Space-based Missile Tracking Sensor Systems Market Size 2026-2030

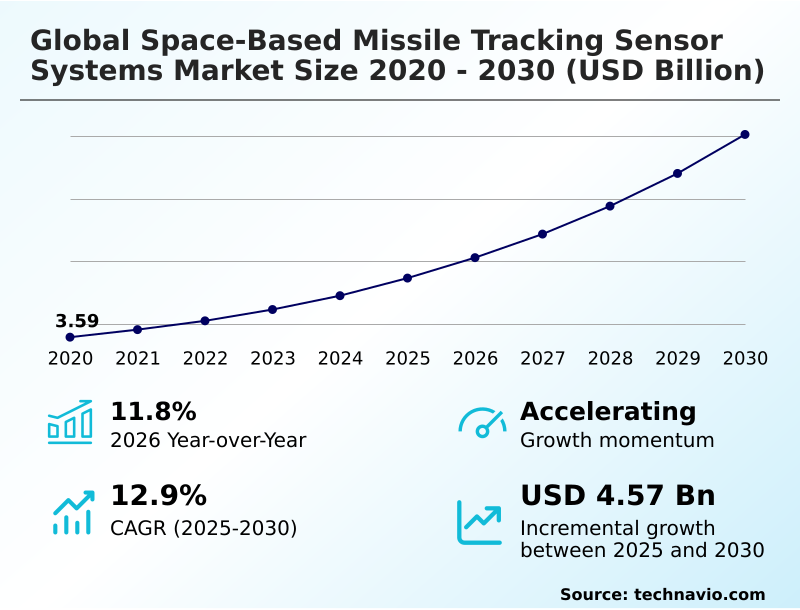

The space-based missile tracking sensor systems market size is valued to increase by USD 4.57 billion, at a CAGR of 12.9% from 2025 to 2030. Proliferation of hypersonic weaponry and requirement for advanced tracking capabilities will drive the space-based missile tracking sensor systems market.

Major Market Trends & Insights

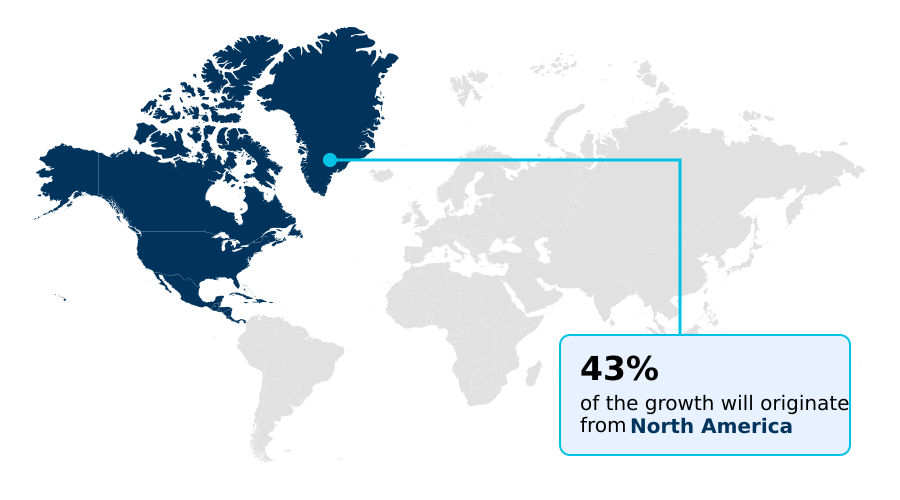

- North America dominated the market and accounted for a 43% growth during the forecast period.

