Special Purpose Logic IC Market Size 2024-2028

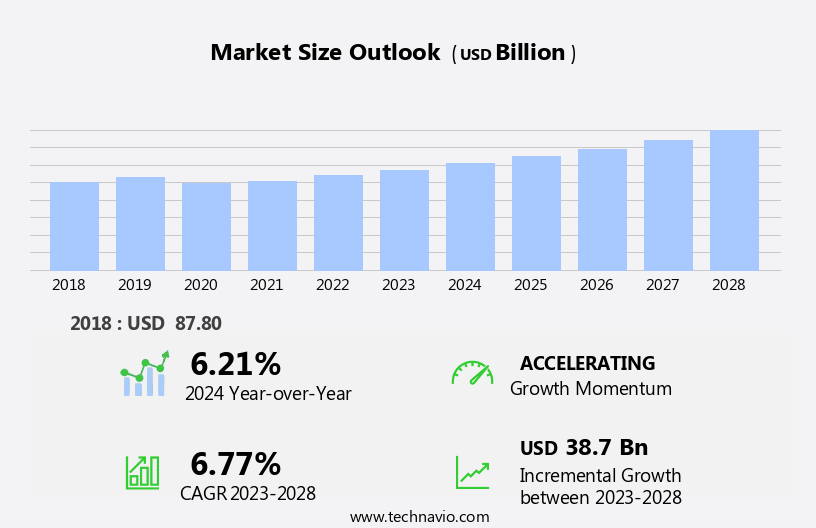

The special purpose logic ic market size is forecast to increase by USD 38.7 billion at a CAGR of 6.77% between 2023 and 2028.

- The market is experiencing significant growth, driven primarily by the high adoption of smartphones and tablets. The miniaturization of electronic devices has led to an increased demand for Special Purpose Logic ICs (SPLICs), which offer improved power efficiency and performance in compact form factors. This trend is expected to continue as the Internet of Things (IoT) and wearable technology markets expand. However, the market also faces challenges, including the increasing complexity of IC designs and the need for higher integration levels. These challenges require significant investments in research and development to ensure the production of advanced SPLICs that can meet the demands of these emerging applications.

- Additionally, the market is subject to price pressures due to intense competition and the need to maintain cost competitiveness. Companies seeking to capitalize on market opportunities must focus on innovation and differentiation to stay ahead of the competition. Adopting advanced design methodologies, such as FinFET and 28nm processes, can help improve product performance and reduce manufacturing costs. Navigating these challenges effectively will require a strategic focus on R&D investments, cost optimization, and a strong understanding of market trends and customer needs.

What will be the Size of the Special Purpose Logic IC Market during the forecast period?

- The market continues to evolve, driven by advancements in process technology and the integration of various technologies. Sequential logic and field-programmable gate arrays (FPGAs) are at the forefront of this evolution, enabling high-performance computing and real-time processing in applications spanning from consumer electronics to aerospace and defense. Performance optimization and electronic design automation (EDA) tools are essential for designing and manufacturing these complex ICs. Cloud computing and high-speed, high-performance computing are catalyzing the market's growth, with data centers and edge computing requiring custom logic solutions. The integration of hardware description language, IP cores, and digital design tools further streamlines the design process.

- Low power and power management are crucial considerations for various sectors, including industrial automation, Internet of Things, and medical devices. The ongoing development of process technology and the emergence of artificial intelligence (AI) and machine learning (ML) are transforming the market landscape. Application-specific integrated circuits (ASICs) and flash memory are becoming increasingly important for AI and ML applications. Intellectual property (IP) protection and design automation tools are essential for managing the intricacies of these complex systems. The market's continuous dynamism underscores the importance of staying abreast of the latest trends and technologies.

How is this Special Purpose Logic IC Industry segmented?

