluminum alloys segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 4.22 billion

- Market Future Opportunities: USD 2.53 billion

- CAGR from 2025 to 2030 : 5.4%

Market Summary

- The silicon metal market is foundational to modern industrial economies, serving as an indispensable input for sectors driving the global energy transition and digital transformation. Demand is primarily fueled by its use in aluminum alloys for automotive lightweighting, the production of silicones for construction and industrial applications, and as the essential polysilicon feedstock for solar panels and semiconductors.

- A key trend shaping the industry is the strategic shift toward low-carbon silicon, where producers leverage renewable energy to meet stringent environmental standards. For instance, an automotive OEM aiming for a carbon-neutral supply chain would exclusively source certified green silicon for its aluminum chassis components, creating a premium market segment.

- However, the industry grapples with significant challenges, including the high energy intensity of the smelting process and price volatility driven by fluctuating electricity costs and geopolitical trade tensions. Navigating this landscape requires balancing large-scale production with the growing demand for specialized, sustainable materials.

What will be the Size of the Silicon Metal Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Silicon Metal Market Segmented?

The silicon metal industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Metallurgy grade

- Chemical grade

- Application

- Aluminum alloys

- Semiconductors

- Solar panels

- Stainless steel

- Others

- Distribution channel

- Direct sales

- Indirect sales

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Type Insights

The metallurgy grade segment is estimated to witness significant growth during the forecast period.

The global silicon metal market is segmented by type, application, and geography.

The metallurgy grade segment is a critical component of the silicon value chain, primarily serving as an essential alloying agent in the production of aluminum-silicon alloys and silumin alloys.

This material, produced via an electro-intensive smelting process involving electrometallurgy, is foundational to creating automotive lightweighting material for advanced metallurgical applications.

Its role as a deoxidizing agent enhances the castability and strength of metals, with producers of sustainable aluminum production noting strength improvements of over 15% in certain alloys.

This makes metallurgical grade silicon indispensable for critical infrastructure material and within the broader energy-intensive industry, solidifying its importance across multiple industrial verticals.

The Metallurgy grade segment was valued at USD 4.12 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 41.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Silicon Metal Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the silicon metal market is characterized by a strategic bifurcation. APAC, contributing over 41% of the incremental growth, remains the dominant production hub, driven by massive industrial capacity and demand from its solar and electronics sectors.

However, North America is aggressively pursuing critical mineral independence through supply chain regionalization and the development of domestic processing capabilities for downstream value-added applications like silane gas and silicon metal powder.

This strategy, reinforced by friend-shoring trends, aims to secure inputs for its burgeoning green energy infrastructure. Meanwhile, Europe's market is defined by its high-cost energy environment and stringent regulations like the carbon border adjustment mechanism.

European producers are focusing on premium, low-carbon silicon and green silicon, leveraging high-purity quartz to differentiate their fumed silica and industrial silicon products, with some achieving over 75% lower emissions compared to conventional methods.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Analyzing the global silicon metal market 2026-2030 requires understanding key pressures, including the direct impact of energy costs on silicon production and shifting silicon metal price volatility factors. A significant portion of market dynamics of metallurgical grade silicon is now dictated by geopolitical risks in silicon supply chains and the proliferation of trade tariffs on silicon metal imports.

- Concurrently, the growth of silicon anode battery technology creates a high-value demand for silicon in electric vehicle batteries, distinct from its traditional use of silicon metal for aluminum alloy casting. The expansion of renewable energy relies on the use of silicon metal in solar panels, which in turn is governed by the supply and demand for polysilicon feedstock.

- This has spurred investment in green silicon production facilities. Downstream, the role of silicones in construction sealants and applications of fumed silica in industry remain stable demand pillars. However, producers must navigate complex environmental regulations for silicon smelting and meet stringent purity requirements for chemical grade silicon, which is a critical silicon metal as a semiconductor precursor.

- Companies focusing on technological advances in silicon metal refining are better positioned, as the impact of drought on hydropower for smelting highlights the vulnerability of producers reliant on specific energy sources.

- Firms that vertically integrate, controlling everything from silicon metal in aerospace applications to feedstock, can mitigate sourcing risks, though this can increase operational overhead by up to 20% compared to specialized producers.

