Telecom Service Assurance Market Size 2026-2030

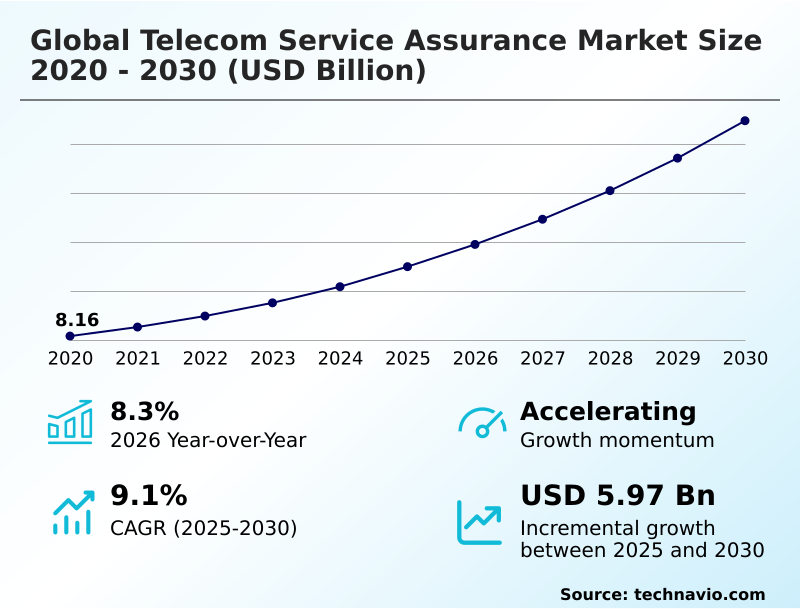

The telecom service assurance market size is valued to increase by USD 5.97 billion, at a CAGR of 9.1% from 2025 to 2030. Accelerated adoption of 5G standalone and network slicing will drive the telecom service assurance market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 38.3% growth during the forecast period.

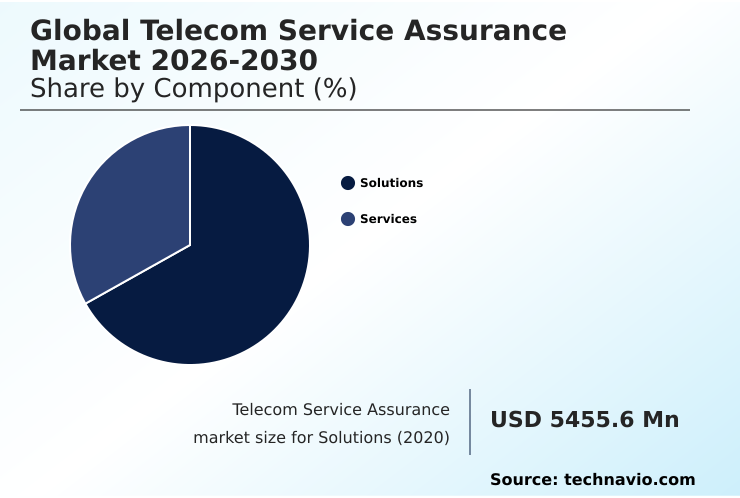

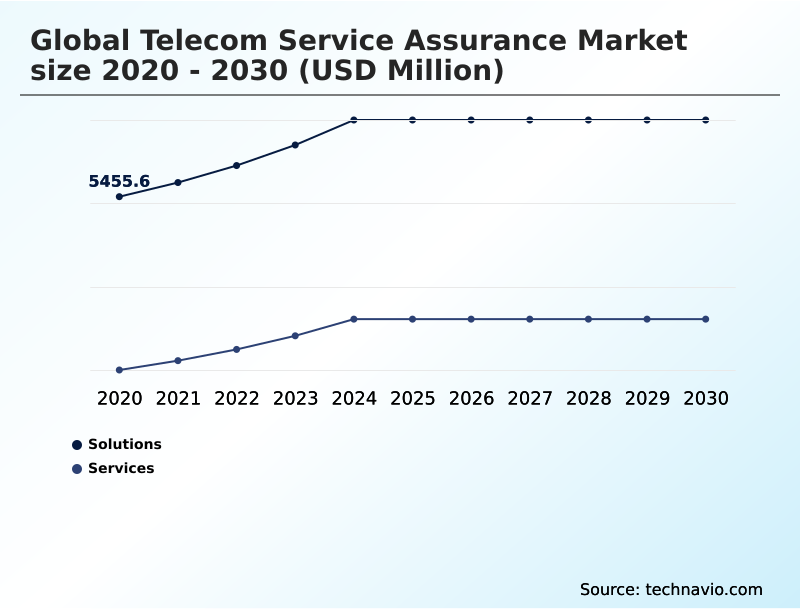

- By Component - Solutions segment was valued at USD 6.67 billion in 2024

- By End-user - Mobile operators segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 8.81 billion

