Thermal Spray Materials Market Size 2024-2028

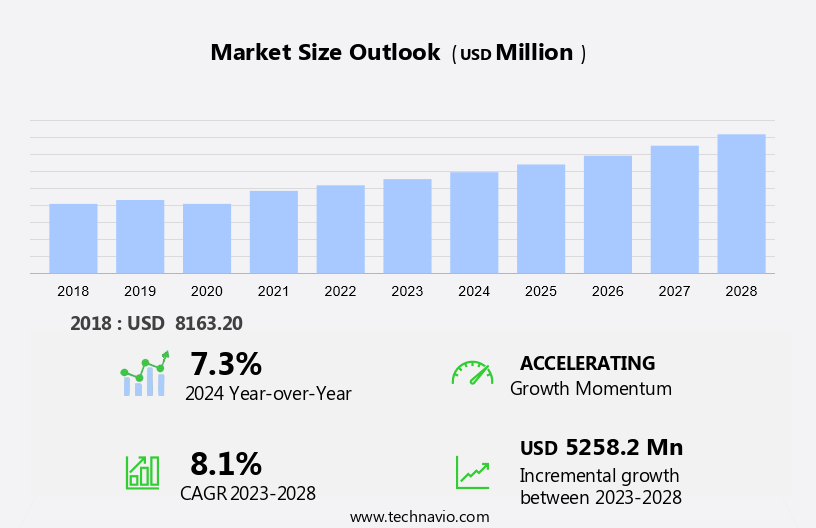

The thermal spray materials market size is forecast to increase by USD 5.26 billion at a CAGR of 8.1% between 2023 and 2028.

- The market exhibits significant growth due to increasing applications in various industries, including aerospace and the medical sector. In the aerospace industry, thermal spray coatings are utilized for their excellent corrosion resistance and high-temperature stability. In the medical industry, these coatings find extensive use in dental implants and orthopedic prosthetics for their low friction and chemical resistance properties. In the market, the increasing focus on occupational safety and infection control across numerous sectors, including healthcare and manufacturing, is driving the demand for thermal spray materials. However, the market faces challenges such as the volatility in raw material costs and availability. Moreover, advancements in technology, like cavitation, are revolutionizing the thermal spray process, offering improved coating quality and efficiency. These trends and challenges shape the market, making it an intriguing area for investment and innovation.

What will be the Size of the Market During the Forecast Period?

- The market encompasses a diverse range of advanced materials used for various coating applications. These materials are renowned for their exceptional properties, including heat resistance, corrosion protection, and abrasion resistance. The market's growth is driven by the increasing demand for surface modification and engineering materials in various industries. Heat resistance is a critical factor in numerous applications, particularly in high-temperature environments. Thermal spray materials, such as nickel plating and titanium coatings, offer excellent thermal stability, making them suitable for use in power generation, aerospace, and automotive industries. Corrosion protection is another essential attribute of thermal spray materials. These materials are used extensively in industries where equipment is exposed to harsh environments, such as the oil and gas sector. Polymer coatings and nanotechnology applications are popular choices due to their superior resistance to chemical and environmental corrosion. Surface characterization plays a significant role in the selection of thermal spray materials. Advanced materials, such as composite coatings and thin film coatings, are designed to enhance surface properties for specific applications.

- Biomaterial coatings are subjected to rigorous biocompatibility testing to ensure they meet the necessary safety and performance standards. Coating deposition technologies, such as hardfacing and coating design, are continually evolving to improve coating performance. These advancements enable the production of high-performance coatings with superior properties, including cavitation resistance, erosion resistance, and high friction. Thermal spray materials find extensive applications in various industries, including engineering materials, tribology, and industrial safety. In the field of material science, surface modification techniques using thermal spray materials are increasingly being used to enhance the properties of engineering materials. For example, nanotechnology coatings are being explored for their potential in enhancing the properties of fossil fuels in the energy sector. Additive manufacturing, a cutting-edge technology, is also driving the growth of the market.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

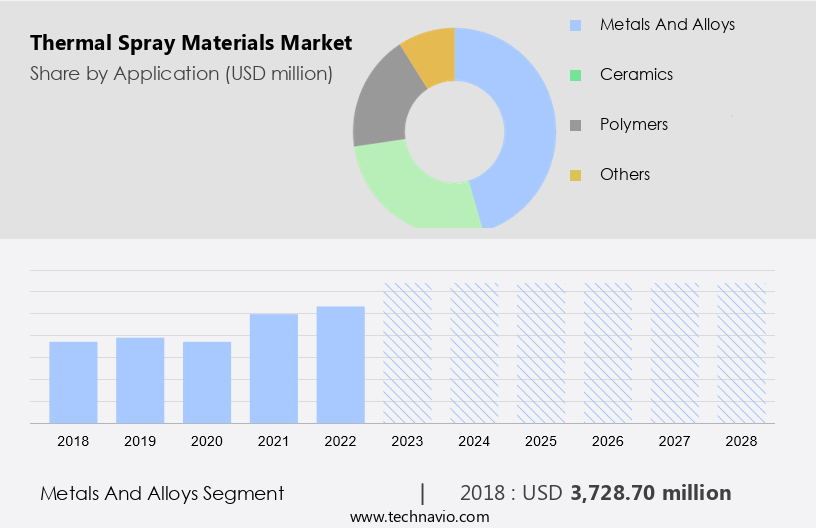

- Metals and alloys

- Ceramics

- Polymers

- Others

- Geography

- North America

- Canada

- US

- Europe

- Germany

- APAC

- China

- Japan

- South America

- Middle East and Africa

- North America

By Application Insights

- The metals and alloys segment is estimated to witness significant growth during the forecast period.

Thermal spraying is a surface coating technique that involves spraying metallic materials onto the surface of another substance. This process is extensively utilized to safeguard ferrous metals from corrosion and enhance the surface characteristics of objects for enhanced wear resistance and thermal conductivity. In the realm of thermal spray coating processes, pure metal alloy coatings are commonly employed, including zinc, bronze, stainless steel, titanium, and nichrome, as well as nickel-aluminum.

Further, the expanding utilization of these coatings in various industries, such as aerospace, automotive, and healthcare, is primarily driven by their ability to provide protection against high temperatures and oxidation, as well as their ease of application for repairing buildup. Consequently, the metals and alloys segment is poised for significant growth in the market during the forecast period.

Get a glance at the market report of share of various segments Request Free Sample

The metals and alloys segment was valued at USD 3.73 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

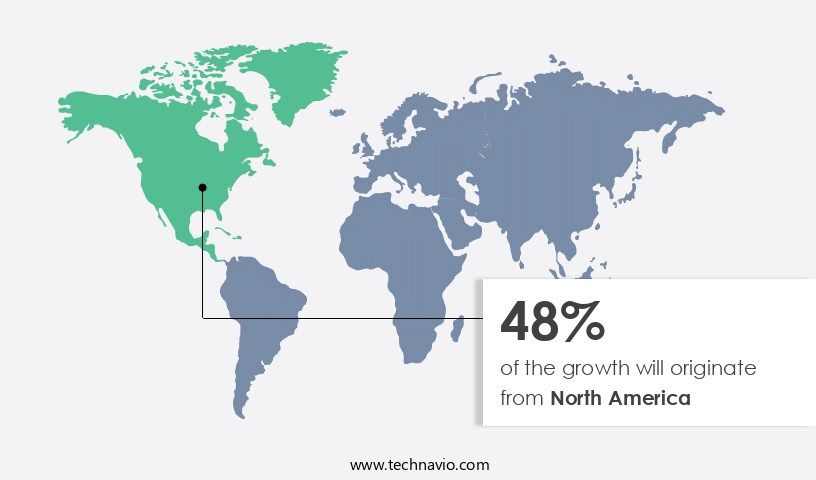

- North America is estimated to contribute 48% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

Thermal spray materials have gained significant importance in various industries due to their ability to provide effective surface coatings with exceptional properties. In the US, the increasing focus on occupational safety and infection control across numerous sectors, including healthcare and manufacturing, is driving the demand for thermal spray materials. These materials offer superior resistance to moisture, wear, and corrosion, making them ideal for coating medical implants and equipment. Moreover, the integration of antimicrobial properties in thermal spray coatings enhances their utility in infection control applications. The ceramics industry in North America, particularly in the US, is a major consumer of thermal spray materials due to its extensive use in aerospace applications.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Thermal Spray Materials Market ?

Increasing demand in aerospace industry is the key driver of the market.

- Thermal spray coatings play a crucial role in the aerospace industry for maintaining and restoring aircraft components, particularly in gas turbines. These coatings offer significant advantages, such as enhanced corrosion protection, resistance to contaminants, improved thermal efficiency, and reduced nitrogen oxide (NOx) emissions. They are applied to various jet engine components, including crankshafts, piston rings, cylinders, and valves, to increase their durability and longevity. In addition, thermal sprays are used to coat landing gear components, such as bearings and axles, to withstand the stresses during take-off and landing. Factors like metal-to-metal wear, hot corrosion, fretting, and particle erosion can lead to engine degradation.

- Personal protective equipment is essential when applying thermal sprays to ensure the safety of workers. In wind energy, thermal spray coatings are used for similar purposes in wind turbines, providing wear resistance and corrosion protection. Nanostructured coatings, such as nanoceramics, are gaining popularity due to their superior properties, including high hardness, wear resistance, and resistance to ultraviolet radiation. Abradable materials are also used in specific applications, such as seals and bushings, to minimize friction and wear. Thermal spray coatings are indispensable in various industries, ensuring optimal performance, safety, and cost savings.

What are the market trends shaping the Thermal Spray Materials Market?

Increasing application of thermal spray coatings in medical industry is the upcoming trend in the market.

- Thermal spraying is a widely utilized process in the medical industry for enhancing the properties of various medical devices. The primary applications include enhancing biocompatibility, improving corrosion resistance, and increasing surface roughness for better bonding with biological tissues. The US Food and Drug Administration (FDA) requires a pre-market evaluation for thermal spray coated medical products before they can be imported into the US. Several thermal spray methods and materials are employed for medical device coatings. Orthopedic devices, in particular, frequently use hydroxyapatite (HA) and plasma-sprayed titanium (Ti) coatings, as well as dual Ti/HA coatings. Metals, such as titanium alloys, cobalt-chrome alloys, and stainless steel alloys, and certain polymers, like polyether ketone, are commonly used as coating materials.

- Thermal spraying offers numerous advantages for medical devices. For instance, hydrophobic coatings can reduce bacterial adhesion, while anti-allergic coatings can improve patient safety. Erosion-resistant coatings can extend the life of prosthetic devices, and friction-reducing coatings can improve their functionality. Sacrificial wear coatings can protect the underlying material from wear and damage. The thermal spraying process involves heating a material to high temperatures and propelling it towards a substrate using a high-velocity gas stream. The coating forms a bond with the substrate upon impact, creating a strong, durable layer. Heat treatment is often used to enhance the coating's properties, such as increasing its hardness and improving its bond strength.

What challenges does Thermal Spray Materials Market face during the growth?

Volatility in raw material costs and availability is a key challenge affecting the market growth.

- The market faces volatility due to fluctuating costs and availability of key raw materials. The prices of metal powders and ceramics used in thermal spray coatings can be influenced by various factors, such as geopolitical tensions, trade restrictions, and shifts in supply and demand. For instance, disruptions in mining operations or production facilities can lead to shortages of essential components, causing manufacturers to either absorb increased costs or pass them on to customers, which may impact their competitiveness. Moreover, relying on specific suppliers for high-quality materials can create vulnerabilities in the supply chain, making it challenging for companies to maintain consistent production levels.

- In the context of the automotive industry, thermal spray materials are used to enhance sliding wear resistance in various components. Adherence to stringent regulations, including those related to volatile organic compounds (VOC) and carcinogenic substances, further complicates the market landscape. Hence, the above factors will impede the growth of the market during the forecast period.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast , partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market. The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alsher APM LLC

- AMETEK Inc.

- C and M Technologies GmbH

- Castolin GmbH

- CenterLine Holdings Inc.

- Compagnie de Saint-Gobain SA

- Flame Spray Technologies B.V.

- Global Tungsten and Powders Corp.

- Hardface Alloys Inc.

- HC Starck Tungsten GmbH

- Hoganas AB

- Kennametal Inc.

- Linde Plc

- Metallisation Ltd.

- OC Oerlikon Corp. AG

- Polymet Corp.

- Powder Alloy Corp.

- Praxair Inc.

- Sandvik AB

- Treibacher Industrie AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a wide range of materials used for surface treatment and coating applications. These materials offer various properties such as corrosion resistance, erosion protection, and wear resistance, making them ideal for numerous industries. In the medical sector, thermal spray coatings are utilized in the production of implantable devices, including dental implants and orthopedic prosthetics, due to their biocompatibility and antimicrobial properties. Ceramics, chromium, and nitride are popular thermal spray materials due to their high durability and chemical resistance. Chrome plating and hard chrome plating are commonly used for their low friction properties in various industries, including automotive and energy generation.

Further, nnanostructured coatings have gained significant attention due to their high abrasion resistance and ability to enhance the performance of equipment in extreme conditions. Thermal spray materials are also used in the production of personal protective equipment, anode making, and occupational safety equipment, providing protection against moisture, UV radiation, and other hazardous elements. In the field of energy generation, thermal spray coatings are used in gas turbines and wind turbines to improve their efficiency and durability. Thermal expansion, adhesion, and thermal expansion are crucial factors that need to be considered when selecting thermal spray materials. Substitutes for thermal spray materials include anodizing and weld overlay, but these methods may not offer the same level of properties and benefits as thermal spray coatings.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

169 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.1% |

|

Market growth 2024-2028 |

USD 5.26 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.3 |

|

Key countries |

US, China, Germany, Canada, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -