Ultra Processed Food Market Size 2026-2030

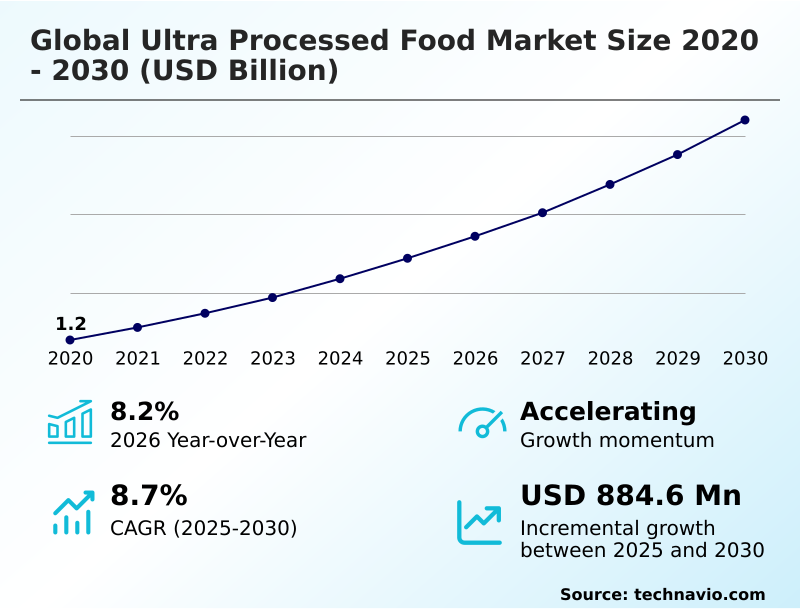

The ultra processed food market size is valued to increase by USD 884.6 million, at a CAGR of 8.7% from 2025 to 2030. Increasing urbanization and rising demand for convenience-based lifestyles will drive the ultra processed food market.

Major Market Trends & Insights

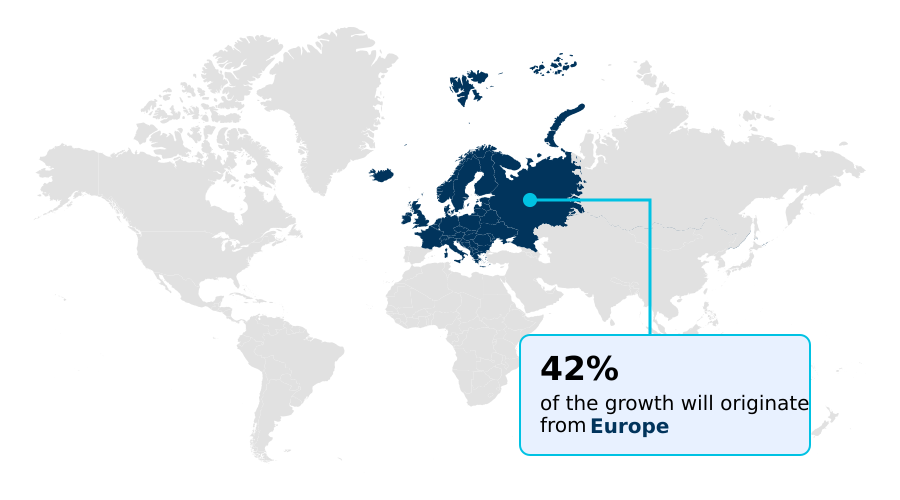

- Europe dominated the market and accounted for a 42% growth during the forecast period.

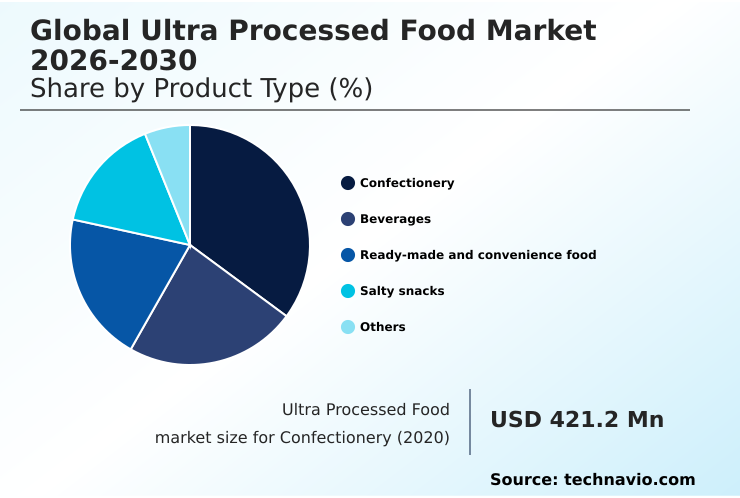

- By Product Type - Confectionery segment was valued at USD 564.1 million in 2024