The special purpose logic ic industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Communications

- Computing

- Consumer electronics

- Others

- Type

- Programmable logic ICs

- High end programmable logic ICs

- Others

- Geography

- North America

- US

- APAC

- China

- Singapore

- South Korea

- Taiwan

- Rest of World (ROW)

- North America

By Application Insights

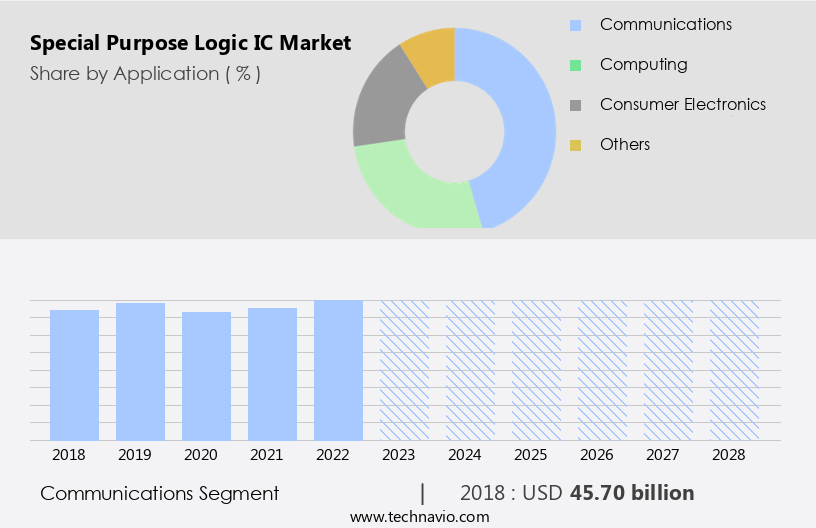

The communications segment is estimated to witness significant growth during the forecast period.

The market is experiencing significant growth, driven by the relentless advancements in Moore's Law and the expanding applications in various industries. In consumer electronics, digital signal processing and combinational logic are essential components, enabling advanced features in smartphones and multimedia devices. The aerospace & defense sector demands custom logic solutions for mission-critical applications, while machine learning and deep learning algorithms in artificial intelligence necessitate high-performance computing and design automation. Industrial automation, internet of things, and edge computing are fueling the demand for low-power, high-speed ICs. The rise of cloud computing and data centers necessitates efficient power management and high-performance computing solutions.

Furthermore, the healthcare sector's increasing reliance on medical devices and intellectual property protection drives the need for application-specific integrated circuits. The telecommunications sector's transition to 5G networks is expected to propel the growth in telecommunication equipment, increasing the demand for special purpose logic ICs. These ICs are crucial for the functioning of enterprise network equipment, wireline network equipment, subscriber equipment, and cable/multiservice operator equipment. Process technology innovations and performance optimization in field-programmable gate arrays continue to be key trends in the market. Electronic design automation and hardware description languages facilitate the design and development of custom logic solutions.

The integration of IP cores and digital design techniques further enhances the market's versatility and adaptability.

The Communications segment was valued at USD 45.70 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

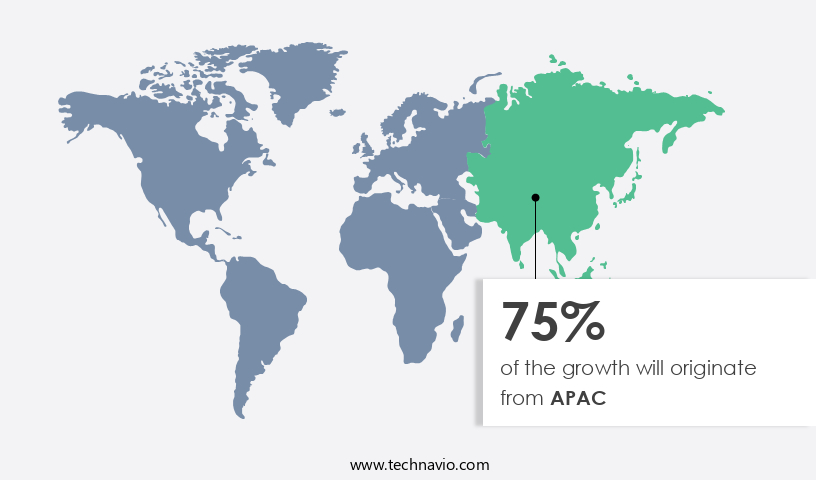

APAC is estimated to contribute 75% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is experiencing significant growth, driven by the advancements in technology and increasing applications across various industries. Moore's Law continues to influence the market, pushing for smaller, faster, and more efficient ICs. Digital signal processing, combinational logic, and sequential logic are key technologies fueling this growth. In the aerospace & defense sector, custom logic and field-programmable gate arrays (FPGAs) are essential for high-performance computing and real-time processing. Machine learning and deep learning are revolutionizing industries, leading to an increased demand for specialized ICs. Process technology advancements enable lower power consumption and improved performance optimization. Electronic design automation (EDA) tools and hardware description languages (HDLs) facilitate digital design and IP core integration.