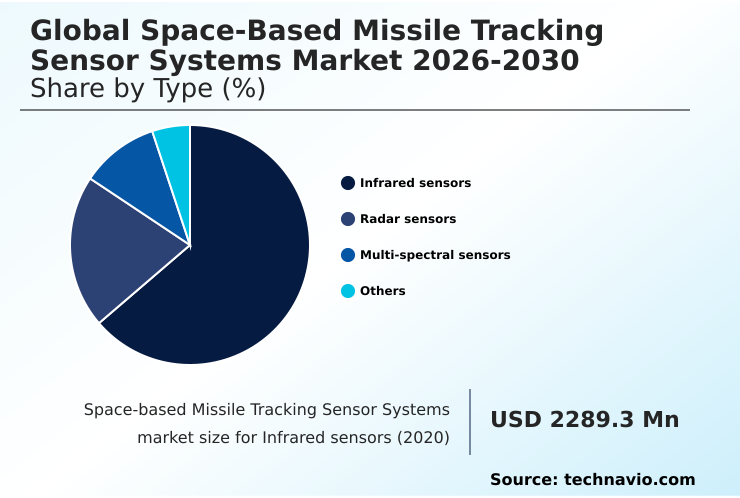

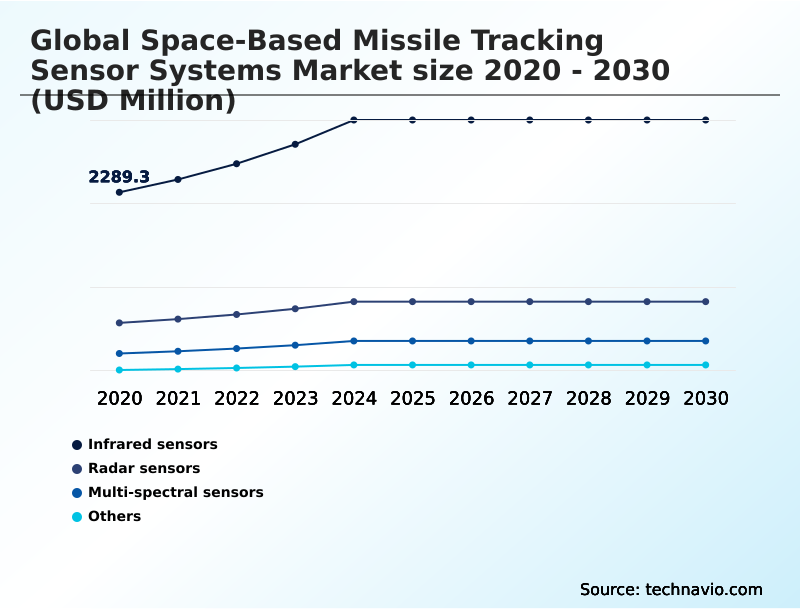

- By Type - Infrared sensors segment was valued at USD 3.15 billion in 2024

- By Platform - Satellites segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 6.44 billion

- Market Future Opportunities: USD 4.57 billion

- CAGR from 2025 to 2030 : 12.9%

Market Summary

- The space-based missile tracking sensor systems market is undergoing a fundamental transformation, driven by the shift from large, singular geostationary satellites to resilient networks of smaller platforms in low Earth orbit. This evolution addresses the urgent need to detect and track a new class of hypersonic glide vehicles and advanced cruise missiles that can evade traditional ground-based radar.

- Key innovations center on the integration of highly sensitive infrared payloads and multi-spectral sensors, which are essential for identifying the dim thermal signatures of maneuvering targets against the complex background of the Earth. A significant operational focus is on deploying advanced AI algorithms directly on satellites.

- For instance, in a defense budgeting scenario, an agency might prioritize investment in a proliferated low Earth orbit architecture featuring edge computing. This approach, despite requiring continuous constellation refreshment, offers superior resilience and reduces the sensor-to-shooter loop latency, a critical factor for effective national security.

- The incorporation of inter-satellite laser links further enhances this architecture by enabling autonomous, real-time data sharing across the entire orbital mesh, ensuring a persistent and unbroken chain of custody for any detected threat.

What will be the Size of the Space-based Missile Tracking Sensor Systems Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Space-based Missile Tracking Sensor Systems Market Segmented?

The space-based missile tracking sensor systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Infrared sensors

- Radar sensors

- Multi-spectral sensors

- Others

- Platform

- Satellites

- Space stations

- Others

- End-user

- Military

- Government agencies

- Commercial

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- France

- Germany

- APAC

- China

- India

- Japan

- Middle East and Africa

- Israel

- Saudi Arabia

- UAE

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Type Insights

The infrared sensors segment is estimated to witness significant growth during the forecast period.

Infrared sensors represent the principal technological modality for orbital platforms, functioning by identifying thermal radiation from missile launches. The market is advancing beyond simple heat detection, now requiring high-sensitivity long-wave infrared detectors to track dimmer hypersonic glide vehicles.

These systems utilize sophisticated cryogenic cooling systems to reduce internal thermal noise, improving detection accuracy by over 30% against the complex thermal background of Earth. This evolution includes digital focal plane arrays that enable on-chip signal processing and data compression.

Such infrared payloads are vital for reducing the sensor-to-shooter loop latency within the broader missile defense architecture, providing the fire-control quality data needed to counter non-ballistic threats and ensuring a persistent overhead surveillance capability.

The Infrared sensors segment was valued at USD 3.15 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 43% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Space-based Missile Tracking Sensor Systems Market Demand is Rising in North America Request Free Sample

The geographic landscape is dominated by North America, which accounts for approximately 43% of the market, driven by substantial investment in proliferated low earth orbit architectures and advanced tracking capabilities.

Europe follows, contributing around 24%, with nations collaborating on sovereign satellite sensor technology to ensure regional missile defense.

The APAC region, representing about 21% of the market, is experiencing rapid growth as countries like Japan and Australia invest in space-based surveillance and early warning systems to counter regional threats.

