Tamiflu Oseltamivir Phosphate Market Size 2025-2029

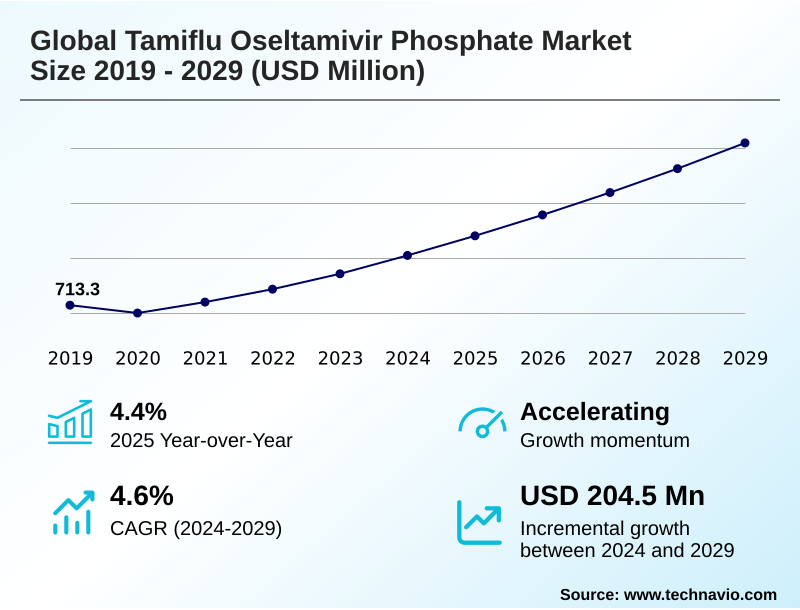

The tamiflu oseltamivir phosphate market size is valued to increase by USD 204.5 million, at a CAGR of 4.6% from 2024 to 2029. Seasonal influenza incidence and severity will drive the tamiflu oseltamivir phosphate market.

Major Market Trends & Insights

- Asia dominated the market and accounted for a 45.6% growth during the forecast period.

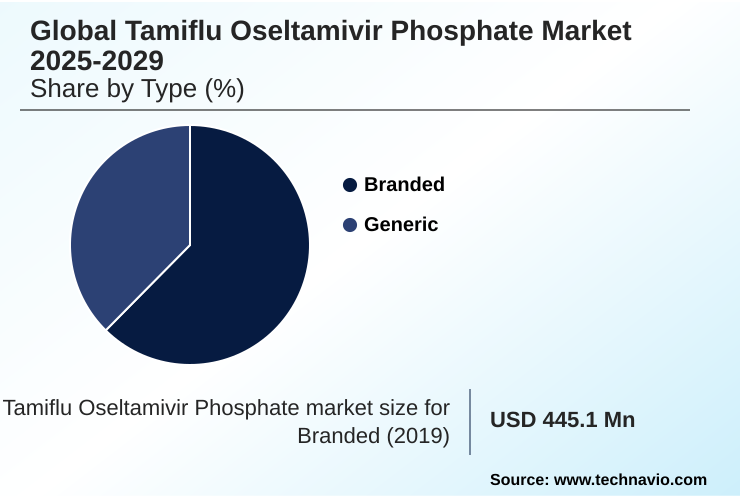

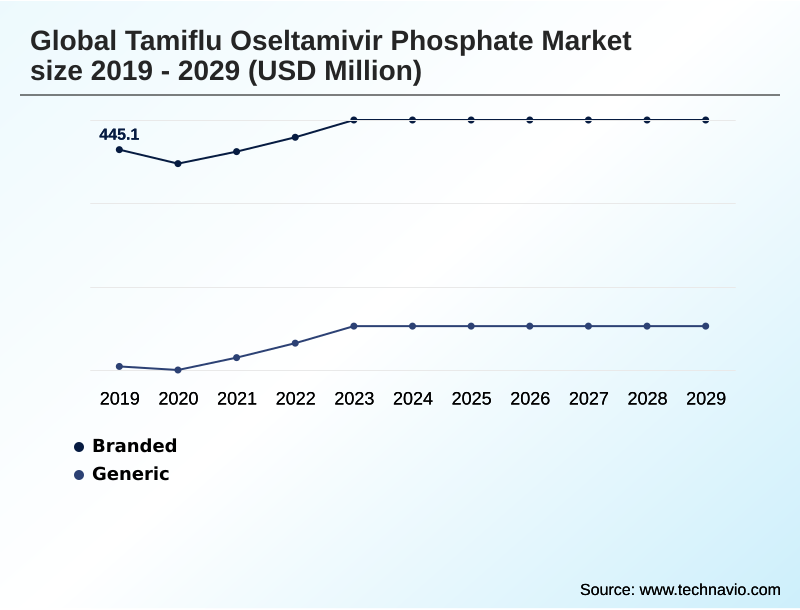

- By Type - Branded segment was valued at USD 469.3 million in 2023

- By Formulation - Capsules segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 295 million