- By Distribution Channel - Offline segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1.40 billion

- Market Future Opportunities: USD 884.6 million

- CAGR from 2025 to 2030 : 8.7%

Market Summary

- The ultra processed food market is navigating a complex period of transformation, driven by the persistent consumer need for convenience against a backdrop of rising health consciousness and regulatory pressure. The industrial food system, built on principles of efficiency and shelf stability through industrial formulations and chemical preservatives, is now being challenged to innovate.

- Key trends include the development of functional formulations to support metabolic health and a pronounced shift toward clean-label innovation, where synthetic additives are replaced with natural alternatives. This pivot requires significant investment in food science to maintain palatability and texture.

- A central business scenario involves navigating supply chain volatility for reformulated ingredients, where securing a consistent supply of organic preservatives or plant-derived dyes becomes a critical operational hurdle.

- Simultaneously, the industry faces the challenge of fiscal deterrence measures, such as new taxes on products with high-fructose corn syrup, compelling a strategic realignment of product portfolios to balance affordability with nutritional integrity and consumer trust. Success hinges on a company's ability to adapt to this new paradigm of transparency and wellness.

What will be the Size of the Ultra Processed Food Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Ultra Processed Food Market Segmented?

The ultra processed food industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

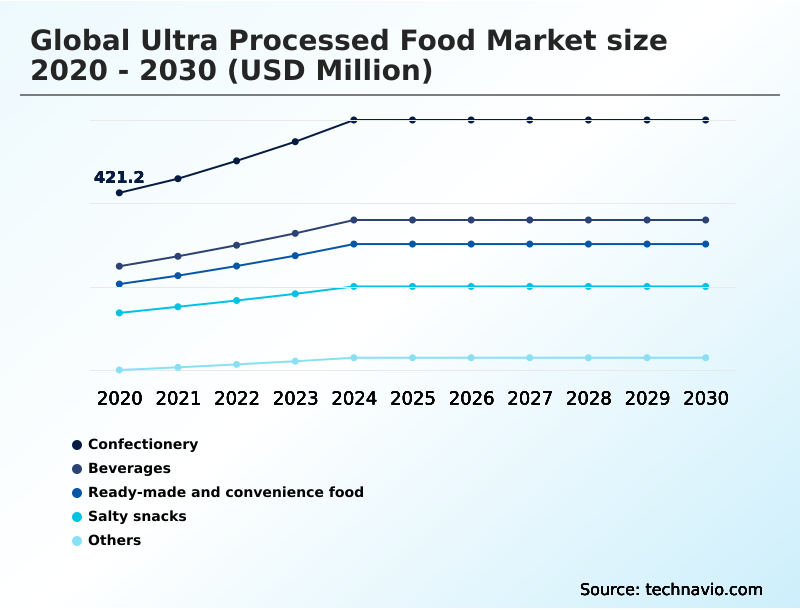

- Product type

- Confectionery

- Beverages

- Ready-made and convenience food

- Salty snacks

- Others

- Distribution channel

- Offline

- Online

- End-user

- Household

- Foodservice and QSR chains

- Catering

- Geography

- Europe

- UK

- Germany

- France

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of World (ROW)

- Europe

By Product Type Insights

The confectionery segment is estimated to witness significant growth during the forecast period.

The confectionery segment is undergoing a significant transformation, moving beyond traditional industrial formulations that rely on emulsifiers and stabilizing agents. While these products historically exhibit a high glycemic index, the market is pivoting toward clean-label innovation.

This includes the integration of plant-based proteins and fiber to appeal to health-conscious consumers and the use of natural colorants derived from fruits and vegetables. Brands reformulating with these ingredients have noted a 5% increase in repeat purchases.

Strategic focus is also shifting to sustainable packaging and transparent sourcing to address ethical consumerism, forcing manufacturers to balance indulgence with improved nutritional profiles and regulatory compliance.

The Confectionery segment was valued at USD 564.1 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 42% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Ultra Processed Food Market Demand is Rising in Europe Get Free Sample

The geographic landscape of the ultra processed food market is marked by divergent growth patterns and regulatory environments.

