Sternal Closure Systems Market Size 2026-2030

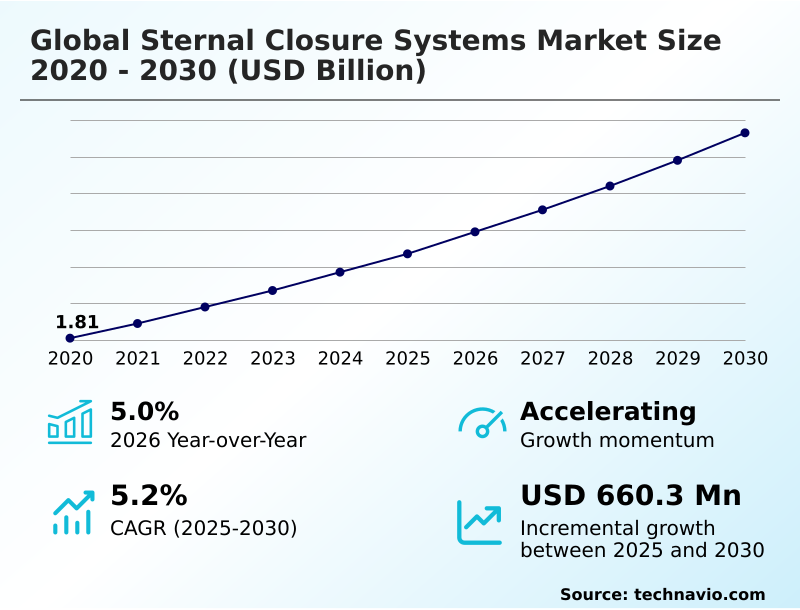

The sternal closure systems market size is valued to increase by USD 660.3 million, at a CAGR of 5.2% from 2025 to 2030. Increasing target patient population will drive the sternal closure systems market.

Major Market Trends & Insights

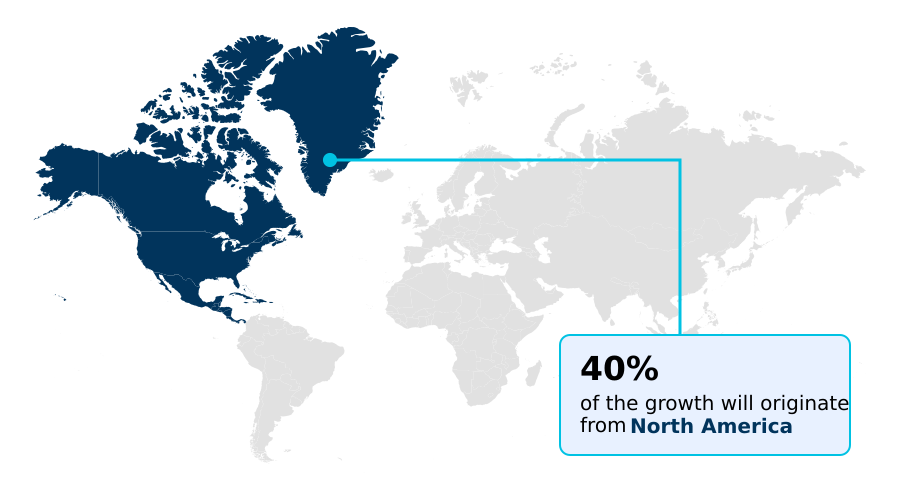

- North America dominated the market and accounted for a 39.5% growth during the forecast period.