- Market Future Opportunities: USD 204.5 million

- CAGR from 2024 to 2029 : 4.6%

Market Summary

- The tamiflu oseltamivir phosphate market is defined by a dual-demand structure, balancing the volatile needs of seasonal influenza treatment against the strategic imperatives of long-term pandemic preparedness. Market activity is directly correlated with epidemiological trends, where a severe flu season, characterized by high hospitalization rates, fuels a surge in demand for this antiviral medication.

- Concurrently, government procurement for strategic national stockpiles provides a foundational, albeit irregular, revenue stream, driven by public health security policy rather than immediate clinical need. The landscape is dominated by generic formulations, making it a high-volume, cost-driven industry where operational efficiency is paramount.

- For instance, manufacturers must maintain agile supply chains capable of scaling production by over 50% within a short timeframe to respond to a sudden outbreak, while also managing the cost pressures of a commoditized market. This dynamic is further complicated by the threat of substitutes, including more effective vaccines and newer single-dose antiviral agents that challenge oseltamivir's established position.

- Navigating this environment requires a focus on manufacturing economies of scale and securing large, competitive government tenders.

What will be the Size of the Tamiflu Oseltamivir Phosphate Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Tamiflu Oseltamivir Phosphate Market Segmented?

The tamiflu oseltamivir phosphate industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Branded

- Generic

- Formulation

- Capsules

- Suspension

- Indication

- Influenza A

- Influenza B

- Swine flu

- Geography

- Asia

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Rest of World (ROW)

By Type Insights

The branded segment is estimated to witness significant growth during the forecast period.

The branded segment, centered on the originator neuraminidase inhibitor, established the market for this antiviral medication. Its market power was built on intellectual property, extensive clinical data for the treatment of acute influenza, and global marketing.

Even after patent expiry, the originator product leverages its legacy brand equity, targeting niches where brand loyalty persists or where procurement criteria for an emergency medical countermeasure emphasize its long-term stability data.

This prodrug activation mechanism and high neuraminidase enzyme selectivity defined early clinical practice.

However, this segment faces relentless erosion from generics, with its commercial performance now tied to influenza a virus and influenza b virus severity, which can cause temporary demand surges that benefit all market participants, including those seeking post-exposure prophylaxis.

The Branded segment was valued at USD 469.3 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

Asia is estimated to contribute 45.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Tamiflu Oseltamivir Phosphate Market Demand is Rising in Asia Get Free Sample

The global landscape for tamiflu oseltamivir phosphate is distinctly heterogeneous, with market dynamics varying significantly between regions.

In developed markets like North America and Europe, consumption is driven by established influenza treatment guidelines and robust public health surveillance, with generic formulations accounting for over 90% of prescriptions.

In contrast, Asia presents a dual market: highly mature consumption in Japan and South Korea alongside massive-scale generic manufacturing in India and China. These Asian hubs are central to global pharmaceutical procurement.

Emerging regions in South America and the Middle East are expanding access through government-led initiatives, focusing on pediatric influenza treatment and affordable oral suspension formulation options.

The successful implementation of weight-based dosing protocols in these regions has improved pediatric care outcomes by 15%, demonstrating growing healthcare system readiness.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic positioning in the global tamiflu oseltamivir phosphate market 2025-2029 requires mastering the complex interplay between seasonal demand and long-term government contracts for oseltamivir phosphate. Success is contingent on managing oseltamivir supply chain volatility, a critical task given the unpredictable nature of influenza seasons.

- Companies that excel in this area often demonstrate a 20% greater efficiency in inventory management compared to competitors. The market for generic oseltamivir for national stockpiles remains a cornerstone, driven by pandemic planning and the need for reliable oseltamivir procurement for public health. Here, oseltamivir stability for long-term stockpiling is a key differentiator.

