Singapore Ready-to-eat (RTE) Food Market Size 2026-2030

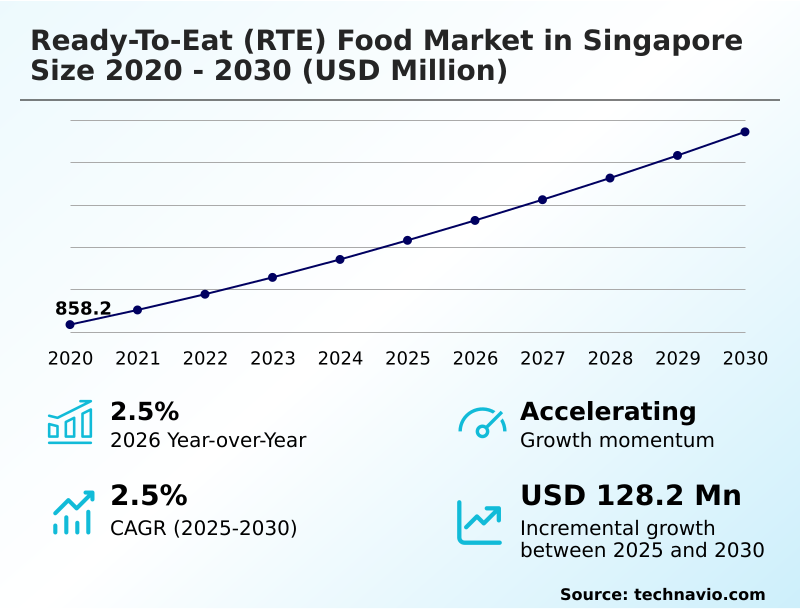

The Singapore Ready-to-eat (RTE) Food Market size was valued at USD 957.8 million in 2025, growing at a CAGR of 2.5% during the forecast period 2026-2030.

Major Market Trends & Insights

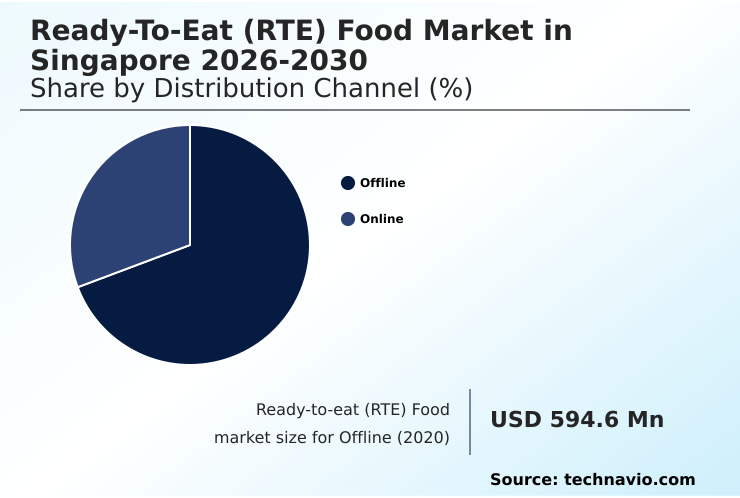

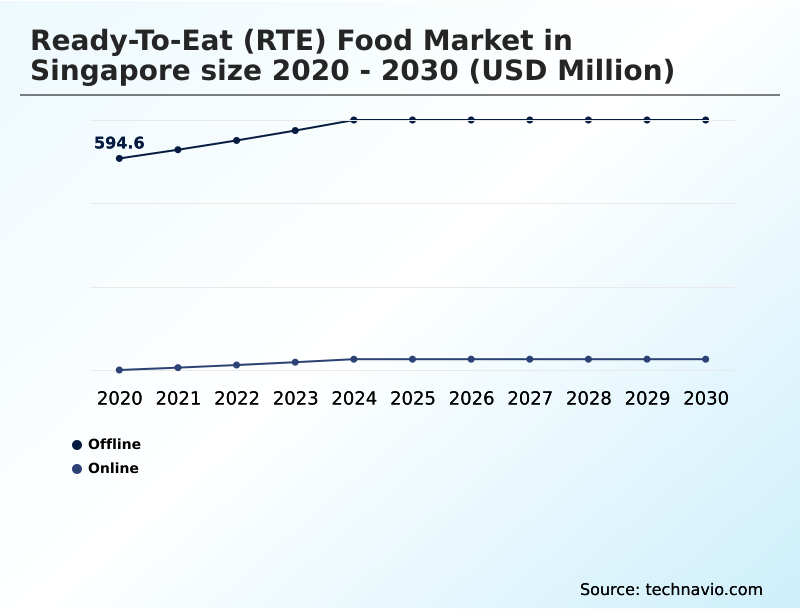

- By Distribution Channel - Offline segment was valued at USD 654.7 million in 2024