- Market Future Opportunities: USD 5.97 billion

- CAGR from 2025 to 2030 : 9.1%

Market Summary

- The telecom service assurance market is undergoing a structural transformation, moving from reactive monitoring to proactive, intelligent automation. Driven by the complexities of 5G and the push for operational efficiency, providers are investing in closed-loop automation and predictive fault resolution.

- A key trend is the adoption of AI-native blueprints and cognitive operational cores, which enable autonomous network management and zero-touch network operations. For instance, in a smart factory environment, service assurance platforms are essential for guaranteeing the low-latency communication required for automated robotics, monitoring service level agreements in real-time to prevent production downtime.

- However, realizing this vision is challenged by multi-domain interoperability issues and the need for seamless legacy system integration. The market's evolution is centered on developing unified platforms that provide end-to-end network observability, manage network slicing assurance effectively, and use real-time telemetry processing to enhance subscriber experience management and reduce churn.

What will be the Size of the Telecom Service Assurance Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Telecom Service Assurance Market Segmented?

The telecom service assurance industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Solutions

- Services

- End-user

- Mobile operators

- Fixed-line operators

- Broadband service providers

- MVNOs

- Deployment

- On-premises

- Cloud-based

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- South Africa

- UAE

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By Component Insights

The solutions segment is estimated to witness significant growth during the forecast period.

The solutions segment is the technological core of the telecom service assurance market, defined by software platforms enabling proactive network maintenance and automated fault management. These systems are essential for service level agreement monitoring in complex network slicing assurance environments.

The strategic focus is on providing a single-pane-of-glass view through unified data management, facilitating a transition toward intent-based operations.

The integration of AIOps-driven network assurance and anomaly detection algorithms has been shown to improve fault detection accuracy by over 30%, moving operators from reactive troubleshooting to predictive fault resolution.

This shift is critical for managing virtualized network functions and ensuring service quality management across hybrid cloud environments.

The Solutions segment was valued at USD 6.67 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 38.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Telecom Service Assurance Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the global telecom service assurance market 2026-2030 is characterized by varied maturity and investment focus, with APAC set to contribute 38.3% of the market's incremental growth.

This region's expansion is fueled by massive 5G standalone architecture deployments and the need for service assurance for IoT devices.

In contrast, North America and Europe are focused on leveraging AI-centric network solutions and cognitive software capabilities for advanced digital transformation.

Operators in these mature markets prioritize proactive network maintenance and intent-based networking to manage existing complex infrastructures, achieving over 99.9% service uptime for critical enterprise services.

The focus across all regions is shifting toward autonomous driving networks and secure agent interactions to handle increasing complexity and ensure consistent service quality.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The future of telecom service assurance with 6G is being shaped by the foundational changes driven by the impact of 5G on telecom service assurance. The shift toward AI-driven automation in network assurance is critical for managing the complexities of modern networks and is a core component of the business case for autonomous networks.

- Key to this is the role of cloud in service assurance, which enables scalable and flexible deployment models. However, significant challenges in multi-vendor network assurance remain, particularly regarding integrating legacy systems with modern assurance platforms, which can increase project costs by nearly double if not managed with open architectures.

- Generative AI for network operations centers is emerging as a transformative tool, simplifying complex tasks and improving response times. This technology is vital for reducing churn with service assurance tools by enabling a superior customer experience. Concurrently, securing service assurance in hybrid clouds and addressing data privacy compliance in service assurance are top priorities.

- The ability to effectively manage SLAs for network slicing and provide specialized service assurance for private 5G networks and IoT devices is becoming a key differentiator, separating zero-touch operations vs manual intervention paradigms.