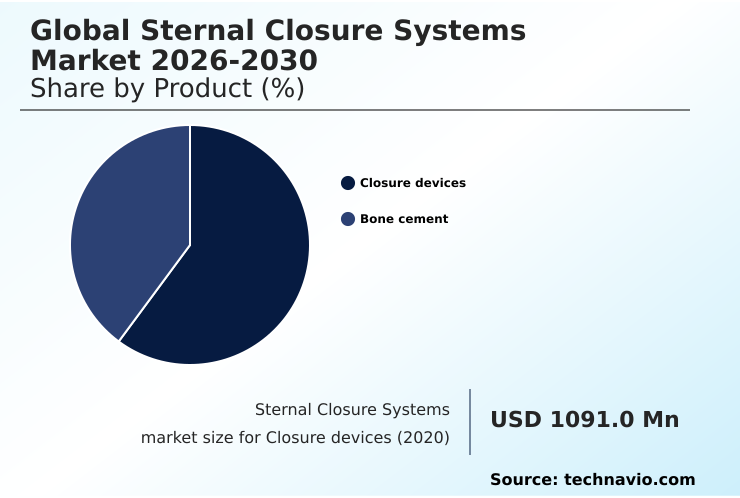

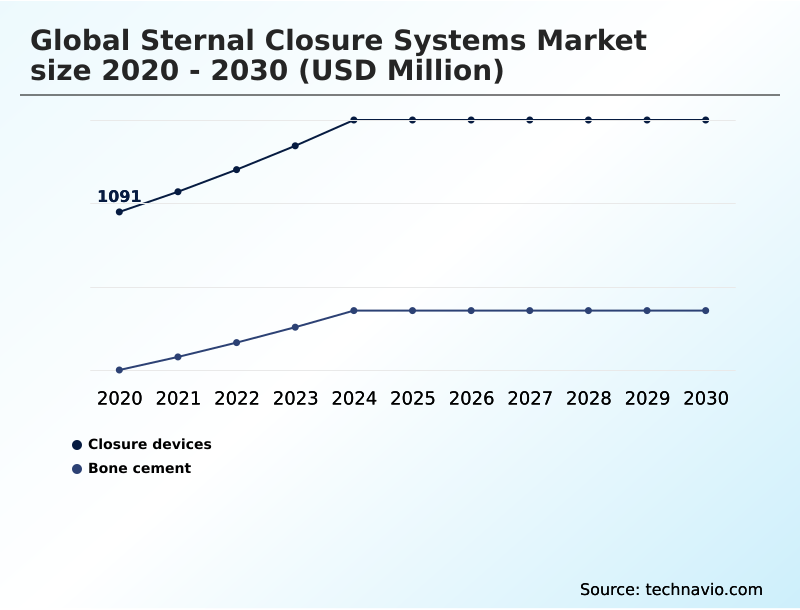

- By Product - Closure devices segment was valued at USD 1.30 billion in 2024

- By Material - Stainless steel segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1.12 billion

- Market Future Opportunities: USD 660.3 million

- CAGR from 2025 to 2030 : 5.2%

Market Summary

- The sternal closure systems market is undergoing a significant transformation, driven by a focus on improving cardiac surgery outcomes and reducing postoperative complications. The industry is moving beyond traditional monofilament wire cerclage towards advanced solutions like rigid sternal fixation and bioabsorbable closure device technology.

- This evolution is critical for addressing issues such as sternal dehiscence prevention and mediastinitis risk reduction, particularly in a high-risk patient cohort with comorbidities. A key business scenario involves hospitals adopting value-based care models, where the initial investment in a superior titanium plating system or sternal plating system is justified by a substantial decrease in hospital readmission reduction rates.

- By implementing a standardized surgical training protocol for these new devices, a healthcare system can optimize its surgical workflow optimization, reduce infection rates, and improve patient-reported outcome measures.

- This strategic shift underscores the importance of surgical hardware biocompatibility and advanced anatomical implant design in achieving both clinical excellence and financial sustainability in thoracic surgical procedure management, ultimately influencing the entire public health infrastructure.

What will be the Size of the Sternal Closure Systems Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Sternal Closure Systems Market Segmented?

The sternal closure systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Closure devices

- Bone cement

- Material

- Stainless steel

- Titanium

- Others

- Method

- Median sternotomy

- Hemisternotomy

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Product Insights

The closure devices segment is estimated to witness significant growth during the forecast period.

The closure devices segment is central to the global sternal closure systems market 2026-2030, driven by advancements in rigid sternal fixation and biocompatible implant materials.