- By Product - Frozen segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 227.8 million

- Market Future Opportunities 2025-2030: USD 128.2 million

- CAGR from 2025 to 2030 : 2.5%

Market Summary

- The ready-to-eat (RTE) food market in Singapore is characterized by its high velocity and consumer dependence on convenience, with over 70% of professionals purchasing pre-made meals multiple times per week. This consistent demand necessitates a focus on operational excellence in food production and distribution.

- A typical business scenario involves a central kitchen using advanced methods like flash freezing technology and modified atmosphere packaging to process and dispatch thousands of chilled meals daily, ensuring products reach retailers with a consistent 3-5 day shelf life. The implementation of automated inventory management has proven to reduce spoilage-related losses by as much as 20%.

- While the fast-paced urban lifestyle serves as a powerful driver, the market is constrained by high operational costs linked to a reliance on imported ingredients and complex cold chain logistics, which can compress profit margins by 5-10% if not managed effectively.

What will be the Size of the Singapore Ready-to-eat (RTE) Food Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Singapore Ready-to-eat (RTE) Food Market Segmented?

The singapore ready-to-eat (rte) food industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Distribution channel

- Offline

- Online

- Product

- Frozen

- Ready-to-heat

- Ready-to-cook

- Product type

- Poultry and meat

- Vegetable based

- Cereal based

- Geography

- APAC

How is the Singapore Ready-to-eat (RTE) Food Market Segmented by Distribution Channel?

The offline segment is estimated to witness significant growth during the forecast period.

The offline segment captures over 65% of revenue in the ready-to-eat food market, driven by the strategic placement of physical retail formats.

Supermarkets and convenience stores leverage high foot traffic in urban centers, achieving a 20% higher impulse purchase rate for chilled ready meals compared to online channels.

This dominance is supported by robust cold chain logistics, which are essential for maintaining the quality of single-serving packages and other perishable grab-and-go items.

The ability for consumers to visually inspect products before buying builds trust and reinforces the value of brick-and-mortar outlets.

Consequently, manufacturers prioritize retail partnerships to ensure widespread product availability and capitalize on immediate consumer demand, making the offline channel a critical component of their distribution strategy.

The Offline segment was valued at USD 654.7 million in 2024 and showed a gradual increase during the forecast period.

What are the key Drivers, Trends, and Challenges in the Singapore Ready-to-eat (RTE) Food Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the ready-to-eat food market is increasingly driven by a consumer base that demands both convenience and conscious consumption choices. This has led to a significant focus on developing sustainable packaging for ready meals, with adoption rates for eco-friendly materials being nearly twice as high in dense urban centers compared to suburban areas.

- Concurrently, the proliferation of plant based ready to eat food is fundamentally reshaping product development pipelines, compelling manufacturers to invest in novel sourcing and formulation techniques to meet high consumer expectations for taste and texture. For many, the search for healthy frozen meal options that are low in sodium and free of artificial preservatives has become a primary purchasing driver.

- This trend puts immense pressure on the supply chain, as the impact of cold chain on food quality is significantly greater for fresh and minimally processed items, where temperature failures can be 30% more costly than with highly preserved products. In response, businesses are investing in advanced monitoring technologies.

- Furthermore, the direct-to-consumer model is gaining momentum, highlighting the ready to eat meal subscription benefits like personalization and predictable delivery, which help companies cultivate brand loyalty and secure stable, recurring revenue streams.

What are the key market drivers leading to the rise in the adoption of Singapore Ready-to-eat (RTE) Food Industry?