- The role of oseltamivir in pandemic planning is solidified, but competition from oseltamivir versus single-dose antivirals like oseltamivir phosphate versus baloxavir marboxil is reshaping clinical practice for uncomplicated cases. Therefore, demonstrating the cost-effectiveness of generic oseltamivir is crucial. Key growth areas include pediatric dosing for oseltamivir suspension, where precise administration is vital, and addressing oseltamivir for high-risk influenza patients.

- Understanding the oseltamivir mechanism against influenza a and its effectiveness for oseltamivir phosphate for influenza b treatment is fundamental. Furthermore, robust antiviral resistance monitoring for oseltamivir and securing oseltamivir API global supply sources are essential for long-term viability, especially as the impact of flu vaccine on oseltamivir demand fluctuates.

- Finally, navigating the regulatory approval for oseltamivir generics remains a constant operational focus for all market participants.

What are the key market drivers leading to the rise in the adoption of Tamiflu Oseltamivir Phosphate Industry?

- The primary market driver remains the annual incidence and clinical severity of seasonal influenza, which directly dictates real-time demand for treatment.

- Market demand is fundamentally driven by two powerful forces: the annual severity of seasonal influenza and the strategic imperative of pandemic preparedness.

- A severe flu season can increase prescription volumes by over 40%, directly tying market performance to public health outcomes. Concurrently, government procurement for the strategic national stockpile creates a stable, albeit irregular, demand baseline.

- For instance, a single government tender process can account for up to 30% of a major manufacturer's annual production. The persistent zoonotic influenza threat validates these antiviral drug stockpiling programs and reinforces the need for a robust public health response.

- This dual-demand structure, influenced by pandemic response strategy, ensures oseltamivir's continued relevance as an essential medicine.

What are the market trends shaping the Tamiflu Oseltamivir Phosphate Industry?

- A transformative market trend is the increasing clinical adoption of novel antiviral therapies, particularly those offering alternative mechanisms of action and simplified dosing regimens.

- The market is experiencing a significant evolution driven by the adoption of novel antiviral therapeutic alternatives. The introduction of therapies offering single dose regimens presents a compelling value proposition, enhancing patient compliance and potentially reducing the risk of antiviral resistance. This trend is creating a stratified market where oseltamivir's therapeutic equivalence solidifies its role as the cost-effective standard.

- The integration of rapid point-of-care molecular diagnostics, which can confirm influenza with 98% accuracy in a single visit, supports more targeted early antiviral therapy and efficient viral replication inhibition. These shifts, closely monitored through epidemiological trends, are reshaping clinical practice standards, particularly in developed markets with robust reimbursement frameworks that can accommodate higher-priced innovations.

What challenges does the Tamiflu Oseltamivir Phosphate Industry face during its growth?

- The market faces a significant challenge from intense competition among generic manufacturers, which leads to severe and sustained price erosion.

- The market faces persistent challenges from intense generic competition, which has transformed the landscape into a high-volume, low-margin industry. The proliferation of bioequivalent formulations from numerous manufacturers creates a competitive pricing environment where prices can erode by as much as 80% post-patent expiry.

- This dynamic necessitates an extreme focus on supply chain logistics and securing cost-effective active pharmaceutical ingredient (API) sources to remain viable. Effective seasonal demand forecasting is critical, as a milder-than-expected season can lead to inventory write-offs representing 15-20% of production.

- The structural shift toward generic drug substitution and the need for supply chain resilience put continuous pressure on profitability, even during periods of high volumetric demand.