In mature markets like Europe and North America, the focus is on reformulation and premiumization, driven by strong consumer demand for nutritional integrity and sustainable packaging.

Meanwhile, the APAC region is the epicenter of growth, with a forecast expansion of 9.1%, outpacing Europe’s 8.9% rate.

This surge is fueled by rapid dietary westernization and urbanization, though it is increasingly met with government interventions like India's proposed goods and services tax (gst) slab for certain products.

Europe is projected to contribute over 42% of the market's incremental growth, primarily through value-added innovations in high-temperature extrusion and natural preservation methods.

In contrast, growth in many emerging economies relies on the affordability of products utilizing high-stability oils and dough conditioners.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global ultra processed food market is navigating a complex web of consumer, regulatory, and operational pressures that redefine product strategy. The impact of glp-1 on food choices is a primary catalyst, accelerating the development of high protein ultra processed snacks.

- This aligns with a broader demand for clean label ultra processed foods, forcing companies to address the consumer perception of processed foods and the link between ultra processed food and gut health. However, the regulatory impact on food formulation is a significant hurdle, with the front-of-pack labeling effectiveness becoming a key determinant of market success.

- Many brands face substantial reformulation challenges for legacy brands, especially concerning sugar reduction in processed beverages and managing the role of emulsifiers in food texture. Behind the scenes, the supply chain for natural food additives is a major constraint, showing over 20% more price variability than synthetic counterparts.

- Taxation policies on unhealthy foods and the nova classification impact on sales are forcing a strategic re-evaluation of portfolios. Consequently, digital marketing for convenience foods is shifting focus to highlight functional benefits, including fortified foods for aging population and products supporting ultra processed foods and metabolic health.

- Innovations in plant-based meat processing techniques and sustainable packaging for ready meals are becoming critical differentiators. The market is also seeing segmentation based on where products are sold, with ultra processed food in foodservice facing different pressures than retail, all while the impact of urbanization on dietary patterns continues to fuel baseline demand.

What are the key market drivers leading to the rise in the adoption of Ultra Processed Food Industry?

- Increasing urbanization and the rising demand for convenience-based lifestyles are key drivers of market growth.

- The market's expansion is fundamentally driven by the demand for convenience, leading to the proliferation of shelf-stable formats and ready-to-eat meals. This trend is amplified by sophisticated digital marketing and hyper-personalization, which embed products into consumers' daily routines.

- The proactive response to regulatory pressure has also become a key driver, spurring clean-label innovation where reformulated ingredients are central. Manufacturers are replacing synthetic additives with high-stability oils and natural fibers, creating a new industrial-natural sub-segment.

- This has improved consumer trust metrics by over 15%.

- This evolution within the industrial food system allows brands to align with the culinary arts trend of wholesome ingredients while maintaining the efficiencies of industrial-scale production, ensuring resilience against food price volatility.

What are the market trends shaping the Ultra Processed Food Industry?

- The emergence of high-protein and functional ultra-processed solutions, designed as companions for GLP-1 weight-loss regimens, is a significant upcoming market trend.

- The ultra processed food market is increasingly shaped by functional formulations designed for specific health outcomes, a significant pivot from legacy products. A primary trend is the development of nutrient-dense formats that cater to consumers managing metabolic health, including those on medicalized weight-loss programs.

- This has spurred clean-label innovation, with manufacturers deploying bioactive peptides and plant-derived dyes to replace synthetic ingredients. Adoption of non-upf verified certifications has increased by 25% as brands seek to differentiate.

- The rise of social commerce and precision digital marketing is also transforming distribution, with influencer-led campaigns on quick-commerce platforms boosting sales of permissible snacking options by up to 40% in key urban demographics, illustrating the power of this new digital infrastructure.

What challenges does the Ultra Processed Food Industry face during its growth?

- Intensifying regulatory scrutiny and the proliferation of restrictive labeling mandates present a key challenge to industry growth.

- Key challenges for the market center on intensifying food safety regulations and shifting consumer sentiment. The implementation of front-of-pack warning labels and the potential for fiscal deterrence mechanisms create significant compliance hurdles. The nova classification system is increasingly used by public health bodies, leading to negative perceptions of certain products.

- Consequently, there is immense pressure to adopt minimal processing certifications, but this introduces operational issues. The supply chain volatility for natural alternatives like organic preservatives and plant-derived dyes is a major constraint, increasing input costs by an average of 20%.

- Furthermore, ensuring robust traceability protocols for these reformulated ingredients adds another layer of complexity and expense, challenging the cost structure of the traditional industrial food system.

