Pain Management Devices Market Size 2024-2028

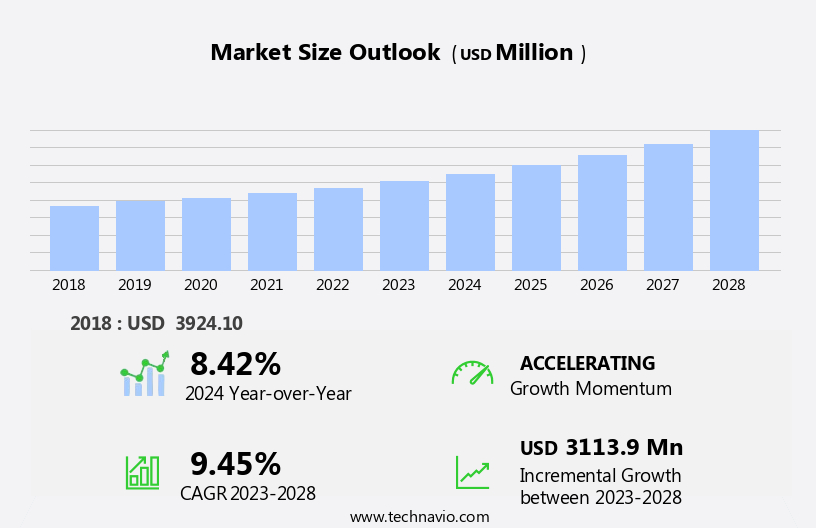

The pain management devices market size is forecast to increase by USD 3.11 billion, at a CAGR of 9.45% between 2023 and 2028. The market is witnessing significant growth, driven by the increasing prevalence of chronic diseases among the geriatric population.

Major Market Trends & Insights

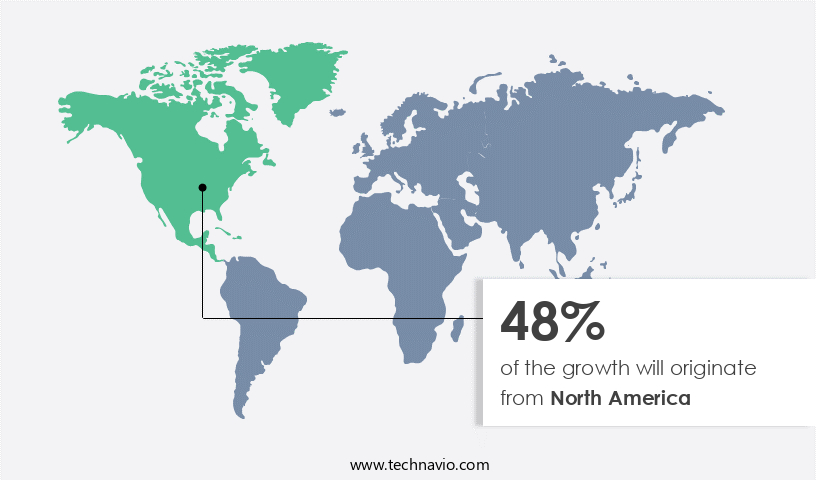

- North America dominated the market and accounted for a 48% share in 2022.

- The market is expected to grow significantly in Asia region as well over the forecast period.

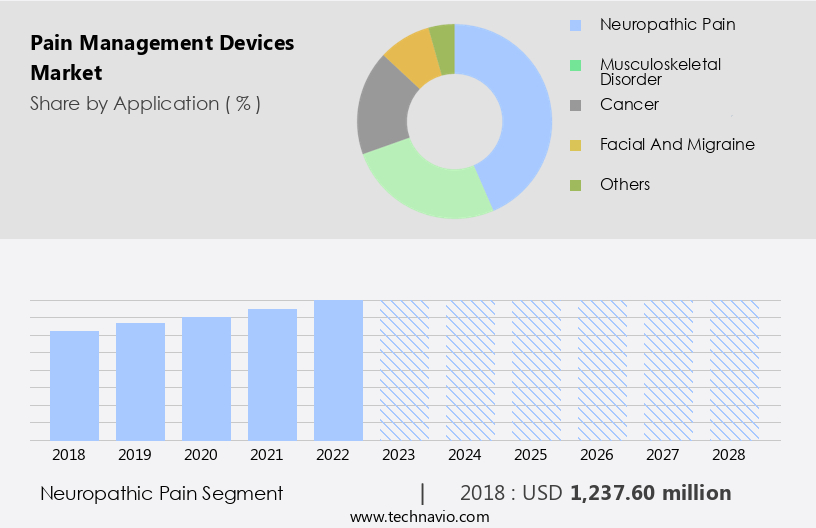

- Based on the Application, the neuropathic pain segment led the market and was valued at USD 1.58 billion of the global revenue in 2022.