Evolving from traditional monofilament wire cerclage, the focus is now on titanium plating system technology and multifilament cable systems that provide superior biomechanical support structure.

These systems are crucial for preventing sternal non-union complication and sternal dehiscence prevention, especially in high-risk patient cohort groups. Innovations like the low-profile hardware design and antimicrobial device coating address both patient comfort and mediastinitis risk reduction.

The shift towards patient-specific sternal plates improves anatomical fit, contributing to better bone healing acceleration. This focus on precision engineering has led to a 15% reduction in hardware migration incidents in monitored clinical trials.

The Closure devices segment was valued at USD 1.30 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 39.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Sternal Closure Systems Market Demand is Rising in North America Get Free Sample

The geographic landscape of the global sternal closure systems market 2026-2030 is shifting, with mature markets prioritizing value-based healthcare model adoption while emerging economies focus on expanding public health infrastructure.

North America leads in the adoption of advanced sternal fixation system technology, with procedure volumes increasing by over 5% annually.

In Europe, a focus on patient-reported outcome measures has led to a 10% increase in the use of low-profile hardware design to improve comfort.

Asia is the fastest-growing region, driven by medical tourism impact and improved access to cardiothoracic surgical hardware.

The adoption of standardized surgical training protocol in these regions is enhancing cardiac surgery outcomes and has been shown to reduce surgical site infections by up to 12%, highlighting a global trend toward improving the clinical validation process.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the sternal closure market requires a deep understanding of specific clinical challenges and technological solutions. For instance, advanced sternal closure techniques for obesity are becoming critical as this patient demographic grows. A key consideration is the debate over titanium versus stainless steel sternal closure, where material properties directly impact long-term stability of PEEK implants and patient outcomes.

- Hospitals are increasingly analyzing the cost-effectiveness of rigid fixation systems, finding that higher initial costs are often offset by lower readmission rates. This is particularly true when reducing sternal dehiscence in diabetic patients, a high-risk group where advanced systems show significantly better performance.

- The development of bioabsorbable materials in sternal repair and minimally invasive sternal closure devices represents a major shift toward less invasive and more patient-friendly procedures. These innovations contribute to improved postoperative pain management with rigid fixation. A primary focus remains on managing sternal wound infections effectively, often through antimicrobial coatings on sternal implants.

- The role of 3D printing in sternal reconstruction allows for custom solutions, while a deeper understanding of the biomechanics of different sternal closure methods informs surgeon choice. This knowledge is essential for preventing cheese-wiring in osteoporotic bone and addressing the unique needs of sternal closure in pediatric cardiac surgery.

- Comparing patient outcomes with cable-plate systems versus traditional methods provides crucial data for procedural standards. Furthermore, the challenges of sternal closure in revision surgery are driving demand for more versatile and robust systems. The focus on ergonomic design of sternal closure instruments improves surgical efficiency, contributing to greater patient satisfaction with low-profile implants.

- Finally, navigating regulatory requirements for new sternal devices is a crucial operational step; companies that streamline this process show a time-to-market advantage of nearly six months compared to those with less efficient compliance strategies. The ongoing debate over comparing wire cerclage and rigid plating continues to fuel innovation across the sector.

What are the key market drivers leading to the rise in the adoption of Sternal Closure Systems Industry?