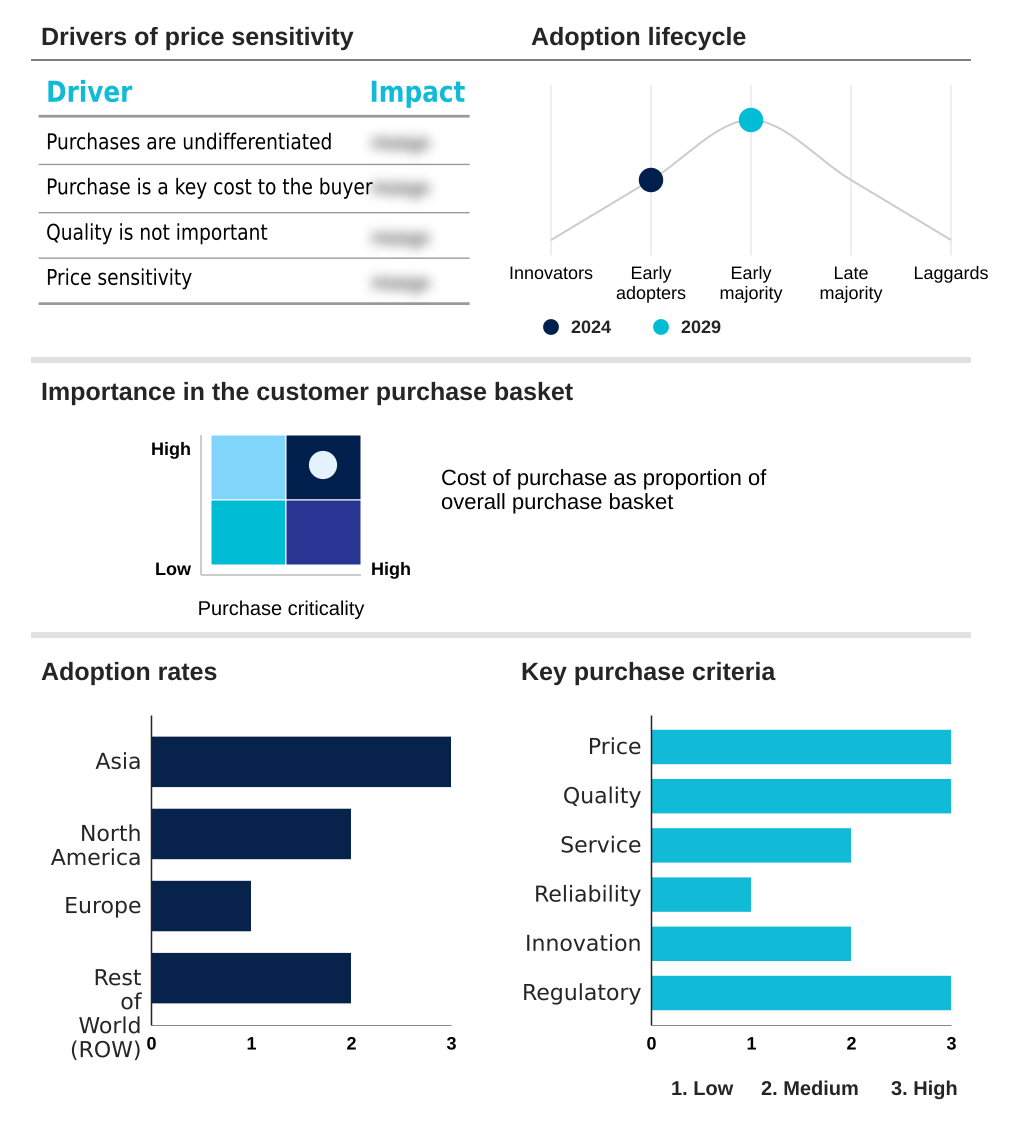

Exclusive Technavio Analysis on Customer Landscape

The tamiflu oseltamivir phosphate market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the tamiflu oseltamivir phosphate market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Tamiflu Oseltamivir Phosphate Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, tamiflu oseltamivir phosphate market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alembic Pharmaceuticals Ltd. - Operations are centered on manufacturing and distributing a diverse portfolio of generic pharmaceuticals, including selective neuraminidase inhibitors for influenza A and B viruses.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alembic Pharmaceuticals Ltd.

- Amneal Pharmaceuticals Inc.

- Aurobindo Pharma Ltd.

- Cipla Inc.

- Epic Pharma LLC

- F. Hoffmann La Roche Ltd.

- Gilead Sciences Inc.

- Hetero Labs Ltd.

- Jubilant Generics Ltd.

- Laurus Labs Ltd.

- Lupin Ltd.

- Macleods Pharmaceuticals Ltd.

- MSN Laboratories

- NATCO Pharma Ltd.

- Nivagen Pharmaceuticals Inc.

- Strides Pharma Ltd.

- Teva Pharmaceutical Ltd.

- Viatris Inc.

- Zydus Group

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Tamiflu oseltamivir phosphate market

- In September, 2024, F. Hoffmann-La Roche Ltd. and Shionogi & Co. Ltd. are expected to file for expanded regulatory approval for baloxavir marboxil for treating hospitalized patients with severe influenza, following positive Phase III trial results, signaling intensified competition in the high-acuity care segment.