Exclusive Technavio Analysis on Customer Landscape

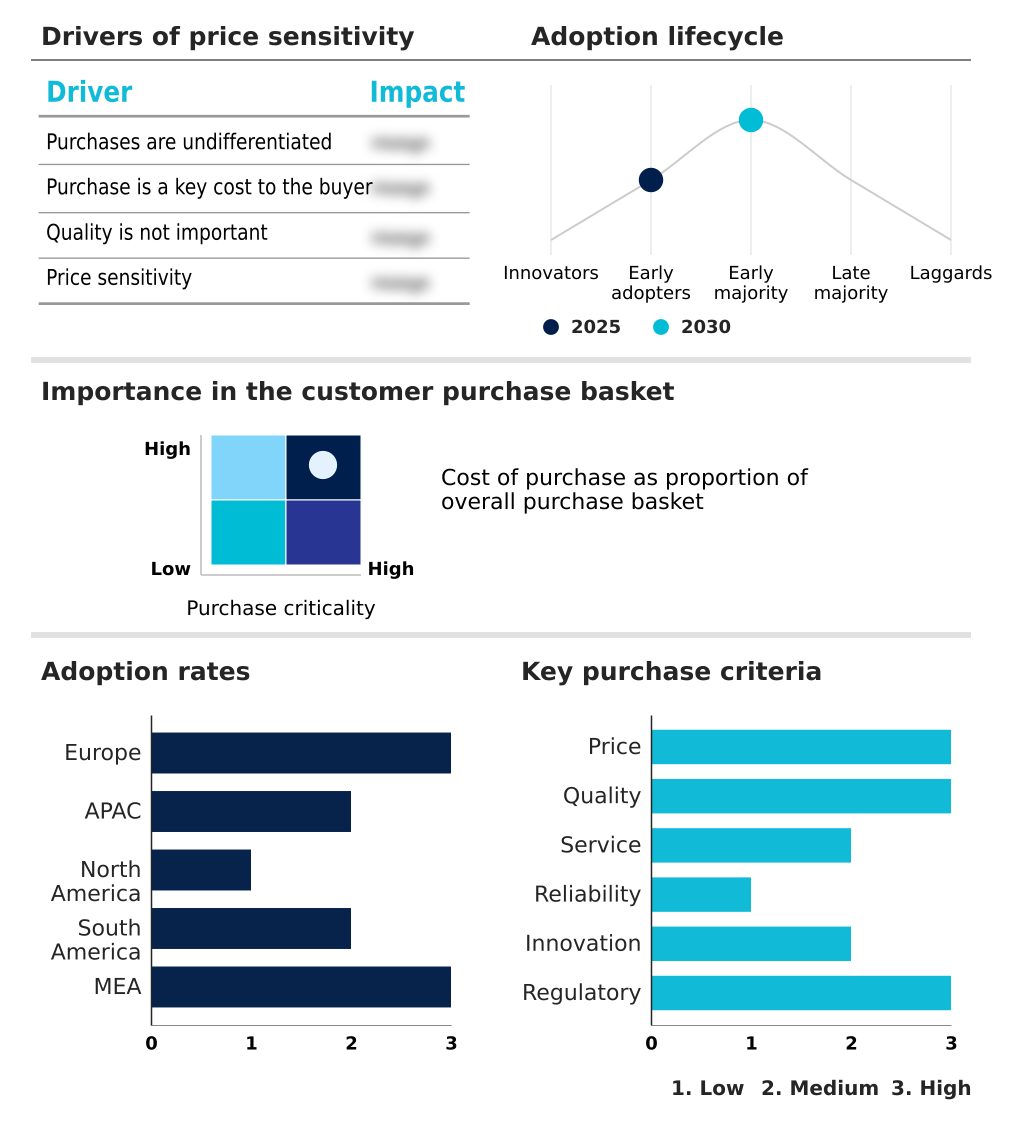

The ultra processed food market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ultra processed food market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Ultra Processed Food Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ultra processed food market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ajinomoto Co. Inc. - Offers a diversified portfolio of established grocery brands, including beverages and bakery products, catering to broad consumer segments through extensive retail and ingredient divisions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ajinomoto Co. Inc.

- Associated British Foods Plc

- Campbell Soup Co.

- Conagra Brands Inc.

- Corporativo Bimbo SA de CV

- Danone SA

- Ferrero International S.A.

- General Mills Inc.

