Thin Film Transistor (TFT) Liquid Crystal Display (LCD) Market Size 2026-2030

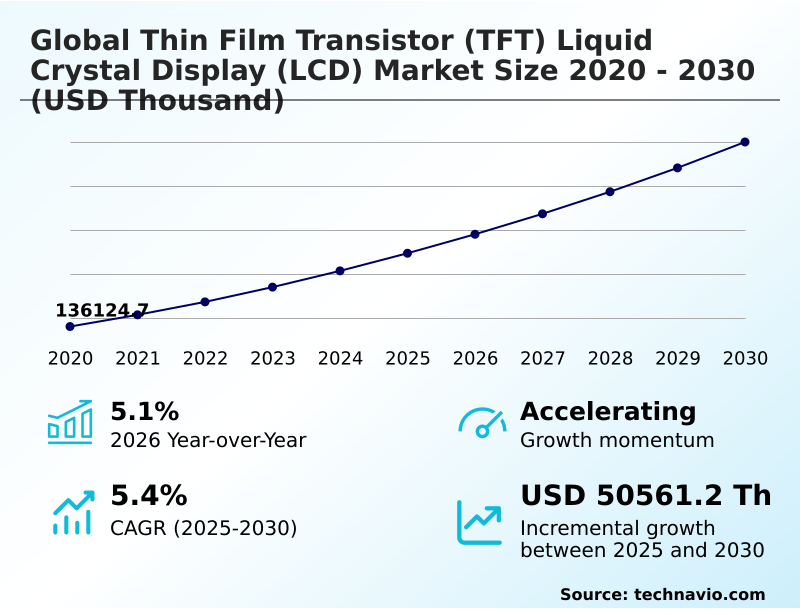

The thin film transistor (tft) liquid crystal display (lcd) market size is valued to increase by USD 50.56 million, at a CAGR of 5.4% from 2025 to 2030. Growing demand for high resolution large format displays in television sector will drive the thin film transistor (tft) liquid crystal display (lcd) market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 32.8% growth during the forecast period.

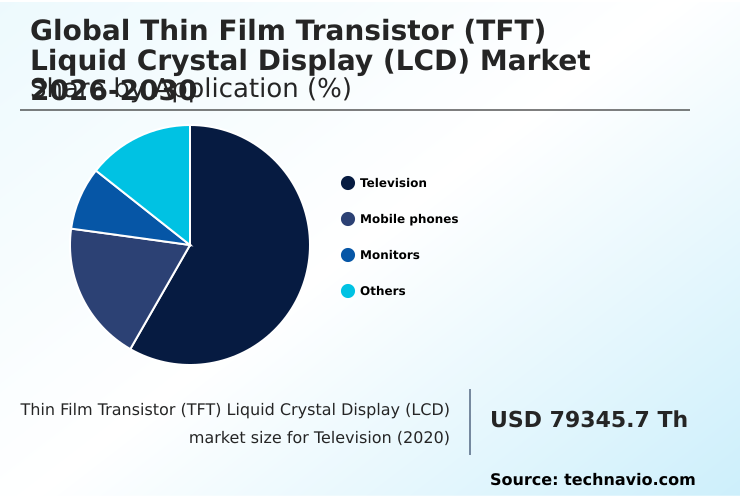

- By Application - Television segment was valued at USD 94.75 million in 2024

- By Type - Large displays segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities:

- Market Future Opportunities: USD 50.56 million

- CAGR from 2025 to 2030 : 5.4%

Market Summary

- The Thin Film Transistor (TFT) Liquid Crystal Display (LCD) Market is sustained by its foundational role in consumer electronics, automotive systems, and industrial controls. Its mature manufacturing ecosystem allows for cost-effective production of reliable panels, a key driver for its continued prevalence.

- A primary trend is the diversification into specialized applications, such as automotive grade displays and industrial strength LCDs, which demand high durability and performance under varied conditions. This necessitates advancements in core components like the transistor backplane and backlight unit to improve energy efficiency and thermal stability.

- However, the industry faces significant challenges from the rise of self-emissive display technologies, which offer superior contrast and form factors. In response, manufacturers are enhancing TFT LCDs with features like mini-LED backlights and higher refresh rates.

- A key business scenario involves optimizing the supply chain for critical materials such as glass substrates and polarizers; a disruption in a single component supplier can halt production lines, impacting delivery schedules for major electronics brands and highlighting the need for supply chain resilience. This dynamic environment compels continuous innovation in both product performance and manufacturing processes to maintain competitiveness.

