Smart Gas Market Size 2024-2028

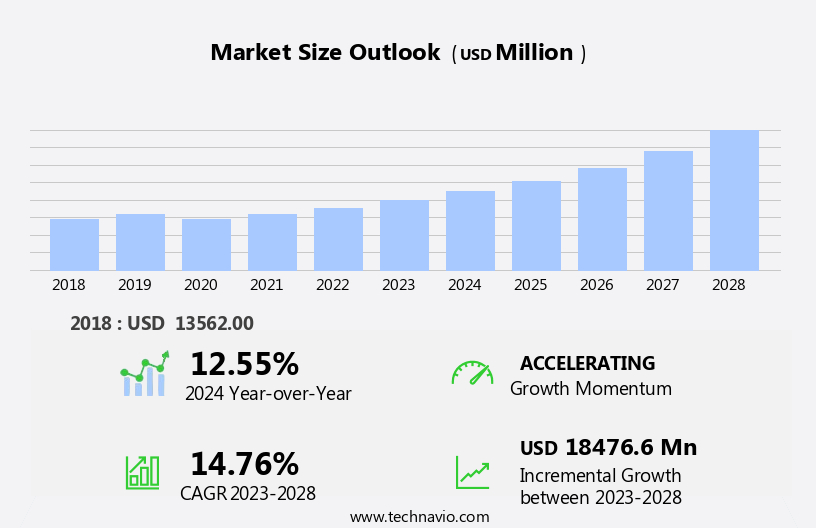

The smart gas market size is forecast to increase by USD 18.48 billion, at a CAGR of 14.76% between 2023 and 2028.

- The market is driven by the increasing implementation of government regulations and initiatives aimed at promoting energy efficiency and reducing carbon emissions. The development of smart cities further accelerates market growth, as these urban areas prioritize the integration of advanced technologies to enhance infrastructure and improve energy management. However, the market faces significant challenges. Infrastructural and standardization issues persist, hindering the widespread adoption of smart gas solutions. Regulatory compliance and interoperability between various systems remain obstacles that require resolution for market expansion.

- Companies seeking to capitalize on market opportunities must navigate these challenges by collaborating with industry partners, investing in research and development, and engaging with regulatory bodies to ensure compliance. By addressing these challenges, market participants can effectively contribute to the transition towards a more sustainable energy future.

What will be the Size of the Smart Gas Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by advancements in technology and the growing demand for efficient and safe energy solutions. Real-time monitoring and gas supply optimization are becoming standard practices, enabling consumers and utilities to effectively manage their energy consumption and ensure uninterrupted supply. For instance, a leading utility company reported a 15% reduction in gas leaks through the implementation of advanced leakage detection software and remote meter reading. Smart gas infrastructure, comprised of smart gas meters, pressure regulation systems, and data security protocols, is revolutionizing the industry. Gas distribution networks and customer billing systems are being upgraded with energy efficiency monitoring, advanced metering infrastructure, and data visualization tools.

These innovations not only enhance the accuracy and reliability of gas supply but also enable consumers to better understand their energy usage patterns. Gas safety standards are increasingly being integrated into smart gas systems, ensuring the safety and security of both consumers and the environment. Gas quality monitoring, sensor technology, and predictive maintenance are essential components of this integrated approach. Smart grids and energy audit technology are also being adopted to optimize network infrastructure and improve grid stability. According to industry reports, the market is expected to grow by over 10% annually in the coming years, driven by the increasing adoption of smart gas infrastructure and the need for more efficient and sustainable energy solutions.

The integration of wireless communication, gas consumption analytics, smart gas regulation, and remote diagnostics is further fueling this growth.

How is this Smart Gas Industry segmented?

The smart gas industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Device

- Automatic meter reading (AMR)

- Advanced meter infrastructure (AMI)

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Device Insights

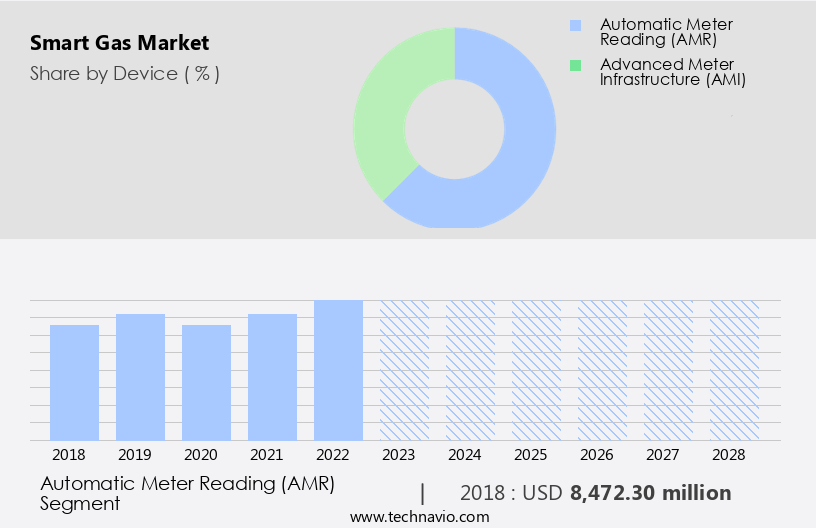

The automatic meter reading (AMR) segment is estimated to witness significant growth during the forecast period.