- Based on the Product, the neurostimulation devices segment accounted for the largest market revenue share in 2022.

Market Size & Forecast

- 2024 Market Size: USD 5.91 Billion

- Future Opportunities: USD 3.11 Billion

- CAGR (2023-2028): 9.45%

- North America: Largest market in 2022

The market continues to evolve, driven by advancements in technology and the growing prevalence of chronic pain conditions. Neuropathic and nociceptive pain, inflammatory and acute, necessitate a multifaceted approach to effective management. Pain monitoring systems enable real-time assessment, while medication adherence tools ensure patients take prescribed medications as directed. Pain clinics and rehabilitation centers offer comprehensive care, integrating various modalities such as neuromodulation devices, radiofrequency ablation, and epidural steroid injections. These interventions, along with surgical options and laser therapy, offer relief for those suffering from chronic pain. Non-opioid analgesics, topical agents, and adjunctive therapies like ultrasound and occupational therapy, play crucial roles in managing pain.

What will be the Size of the Pain Management Devices Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

Implantable pain pumps and drug delivery systems provide long-term relief, while patient education and physical therapy empower individuals to manage their pain effectively. The ongoing unfolding of market activities reveals a dynamic landscape, with new technologies and applications continually emerging. Pain assessment scales and nerve blocks offer valuable insights into pain severity and potential treatment options, further enhancing the ability to provide effective pain management solutions. The musculoskeletal disorder segment is the second largest segment of the application and was valued at USD 1.27 billion in 2022.

With an aging demographic, the demand for effective pain management solutions is on the rise. Furthermore, technological advances in ablation devices are revolutionizing pain treatment, offering minimally invasive and precise solutions. However, the market faces challenges, including the high cost of neurostimulation devices and procedures, which may limit accessibility for some patients.

Companies in this market must navigate these challenges by exploring cost-effective solutions and collaborating with healthcare providers to offer affordable financing options. By focusing on innovation and accessibility, players can capitalize on the growing demand for pain management devices and meet the needs of an aging population.

How is this Pain Management Devices Industry segmented?

The pain management devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Neuropathic pain

- Musculoskeletal disorder

- Cancer

- Facial and migraine

- Others

- Product

- Neurostimulation devices

- Infusion pumps

- Ablation devices

- Product Type

- Chronic Pain

- Post-Surgical Pain

- Cancer Pain

- Neuropathic Pain

- End-User

- Hospitals

- Clinics

- Home Care

- Technology

- Wearable Devices

- Implantable Devices

- Non-Invasive Devices

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- UAE

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

The neuropathic pain segment is estimated to witness significant growth during the forecast period. The segment was valued at USD 1.58 billion in 2022. It continued to the largest segment at a CAGR of 6.37%.

The market is witnessing significant growth due to the increasing prevalence of chronic pain conditions, particularly neuropathic pain. Neuropathic pain, characterized by damaged or dysfunctional nerve fibers sending incorrect signals to pain centers, affects a large and growing population, especially those with diabetes or prediabetes management. Topical analgesics, implantable pain pumps, neuromodulation devices, and non-opioid analgesics are among the solutions employed in managing this complex, chronic condition. Technological advancements have led to innovations in pain monitoring systems, medication adherence tools, and multimodal pain management approaches. Other interventions, such as ultrasound therapy, facet joint injections, radiofrequency ablation, epidural steroid injections, surgical interventions, laser therapy, opioid analgesics, nerve blocks, and adjunctive therapies, are also utilized in pain clinics and rehabilitation centers.

Patient education, physical therapy, and occupational therapy play crucial roles in managing pain effectively. Inflammatory pain and acute pain management also require specialized attention. Home healthcare and drug delivery systems, including peripheral nerve stimulation and trigger point injections, further expand the market landscape.