What will be the Size of the Thin Film Transistor (TFT) Liquid Crystal Display (LCD) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Thin Film Transistor (TFT) Liquid Crystal Display (LCD) Market Segmented?

The thin film transistor (tft) liquid crystal display (lcd) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD thousand" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

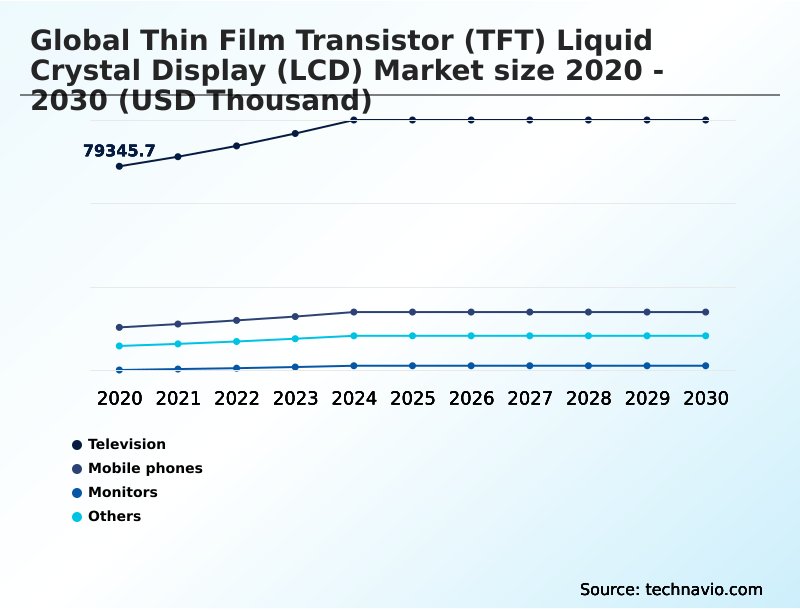

- Application

- Television

- Mobile phones

- Monitors

- Others

- Type

- Large displays

- Small and medium displays

- End-user

- Consumer electronics

- Automotive

- Retail and hospitality

- Industrial

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Application Insights

The television segment is estimated to witness significant growth during the forecast period.

The television segment is a cornerstone of the market, driven by consumer demand for high resolution imaging. This trend fuels advancements in large format screens with high refresh rates and faster response times.

The industry is optimizing the deposition process and investing in advanced backlighting technologies, including mini-LED backlights, to improve the contrast ratio. Manufacturers are focusing on the transistor backplane to support higher pixel density.

The implementation of automated inspection systems has improved production yield by over 10%, ensuring a stable supply of panels with consistent color accuracy.

This focus on operational efficiency helps manage costs while developing premium screens with superior viewing angles and a wider color gamut, alongside advancements in medical imaging displays.

The Television segment was valued at USD 94.75 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 32.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Thin Film Transistor (TFT) Liquid Crystal Display (LCD) Market Demand is Rising in APAC Get Free Sample

The geographic landscape is dominated by manufacturing hubs in APAC, which accounts for over 32% of the incremental growth opportunities, driven by economies of scale in producing everything from high brightness panels to flexible LCD displays.

This region's focus on smart manufacturing has led to significant operational gains, with some facilities reporting a 12% improvement in yield management systems through the use of machine learning quality control.

North America and Europe remain key consumption markets, demanding high-performance automotive grade displays and specialized medical imaging displays. The emphasis in these regions is on adherence to stringent environmental compliance and energy efficiency mandates.

This global dynamic creates a market where Asian production efficiency, centered on technologies like LTPS TFT panels and photolithography, serves the high-value, application-specific demands of Western economies.

