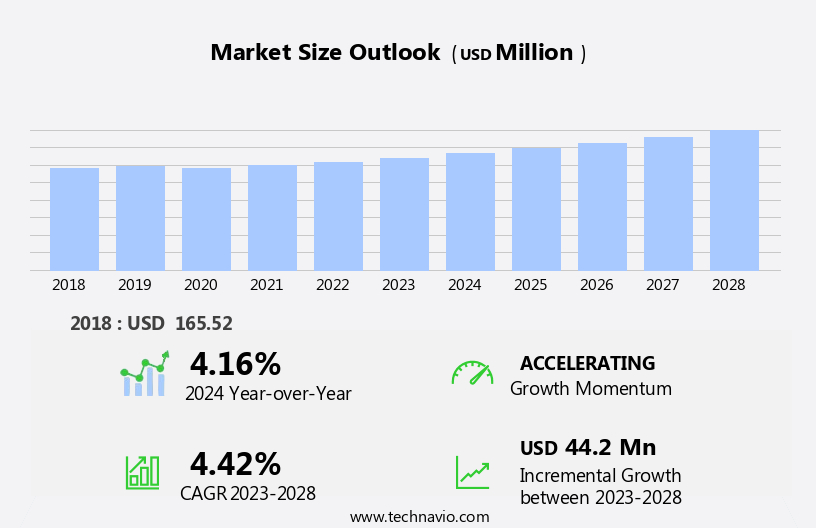

Tapioca Market Size 2024-2028

The tapioca market size is forecast to increase by USD 44.2 million, at a CAGR of 4.42% between 2023 and 2028.

- The market is driven by the growing trend towards alternative food options, particularly those that are gluten-free and grain-free. Tapioca, derived from the cassava root, offers a versatile and cost-effective solution for consumers seeking to avoid traditional grains. Additionally, the usage of tapioca in bioplastics and infant nutrition supplements, including infant formula, baby food products, and organic meat alternatives, is driving market expansion. However, the complexities related to the overconsumption of tapioca, such as its high glycemic index and potential contribution to heart disease, pose challenges to market growth. Furthermore, the increasing popularity of superfoods and organic products is fueling demand for high-quality, sustainably sourced tapioca extracts. The complexities surrounding the sustainability and ethical implications of mass production and consumption of tapioca products must be addressed to ensure long-term market growth.

- Companies seeking to capitalize on this market's opportunities must focus on innovation, sustainability, and ethical production practices to meet the evolving demands of consumers and stakeholders.

What will be the Size of the Tapioca Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

Tapioca, derived from the root of the cassava plant, continues to be a dynamic and evolving market due to its versatile applications across various sectors. Its unique properties, including high amylose content and amylopectin, make it a valuable resource for industries such as food and beverage, pharmaceuticals, and industrial sectors. The ongoing research and development in tapioca processing techniques aim to enhance its efficiency and utility. Tapioca waste and by-products are being explored for their potential in creating new value-added products, such as starch derivatives and films. The focus on sustainability metrics and eco-friendly processing methods is also gaining momentum in the tapioca industry.

Tapioca starch extraction and gelatinization processes are continually refined to optimize yield and functionality. The rheological properties of tapioca starch are of particular interest, as they impact its use in various applications, from food grade to industrial applications. The continuous exploration of tapioca's potential is evident in the emergence of new technologies and applications. For instance, tapioca starch hydrolysis leads to the production of syrups and sweeteners, while tapioca-based adhesives offer sustainable alternatives to traditional adhesives. The dynamic nature of the market is further underscored by ongoing research into its properties and potential applications. For example, tapioca starch crystallization and modifications are being studied to expand its use in various industries.

The potential for tapioca starch films and Biodegradable Plastics is a promising area of exploration, highlighting the ongoing evolution of the market.

How is this Tapioca Industry segmented?

The tapioca industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

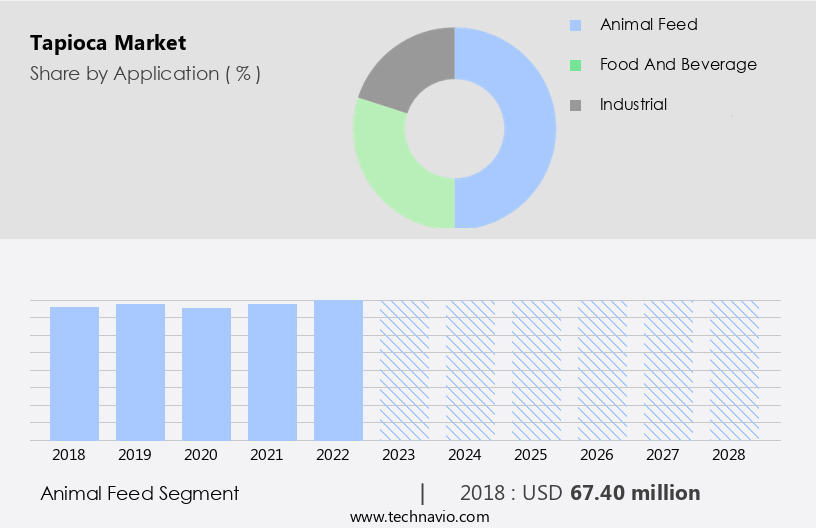

- Animal feed

- Food and beverage

- Industrial

- Type

- Fresh

- Dried

- Product

- Tapioca Animal Feed

- Tapioca Flour

- Tapioca Chips

- Tapioca Pellets

- Tapioca Pearls

- Tapioca Syrup

- Tapioca Maltodextrins

- Tapioca Syrup Solids

- Source

- Organic

- Conventional

- Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

The animal feed segment is estimated to witness significant growth during the forecast period.

Tapioca, derived from the cassava root, offers versatile applications in various industries. The animal feed segment dominates The market, accounting for over a quarter of its usage in 2023. This is due to the increasing demand for alternative feed sources as the prices of traditional animal feed raw materials like maize continue to rise. Tapioca waste, or cassava pomace, is a byproduct of starch processing and is primarily used as animal feed. Approximately equal amounts of starch and cassava pomace are generated from cassava roots. Industrial tapioca applications include food, pharmaceuticals, and paper industries.

Tapioca starch undergoes processes like retrogradation, oxidation, gelatinization, and hydrolysis to enhance its functionality. Modifications like derivatives and crystallization further expand its uses. Tapioca dextrin, with its unique properties, is gaining popularity in food and pharmaceutical industries. Sustainability is a significant concern in tapioca processing, with efforts being made to optimize processing efficiency and minimize waste. Cassava processing techniques, such as fermentation and enzyme treatment, are being explored to enhance tapioca starch quality. Tapioca syrup manufacturing and the production of tapioca-based adhesives are other growing applications. Food grade tapioca and its rheological properties are crucial in the food industry, while tapioca starch films find applications in packaging.

The Animal feed segment was valued at USD 67.40 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

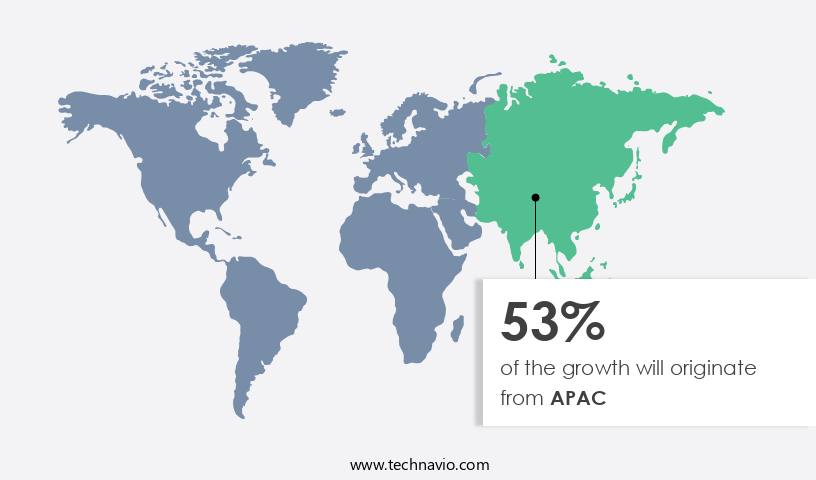

APAC is estimated to contribute 53% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is characterized by its extensive use in various industries and applications. Tapioca pearls come in different sizes, catering to diverse consumer preferences in food and beverage sectors. Industrial tapioca finds significant use in the production of adhesives, paper, and textiles. Tapioca starch undergoes retrogradation and oxidation, influencing its functionality and viscosity. Gelatinization is a crucial process in tapioca starch production, while dextrin is a valuable by-product with unique properties. The amylose and amylopectin content in tapioca varies, affecting its processing efficiency and end-use applications. Cassava processing techniques are essential in tapioca production, with countries like Thailand and Vietnam being major global exporters.

South-Eastern Asia is the largest consumer region, with China, Thailand, Indonesia, Vietnam, and India being key markets. Japan, Cambodia, and the Philippines also exhibit rising demand. Tapioca starch hydrolysis leads to derivatives and modifications, expanding its applications in food, pharmaceuticals, and other industries. Sustainability metrics are increasingly important in tapioca production and processing, with a focus on minimizing waste and optimizing efficiency. Tapioca starch films, syrup manufacturing, and other value-added products further broaden its market scope.

Market Dynamics

The Global Tapioca Market is experiencing robust growth, fueled by versatile applications and rising health-conscious demand. The commercial tapioca market thrives as tapioca in food industry gains popularity, particularly in tapioca for bubble tea and tapioca for vegan diets. Innovations like tapioca-based bioplastics and tapioca sustainable packaging address eco-friendly trends, while tapioca for digestive health and benefits of tapioca for digestive health appeal to wellness-focused consumers. The tapioca gluten-free market grows with gluten-free tapioca products, supported by tapioca for clean-label foods. Advanced tapioca starch extraction and tapioca processing technology, including tapioca pearl machines, enhance efficiency. Tapioca for food texture and tapioca starch innovations drive the tapioca beverage market and tapioca for low-carb diets, shaping a dynamic industry landscape.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Tapioca Industry?

- The growing preference for alternatives to gluten and grain food products is the primary market driver. This trend is shaped by an increasing awareness and intolerance towards gluten and grains among consumers, leading to a significant demand for gluten-free and grain-free food options.

- Tapioca, derived from the cassava root, is a popular alternative to gluten-for those with intolerance or allergies to wheat and related grains. The versatile starch is available in various sizes as tapioca pearls and is used extensively in industrial applications, including food, pharmaceuticals, and cosmetics. Tapioca starch undergoes processes like retrogradation and oxidation, which affect its functionality and gelatinization properties. These processes are crucial in determining the final product's texture and performance.

- The production of tapioca flour is a significant industry, with various methods used to extract and refine the starch. Understanding the dynamics of tapioca starch's behavior during processing is essential for optimizing its functionality in various applications.

What are the market trends shaping the Tapioca Industry?

- Trends in the bioplastics industry include the increasing use of tapioca as a raw material. This eco-friendly alternative to traditional plastics is gaining popularity due to its sustainability and biodegradability.

- Tapioca, a starch derived from the cassava root, offers valuable properties for the production of biodegradable bioplastics. With an amylose content of approximately 25%, tapioca starch is an effective raw material for bioplastic manufacturing. The utilization of tapioca waste in bioplastic production is a sustainable solution for reducing industrial waste and increasing processing efficiency. Tapioca processing involves the extraction of starch, which is rich in amylopectin, a complex carbohydrate that enhances the biodegradability of bioplastics. The bioplastics derived from tapioca are characterized by their odorless, smooth, and transparent properties.

- Tapioca processing by-products can be further refined to extract additional value, such as tapioca dextrin, which can be used as a thickener or sweetener in various industries. The use of tapioca in bioplastic production is a promising development in the bioplastics industry, contributing to the production of eco-friendly and sustainable materials.

What challenges does the Tapioca Industry face during its growth?

- The complexities arising from overconsumption pose a significant challenge to the industry's growth trajectory.