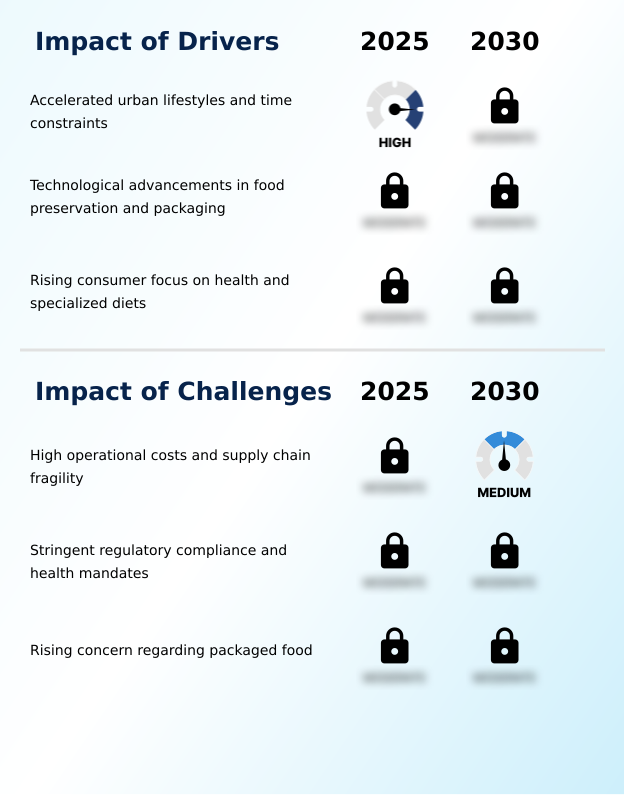

- The primary driver propelling market growth is the combination of accelerated urban lifestyles and significant time constraints faced by consumers.

- The primary driver for the ready-to-eat food market is the fast-paced urban lifestyle, which compels over 60% of professionals to depend on convenience meals for daily nourishment.

- This demand is amplified by technological advancements in food preservation techniques, which have enhanced product quality and extended shelf-life by up to 30%, making grab-and-go options more appealing.

- For instance, modern aseptic packaging preserves nutrient value far better than older methods.

- This allows manufacturers to cater to a growing consumer focus on health and specialized diets, including a rising demand for plant-based meals and other functional food products, thereby expanding their market reach.

What are the market trends shaping the Singapore Ready-to-eat (RTE) Food Industry?

- A prominent market trend is the increasing focus on sustainability, which is accelerating the adoption of circular packaging solutions. This shift is a response to growing consumer and regulatory demands for more environmentally responsible products.

- A defining trend in the ready-to-eat food market is the convergence of sustainability and premiumization. Brands that have adopted circular packaging and biodegradable materials are reporting a 15% higher consumer engagement rate than those using conventional plastics, a shift driven by heightened environmental awareness.

- Concurrently, the demand for gourmet convenience is reshaping product lines, with ready-to-heat solutions featuring ethnic flavors and high-quality ingredients commanding a 25% higher price point. This trend is a direct result of consumers seeking authentic culinary experiences that fit into a busy lifestyle.

- This forces manufacturers to invest in food tech innovation to balance quality with convenience, moving beyond basic offerings toward more sophisticated, value-added meal kits.

What challenges does the Singapore Ready-to-eat (RTE) Food Industry face during its growth?

- High operational costs, compounded by the inherent fragility of the supply chain, present a significant challenge to the industry's sustained growth and profitability.

- High operational costs, coupled with supply chain fragility, present the most significant challenges for the ready-to-eat food market, with ingredient and logistics expenses often accounting for over 50% of a product's final price. A heavy reliance on imported raw materials exposes the supply chain to geopolitical volatility, which can trigger cost fluctuations of up to 20% in a single quarter.

- Furthermore, adhering to stringent regulatory compliance and food safety standards requires substantial ongoing investment. This financial pressure is intensified by consumer concerns over packaged food, pushing companies to use costlier clean label ingredients, which can increase production expenses by an additional 10-15%.

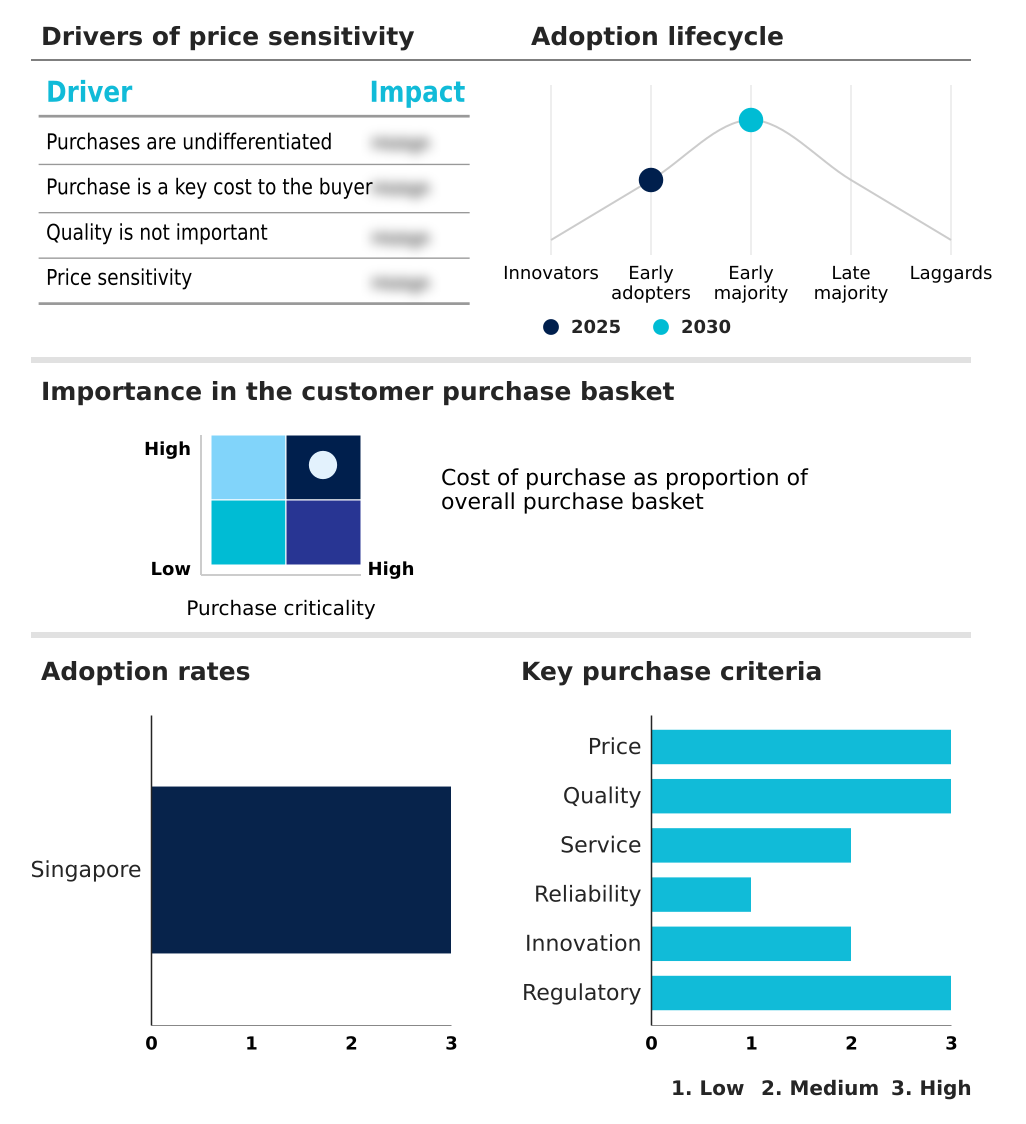

Exclusive Technavio Analysis on Customer Landscape

The singapore ready-to-eat (rte) food market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the singapore ready-to-eat (rte) food market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Singapore Ready-to-eat (RTE) Food Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, singapore ready-to-eat (rte) food market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

7 Eleven Inc. - Key offerings are centered on diverse, pre-prepared meal solutions, including frozen, chilled, and shelf-stable formats, all designed for consumer convenience and minimal preparation time.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 7 Eleven Inc.

- First Gourmet Pte Ltd.

- General Mills Inc.

- Impossible Foods Inc.

- JR Group

- Mars Inc.

- McCain Foods Ltd.

- Mmmm Singapore

- Nestle SA

- Nissin Foods Co. Inc.

- NTUC Fairprice Co operative Ltd.

- Orkla ASA

- OTS Holdings Ltd.