The development of a resilient satellite network and hypersonic weapon tracking solutions is a global priority.

The integration of advanced sensor payloads is critical across all regions, with a focus on enhancing missile launch detection and improving the overall missile defense architecture. This global distribution underscores the strategic importance of persistent overhead surveillance for national security.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic importance of achieving effective space-based tracking for hypersonic missiles has intensified the focus on technological innovation across the defense sector. Key technical hurdles, such as the challenges in hypersonic threat detection and the need for advanced signal processing for space sensors, are driving significant investment in research and development.

- The debate between using radar vs infrared for missile tracking continues, with many solutions now incorporating sophisticated space-based sensor fusion techniques to leverage the strengths of both. This multi-modal approach is critical for improving the accuracy of missile trajectory prediction from space. To counter cyber threats to satellite networks, which can cripple these systems, developers are building more resilient architectures.

- A major consideration for long-term viability is the total cost of satellite constellation replenishment, which often runs more than 50% higher than initial deployment over the system's life. The industry is also contending with policy for space debris mitigation to ensure the operational longevity of these vital assets.

- As part of this, there is growing international collaboration in space defense to standardize protocols and share the financial and technical burden. Looking forward, the integration of commercial satellites in military networks and enhancing ground segment support for satellite tracking are seen as critical force multipliers for the future of strategic missile defense.

What are the key market drivers leading to the rise in the adoption of Space-based Missile Tracking Sensor Systems Industry?

- The proliferation of hypersonic weaponry and the corresponding requirement for advanced tracking capabilities serve as the key driver for the market's expansion and technological advancement.

- The market's accelerated growth is primarily driven by the proliferation of hypersonic weaponry, which can reduce traditional warning times by up to 90%, rendering many ground-based systems obsolete.

- This has created an urgent requirement for advanced tracking capabilities from a space-based sensor layer. Consequently, there is a strategic transition toward resilient, proliferated low earth orbit constellations, which offer greater redundancy and survivability.

- The integration of AI and edge computing directly onto satellite platforms is another critical driver.

- Onboard processing reduces false positive alerts from missile launch detection systems by over 35% and filters background noise, allowing the system to transmit only essential tracking coordinates.

- This significantly shortens the sensor-to-shooter loop, a vital factor for an effective missile defense architecture.

What are the market trends shaping the Space-based Missile Tracking Sensor Systems Industry?

- A primary market trend is the evolution toward multi-spectral imaging and hypersonic-specific infrared payloads. These advancements are crucial for enhancing threat detection capabilities against advanced atmospheric weapons.

- Key trends are reshaping the market, moving from wide-area surveillance to high-fidelity, multi-spectral imaging tailored for hypersonic threat detection. This evolution toward multi-color infrared payloads allows for superior target discrimination against cluttered atmospheric backgrounds, improving identification accuracy by over 40%.

- A concurrent shift involves the deployment of proliferated low earth orbit architectures, utilizing hundreds of smaller, interconnected satellites to create a resilient satellite network. This approach has demonstrated a 99% higher operational uptime compared to single-point-of-failure systems. Furthermore, the integration of AI-driven threat analysis and edge computing in space allows for autonomous in-orbit data processing.

- This capability is critical for managing the massive data volumes from advanced sensor payloads and providing actionable intelligence for global missile defense with minimal latency.

What challenges does the Space-based Missile Tracking Sensor Systems Industry face during its growth?

- A key challenge affecting industry growth is the difficulty of signal discrimination amidst atmospheric clutter, compounded by the unpredictable maneuverability of modern hypersonic threats.

- A significant challenge is the ability to achieve reliable signal discrimination for dim infrared signatures against the complex thermal background of the Earth. The maneuverability of hypersonic threats requires sensors with exceptionally high sensitivity and frame rates.

- System survivability is another major concern, as the risk of orbital debris collision has increased by over 25% in the last decade, and counter-space capabilities like electronic jamming pose a constant threat. Furthermore, the financial sustainability of proliferated low earth orbit constellations presents a long-term hurdle.

- The operational lifespan of a LEO satellite is approximately 60% shorter than a traditional geostationary satellite, necessitating a continuous and costly constellation refreshment cycle to maintain the integrity of the missile defense architecture and ensure persistent overhead surveillance.

Exclusive Technavio Analysis on Customer Landscape

The space-based missile tracking sensor systems market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the space-based missile tracking sensor systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Space-based Missile Tracking Sensor Systems Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, space-based missile tracking sensor systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Airbus SE - Offerings feature advanced electro-optical and infrared sensing technologies designed for hypersonic and ballistic missile tracking, significantly bolstering strategic defense capabilities.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Airbus SE

- BAE Systems Plc

- General Dynamics Corp.