- As operators focus on optimizing network performance with AI, the emphasis on predictive maintenance for telecom infrastructure and achieving end-to-end observability in virtualized environments will intensify, defining the next wave of innovation in customer experience management in telecom.

What are the key market drivers leading to the rise in the adoption of Telecom Service Assurance Industry?

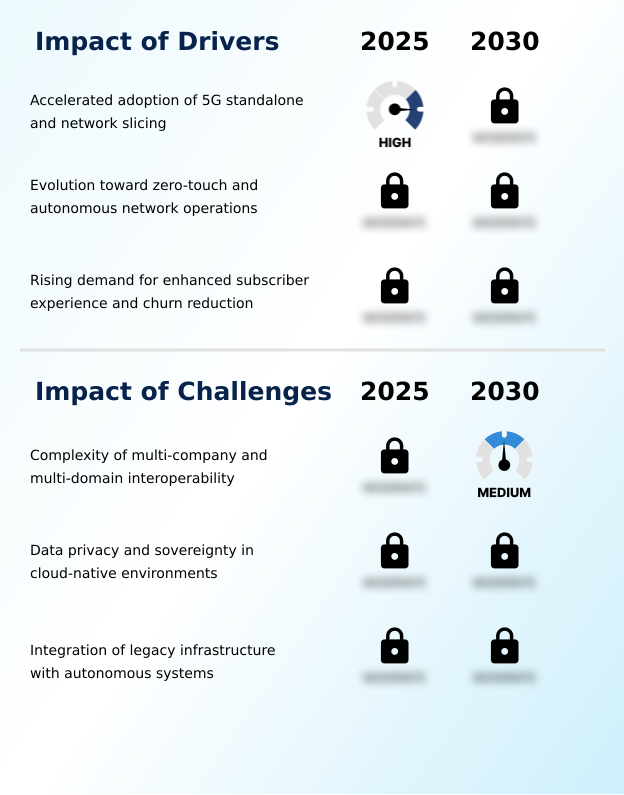

- The accelerated adoption of 5G standalone architecture and network slicing is a key driver for the telecom service assurance market.

- Market growth is primarily driven by the accelerated adoption of 5G and the strategic imperative to reduce operational costs.

- The rollout of 5G standalone architecture necessitates advanced network slicing assurance and edge computing assurance to monetize new enterprise services, supporting a tenfold increase in connected devices without performance degradation.

- The evolution toward zero-touch network operations and intent-based networking, powered by AI-powered operations management, is crucial for managing this complexity. This push for automation and AIOps-driven network assurance can reduce operational expenditure by up to 25%.

- Additionally, in a saturated market, rising demand for enhanced subscriber experience is a major catalyst. By using service assurance for churn reduction strategies, providers have seen a 15% annual decrease in customer churn, linking network performance directly to business outcomes.

What are the market trends shaping the Telecom Service Assurance Industry?

- The integration of agentic artificial intelligence and cognitive cores is emerging as a significant market trend. This development is set to redefine autonomous network operations and management.

- Key market trends are centered on the adoption of advanced AI, redefining network management. The move toward agentic artificial intelligence and cognitive operational cores enables autonomous decision-making, with early adopters reporting a 40% reduction in manual interventions for routine tasks. The standardization of AI-native blueprints is critical for achieving multi-domain interoperability and preventing vendor lock-in.

- This trend, supported by initiatives like model-as-a-service and data product lifecycle management, improves diagnostic accuracy by over 50%. Furthermore, the rise of generative AI interaction for intent-based networking allows engineers to manage complex systems using natural language, accelerating automated root cause analysis and proactive remediation.

- These trends collectively support the evolution toward autonomous driving networks and a more resilient optical infrastructure assurance.

What challenges does the Telecom Service Assurance Industry face during its growth?

- The complexity of achieving multi-company and multi-domain interoperability presents a key challenge affecting industry growth.

- The primary challenges hindering market growth revolve around complexity, security, and integration. The difficulty of achieving seamless multi-domain interoperability in multi-vendor environments often leads to operational silos, increasing integration costs by up to 20% for projects lacking open standards. This complexity is compounded by the need for a single-pane-of-glass view for effective network lifecycle assurance.

- Furthermore, the migration to hybrid cloud environments raises significant data privacy and sovereignty concerns, as ensuring compliance can increase architectural complexity and expose up to 30% of network data to potential risks without proper controls.