Market Dynamics

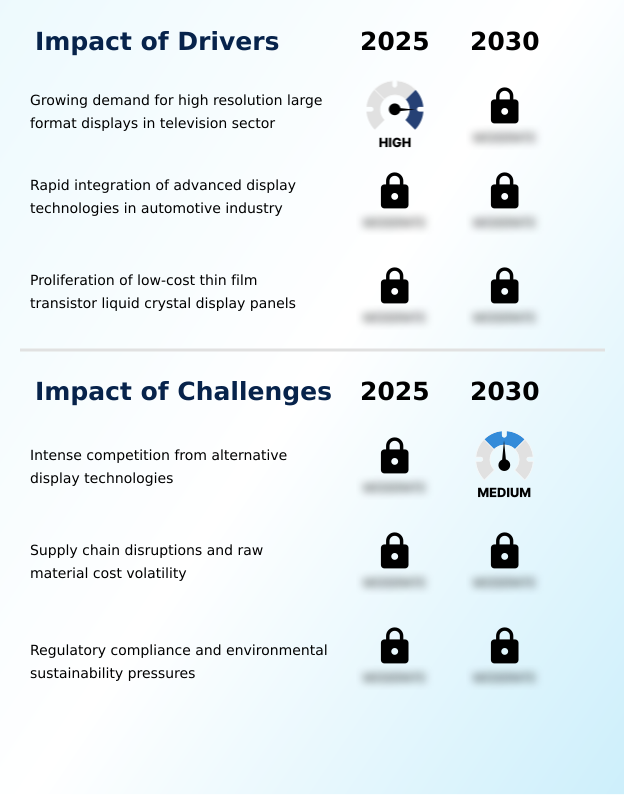

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the market is increasingly granular, focusing on specific applications and competitive positioning. For instance, the market for high refresh rate gaming monitors is pushing technical boundaries, while the demand for durable displays for industrial automation and industrial hmi with tft display technology prioritizes reliability over peak performance.

- Similarly, the requirements for tft lcd for automotive dashboards and advanced driver assistance system displays differ significantly from those for tft lcd in consumer electronics. The debate over tft vs oled for smartphones continues in mid-range segments, where cost effective tft panel production remains a key advantage.

- Companies are engineering specialized solutions like sunlight readable marine displays and medical grade diagnostic displays. The development of energy efficient backlight units and low power tft for wearables addresses battery life concerns. Meanwhile, the growth in large format digital signage solutions and high resolution professional monitors creates distinct supply chain demands.

- The market for curved tft displays for cockpits and the versatile tft panel for portable devices shows further diversification. Operational planning must account for regional growth disparities; with some markets growing more than 1.5 times faster than others, this directly impacts logistics and inventory management, especially given the impact of raw material costs and potential tft display supply chain disruptions.

- Furthermore, navigating regulatory compliance for display manufacturing and establishing processes for recycling tft lcd panel components are becoming critical to long-term viability.

What are the key market drivers leading to the rise in the adoption of Thin Film Transistor (TFT) Liquid Crystal Display (LCD) Industry?

- The growing demand for high-resolution, large-format displays within the television sector is a key driver of market growth.

- Market growth is primarily driven by expanding applications in the automotive and consumer electronics sectors. The increasing digitization of vehicle cockpits is fueling demand for automotive infotainment displays, with some luxury models now featuring screens as large as 31 inches.

- This trend requires high-performance panels with excellent thermal stability and color accuracy, often in sunlight readable display formats. In consumer electronics, the proliferation of affordable smartphones with features like blue light filtering remains a significant driver.

- The cost-effectiveness of thin film transistor technology allows manufacturers to deliver high resolution imaging at competitive price points. Demand for large-format televisions with high pixel density and superior viewing angles also continues to drive volume, supported by manufacturing advancements.

What are the market trends shaping the Thin Film Transistor (TFT) Liquid Crystal Display (LCD) Industry?

- The integration of high refresh rate and ultra-high-definition technologies represents an important market trend. This evolution is driven by increasing demand for superior visual performance across consumer and professional applications.

- Key market trends are centered on enhancing production efficiency and panel performance through smart manufacturing. The adoption of AI-driven automated inspection systems has significantly reduced pixel defects, while the implementation of advanced process control algorithms has improved production yields by up to 12%. This push for automation extends to robotic systems handling large glass substrates, optimizing the clean room environment.

- On the product side, diversification into specialized applications like automotive grade displays and industrial strength LCDs is a primary focus.

- These trends are supported by technological advancements in core components, such as the use of oxide transistors and LTPS TFT panels to achieve higher refresh rates and better energy efficiency, making them competitive for high-performance applications that demand high dynamic range.

What challenges does the Thin Film Transistor (TFT) Liquid Crystal Display (LCD) Industry face during its growth?

- Intense competition from alternative display technologies presents a key challenge affecting the industry's growth trajectory.

- The market faces significant headwinds from supply chain volatility and intense competition from electrophoretic display options. Price adjustments for essential raw materials, such as display glass substrates, are putting direct pressure on manufacturer margins. Geopolitical instability has also led to shipping delays for critical components like polarizers and driver integrated circuits, disrupting production schedules.

- Furthermore, the industry is grappling with stringent environmental compliance, with new wastewater and air emission standards leading to increased operational costs. For instance, some companies have reported significant increases in environmental compliance expenditures.

- These factors, combined with the technical difficulty of electronic waste recycling and the rise of alternative dual stack panels, create a challenging environment requiring robust supply chain resilience and strategic innovation.