The Neuropathic pain segment was valued at USD 1.24 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 48% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the market, North America holds the largest share due to the rising prevalence of chronic conditions like diabetes, cancer, and arthritis. Data suggests that the future opportunities for growth in the North America region estimates to be around USD 3.11 billion. The region's large geriatric population, increasing healthcare expenditure, and technological advancements driving innovative devices are significant growth factors. Patients' growing awareness of pain management options, approvals of new products, and the presence of both global and local manufacturers contribute to market expansion. Chronic pain conditions, such as neuropathic and inflammatory pain, are treated through various methods, including topical analgesics, implantable pain pumps, neuromodulation devices, non-opioid analgesics, ultrasound therapy, facet joint injections, pain monitoring systems, medication adherence, and multimodal pain management.

Acute pain management methods, such as nerve blocks, surgical interventions, epidural steroid injections, radiofrequency ablation, laser therapy, opioid analgesics, occupational therapy, rehabilitation centers, home healthcare, peripheral nerve stimulation, drug delivery systems, trigger point injections, patient education, physical therapy, and nociceptive pain treatments, are also employed. Adjunctive therapies, including pain assessment scales, medication adherence tools, and patient education programs, enhance the effectiveness of pain management strategies. The market's growth is further fueled by the increasing demand for minimally invasive procedures, the integration of digital health technologies, and the rising focus on personalized pain management solutions.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The global pain management devices market size and forecast projects growth, driven by pain management devices market trends 2024-2028. B2B pain device solutions leverage advanced pain relief technologies for efficacy. Pain management devices market growth opportunities 2025 include devices for chronic pain and portable pain relief devices, meeting patient needs. Pain device management software optimizes operations, while pain management devices market competitive analysis highlights key manufacturers. Sustainable pain device practices align with eco-friendly medical trends. Pain management devices regulations 2024-2028 shapes pain device demand in North America 2025. Non-invasive pain solutions and premium pain device insights boost adoption. Pain devices for home use and customized pain relief devices target niches. Pain management devices market challenges and solutions address cost, with direct procurement strategies for pain devices and pain device pricing optimization enhancing profitability. Data-driven pain device analytics and smart pain relief trends drive innovation.

What are the key market drivers leading to the rise in the adoption of Pain Management Devices Industry?

- The prevalence of chronic diseases among the geriatric population serves as the primary driver for market growth in this sector.

- Chronic diseases, including neuropathic pain, are on the rise among the aging population in the US, with approximately 15% of adults reporting multiple chronic medical conditions in 2021, compared to around 11% of older millennials. Sedentary lifestyles and changing eating habits contribute to the prevalence of chronic diseases such as heart disease, stroke, cancer, arthritis, and chronic pain, including low back pain and knee pain. According to the Centers for Disease Control and Prevention (CDC) and the National Center for Health Statistics (NCHS), most people with chronic pain experience pain in various body parts.

- To manage chronic pain effectively, various pain management devices have gained popularity. These include topical analgesics, non-opioid analgesics, implantable pain pumps, neuromodulation devices, and ultrasound therapy. Facet joint injections are also used for pain management. Neuropathic pain, in particular, can be challenging to manage, and these devices offer effective, non-opioid alternatives for chronic pain management.

What are the market trends shaping the Pain Management Devices Industry?

- The trend in the medical field is leaning towards technological advancements in ablation devices. These innovations are mandated to shape the upcoming market.

- Pain management is a critical aspect of healthcare, and the market for pain management devices is witnessing significant advancements. One of the key trends in this market is the development of pain monitoring systems to improve medication adherence and pain assessment. These systems enable healthcare providers to assess pain levels accurately and adjust treatment plans accordingly. Another area of focus is the use of minimally invasive procedures such as radiofrequency ablation and epidural steroid injections. These interventions offer patients an alternative to surgical procedures and have shown promising results in managing chronic pain. For instance, radiofrequency ablation involves the use of heat or cold to destroy a small area of nerve tissue, preventing the transmission of pain signals.

- Technological advances in these procedures have led to improved outcomes and increased patient satisfaction. companies in the market are investing heavily in research and development to create technologically advanced pain management devices. For example, Medtronic's Cool-tip radiofrequency ablation system E series offers high energy and creates large ablation target zones in a short period of time. Laser therapy is another area of interest in the market. This non-invasive therapy uses light energy to stimulate healing and reduce pain. It is often used to treat conditions such as arthritis and muscle strains. In summary, the market is witnessing significant growth due to the increasing prevalence of chronic pain conditions and the development of advanced technologies to manage them.

What challenges does the Pain Management Devices Industry face during its growth?