What are the key market drivers leading to the rise in the adoption of Silicon Metal Industry?

- A surge in demand for aluminum alloys, driven by the automotive industry's pursuit of lightweighting solutions, serves as a primary driver for the market.

- Demand for silicon metal is accelerating, driven by its critical role as a renewable energy raw material and its application in advanced mobility.

- The massive global expansion of solar energy relies on photovoltaic grade silicon for n-type topcon cells, while the electric vehicle sector's growth fuels demand for silicon-anode batteries and silicon-carbon composite materials, which can boost battery capacity by over 20%.

- This has intensified supply chain de-risking efforts and prompted governments to enact production linked incentive schemes to bolster domestic manufacturing. Despite geopolitical trade barriers, the need for electronic-grade silicon and semiconductor grade silicon for high-performance computing remains robust.

- Furthermore, innovations in automotive manufacturing, such as giga casting components, depend on high-quality silicon alloys.

- This convergence of drivers necessitates strategic mineral stockpiling and creates new energy security initiatives focused on securing a stable silicon supply, with some companies reducing material waste by 15% through optimized casting techniques.

What are the market trends shaping the Silicon Metal Industry?

- The market is defined by a significant trend toward strategic supply chain regionalization. This shift is reinforced by the increasing implementation of trade defense mechanisms.

- Key trends reshaping the silicon metal market center on supply chain security and sustainability. The industry is moving away from globalized sourcing toward regionalized networks, driven by trade defense mechanisms and circular economy initiatives. This shift encourages investment in local production, from the initial carbothermic reduction in a submerged electric arc furnace to the manufacturing of finished silicone precursors.

- Simultaneously, there is a strong push for decarbonization of smelting, with producers adopting low-carbon production pathways and bio-based reductants to meet stringent scope 3 emissions tracking requirements. This focus on sustainability has led to a 10% increase in the adoption of net-zero technology feedstock among leading producers.

- As a result, the market for chemical grade silicon and polysilicon feedstock is increasingly segmented, with certified low-carbon materials commanding premium prices in an otherwise electro-intensive process.

What challenges does the Silicon Metal Industry face during its growth?

- High energy production costs combined with the persistent volatility of electricity prices represent a key challenge affecting the industry's growth trajectory.

- The silicon metal market faces significant headwinds from operational and structural challenges. As an electro-intensive manufacturing process, the industry is highly vulnerable to energy price fluctuations, which can alter production costs by as much as 40% in a single quarter, impacting the competitiveness of ferrosilicon and calcium silicon.

- This is compounded by the variable renewable power availability for smelters committed to industrial decarbonization. Furthermore, the market is navigating the complexities of strategic raw material classification, which, while beneficial, adds regulatory burdens.

- The demand for critical infrastructure material like alkoxy silicone sealants is steady, but the broader market experiences volatility from the solar sector, where oversupply of high-purity polysilicon and silicon wafers can depress upstream prices. Obtaining carbon footprint certification for products made from quartzite raw material requires significant investment, adding another layer of financial pressure on producers of single-crystal wafers.

Exclusive Technavio Analysis on Customer Landscape

The silicon metal market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the silicon metal market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Silicon Metal Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, silicon metal market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Anyang Jinsheng Co. Ltd. - Offers metallurgical-grade silicon metal, ferrosilicon, and calcium silicon, catering to the specialized requirements of steelmaking and foundry industries worldwide.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Anyang Jinsheng Co. Ltd.

- Anyang Wanhua Metal Co. Ltd.

- Dow Chemical Co.

- Elkem ASA

- Ferroglobe Plc

- Hoshine Silicon Co. Ltd.

- Ligas de Aluminio S.A.

- Minasligas

- Mississippi Silicon

- PCC SE

- RIMA INDUSTRIAL

- RW silicium GmbH

- Shin Etsu Chemical Co. Ltd.

- Simcoa Operations Pty Ltd.

- Tokuyama Corp.

- United Co. RUSAL

- Wacker Chemie AG

- Westbrook Resources Ltd.

- Wynca Group

- Zhejiang Silicon Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Silicon metal market

- In September, 2024, the United States Department of Energy negotiated an award of up to $200 million for Group14 Technologies to construct a silane gas plant, a key precursor for advanced silicon battery materials.

