US Organic Packaged Food Market Size 2024-2028

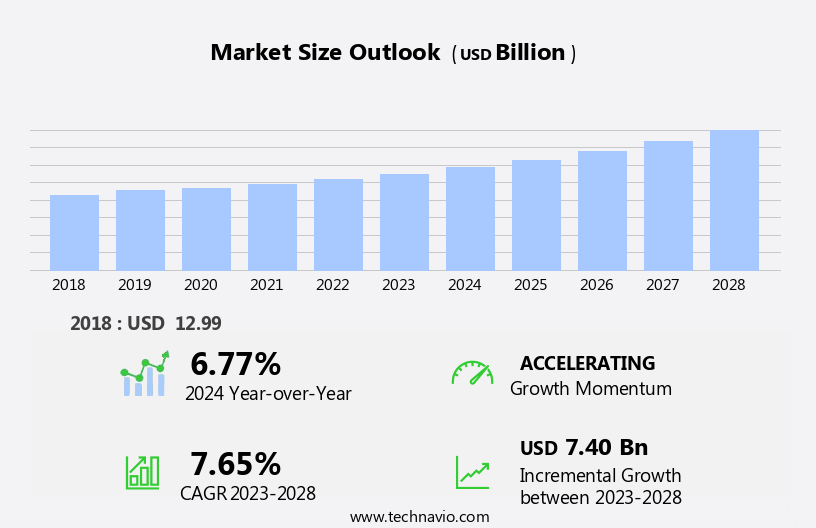

US organic packaged food market size is forecast to increase by USD 7.40 billion, at a CAGR of 7.65% between 2023 and 2028.

- The organic packaged food market in the US is booming, driven by conscious consumerism, rising demand for healthy eating, and a shift toward natural ingredients and non-GMO food. Consumers, including athletes, working women, and pets owners, seek organic snacks, organic treats, and gluten-free options to support a healthy lifestyle and weight loss goals.

- Trends in plant-based food, vegan food, and dairy-free food are influencing food innovation and food technology, with organic meal kits, subscription boxes, and grocery delivery gaining traction. Emphasis on sustainable packaging, eco-friendly bakery, and sustainable food aligns with ethics and the movement toward food safety. Meanwhile, social media, influencers, and online distribution drive food branding, food marketing, and corporate wellness, shaping modern food trends and recipes.

What will be the size of the US Organic Packaged Food Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

- The organic packaged food market is experiencing significant growth, with a focus on healthy options that cater to the demands of busy professionals and ethical consumers. Delivery services have become increasingly popular, offering taste benefits and convenience for those with limited time. Natural sweeteners and ingredients are prioritized, reflecting the trend towards clean eating and responsible consumption. Wholesale food distribution and food manufacturing have adapted to this shift, ensuring certification and ethical sourcing. Packaging plays a crucial role in food retail, with a focus on transparency and food labeling that accurately reflects organic and natural credentials.

- Research and development in food processing and marketing have led to an abundance of plant-based options, including organic confectionery , bakery products and vegan bakery products. Offline distribution channels, such as health food stores and organic grocery, continue to thrive, while online shopping and recipe sharing have expanded the market's reach. Festivals and events have become platforms for showcasing organic and natural food offerings, highlighting the availability and benefits of these options. Time-saving meals and workplace snacks have gained popularity, with a focus on reducing food waste and maintaining food quality. Restaurants have responded by offering organic and plant-based options, further expanding the market's scope. Overall, the organic packaged food market in the US is a dynamic and evolving industry, driven by consumer demand for healthy, natural, and ethically sourced options.

How is this market segmented?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Dairy bakery and confectionaries

- Meat seafood fruits and vegetables

- Sauces dressings condiments and spreads

- Others

- Packaging

- Flexible packaging

- Rigid packaging

- Paperboard packaging

- Metal packaging

- Distribution Channel

- Offline

- Online

- Supermarkets and Hypermarkets

- Specialty Stores

- Convenience Stores

- Consumer Segment

- Health-Conscious Consumers

- Vegans

- Vegetarians

- General Consumers

- Geography

- North America

- US

- North America

By Product Insights

The dairy bakery and confectionaries segment is estimated to witness significant growth during the forecast period.

In the dynamic organic packaged food market in the US, working-class professionals and urban consumers seek delicious, healthier alternatives to conventional food. General stores and supermarkets, as well as online platforms, cater to this demand, offering a wide array of organic food products. Organic farming practices, such as natural methods and the absence of synthetic pesticides and chemical fertilizer, are increasingly preferred. This is particularly true for produce, including vegetables, fruits, and even meat, as consumers prioritize health benefits and sustainability. Snacks, such as nutrition bars and organic chips, are popular choices for busy lifestyles. Organic sauces, dressings, and condiments add flavor to meals without the added concern of health-related disorders.

Boxed food, with its long shelf life and express delivery, is a convenient option for eco-conscious consumers seeking clear sourcing and natural food options. Organic certification ensures the absence of antibiotics, growth hormones, and irradiation. The organic packaged food market encompasses various product categories, including dairy products, bakery items, and organic beverages. Dairy products, such as milk, yogurt, cheese, and butter, are sourced from organically raised animals, ensuring animal welfare and the absence of synthetic additives. In the bakery sector, items like bread, pastries, cookies, and cakes are made from organic ingredients, contributing to the market's growth. Organic farming practices extend to fish and other seafood, as well as organic farm products, such as sauces, dressings, and condiments.

Sustainability and eco-consciousness are key selling points for these products, appealing to modern work-lifestyles and household chores. The market's unique selling proposition lies in its commitment to healthier, natural food options, catering to the diverse needs and preferences of consumers.

The Dairy bakery and confectionaries segment was valued at USD 7.41 billion in 2018 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the US Organic Packaged Food Market drivers leading to the rise in adoption of the Industry?

- ai_driver_intro

ai_driver_content_dynamics_gai.multili

What are the US Organic Packaged Food Market trends shaping the Industry?

- ai_trend_intro

ai_trends_content_dynamics_gai.multili

How does US Organic Packaged Food Market faces challenges face during its growth?

- ai_challenge_intro

ai_challenge_content_dynamic_gai.multili

Exclusive US Organic Packaged Food Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amys Kitchen Inc.

- Arla Foods amba

- Aurora Organic Dairy

- Barilla G. e R. Fratelli Spa

- Campbell Soup Co.

- Corporativo Bimbo SA de CV

- Danone

- DAVES KILLER BREAD

- Flowers Foods Inc.

- General Mills Inc.

- LT Foods Ltd.

- Nestle SA

- Organic Valley

- Perdue Farms Inc.

- The Hain Celestial Group Inc.

- The Hershey Co.

- Tyson Foods Inc.

- Hormel Foods Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Organic Packaged Food Market In US

ai_recent_development.aili

Research Analyst Overview

ai_research_analyst_overview.multip

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Organic Packaged Food Market in US insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

152 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.65% |

|

Market growth 2024-2028 |

USD 7.40 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.77 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across US

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -