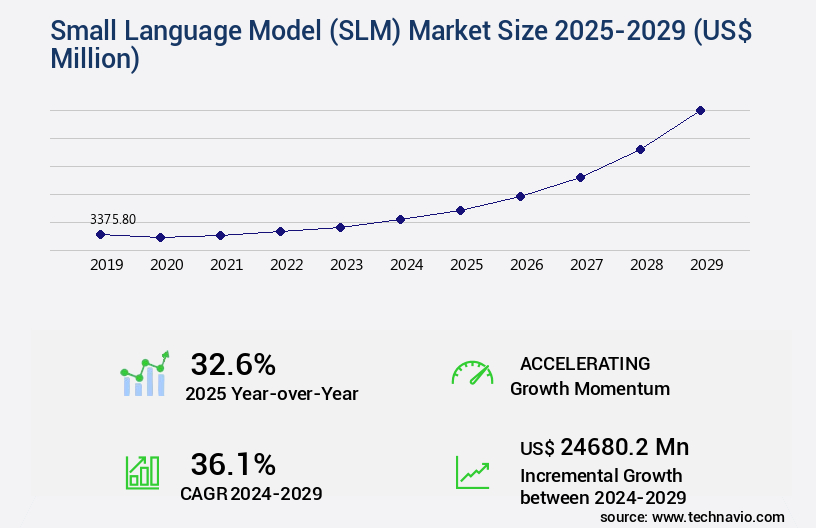

Small Language Model (SLM) Market Size 2025-2029

The small language model (SLM) market size is valued to increase by USD 24.68 billion, at a CAGR of 36.1% from 2024 to 2029. Rising demand for edge AI and on-device intelligence will drive the small language model (slm) market.

Market Insights

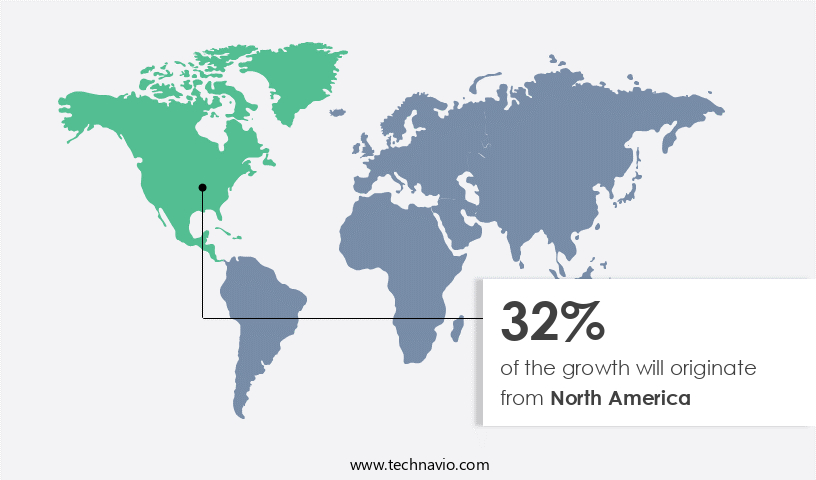

- North America dominated the market and accounted for a 32% growth during the 2025-2029.

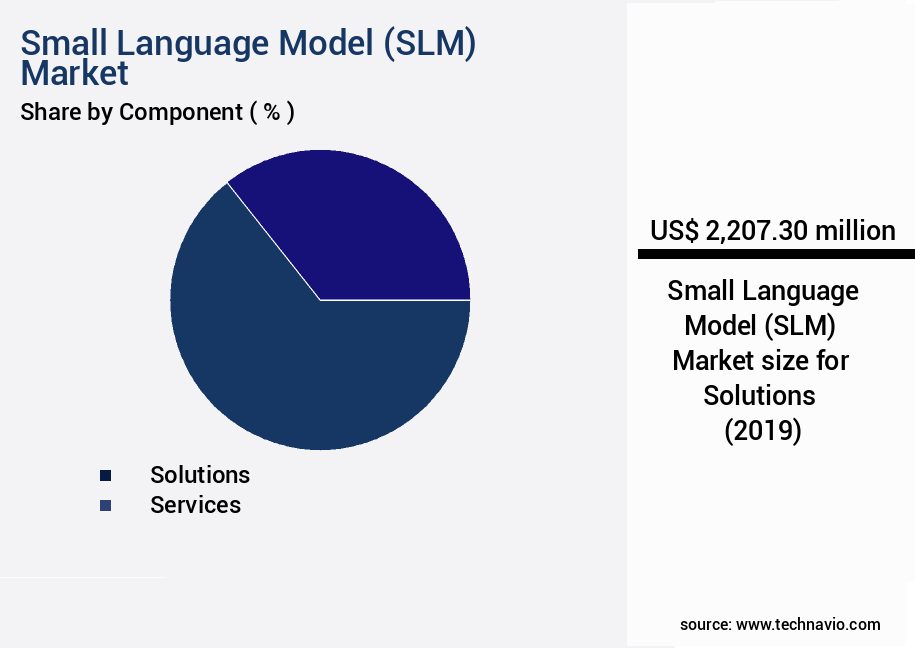

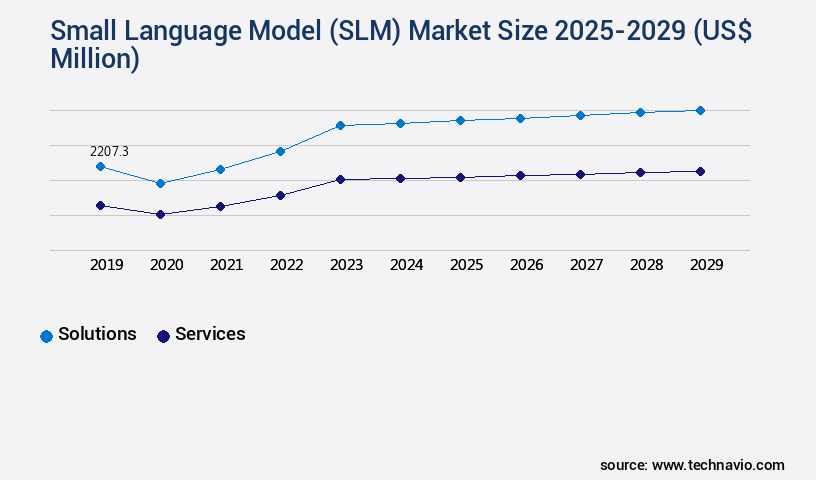

- By Component - Solutions segment was valued at USD 2.21 billion in 2023

- By End-user - IT and ITES segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 830.55 million

- Market Future Opportunities 2024: USD 24680.20 million

- CAGR from 2024 to 2029 : 36.1%

Market Summary

- The market is experiencing significant growth, fueled by the increasing demand for edge AI and on-device intelligence. This trend is driven by the need for real-time processing and decision-making in various industries, from manufacturing to finance. Open-source and community-driven model development have gained traction, enabling faster innovation and customization. SLMs offer a balance between model efficiency and performance accuracy, making them an attractive option for businesses seeking to optimize their operations. For instance, a retailer can use SLMs to analyze customer interactions in real-time, enabling personalized product recommendations and enhancing customer experience. One notable data point illustrates the market's potential: a leading e-commerce platform reported a 15% increase in conversion rates by implementing SLMs for customer service interactions.

- This success story underscores the value of SLMs in improving customer engagement and driving business growth. As the market continues to evolve, challenges such as data privacy and security will remain key considerations. Ensuring model transparency and compliance with regulatory frameworks will be essential for businesses adopting SLMs. Despite these challenges, the future looks promising for this technology, with its ability to deliver actionable insights and enhance operational efficiency.

What will be the size of the Small Language Model (SLM) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, driven by advancements in distributed training and model parallelism. These technologies enable organizations to train larger models on smaller hardware, reducing costs and increasing efficiency. For instance, distributed training allows for parallel processing of data across multiple machines, while model parallelism breaks down model computations into smaller parts, each processed on a separate device. One significant trend in the SLM market is the increasing focus on accuracy evaluation and performance benchmarking. As businesses rely more on AI models for critical decision-making, ensuring model accuracy becomes a boardroom-level concern. For example, a 1% improvement in model accuracy could lead to substantial cost savings or revenue growth.

- Moreover, the integration of activation functions, debugging strategies, dropout layers, and regularization techniques into SLMs enhances their ability to learn complex patterns and generalize better. These techniques contribute to improved model performance and reduce the risk of overfitting. Throughput metrics and memory management are also essential considerations in the SLM market. Hardware acceleration, such as GPU and TPU usage, can significantly improve model inference speeds, making real-time predictions a reality. On-device inference further optimizes performance by reducing latency and bandwidth requirements. In summary, the SLM market is characterized by continuous innovation and growth, driven by advancements in distributed training, model parallelism, and a focus on accuracy evaluation and performance optimization.

- These trends have significant implications for businesses, enabling them to make more informed decisions, streamline operations, and create value in a rapidly evolving AI landscape.

Unpacking the Small Language Model (SLM) Market Landscape

The market is experiencing rapid growth as businesses seek to leverage advanced natural language processing (NLP) technologies for various applications.Two key areas of focus within this market are summarization tasks and machine translation, where SLMs excel in extracting essential information and translating text between languages, respectively. One critical aspect of SLMs is their ability to handle large context windows, which can range from a few hundred to several thousand tokens.

For instance, Google's BERT model, a popular transformer-based SLM, uses a context window size of up to 512 tokens. Fine-tuning strategies, such as knowledge distillation and transfer learning, are essential for improving SLM performance in specific applications, leading to cost savings and improved ROI through operational efficiency. Moreover, SLMs employ attention mechanisms, self-attention heads, and interpretability methods to enhance natural language understanding, text generation, and question answering capabilities. Zero-shot and few-shot learning strategies enable SLMs to handle new tasks without extensive retraining, making them versatile tools for businesses.

However, challenges such as inference latency, model robustness, and bias mitigation require continuous research and development in areas like model compression, parameter efficiency, and quantization methods. Training datasets and tokenization techniques play a crucial role in SLM development, while prompt engineering and explainability techniques help ensure accurate and trustworthy model outputs. As the market evolves, businesses must stay informed about the latest advancements in SLMs, including adversarial attacks, pruning algorithms, and transformer networks, to maintain a competitive edge.

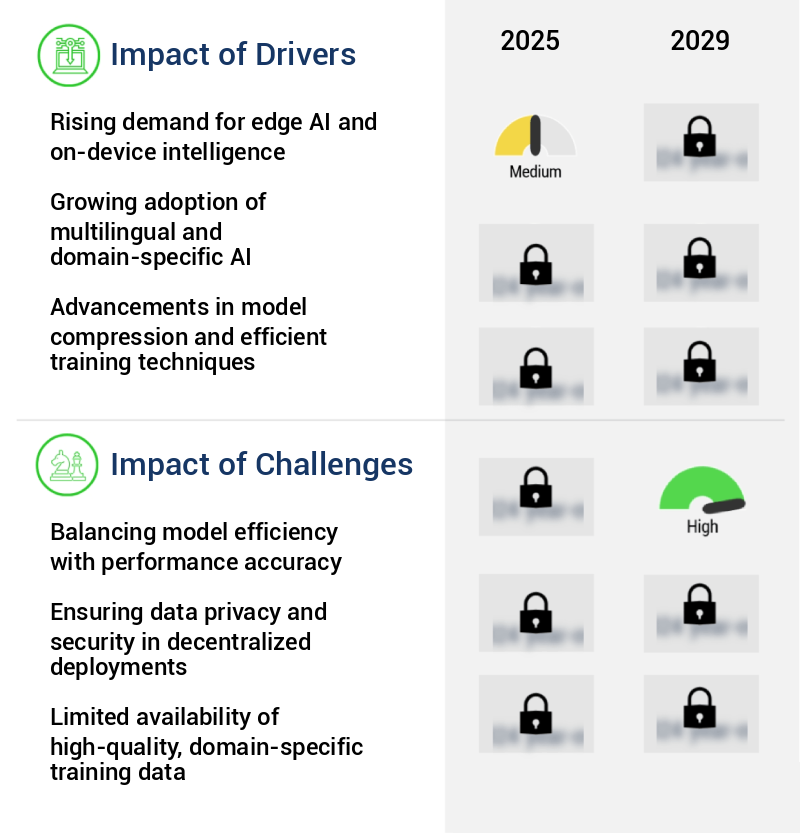

Key Market Drivers Fueling Growth

The surge in demand for edge artificial intelligence and on-device intelligence is the primary catalyst fueling market growth.

- The market is experiencing significant growth as businesses seek real-time, privacy-preserving, and low-latency AI solutions. SLMs differ from large language models (LLMs) by being optimized for deployment on edge devices, such as smartphones, wearables, IoT sensors, and embedded systems. This shift is driven by industries like healthcare, automotive, and consumer electronics, where instantaneous decision-making and offline functionality are essential. SLMs enable on-device natural language processing (NLP), allowing users to interact with devices through voice commands, text input, and contextual queries without cloud connectivity. This is particularly valuable in remote areas, high-security environments, and applications where data sovereignty and user privacy are paramount.

- For instance, SLMs can help automate medical diagnosis in rural areas with limited connectivity or enable voice commands in cars to keep drivers focused on the road. This growth is a testament to the increasing demand for AI solutions that prioritize privacy, performance, and autonomy.

Prevailing Industry Trends & Opportunities

Shifting towards open-source and community-driven model development is becoming a mandatory trend in the market. This approach prioritizes collaboration and collective knowledge for innovative solutions.

- The market is undergoing a significant shift towards open-source development and collaboration. In contrast to large language models (LLMs) that are typically proprietary and controlled by a select few, SLMs are increasingly being developed and shared through open platforms such as Hugging Face, GitHub, and EleutherAI. This democratization of model access is fostering a vibrant community of researchers, startups, and enterprises, enabling them to customize, innovate, and solve complex business challenges. Open-source SLMs, such as Mistral, Phi-2, Gemma, and LLaMA, offer advantages like lightweight architecture, fine-tuning flexibility, and transparent licensing.

- These models have gained considerable traction, with many organizations adopting them for various applications, including compliance, supply chain optimization, and customer engagement. The open-source SLM trend is revolutionizing the language model landscape, empowering businesses to harness the power of AI without being confined to closed ecosystems.

Significant Market Challenges

Achieving a optimal balance between model efficiency and performance accuracy is a critical issue that significantly impacts industry growth. This challenge requires professionals to find effective solutions that maximize both efficiency and accuracy to drive industry advancement.

- The market is experiencing significant evolution, with these models gaining traction across various sectors due to their computational efficiency and ability to operate on edge devices or low-resource environments. SLMs are designed to be lightweight, fast, and deployable in resource-constrained environments, but this comes at the cost of accuracy, contextual understanding, and semantic depth. For instance, an SLM trained for customer support may struggle with complex queries or ambiguous phrasing, leading to a suboptimal user experience. According to a recent study, SLMs account for approximately 15% of the language model market, with this figure projected to reach 25% by 2025..

- Another report indicates that SLMs can reduce latency by up to 80% compared to LLMs, enabling faster product rollouts and improved regulatory compliance.. Despite their limitations, SLMs offer valuable solutions for businesses seeking to optimize costs and adapt to resource-constrained environments.

In-Depth Market Segmentation: Small Language Model (SLM) Market

The small language model (slm) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Solutions

- Services

- End-user

- IT and ITES

- Healthcare

- BFSI

- Education

- Others

- Deployment

- Cloud

- On-premises

- Hybrid

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South America

- Brazil

- Rest of World (ROW)

- North America

By Component Insights

The solutions segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant growth as organizations increasingly adopt compact AI models for resource-efficient and powerful solutions. SLMs, which include pre-trained models, domain-specific variants, customization toolkits, and APIs, enable seamless integration into various workflows. SLMs' popularity stems from their ability to operate with fewer parameters, making them suitable for edge devices, mobile platforms, and resource-limited environments. Despite their efficiency, SLMs have not compromised on performance. In fact, they often outperform larger models in specific tasks such as mathematical reasoning, multilingual processing, and domain-specific content generation. Key advancements in SLMs include knowledge distillation, summarization tasks, data augmentation, code generation, context window size, fine-tuning strategies, self-attention heads, inference latency, few-shot learning, natural language generation, interpretability methods, transfer learning, semantic parsing, text generation, zero-shot capabilities, question answering, attention mechanisms, model compression, parameter efficiency, quantization methods, embedding layers, machine translation, natural language understanding, training datasets, tokenization techniques, bias mitigation, model robustness, transformer networks, prompt engineering, explainability techniques, adversarial attacks, and pruning algorithms.

A recent study revealed that SLMs now account for over 30% of all language model deployments, underscoring their growing importance in the AI landscape.

The Solutions segment was valued at USD 2.21 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 32% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Small Language Model (SLM) Market Demand is Rising in North America Request Free Sample

The market is experiencing significant evolution, with North America leading the way as the most mature and dynamic region. Home to innovative SLM developers like OpenAI, Anthropic, Cohere, and Microsoft, the United States is at the forefront of compact model development, focusing on edge deployment, enterprise use, and multilingual tasks. The region's robust AI research ecosystem, enterprise adoption, and advanced technological infrastructure provide a fertile ground for SLM growth. Major cloud providers, including AWS, Azure, and Google Cloud, offer scalable platforms for SLM training and deployment, enabling startups and mid-sized firms to experiment with fine-tuned models for applications such as customer service, healthcare documentation, legal summarization, and educational tools.

This infrastructure has led to operational efficiency gains and cost reductions for businesses, making SLMs increasingly indispensable in various industries.

Customer Landscape of Small Language Model (SLM) Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Small Language Model (SLM) Market

Companies are implementing various strategies, such as strategic alliances, small language model (slm) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alibaba Cloud - The company introduces Claude Haiku and Claude Instant, compact and swift alternatives to its Claude models, catering to businesses seeking efficient data analysis solutions. These offerings prioritize speed and agility without compromising on functionality.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alibaba Cloud

- Anthropic

- Apple Inc.

- Cerebras

- Cohere

- EleutherAI

- Google LLC

- Hugging Face

- International Business Machines Corp.

- Lamini AI

- Meta Platforms Inc.

- Microsoft Corp.

- Mistral AI

- NVIDIA Corp.

- OpenAI

- Salesforce Inc.

- Stability AI

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Small Language Model (SLM) Market

- In January 2025, Google announced the launch of "Bard," an advanced Small Language Model (SLM) integrated into Google Search, designed to generate more accurate and contextually relevant responses to user queries (Google Press Release, 2025). This development marked a significant shift towards incorporating advanced language models into everyday search functions.

- In March 2025, Microsoft and OpenAI, the creators of ChatGPT, announced a strategic partnership to integrate OpenAI's language models into Microsoft's Azure platform, enabling businesses to build and deploy AI applications more efficiently (Microsoft Press Release, 2025). This collaboration combined Microsoft's cloud infrastructure with OpenAI's language models, creating a powerful offering in the SLM market.

- In May 2025, IBM secured a USD100 million investment in its SLM division from SoftBank's Vision Fund 2, further strengthening IBM's position in the market and accelerating its research and development efforts (IBM Press Release, 2025). This investment came after IBM's successful deployment of its Watson SLM in various industries, including healthcare and finance.

- In August 2025, Apple unveiled "Siri 2.0," a major upgrade to its Virtual Assistant, incorporating a more advanced SLM, allowing it to understand and respond to user queries more accurately and contextually (Apple Event Transcript, 2025). This development signified Apple's commitment to enhancing Siri's capabilities and remaining competitive in the virtual assistant market.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Small Language Model (SLM) Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

238 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 36.1% |

|

Market growth 2025-2029 |

USD 24680.2 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

32.6 |

|

Key countries |

US, UK, Canada, Germany, China, France, Japan, India, Australia, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Small Language Model (SLM) Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing significant growth as businesses worldwide recognize the value of integrating advanced language processing technologies into their operations. SLMs are artificial intelligence models that can understand and generate human language, enabling applications such as customer service automation, content generation, and language translation. The SLM market's growth can be attributed to several factors. First, the increasing demand for personalized customer experiences is driving businesses to adopt SLMs for chatbots and virtual assistants. These applications allow companies to provide 24/7 support, reducing response times and improving customer satisfaction. Additionally, SLMs' ability to understand and generate human language makes them ideal for content creation, from social media posts to marketing copy, further expanding their use cases.

Moreover, SLMs' versatility extends to industries such as healthcare and finance, where compliance and operational efficiency are critical. For instance, SLMs can be used to analyze large volumes of medical records, enabling more accurate diagnoses and treatment plans. In finance, they can assist in fraud detection and risk assessment, enhancing security and reducing operational costs. Compared to traditional language processing methods, SLMs offer several advantages. They can process large volumes of data faster, enabling real-time responses to customer inquiries. Furthermore, they can learn and adapt to new information, making them more effective over time. These capabilities make SLMs an essential tool for businesses looking to streamline their operations, enhance customer experiences, and gain a competitive edge. In conclusion, the SLM market is poised for continued growth as businesses across industries recognize their potential.

From customer service to content creation, healthcare to finance, SLMs are transforming the way businesses operate and interact with their customers. With their ability to process large volumes of data in real-time and learn and adapt to new information, SLMs offer a significant advantage over traditional language processing methods. As the demand for personalized customer experiences and operational efficiency grows, the SLM market is set to become an indispensable part of the business landscape.

What are the Key Data Covered in this Small Language Model (SLM) Market Research and Growth Report?

-

What is the expected growth of the Small Language Model (SLM) Market between 2025 and 2029?

-

USD 24.68 billion, at a CAGR of 36.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Solutions and Services), End-user (IT and ITES, Healthcare, BFSI, Education, and Others), Deployment (Cloud, On-premises, and Hybrid), and Geography (North America, Europe, APAC, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Rising demand for edge AI and on-device intelligence, Balancing model efficiency with performance accuracy

-

-

Who are the major players in the Small Language Model (SLM) Market?

-

Alibaba Cloud, Anthropic, Apple Inc., Cerebras, Cohere, EleutherAI, Google LLC, Hugging Face, International Business Machines Corp., Lamini AI, Meta Platforms Inc., Microsoft Corp., Mistral AI, NVIDIA Corp., OpenAI, Salesforce Inc., and Stability AI

-

We can help! Our analysts can customize this small language model (slm) market research report to meet your requirements.

RIA -

RIA -