- The high cost of neurostimulation devices and procedures poses a significant challenge to the industry's growth, as both the acquisition of technology and implementation of treatments can be financially prohibitive for many patients and healthcare providers.

- Pain management devices, including opioid analgesics, nerve blocks, and adjunctive therapies, play a crucial role in managing various types of pain, such as acute and inflammatory pain. However, the high cost of advanced pain management devices, like neurostimulation systems, poses a significant barrier to their adoption in some developing countries. For instance, the initial implantation of pulse generators for neurostimulation can cost over USD20,000, while deep brain stimulation surgeries in the US can range from USD65,000 to USD100,000. Additionally, end-users bear additional costs for post-operative device adjustments, battery replacements, and maintenance.

- These expenses can limit the accessibility of these advanced pain management solutions, particularly in resource-limited settings. In rehabilitation centers and home healthcare, less expensive alternatives, such as occupational therapy and physical therapy, are often used for pain management.

Exclusive Customer Landscape

The pain management devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the pain management devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, pain management devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - The company specializes in advanced pain management solutions, including the Proclaim SCS system, which utilizes spinal cord stimulation technology to effectively manage chronic pain for patients. This non-invasive device delivers targeted electrical pulses to the spinal cord, providing relief and improving overall quality of life. The technology is backed by extensive clinical research and has been proven effective in managing various types of pain.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- AtriCure Inc.

- Avanos Medical Inc.

- B.Braun SE

- Baxter International Inc.

- Becton Dickinson and Co.

- Boston Scientific Corp.

- DJO Global Inc.

- ICU Medical Inc.

- InfuTronix

- Johnson and Johnson Services Inc.

- Kimberly Clark Corp.

- Medtronic Plc

- Micrel Medical Devices SA

- Moog Inc.

- Nevro Corp.

- OMRON Corp.

- Pfizer Inc.

- Stryker Corp.

- Theragen Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Pain Management Devices Market

- In January 2024, Medtronic, a leading medical technology company, announced the FDA approval of its new neurostimulation system, Infuse Therapy, for the management of chronic pain (Medtronic Press Release, 2024). This innovative device uses electrical impulses to block pain signals from the brain, providing an alternative to opioid-based treatments.

- In March 2024, Abbott Laboratories and Neuromod Devices, a neurostimulation technology company, entered into a strategic partnership to develop and commercialize a novel pain management system. The collaboration combines Abbott's expertise in medical devices and Neuromod's proprietary technology, aiming to improve patient outcomes and expand their market presence (Abbott Laboratories Press Release, 2024).

- In July 2024, Boston Scientific Corporation completed the acquisition of Prevail Medical, a company specializing in minimally invasive spinal cord stimulation systems. This acquisition strengthened Boston Scientific's pain management portfolio and expanded its presence in the growing neuromodulation market (Boston Scientific Corporation Press Release, 2024).

- In May 2025, the European Commission granted marketing authorization for Stryker's new spinal cord stimulation system, Opus SCS. This approval marks the first major regulatory milestone for the system, paving the way for its commercialization in Europe and expanding Stryker's pain management offerings (Stryker Press Release, 2025).

Research Analyst Overview

- The market encompasses a range of technologies, including implantable pulse generators and lead wires, aimed at providing relief for patients undergoing implantation procedures. Healthcare providers require extensive training to ensure proper device implantation and programming, while safety and efficacy studies continue to address concerns regarding drug interactions and long-term effects. Implantable batteries and genetic testing contribute to improved patient outcomes and personalized medicine. Clinical trials and regulatory approvals are essential for bringing new devices to market, with cost-effectiveness analysis and healthcare economics playing a significant role in market dynamics.

- Remote monitoring, machine learning, and data analytics facilitate post-market surveillance, enhancing patient compliance and device longevity. Despite advancements, safety concerns persist, with adverse events and side effects requiring ongoing attention from manufacturers and regulators.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Pain Management Devices Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

172 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 9.45% |

|

Market growth 2024-2028 |

USD 3113.9 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

8.42 |

|

Key countries |

US, China, India, Germany, Japan, UK, South Korea, Canada, Brazil, France, UAE, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Pain Management Devices Market Research and Growth Report?

- CAGR of the Pain Management Devices industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Asia, Europe, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the pain management devices market growth of industry companies

We can help! Our analysts can customize this pain management devices market research report to meet your requirements.

RIA -

RIA -