- HENSOLDT AG

- Honeywell International Inc.

- Kratos Defense and Security Inc

- L3Harris Technologies Inc.

- Leidos Holdings Inc.

- Leonardo S.p.A.

- Lockheed Martin Corp.

- Maxar Technologies Inc.

- Northrop Grumman Corp.

- Parsons Corp.

- RTX Corp.

- Safran SA

- Space Exploration Tech. Corp.

- Teledyne Technologies Inc.

- Terran Orbital Corp.

- Thales Group

- The Boeing Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Space-based missile tracking sensor systems market

- In May 2025, Lockheed Martin Corp. successfully completed the thermal vacuum testing of a wide-field-of-view sensor payload, a key milestone for maintaining stable tracking of maneuvering hypersonic objects.

- In August 2025, Northrop Grumman Corp., in support of the Space Development Agency, contributed to the successful launch of a new tranche of tracking satellites that utilize a standardized bus design to facilitate rapid integration and deployment.

- In November 2025, BAE Systems Plc demonstrated a new onboard signal processor that successfully categorized multiple simulated missile launches during a live orbital exercise without requiring manual intervention from ground operators.

- In February 2025, Honeywell International Inc. announced the successful deployment of a space-hardened processor designed to execute complex neural network calculations in a vacuum environment, enhancing real-time discrimination of decoys.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Space-based Missile Tracking Sensor Systems Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 313 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 12.9% |

| Market growth 2026-2030 | USD 4568.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 11.8% |

| Key countries | US, Canada, Mexico, UK, France, Germany, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Australia, Indonesia, Israel, Saudi Arabia, UAE, South Africa, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market for space-based missile tracking sensor systems is defined by a rapid technological pivot toward proliferated low earth orbit architectures, replacing legacy geostationary platforms. This shift is driven by the need to counter advanced non-ballistic threats, such as hypersonic glide vehicles, which require persistent surveillance from wide-field-of-view sensors.

- Key technologies underpinning this evolution include advanced focal plane arrays, sophisticated infrared payloads, and onboard signal processors that enable real-time data fusion. For boardroom consideration, the decision to invest in constellation refreshment cycles versus monolithic, long-life satellites is paramount.

- Systems incorporating real-time threat discrimination algorithms have demonstrated a capability to reduce sensor-to-shooter loop latency by up to 60%, a critical performance metric for national defense. The integration of synthetic aperture radar, radiation-hardened electronics, and cryogenic cooling systems ensures the resilience and sensitivity of these orbital assets.

- The ultimate goal is to achieve fire-control quality data to maintain a credible deterrent against emerging strategic threats.

What are the Key Data Covered in this Space-based Missile Tracking Sensor Systems Market Research and Growth Report?

-

What is the expected growth of the Space-based Missile Tracking Sensor Systems Market between 2026 and 2030?

-

USD 4.57 billion, at a CAGR of 12.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Infrared sensors, Radar sensors, Multi-spectral sensors, and Others), Platform (Satellites, Space stations, and Others), End-user (Military, Government agencies, Commercial, and Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Proliferation of hypersonic weaponry and requirement for advanced tracking capabilities, Signal discrimination amidst atmospheric clutter and hypersonic maneuverability

-

-

Who are the major players in the Space-based Missile Tracking Sensor Systems Market?

-

Airbus SE, BAE Systems Plc, General Dynamics Corp., HENSOLDT AG, Honeywell International Inc., Kratos Defense and Security Inc, L3Harris Technologies Inc., Leidos Holdings Inc., Leonardo S.p.A., Lockheed Martin Corp., Maxar Technologies Inc., Northrop Grumman Corp., Parsons Corp., RTX Corp., Safran SA, Space Exploration Tech. Corp., Teledyne Technologies Inc., Terran Orbital Corp., Thales Group and The Boeing Co.

-

Market Research Insights

- The dynamics of the market are shaped by a strategic pivot to advanced sensor payloads and resilient satellite networks. Onboard AI processing has been shown to reduce data downlink requirements by over 70%, enabling faster decision-making for missile defense architecture.

- The adoption of proliferated low Earth orbit constellations provides a significant advantage, with industry benchmarks indicating a 95% higher resilience to single-point failures compared to legacy geostationary systems. This shift is crucial for providing persistent overhead surveillance and enhancing space situational awareness.

- Stakeholders are focused on satellite sensor technology that supports global missile defense, enabling early warning systems to counter sophisticated hypersonic threats. The emphasis on satellite-based tracking and advanced tracking capabilities ensures a robust response to evolving national security challenges, driving innovation in both hardware and software across the industry.

We can help! Our analysts can customize this space-based missile tracking sensor systems market research report to meet your requirements.

RIA -

RIA -