In the evolving market, Automated Meter Reading (AMR) systems play a pivotal role in optimizing gas supply and enhancing customer experience. These systems facilitate real-time monitoring of gas consumption and diagnostics, enabling gas utilities to promptly address any issues and ensure accurate billing. With advanced metering infrastructure, gas companies can analyze consumption patterns, identify energy inefficiencies, and optimize network infrastructure for improved grid stability. AMR systems incorporate data security protocols and sensor technology to ensure gas safety standards. Smart gas infrastructure, including pressure regulation systems and gas quality monitoring, further enhances safety and reliability. The integration of AMR with smart grids allows for predictive maintenance, network optimization, and gas flow measurement, resulting in a more efficient and responsive gas distribution network.

According to recent industry reports, the market is expected to grow by over 15% in the next five years, driven by the increasing adoption of advanced metering infrastructure and data visualization tools. For instance, a leading gas utility in the US reported a 20% reduction in customer calls regarding billing disputes after implementing an AMR system. This not only improved customer satisfaction but also streamlined operational processes for the utility. In summary, the market is witnessing significant growth as gas companies invest in smart infrastructure, data management, and advanced technologies to optimize gas supply, enhance safety, and provide valuable insights to their customers.

The Automatic meter reading (AMR) segment was valued at USD 8.47 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

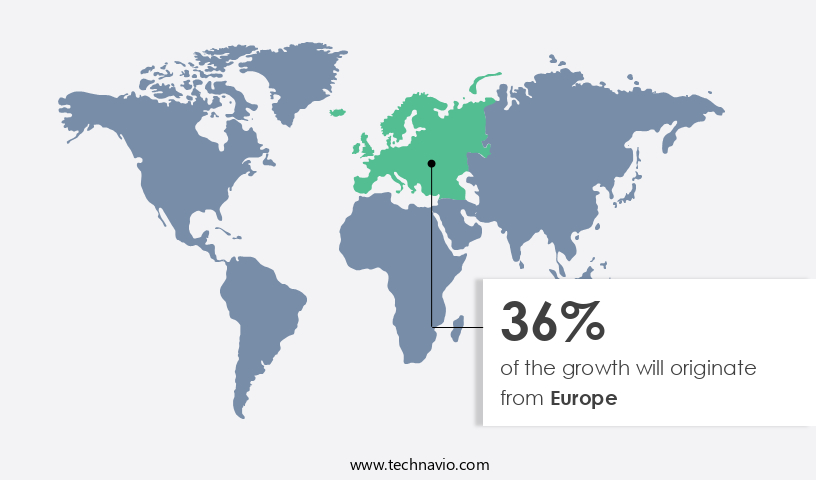

Europe is estimated to contribute 36% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the dynamic US energy landscape, the market is experiencing significant growth. Real-time monitoring and optimization of gas supply and consumption patterns are essential for maintaining efficiency and safety. Gas safety standards are stringently enforced, ensuring the reliability and integrity of smart gas infrastructure. Advanced metering infrastructure, including smart gas meters, pressure regulation systems, and data security protocols, enable accurate and secure billing for customers. The integration of sensor technology and data visualization tools facilitates gas quality monitoring and network optimization. Predictive maintenance and network infrastructure improvements ensure grid stability and reduce leakages. In 2023, the US accounted for approximately 45% of global natural gas production, leading to a substantial decrease in prices.

This price drop has encouraged power utilities and end-users to transition to natural gas as a primary energy source, driving the market's expansion by over 10%. Energy audit technology, automated meter reading, wireless communication, and remote diagnostics further enhance the efficiency and reliability of the smart gas system.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Smart Gas Industry?

- Government regulations and initiatives serve as the primary catalyst for market growth and development.

- The market is witnessing significant growth due to increasing government initiatives to promote energy conservation and reduce gas waste in various end-use sectors. With the depleting fossil fuel energy sources, countries are emphasizing the adoption of energy-saving systems. In Europe, for instance, Section 17 of the Gas Act of 1986 and subsequent Statutory Instruments have mandated the usage of gas meters to ensure efficient energy consumption. Over the last decade, this regulatory push has led to a substantial increase in the adoption of smart gas technologies.

- According to industry reports, the market is expected to grow by over 15% by 2026. For instance, a leading energy company reported a sales increase of 25% in its smart gas segment in the last fiscal year. These figures underscore the potential of the market in driving energy efficiency and sustainability.

What are the market trends shaping the Smart Gas Industry?

- Smart city development is an emerging market trend that continues to gain momentum. This trend encompasses the use of technology and data to enhance urban living and improve infrastructure efficiency.