Exclusive Technavio Analysis on Customer Landscape

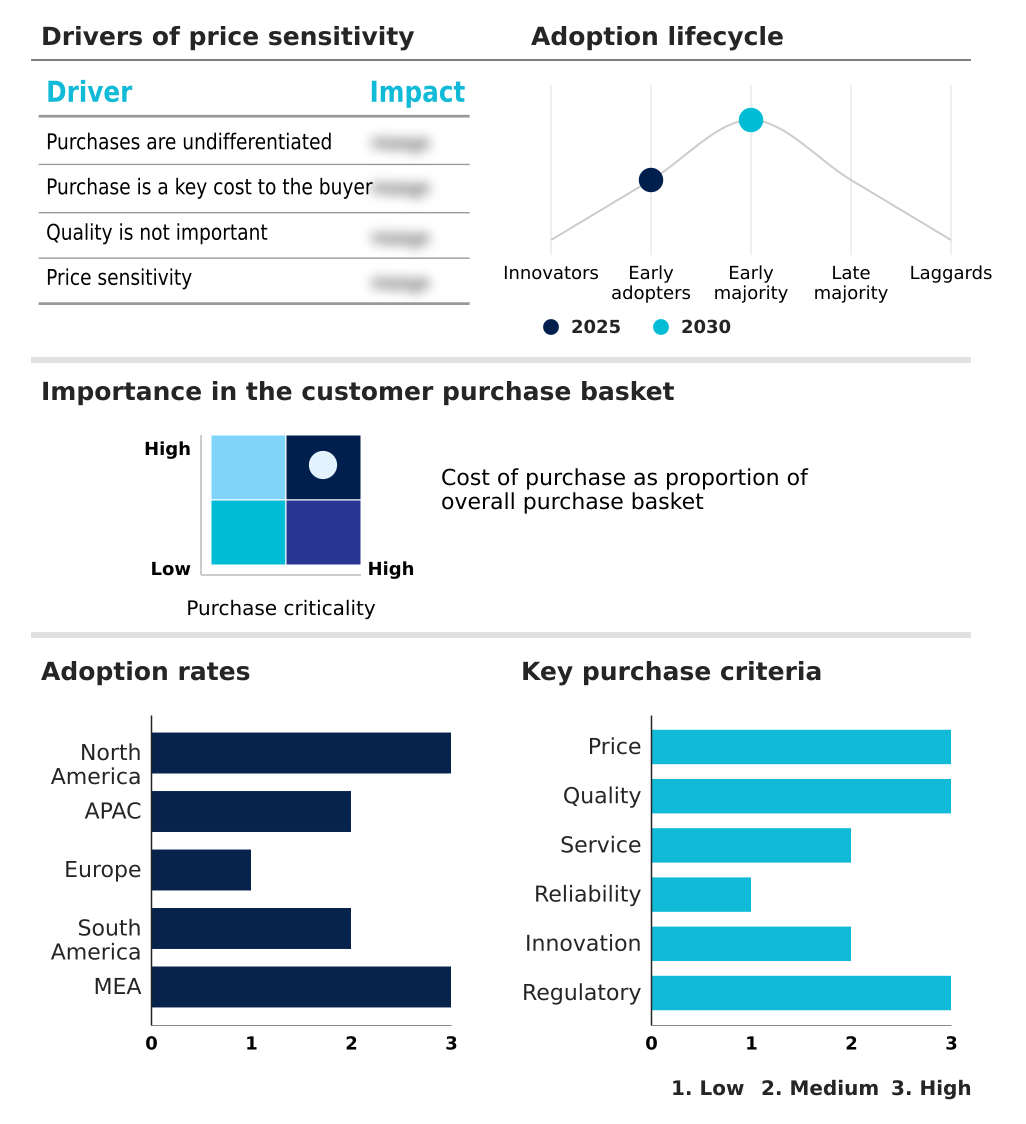

The thin film transistor (tft) liquid crystal display (lcd) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the thin film transistor (tft) liquid crystal display (lcd) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Thin Film Transistor (TFT) Liquid Crystal Display (LCD) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, thin film transistor (tft) liquid crystal display (lcd) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AUO Corp. - Specialized thin film transistor (TFT) liquid crystal display (LCD) modules are offered, focusing on robust panels engineered for demanding automotive and industrial applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AUO Corp.

- BOE Technology Group Co. Ltd.

- E Ink Holdings Inc.

- Fujitsu Ltd.

- Hannstar Display Corp.