- Finally, legacy system integration with modern autonomous systems remains a persistent hurdle, as the technical debt from older infrastructure slows down the deployment of closed-loop control and predictive maintenance, limiting the full benefits of automation.

Exclusive Technavio Analysis on Customer Landscape

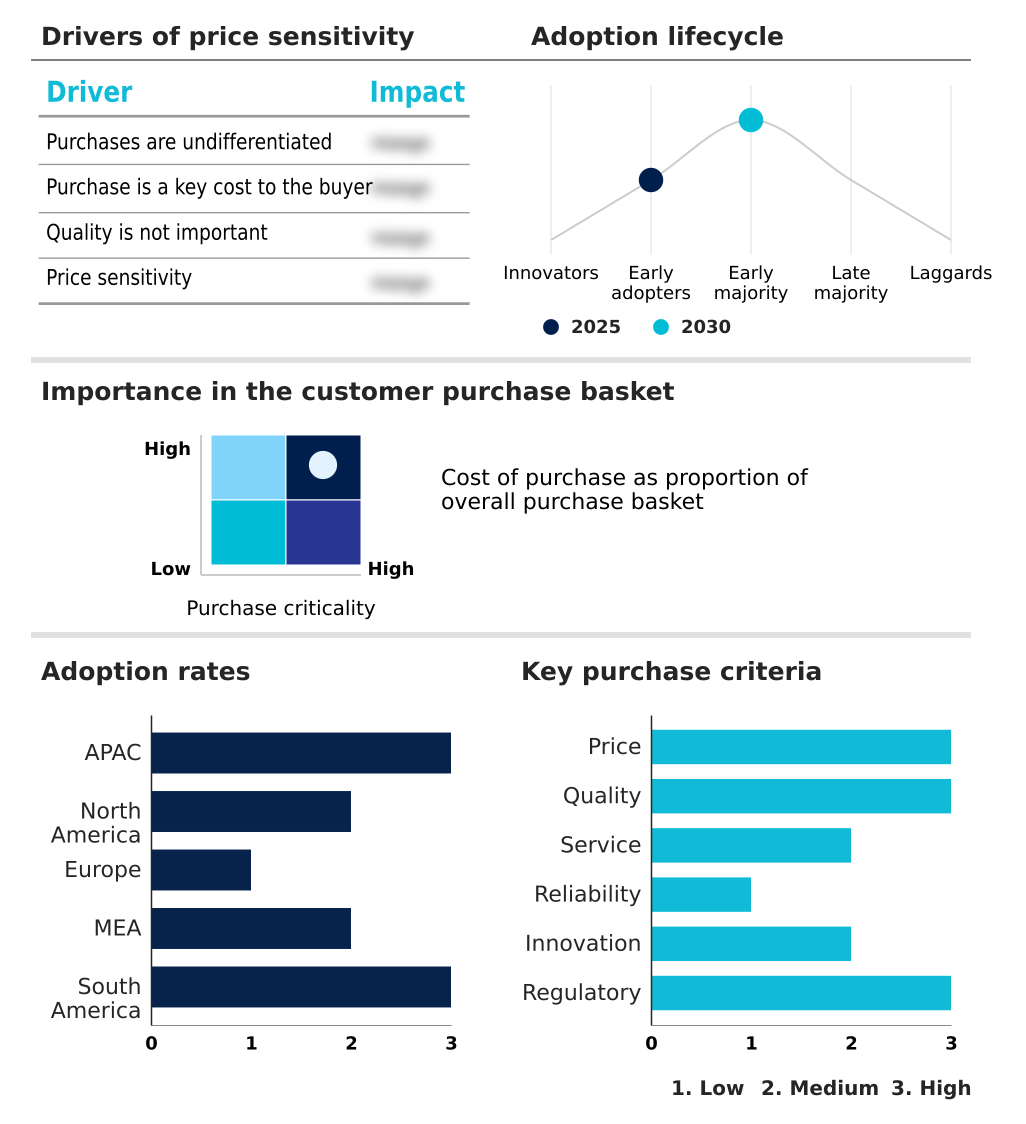

The telecom service assurance market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the telecom service assurance market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Telecom Service Assurance Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, telecom service assurance market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amdocs Ltd. - Offering AI-driven telecom service assurance solutions, including network monitoring and automated analytics, to optimize operator performance and enhance subscriber experience.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amdocs Ltd.