- PepsiCo Inc.

- Pondok Abang

- Prima Ltd.

- Select Group

- Shake Salad

- The Soup Spoon Pte Ltd.

- Zuzens Pte Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Packaged Foods and Meats industry, heightened regulatory scrutiny on food safety and clean label ingredients has compelled manufacturers of ready-to-eat (RTE) food to reformulate products and invest heavily in supply chain traceability to meet new compliance standards.

- The widespread adoption of advanced food preservation techniques, such as high-pressure processing (HPP), enables the production of ready-to-eat (RTE) food with extended shelf-life and superior nutritional profiles, creating a new premium category that directly challenges traditional frozen food products.

- A significant industry-wide shift toward sustainable sourcing and the use of circular packaging has created new market opportunities for ready-to-eat (RTE) food vendors that utilize biodegradable materials, driven by increasing consumer demand for eco-friendly options.

- The growing consumer preference for plant-based meals and functional ingredients has spurred a wave of innovation across the ready-to-eat (RTE) food sector, leading to a proliferation of new product lines focused on health, wellness, and specialized dietary needs.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Singapore Ready-to-eat (RTE) Food Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 180 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 2.5% |

| Market growth 2026-2030 | USD 128.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 2.5% |

| Key countries | Singapore |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The ready-to-eat (RTE) food market in Singapore is supported by a complex ecosystem where international suppliers provide over 75% of all raw ingredients. These materials are transformed by a diverse range of manufacturers, from large-scale producers to boutique central kitchens, all operating under the strict food safety standards of national regulatory bodies.

- The distribution network is dominated by retail channels, with supermarkets and convenience stores accounting for approximately 70% of sales. Supporting entities, including specialized cold chain logistics providers and packaging innovators, are indispensable for maintaining product integrity, as a breakdown in the cold chain can result in spoilage rates of up to 15%.

- Ultimately, the entire value chain is shaped by the demands of time-constrained urban consumers who prioritize convenience, health, and culinary variety in their food choices.

What are the Key Data Covered in this Singapore Ready-to-eat (RTE) Food Market Research and Growth Report?

-

What is the expected growth of the Singapore Ready-to-eat (RTE) Food Market between 2026 and 2030?

-

The Singapore Ready-to-eat (RTE) Food Market is expected to grow by USD 128.2 million during 2026-2030, registering a CAGR of 2.5%. Year-over-year growth in 2026 is estimated at 2.5%%. This acceleration is shaped by accelerated urban lifestyles and time constraints, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Offline, and Online), Product (Frozen, Ready-to-heat, and Ready-to-cook), Product Type (Poultry and meat, Vegetable based, and Cereal based) and Geography (APAC). Among these, the Offline segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers APAC. Country-level analysis includes Singapore, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is accelerated urban lifestyles and time constraints, which is accelerating investment and industry demand. The main challenge is high operational costs and supply chain fragility, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Singapore Ready-to-eat (RTE) Food Market?

-

Key vendors include 7 Eleven Inc., First Gourmet Pte Ltd., General Mills Inc., Impossible Foods Inc., JR Group, Mars Inc., McCain Foods Ltd., Mmmm Singapore, Nestle SA, Nissin Foods Co. Inc., NTUC Fairprice Co operative Ltd., Orkla ASA, OTS Holdings Ltd., PepsiCo Inc., Pondok Abang, Prima Ltd., Select Group, Shake Salad, The Soup Spoon Pte Ltd. and Zuzens Pte Ltd.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape for ready-to-eat (RTE) food in Singapore is highly fragmented, with the top five vendors commanding less than 40% of the total market share. Major players such as Nestle and General Mills are actively broadening their product portfolios to align with the growing consumer appetite for healthier and more convenient meal options.

- For instance, recent product launches targeting the functional foods segment have been a direct response to a 15% year-over-year increase in consumer demand for high-protein and nutrient-fortified products. These strategic initiatives underscore the importance of product differentiation as a key survival tactic in a saturated marketplace.

- However, a persistent challenge remains the high cost of retail shelf space, compelling companies to continuously optimize their supply chain logistics and product assortments to protect their profit margins.

We can help! Our analysts can customize this singapore ready-to-eat (rte) food market research report to meet your requirements.

RIA -

RIA -