- Hitachi Ltd.

- Japan Display Inc.

- LG Electronics Inc.

- Panasonic Holdings Corp.

- Samsung Electronics Co. Ltd.

- Sharp Corp.

- Shenzhen Wan Display Co. Ltd.

- Sony Group Corp.

- TCL Industries Holdings Ltd.

- Tianma Microelectronics Co.

- Toshiba Corp.

- Truly International Holdings

- Winstar Display Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Thin film transistor (tft) liquid crystal display (lcd) market

- In August, 2024, BMW Group unveiled a luxury sedan featuring a thirty-one-inch theater screen for rear-seat passengers, utilizing thin film transistor liquid crystal display technology to provide a premium entertainment experience.

- In December, 2024, Continental AG entered a partnership with several display companies to develop curved thin film transistor liquid crystal display units for integrated dashboard systems, focusing on improving cockpit ergonomics.

- In February, 2025, General Motors Company announced the inclusion of a pillar-to-pillar screen in its upcoming luxury electric SUV series, relying on the stability of thin film transistor liquid crystal display technology for critical information visibility.

- In May, 2025, Hyundai Motor Company reported the successful implementation of a new head-up display system that projects navigation data onto the windshield using a compact thin film transistor liquid crystal display.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Thin Film Transistor (TFT) Liquid Crystal Display (LCD) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 314 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.4% |

| Market growth 2026-2030 | USD 50561.2 thousand |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.1% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Thin Film Transistor (TFT) Liquid Crystal Display (LCD) Market remains relevant through continuous innovation in its core architecture, from the thin film transistor itself to the liquid crystal cells it controls. As an active switching device technology, its performance is being enhanced with advanced components like IGZO TFT panels and LTPS TFT panels, moving beyond traditional amorphous silicon.

- This evolution is critical as the market competes with self-emissive display technologies such as OLED and micro-LED. Boardroom decisions are increasingly influenced by the sustainability of the manufacturing process, which includes photolithography and the deposition process. The adoption of AI-driven inspection systems has proven effective, reducing panel defects significantly and directly impacting profitability.

- Innovations in the backlight unit, including mini-LED backlights and advanced color filters and polarizers, are improving performance metrics like contrast ratio, color gamut, and peak brightness. These enhancements, combined with higher refresh rates and faster response times, make modern TFT-LCDs suitable for demanding applications.

- The technology is adapting with developments like in-cell touch LCDs, curved display modules, and flexible LCD displays, ensuring its place in next-generation products from pillar to pillar screens in vehicles to high-resolution imaging devices.

What are the Key Data Covered in this Thin Film Transistor (TFT) Liquid Crystal Display (LCD) Market Research and Growth Report?

-

What is the expected growth of the Thin Film Transistor (TFT) Liquid Crystal Display (LCD) Market between 2026 and 2030?

-

USD 50.56 million, at a CAGR of 5.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Television, Mobile phones, Monitors, and Others), Type (Large displays, and Small and medium displays), End-user (Consumer electronics, Automotive, Retail and hospitality, Industrial, and Others) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing demand for high resolution large format displays in television sector, Intense competition from alternative display technologies

-

-

Who are the major players in the Thin Film Transistor (TFT) Liquid Crystal Display (LCD) Market?

-

AUO Corp., BOE Technology Group Co. Ltd., E Ink Holdings Inc., Fujitsu Ltd., Hannstar Display Corp., Hitachi Ltd., Japan Display Inc., LG Electronics Inc., Panasonic Holdings Corp., Samsung Electronics Co. Ltd., Sharp Corp., Shenzhen Wan Display Co. Ltd., Sony Group Corp., TCL Industries Holdings Ltd., Tianma Microelectronics Co., Toshiba Corp., Truly International Holdings and Winstar Display Co. Ltd.

-

Market Research Insights

- The market's dynamics are shaped by a strategic push toward smart manufacturing and application-specific product development. The integration of automated inspection systems has led to a significant reduction in pixel defects, while the use of advanced process control algorithms has improved production yields by as much as 12%.

- These efficiencies are critical for producing cost-effective consumer electronics and high-performance industrial TFT monitors. Demand is growing for ruggedized displays in industrial settings and advanced automotive infotainment displays featuring superior thermal stability and color accuracy.

- As companies focus on supply chain resilience, they are also navigating strict environmental compliance standards, driving innovation in energy efficiency and electronic waste recycling to meet global sustainability goals.

We can help! Our analysts can customize this thin film transistor (tft) liquid crystal display (lcd) market research report to meet your requirements.

RIA -

RIA -