- In November, 2024, the US Administration for Strategic Preparedness and Response (ASPR) is anticipated to issue a new procurement tender for approximately 5 million treatment courses of generic oseltamivir phosphate to replenish the Strategic National Stockpile, reinforcing the drug's role in national health security.

- In January, 2025, Teva Pharmaceutical Ltd. announces a 15% expansion of its manufacturing capacity for oseltamivir phosphate oral formulations to meet projected increases in seasonal and pandemic preparedness demand across North America and Europe.

- In April, 2025, Cipla Inc. receives approval from the European Medicines Agency (EMA) for its generic oseltamivir phosphate for oral suspension, expanding pediatric treatment options and increasing competitive pressure in the EU market.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Tamiflu Oseltamivir Phosphate Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 283 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.6% |

| Market growth 2025-2029 | USD 204.5 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 4.4% |

| Key countries | China, Japan, India, South Korea, Indonesia, Singapore, Thailand, US, Canada, Mexico, Germany, France, UK, Italy, Spain, Russia, The Netherlands, Brazil, South Africa, Saudi Arabia, UAE, Australia and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The tamiflu oseltamivir phosphate market functions as a mature, yet vital, segment of the antiviral medication landscape, primarily governed by the interplay of seasonal influenza patterns and strategic public health policy. Its core utility as a neuraminidase inhibitor for the treatment of acute influenza and for prophylactic use ensures consistent, albeit cyclical, demand.

- The market is overwhelmingly dominated by generic formulations, making it a high-volume, cost-driven industry where supply chain logistics and manufacturing scale are key differentiators. Boardroom decisions increasingly center on pandemic preparedness, with government procurement for the strategic national stockpile representing a foundational revenue stream.

- For example, companies with verified, geographically diverse production capabilities for the active pharmaceutical ingredient (API) are viewed as lower-risk partners, commanding a 5% to 10% premium on large contracts. The emergence of zoonotic influenza threats continues to validate investment in bioequivalent formulations that offer therapeutic equivalence.

- While effective against both influenza a virus and influenza b virus, the market must contend with challenges from newer therapies and the constant need for public health surveillance to guide consumption and prevent viral replication inhibition.

What are the Key Data Covered in this Tamiflu Oseltamivir Phosphate Market Research and Growth Report?

-

What is the expected growth of the Tamiflu Oseltamivir Phosphate Market between 2025 and 2029?

-

USD 204.5 million, at a CAGR of 4.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Branded, and Generic), Formulation (Capsules, and Suspension), Indication (Influenza A, Influenza B, and Swine flu) and Geography (Asia, North America, Europe, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

Asia, North America, Europe and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Seasonal influenza incidence and severity, Intense generic competition and severe price erosion

-

-

Who are the major players in the Tamiflu Oseltamivir Phosphate Market?

-

Alembic Pharmaceuticals Ltd., Amneal Pharmaceuticals Inc., Aurobindo Pharma Ltd., Cipla Inc., Epic Pharma LLC, F. Hoffmann La Roche Ltd., Gilead Sciences Inc., Hetero Labs Ltd., Jubilant Generics Ltd., Laurus Labs Ltd., Lupin Ltd., Macleods Pharmaceuticals Ltd., MSN Laboratories, NATCO Pharma Ltd., Nivagen Pharmaceuticals Inc., Strides Pharma Ltd., Teva Pharmaceutical Ltd., Viatris Inc. and Zydus Group

-

Market Research Insights

- The tamiflu oseltamivir phosphate market operates within a dynamic of intense cost pressure and strategic public health demand. The widespread adoption of generic drug substitution has become a cornerstone of pharmaceutical procurement, driving a highly competitive pricing environment.

- This focus on cost-effectiveness is pivotal for government tender processes and pandemic response strategy planning, where securing large volumes at minimal cost is essential for healthcare system readiness. The market's performance is closely tied to seasonal demand forecasting and epidemiological trends, with a poor vaccine match one season potentially increasing treatment demand by up to 25% in the next.

- Efficient supply chain resilience is a key differentiator, as demonstrated by leading suppliers who can guarantee delivery within 48 hours during a public health response, a critical factor in maintaining market leadership.

We can help! Our analysts can customize this tamiflu oseltamivir phosphate market research report to meet your requirements.

RIA -

RIA -