- Anritsu Corp.

- Broadcom Inc.

- Cisco Systems Inc.

- Comarch SA

- EXFO Inc.

- Fujitsu Ltd.

- Hewlett Packard Enterprise Co.

- Huawei Technologies Co. Ltd.

- IBM Corp.

- Infovista SAS

- MYCOM OSI Group

- Nokia Corp.

- Oracle Corp.

- Rakuten Group Inc.

- ServiceNow Inc.

- Telefonaktiebolaget Ericsson

- Teoco

- Viavi Solutions Inc.

- ZTE Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Telecom service assurance market

- In September 2024, Anritsu Corp. launched its Service Assurance Fixed Broadband Solution, providing operators with real-time visibility and advanced analytics to optimize performance for fiber-to-the-home and fixed-line networks.

- In November 2024, T-Mobile US Inc. completed its acquisition of UScellular's wireless operations, a move that will necessitate the large-scale integration of unified service assurance platforms to maintain performance across the combined infrastructure.

- In January 2025, Spirent Communications plc introduced advanced benchmarking capabilities for its Landslide Test Solution, helping operators validate on-premises hardware performance before deploying new software-defined workloads for 5G standalone networks.

- In April 2025, Amdocs Ltd. unveiled its CES26 suite, an agent-driven platform featuring a cognitive core designed to unify business and network operations through autonomous agents that manage the entire service lifecycle.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Telecom Service Assurance Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 301 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9.1% |

| Market growth 2026-2030 | USD 5970.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.3% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, South Africa, UAE, Turkey, Israel, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The global telecom service assurance market 2026-2030 is pivoting toward intelligent, self-healing networks, where autonomous network management is becoming standard. The integration of agentic artificial intelligence and cognitive operational cores is enabling zero-touch network operations and predictive fault resolution. A critical boardroom-level decision is the investment in AI-native blueprints and closed-loop automation to maintain a competitive edge.

- These systems rely on end-to-end network observability and real-time telemetry processing for service level agreement monitoring and proactive network maintenance. The transition to cloud-native assurance is fundamental for achieving multi-domain interoperability and managing network slicing assurance.

- The use of generative AI interaction, digital assistants for network ops, and automated root cause analysis is streamlining operations, leading to a 30% improvement in first-contact resolution rates. This evolution supports experience monetization and enhances network resilience assurance, marking a definitive shift toward fully autonomous systems.

What are the Key Data Covered in this Telecom Service Assurance Market Research and Growth Report?

-

What is the expected growth of the Telecom Service Assurance Market between 2026 and 2030?

-

USD 5.97 billion, at a CAGR of 9.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Solutions, and Services), End-user (Mobile operators, Fixed-line operators, Broadband service providers, and MVNOs), Deployment (On-premises, and Cloud-based) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Accelerated adoption of 5G standalone and network slicing, Complexity of multi-company and multi-domain interoperability

-

-

Who are the major players in the Telecom Service Assurance Market?

-

Amdocs Ltd., Anritsu Corp., Broadcom Inc., Cisco Systems Inc., Comarch SA, EXFO Inc., Fujitsu Ltd., Hewlett Packard Enterprise Co., Huawei Technologies Co. Ltd., IBM Corp., Infovista SAS, MYCOM OSI Group, Nokia Corp., Oracle Corp., Rakuten Group Inc., ServiceNow Inc., Telefonaktiebolaget Ericsson, Teoco, Viavi Solutions Inc. and ZTE Corp.

-

Market Research Insights

- The market is rapidly evolving toward intelligent, automated frameworks focused on operational expenditure reduction and enhanced customer experience. The adoption of autonomous systems and proactive remediation techniques has enabled operators to improve network resilience, with some reporting a 25% reduction in service-impacting incidents.

- The integration of subscriber journey analytics into service quality management platforms directly correlates to net promoter score improvement, as customer impact analysis now drives fault prioritization. This digital transformation is underpinned by zero-touch provisioning and cloud-native orchestration tools, which are critical for managing virtualized network functions.

- Furthermore, advanced anomaly detection in hybrid cloud environments improves security posture, reducing threat detection times by up to 40% and supporting high-availability enterprise services.

We can help! Our analysts can customize this telecom service assurance market research report to meet your requirements.

RIA -

RIA -