Cloud computing, high-speed networks, and edge computing are driving the need for specialized ICs in data centers and embedded systems. Industrial automation, the Internet of Things (IoT), and medical devices also rely on specialized ICs for low power consumption and high performance. APAC holds the largest market share due to the presence of numerous electronic device manufacturers and the expansion of telecommunication networks in developing countries like China, Thailand, Malaysia, South Korea, and India. Consumer electronics, particularly mobile devices, are expected to witness remarkable growth due to increasing disposable income and the continuous pursuit of high-performance, low-power ICs.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Special Purpose Logic IC Industry?

- The prevalent trend of smartphone and tablet adoption significantly drives the market growth.

- The market is experiencing significant growth due to the increasing demand for low power and power management solutions in various applications. This trend is particularly noticeable in sectors such as medical devices, data centers, and embedded systems. Intellectual property protection is another key driver, as companies seek to protect their unique technologies and innovations. In the medical device industry, the integration of application-specific integrated circuits (ASICs) and flash memory is enabling the development of more advanced and compact devices. For instance, ASICs are being used to create more efficient power management systems, while flash memory is enabling the storage of large amounts of data.

- In the data center sector, the need for energy efficiency and high performance is driving the adoption of low power ICs. These ICs are being used to optimize power consumption in servers, storage systems, and networking equipment. Moreover, the use of ASICs in embedded systems is enabling the development of more advanced and specialized devices. For example, ASICs are being used in automotive applications to improve fuel efficiency and safety. Overall, the market for Special Purpose Logic ICs is expected to continue growing due to the increasing demand for low power and power management solutions in various applications.

- This trend is likely to be driven by the development of new technologies and the increasing importance of data in various industries.

What are the market trends shaping the Special Purpose Logic IC Industry?

- The shift towards smaller wafer sizes is a significant market trend that is gaining momentum in the semiconductor industry. This trend signifies a move towards increased efficiency and higher production capacity for semiconductor manufacturers.

- The semiconductor industry has experienced significant advancements over the past four decades, with wafer sizes evolving from 100mm to the current prevalent 300mm. This transition, driven by Moore's Law, has resulted in substantial cost savings for semiconductor manufacturers, amounting to at least 20-25%. The industry's focus on 300mm wafers is anticipated to persist throughout the forecast period due to substantial investments in upgrading and constructing new fabrication plants for this size. Despite the widespread adoption of 300mm wafers, the demand for 200mm wafers remains steady. Various consumer electronics, including sensors, microcontrollers, display drivers, and a few MEMS-based products like accelerometers, continue to be manufactured using 200mm wafers.

- Furthermore, the aerospace and defense sector, digital signal processing, combinational logic, machine learning, and deep learning applications also rely on 200mm wafers. This dual demand for both wafer sizes underscores the industry's continuous evolution and the importance of staying abreast of technological advancements.

What challenges does the Special Purpose Logic IC Industry face during its growth?

- The miniaturization of electronic devices poses a significant challenge to the industry's growth, as manufacturers strive to create smaller, more efficient technologies while maintaining high performance and functionality.

- In the ever-evolving world of semiconductor technology, the demand for compact and high-performance Integrated Circuits (ICs) has grown significantly. With the miniaturization of electronic devices, IC manufacturers face the challenge of embedding over 30 different high- and low-voltage circuits and analog functions on a single chip, while keeping manufacturing costs low. This design complexity increases as the size of circuits and chips continues to decrease, necessitating uncompromised performance. To address these challenges, process technology advancements such as FinFET and 7nm have emerged. Sequential logic and field-programmable gate arrays (FPGAs) are increasingly being used for performance optimization in IC design.

- Electronic Design Automation (EDA) tools and cloud computing have become essential for designing high-speed, high-performance computing ICs. The integration of these technologies enables the creation of robust, immersive, and harmonious ICs, meeting the demands of the modern technology landscape. In conclusion, the IC market is undergoing a transformative phase, driven by the need for miniaturization, high performance, and cost-effective manufacturing. The integration of advanced process technologies, sequential logic, FPGAs, EDA tools, and cloud computing is crucial for designing next-generation ICs that cater to the evolving needs of the industry.