- Tapioca, derived from the cassava root, is a starch that offers various applications in the food, pharmaceutical, and industrial sectors. The production process involves tapioca starch hydrolysis, which affects its viscosity and determines its suitability for different uses. Tapioca starch derivatives and modifications are essential for enhancing its functional properties, such as thickening, gelling, and film-forming abilities. Sustainability metrics play a crucial role in the market, with a focus on eco-friendly cassava processing techniques that minimize waste and ensure efficient use of resources. Tapioca starch films are gaining popularity due to their biodegradability and potential as sustainable alternatives to synthetic plastics.

- Despite its numerous benefits, tapioca consumption should be monitored due to its high glycemic index, which can cause rapid increases in blood sugar levels. Proper processing techniques are also necessary to eliminate linamarin, a toxic compound found in raw tapioca, which can be converted to cyanide in the human body.

Exclusive Customer Landscape

The tapioca market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the tapioca market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, tapioca market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

American Key Products Inc. - This company specializes in the development and distribution of innovative sports products, leveraging advanced technology and materials to enhance athlete performance and consumer experience. Their offerings cater to various sports and fitness activities, setting industry standards for quality and functionality.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- American Key Products Inc.

- Authentic Foods

- Cargill Inc.

- Ciranda Inc.

- Ekta International

- Emsland Starke GmbH

- Hunan Kang pharmaceutical Ltd.

- Ingredion Inc.

- Jayavel Sago Factory

- KengSeng Group of Co.

- Malt Products Corp.

- Parchem Fine and Specialty Chemicals Inc.

- PT Budi Starch and Sweetener Tbk

- Royal Ingredients Group BV

- Sonish Starch Technology Co. Ltd.

- SPAC Starch Products India Pvt. Ltd.

- Tapioca Vietnam

- Tate and Lyle PLC

- Tereos Participations

- Venus Starch Suppliers

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Tapioca Market

- In January 2024, leading tapioca starch producer, Amalgamated Starch Corporation, announced a strategic partnership with food processing giant, Nestle, to expand their tapioca-based food offerings. This collaboration aimed to increase the production capacity of tapioca starch by 30%, as reported in Amalgamated Starch's Q1 2024 press release.

- In March 2024, Brazilian tapioca starch manufacturer, GranBio, secured a USD50 million investment from the Brazilian Development Bank (BNDES) to expand its production capacity and support the growing global demand for sustainable bio-based ingredients. According to GranBio's press release, the investment would enable the company to increase its annual production capacity to 1.5 million metric tons.

- In May 2024, the European Union approved the use of tapioca starch as a functional ingredient in food and feed applications, as stated in the European Commission's official press release. This approval opened new opportunities for tapioca starch producers to enter the European market, which is the world's second-largest food market.

- In April 2025, Thai tapioca starch producer, Mitr Phol, acquired a 51% stake in Indonesian tapioca starch manufacturer, PT Pabrik Tapioka Indonesia. The acquisition, as reported in Mitr Phol's Q1 2025 financial report, was aimed at expanding Mitr Phol's production capacity and market share in the Southeast Asian region.

Research Analyst Overview

- In the dynamic tapioca starch market, various types of tapioca starch, including native, hydroxypropyl, phosphate-modified, and pre-gelatinized, cater to diverse applications. Tapioca starch packaging ensures product preservation, while rheology and digestibility properties influence its usage in food, pharmaceutical, and industrial sectors. Nutrition and benefits of tapioca starch, such as high digestibility and gluten-free properties, fuel demand. Pricing, storage, and transportation costs are crucial factors influencing market trends.

- Cassava cultivation methods impact the purity and quality of tapioca starch production. Oxidized, acetylated, crosslinked, and enzyme-modified tapioca starch varieties expand the market scope. Tapioca starch uses in industries like paper, textile, and adhesives continue to grow, driving market expansion.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Tapioca Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

166 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.42% |

|

Market growth 2024-2028 |

USD 44.2 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.16 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Tapioca Market Research and Growth Report?

- CAGR of the Tapioca industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the tapioca market growth of industry companies

We can help! Our analysts can customize this tapioca market research report to meet your requirements.

RIA -

RIA -