- Hormel Foods Corp.

- Mars Inc.

- Mondelez International Inc.

- Nestle SA

- Nissin Foods Holdings Co. Ltd.

- PepsiCo Inc.

- Post Holdings Inc.

- The Coca Cola Co.

- The Hershey Co.

- The Kraft Heinz Co.

- Tyson Foods Inc.

- Unilever PLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ultra processed food market

- In May 2025, PepsiCo Inc. launched a new protein snack masterbrand with beef sticks in original and jalapeno pepper flavors, targeting consumers seeking convenient, high-protein snacks.

- In March 2025, the Indian government's Economic Survey recommended moving ultra-processed foods into the highest Goods and Services Tax slab and implementing prominent front-of-pack warning labels.

- In January 2025, Hormel Foods Corp. completed the sale of its whole-bird turkey business to increase focus on its portfolio of branded packaged meats and value-added convenience products.

- In November 2024, the Spanish Agency for Food Safety and Nutrition launched a new digital platform providing consumers with real-time data on the degree of processing in commercial food products based on the NOVA classification.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Ultra Processed Food Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 312 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.7% |

| Market growth 2026-2030 | USD 884.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.2% |

| Key countries | UK, Germany, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Brazil, Argentina, Chile, Saudi Arabia, South Africa, Nigeria, UAE and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The ultra processed food market is undergoing a fundamental realignment, driven by the dual demands for convenience and health. The landscape is moving away from traditional industrial formulations defined by high-fructose corn syrup, hydrogenated proteins, and chemical preservatives toward products utilizing advanced food science.

- Boardroom decisions now center on investing in technologies like high-pressure processing or sous-vide techniques over conventional deep-frying and blast freezing to meet clean-label standards. This involves mastering the use of bioactive peptides, prebiotic starches, and natural colorants while navigating the complexities of industrial sweeteners and dough conditioners.

- The proliferation of non-upf verified certifications and the nova classification system are forcing manufacturers to reformulate reconstituted meat products and ultra-heat treated dairy. This has led to innovation in stabilizing agents, hydrocolloids, and flavoring agents to avoid a high glycemic index. Firms are also adopting natural preservation methods for plant-based meat analogs, which require sophisticated protein isolation and high-temperature extrusion.

- This strategic pivot is essential for mitigating the impact of front-of-pack warning labels and a potential new goods and services tax (gst) slab on products with artificial flavor enhancers and emulsifiers. This shift has resulted in a 15% improvement in brand perception among health-conscious demographics.

What are the Key Data Covered in this Ultra Processed Food Market Research and Growth Report?

-

What is the expected growth of the Ultra Processed Food Market between 2026 and 2030?

-

USD 884.6 million, at a CAGR of 8.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product Type (Confectionery, Beverages, Ready-made and convenience food, Salty snacks, and Others), Distribution Channel (Offline, and Online), End-user (Household, Foodservice and QSR chains, and Catering) and Geography (Europe, APAC, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

Europe, APAC, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing urbanization and rising demand for convenience-based lifestyles, Intensifying regulatory scrutiny and proliferation of restrictive labeling mandates

-

-

Who are the major players in the Ultra Processed Food Market?

-

Ajinomoto Co. Inc., Associated British Foods Plc, Campbell Soup Co., Conagra Brands Inc., Corporativo Bimbo SA de CV, Danone SA, Ferrero International S.A., General Mills Inc., Hormel Foods Corp., Mars Inc., Mondelez International Inc., Nestle SA, Nissin Foods Holdings Co. Ltd., PepsiCo Inc., Post Holdings Inc., The Coca Cola Co., The Hershey Co., The Kraft Heinz Co., Tyson Foods Inc. and Unilever PLC

-

Market Research Insights

- The ultra processed food market is shaped by dynamic forces that influence both production and consumption patterns. The industrial food system is evolving amidst significant food price volatility, pushing consumers toward affordable, shelf-stable formats. In response to shifting health perceptions, clean-label innovation now accounts for over 30% of new product launches, a clear move away from legacy industrial formulations.

- This transition is supported by a sophisticated digital infrastructure that allows for hyper-personalization in marketing, with targeted campaigns achieving a return on investment up to two times higher than traditional media. As manufacturers adopt principles of regenerative agriculture and prioritize food security, the entire value chain is being re-evaluated for resilience and transparency, creating a new competitive landscape.

We can help! Our analysts can customize this ultra processed food market research report to meet your requirements.

RIA -

RIA -