- In September, 2024, PCC SE obtained the International Sustainability and Carbon Certification (ISCC) for its silicon metal production in Iceland, validating its low-carbon manufacturing process.

- In August, 2024, RIMA INDUSTRIAL formed a joint venture with SIMPAC to produce low-carbon ferrosilicon in Brazil, strengthening its commitment to sustainable metallurgical products.

- In February, 2025, Elkem ASA announced a strategic review of its Silicones division to optimize capital allocation and focus on its core Silicon Products and Carbon Solutions businesses.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Silicon Metal Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 297 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.4% |

| Market growth 2026-2030 | USD 2525.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.1% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The silicon metal market is undergoing a structural transformation, moving beyond its role as a traditional industrial silicon commodity. Its function as a primary alloying agent and deoxidizing agent for aluminum-silicon alloys and silumin alloys is being complemented by high-tech applications.

- The market now requires advanced materials like silicon-anode batteries and silicon-carbon composite for the energy sector, and single-crystal wafers, electronic-grade silicon, and semiconductor grade silicon for the digital economy. This diversification is driving investment in refining high-purity quartz and quartzite raw material into silicon wafers and high-purity polysilicon.

- The production of silicones, fumed silica, and alkoxy silicone sealants remains a key demand pillar. A central boardroom decision revolves around capital allocation for decarbonization, as the industry's electro-intensive smelting process, often using a submerged electric arc furnace for carbothermic reduction, is under scrutiny. Adopting bio-based reductants and other innovations can improve furnace efficiency by up to 5%.

- This pivot is critical for producing photovoltaic grade silicon for n-type topcon cells, silicon metal powder for advanced manufacturing, and materials for giga casting components, defining the next generation of metallurgical grade silicon and chemical grade silicon applications. This includes specialized products like ferrosilicon, calcium silicon, and silane gas, which are integral to modern electrometallurgy and silicone precursors.

What are the Key Data Covered in this Silicon Metal Market Research and Growth Report?

-

What is the expected growth of the Silicon Metal Market between 2026 and 2030?

-

USD 2.53 billion, at a CAGR of 5.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Metallurgy grade, and Chemical grade), Application (Aluminum alloys, Semiconductors, Solar panels, Stainless steel, and Others), Distribution Channel (Direct sales, and Indirect sales) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Surge in aluminum alloy demand for automotive lightweighting, High energy production costs and electricity price volatility

-

-

Who are the major players in the Silicon Metal Market?

-

Anyang Jinsheng Co. Ltd., Anyang Wanhua Metal Co. Ltd., Dow Chemical Co., Elkem ASA, Ferroglobe Plc, Hoshine Silicon Co. Ltd., Ligas de Aluminio S.A., Minasligas, Mississippi Silicon, PCC SE, RIMA INDUSTRIAL, RW silicium GmbH, Shin Etsu Chemical Co. Ltd., Simcoa Operations Pty Ltd., Tokuyama Corp., United Co. RUSAL, Wacker Chemie AG, Westbrook Resources Ltd., Wynca Group and Zhejiang Silicon Co. Ltd.

-

Market Research Insights

- The silicon metal market is shaped by a complex interplay of industrial decarbonization goals and the pursuit of critical mineral independence. The strategic raw material classification of silicon compels nations to foster domestic processing capabilities through friend-shoring trends and production linked incentive schemes, with some achieving up to a 15% reduction in supply chain risks.

- Energy security initiatives and the push for a robust silicon value chain are central to this transformation. As an energy-intensive industry, manufacturers focus on low-carbon production pathways and decarbonization of smelting to comply with regulations like the carbon border adjustment mechanism and facilitate scope 3 emissions tracking.

- This pivot toward downstream value-added applications and sustainable aluminum production, supported by carbon footprint certification, enables companies to meet compliance goals that improve market access by 25%. Circular economy initiatives and strategic mineral stockpiling further mitigate geopolitical trade barriers, while ensuring renewable power availability is crucial for electro-intensive manufacturing of this critical infrastructure material and renewable energy raw material.

We can help! Our analysts can customize this silicon metal market research report to meet your requirements.

RIA -

RIA -