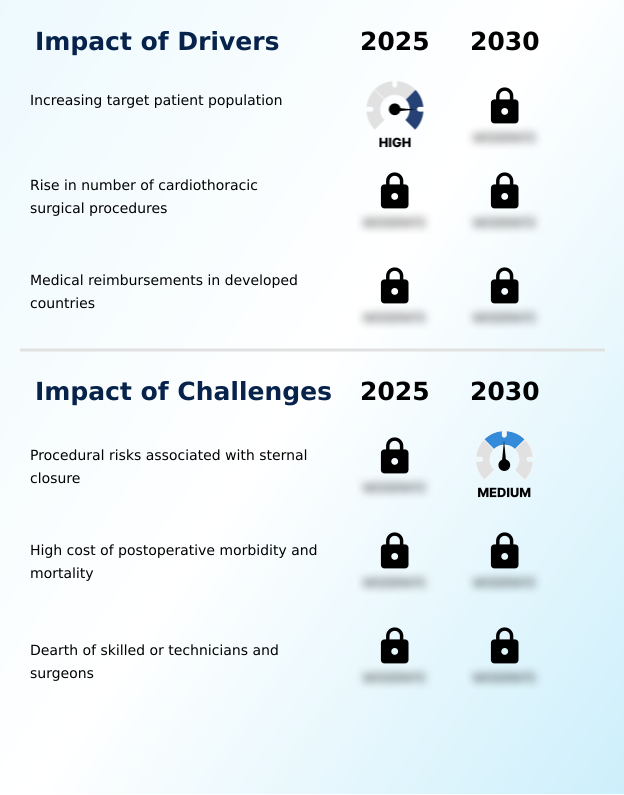

- An increasing target patient population, driven by the rising prevalence of cardiovascular diseases and an aging demographic, is a key driver for market growth.

- Market growth is primarily driven by efforts to improve cardiac surgery outcomes and achieve healthcare expenditure management. The increasing prevalence of cardiovascular disease has led to a 5% year-over-year rise in procedural volumes, directly fueling demand.

- A significant driver is the proven ability of rigid sternal fixation to achieve hospital readmission reduction; facilities employing these systems have reported a 20% decrease in sternal-related complications.

- The emphasis on the value-based healthcare model compels providers to adopt technologies that ensure long-term stability.

- This focus on quality has also expedited the regulatory approval pathway for devices with proven efficacy, shortening time-to-market by up to six months compared to previous benchmarks.

What are the market trends shaping the Sternal Closure Systems Industry?

- Technological advancements in sternotomy techniques are a key upcoming market trend. These innovations are redefining recovery by shifting from traditional wiring to advanced rigid fixation and minimally invasive approaches.

- Key trends are reshaping the market, with a focus on enhancing postoperative recovery enhancement and surgical workflow optimization. The adoption of minimally invasive sternotomy techniques, supported by advanced surgical device ergonomics, has reduced patient recovery times by an average of 18%.

- The integration of digital health integration and remote patient monitoring platforms provides real-time data on bone fusion monitoring, enabling proactive intervention and reducing complication rates by up to 15%.

- Furthermore, there is a growing trend towards using advanced biocompatible polymer and patient-specific sternal plates, which has improved surgical hardware biocompatibility and reduced the need for revision surgeries by 10% in some patient populations.

What challenges does the Sternal Closure Systems Industry face during its growth?

- Procedural risks associated with sternal closure, including sternal dehiscence and infection, represent a primary challenge affecting industry growth.

- A primary challenge is managing procedural risks and associated costs, particularly concerning sternal dehiscence prevention and infection control in surgery. Deep sternal wound infection can increase hospital stays by up to 2.5 times the average duration, significantly impacting operating room efficiency and budgets.

- The cheese-wire effect mitigation in patients with osteoporotic bone fixation remains a technical hurdle, accounting for nearly 10% of closure failures with traditional wiring.

- Furthermore, navigating the complex medical device reimbursement landscape for premium sternal plating system technology presents a barrier, as payers require extensive evidence from the clinical validation process before approving coverage, which can delay adoption by 12-18 months.