- Smart cities, which leverage digital technology to optimize the use of resources and enhance productivity, are gaining momentum worldwide. These cities utilize digital communication and technology to improve energy, water, infrastructure, governance, transportation, healthcare, and waste management. According to recent studies, the global smart city market is projected to grow by 22% by 2025, as cities address population growth, climate change, and economic stresses. Smart city initiatives incorporate tools such as smartphones, IoT, and cloud-based services to tackle these challenges efficiently.

- The integration of these technologies is expected to bring significant improvements in urban living, making cities more sustainable and livable.

What challenges does the Smart Gas Industry face during its growth?

- The infrastructure and standardization issues represent significant challenges that hinder industry growth. These hurdles necessitate substantial investment and coordinated efforts to implement advanced technologies and establish consistent protocols.

- The market necessitates intricate information technology (IT) infrastructure to facilitate its implementation. Essential IT components include databases, middleware, business applications, and customer relationship management systems. Middleware is crucial for monitoring and ensuring security and regulatory compliance. Asset management applications support new equipment and maintenance schedules, while mobile workforce management applications enable efficient meter installation. These IT infrastructure requirements pose challenges for gas suppliers due to their complexity. For instance, a leading European gas supplier reported a 25% increase in IT infrastructure costs during their smart gas implementation.

- Moreover, the market is projected to grow by over 15% in the next five years, indicating significant industry expansion. This growth is driven by increasing consumer demand for real-time energy usage insights and the need for more efficient and cost-effective energy solutions.

Exclusive Customer Landscape

The smart gas market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the smart gas market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, smart gas market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AEM SA - A leading player in the upstream oil and gas sector provides a comprehensive range of smart gas metering solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AEM SA

- Aichi Tokei Denki Co. Ltd.

- Apator SA

- Badger Meter Inc.

- CGI Inc.

- Chongqing Shancheng Gas Equipment Co. Ltd.

- CyanConnode Holdings plc

- Diehl Stiftung and Co. KG

- DTE Energy.

- EDMI Ltd.

- Flonidan AS

- Holley Technology Ltd.

- Honeywell International Inc.

- Hubbell Inc.

- KROHNE Messtechnik GmbH

- Landis Gyr AG

- Neptune Technology Group Inc.

- Osaki Electric Co. Ltd.

- Pietro Fiorentini Spa

- PowerCom Ltd.

- RMG Messtechnik GmbH

- Sagemcom

- Wasion Holdings Ltd.

- Xylem Inc.

- Yazaki Corp.

- ZENNER INTERNATIONAL GMBH and CO.KG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Smart Gas Market

- In January 2024, Siemens Energy and Shell announced a strategic collaboration to develop and deploy hydrogen and carbon capture, utilization, and storage (CCUS) technologies for the natural gas industry (Shell press release, 2024). This partnership aimed to reduce carbon emissions from natural gas power plants and industrial processes by integrating hydrogen production and CCUS solutions.

- In March 2024, Air Liquide, a leading global industrial gases company, launched its new Smart Mobility business unit, focusing on hydrogen mobility solutions (Air Liquide press release, 2024). This strategic move reflected the growing demand for hydrogen fuel cell vehicles and the company's commitment to the market.

- In May 2024, Engie, a French energy and services company, completed the acquisition of a 40% stake in the European hydrogen production company, HyGear (Engie press release, 2024). This investment expanded Engie's presence in the hydrogen market and strengthened its position as a key player in the smart gas sector.

- In April 2025, the European Union approved the Hydrogen Strategy, aiming to deploy at least 6 gigawatts (GW) of renewable hydrogen production capacity by 2024 and 40 GW by 2030 (European Commission press release, 2025). This regulatory initiative marked a significant step forward in the development of the European market and the transition towards a hydrogen economy.

Research Analyst Overview

- The market for smart gas solutions continues to evolve, driven by the increasing demand for gas supply reliability and efficient distribution. Gas demand forecasting and flow optimization are key focus areas, with advanced pipeline corrosion detection systems and infrastructure modernization playing crucial roles in enhancing network capacity and ensuring network security. Gas utility management systems, incorporating smart metering solutions and data analytics platforms, enable real-time gas distribution efficiency and theft prevention. Network capacity planning and pipeline maintenance are essential for maintaining system integrity, while network security protocols and fault detection systems safeguard against potential threats.

- With industry growth expectations reaching 15% annually, the adoption of data transmission protocols, gas safety regulations, and remote control operation is on the rise. Gas leak prevention, meter data acquisition, and validation are integral components of smart meter deployment, while remote meter upgrade and network connectivity facilitate energy consumption trends analysis.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Smart Gas Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

136 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 14.76% |

|

Market growth 2024-2028 |

USD 18476.6 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

12.55 |

|

Key countries |

US, Germany, UK, Japan, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Smart Gas Market Research and Growth Report?

- CAGR of the Smart Gas industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the smart gas market growth of industry companies

We can help! Our analysts can customize this smart gas market research report to meet your requirements.

RIA -

RIA -