Exclusive Customer Landscape

The special purpose logic ic market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the special purpose logic ic market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, special purpose logic ic market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Micro Devices Inc. - The company specializes in providing advanced logic integrated circuit (IC) solutions, including AMD CDNA and Milan X. Our offerings cater to specific applications, enhancing search engine visibility and delivering informed insights from a research analyst's perspective. These innovative IC solutions enable high-performance computing and graphics processing, ensuring alignment with the company's commitment to technological advancement.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Micro Devices Inc.

- Analog Devices Inc.

- Broadcom Inc.

- GOWIN Semiconductor Corp.

- Infineon Technologies AG

- Intel Corp.

- Kingston Technology Co. Inc.

- Microchip Technology Inc.

- NXP Semiconductors NV

- Phoenix Contact GmbH and Co. KG

- Qualcomm Inc.

- Renesas Electronics Corp.

- STMicroelectronics International N.V.

- Texas Instruments Inc.

- Trenz Electronic GmbH

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Special Purpose Logic IC Market

- In February 2024, Intel Corporation announced the launch of its new FPGA-based Special Purpose Logic IC (SPLIC), named Stratix 10 GX FPGA. This product launch marked a significant advancement in the SPLIC market, as Intel's Stratix 10 GX FPGAs offered improved power efficiency and increased logic density compared to previous generations (Intel Press Release, 2024).

- In June 2025, Samsung Electronics and Xilinx, Inc. Entered into a strategic partnership to develop and manufacture custom SPLICs for automotive applications. This collaboration aimed to address the growing demand for advanced driver-assistance systems (ADAS) and autonomous driving technologies (Samsung Newsroom, 2025).

- In August 2025, Synopsys, a leading provider of semiconductor design software, acquired Doulos, a leading provider of formal verification IP for SPLICs. This acquisition was expected to strengthen Synopsys' position in the SPLIC market by expanding its offerings and enhancing its design capabilities (Synopsys Press Release, 2025).

- In December 2025, the European Union introduced new regulations for automotive safety systems, mandating the use of SPLICs in advanced driver-assistance systems (ADAS) and autonomous driving technologies. This regulatory approval marked a significant market opportunity for SPLIC suppliers, as the European automotive market is one of the largest globally (European Commission Press Release, 2025).

Research Analyst Overview

The market is witnessing significant advancements with the integration of various technologies. Heterogeneous computing, a key trend, enables the efficient utilization of resources by combining different processing elements. Reliability testing and performance benchmarking are crucial in ensuring the optimal functioning of these complex systems. Open source hardware and software play a pivotal role in cost optimization and design flexibility. Thermal management and power consumption are critical concerns in the development of high-performance ICs. Data security is another pressing issue, with emerging technologies like quantum computing posing new challenges. Three-dimensional integration, design for testability, and supply chain management are essential for enhancing yield and reducing time-to-market.

Reconfigurable computing, hardware acceleration, and high bandwidth memory are key enablers for real-time processing and system integration. Fault tolerance, parallel processing, and driver development are essential for enhancing functional safety and ensuring industry regulations are met. Neuromorphic computing, bio-inspired computing, and hardware-software co-design are promising areas for innovation. Standards compliance and cost optimization are essential for next-generation semiconductors, which must balance performance and energy efficiency. Emerging technologies like reconfigurable computing and quantum computing require innovative thermal management solutions and design optimization strategies. System integration, power consumption, and design optimization are crucial for the successful implementation of complex IC designs. Industry regulations, such as those related to safety and security, must be carefully considered throughout the life cycle management of these systems.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Special Purpose Logic IC Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

183 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.77% |

|

Market growth 2024-2028 |

USD 38.7 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.21 |

|

Key countries |

China, US, South Korea, Taiwan, and Singapore |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Special Purpose Logic IC Market Research and Growth Report?

- CAGR of the Special Purpose Logic IC industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the special purpose logic ic market growth of industry companies

We can help! Our analysts can customize this special purpose logic ic market research report to meet your requirements.

RIA -

RIA -