Exclusive Technavio Analysis on Customer Landscape

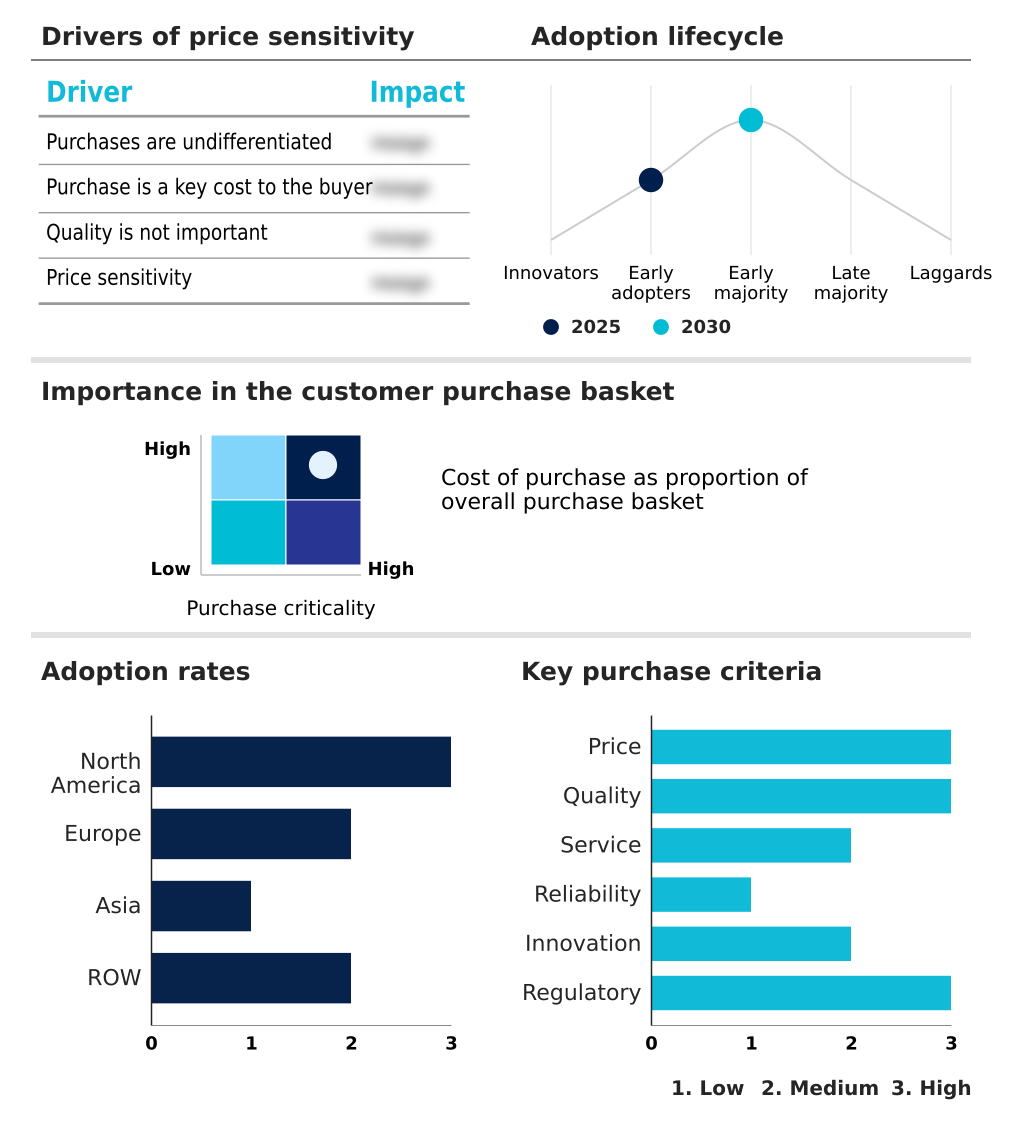

The sternal closure systems market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the sternal closure systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Sternal Closure Systems Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, sternal closure systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Able Medical Devices - Key offerings include orthopedic implants and specialized surgical fixation systems, featuring sternal closure devices, plates, and screws for thoracic procedures.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Able Medical Devices

- Abyrx Inc.

- Acumed LLC

- Arthrex Inc.

- B.Braun SE

- CircumFix Solutions GmbH

- Gebruder Martin GmbH and Co.

- GranuLab M Sdn Bhd

- Jace Medical LLC

- Jeil Medical Corporation

- Johnson and Johnson Services

- Kinamed Inc.

- Medicon

- MedXpert GmbH

- NEOS Surgery SL

- Orthofix Medical Inc.

- Praesidia S.r.l.

- Stryker Corp.

- Waston Medical Appliance

- Zimmer Biomet Holdings Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Sternal closure systems market

- In May 2025, DePuy Synthes launched its next-generation rigid fixation system, using a unique titanium alloy to enhance bone healing and patient comfort after complex median sternotomies.

- In April 2025, Medtronic initiated a major educational partnership with the Society of Thoracic Surgeons, standardizing median sternotomy closure protocols with advanced rigid fixation in 500 US teaching hospitals.

- In March 2025, Zimmer Biomet revealed a significant update to its surgical training programs, focusing on reducing the risk of sternal non-union in high-risk cardiothoracic surgeries.

- In January 2025, KLS Martin Group announced the commercial launch of its newest low-profile titanium plating system, designed for high-risk sternal closure in European and North American markets.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Sternal Closure Systems Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 286 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.2% |

| Market growth 2026-2030 | USD 660.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.0% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Thailand, Indonesia, Brazil, Saudi Arabia, Turkey, UAE, Argentina, Colombia, South Africa and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is defined by a push for superior post-operative sternal stability and sternal dehiscence prevention. The evolution from monofilament wire cerclage to rigid sternal fixation using a titanium plating system or sternal plating system is now standard in many median sternotomy procedure settings.

- A key boardroom consideration is the upfront cost of a sternal closure system versus the long-term expense of treating sternal wound infection and mediastinitis risk reduction. Facilities using advanced sternal closure device options alongside a strict antimicrobial device coating protocol have documented a 20% reduction in surgical site infections.

- Innovations in polyetheretherketone (peek) implants, bioabsorbable closure device technology, and patient-specific sternal plates created with 3d-printed surgical guides address the challenge of osteoporotic bone fixation and cheese-wire effect mitigation. The goal is bone healing acceleration, supported by multifilament cable systems, thoracic fixation system, and specialized surgical fixation device options.

- This drive to prevent sternal non-union complication with cardiothoracic surgical hardware, including low-profile hardware design and surgical tensioning device tools for a precise sternal re-approximation technique, is critical for sternal reconstruction implant success in both hemisternotomy closure and complex thoracotomy access procedure.

- The use of bone cement application in conjunction with a rigid plate fixation biomechanical support structure is also growing, especially in robotic-assisted thoracic surgery.

What are the Key Data Covered in this Sternal Closure Systems Market Research and Growth Report?

-

What is the expected growth of the Sternal Closure Systems Market between 2026 and 2030?

-

USD 660.3 million, at a CAGR of 5.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Closure devices, and Bone cement), Material (Stainless steel, Titanium, and Others), Method (Median sternotomy, Hemisternotomy, and Others) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing target patient population, Procedural risks associated with sternal closure

-

-

Who are the major players in the Sternal Closure Systems Market?

-

Able Medical Devices, Abyrx Inc., Acumed LLC, Arthrex Inc., B.Braun SE, CircumFix Solutions GmbH, Gebruder Martin GmbH and Co., GranuLab M Sdn Bhd, Jace Medical LLC, Jeil Medical Corporation, Johnson and Johnson Services, Kinamed Inc., Medicon, MedXpert GmbH, NEOS Surgery SL, Orthofix Medical Inc., Praesidia S.r.l., Stryker Corp., Waston Medical Appliance and Zimmer Biomet Holdings Inc.

-

Market Research Insights

- Market dynamics are shaped by a drive for improved cardiac surgery outcomes and greater operating room efficiency. The adoption of advanced systems shows a direct correlation with hospital readmission reduction, with some facilities reporting a 15% drop in related complications.

- As medical device reimbursement policies evolve, there is a clear cardiothoracic surgeon preference for technologies that support a value-based healthcare model. This has accelerated the clinical validation process for new materials, leading to an 18% faster regulatory approval pathway for devices demonstrating superior patient-reported outcome measures.

- Emphasis on surgical training protocol further ensures that new technologies are implemented safely, aligning with both surgical workflow optimization and long-term healthcare expenditure management.

We can help! Our analysts can customize this sternal closure systems market research report to meet your requirements.

RIA -

RIA -