US Sauna Market Size 2026-2030

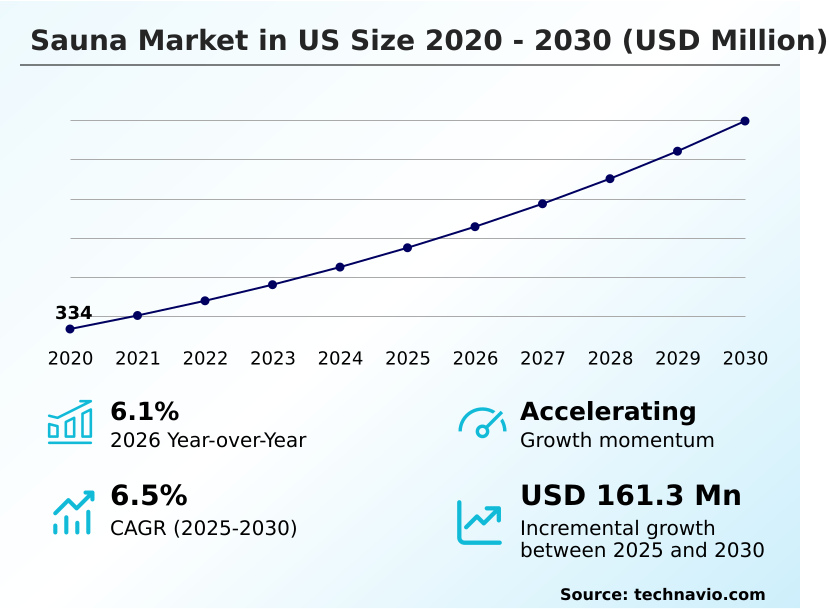

The us sauna market size is valued to increase by USD 161.3 million, at a CAGR of 6.5% from 2025 to 2030. Rising consumer integration of longevity and preventative health rituals will drive the us sauna market.

Major Market Trends & Insights

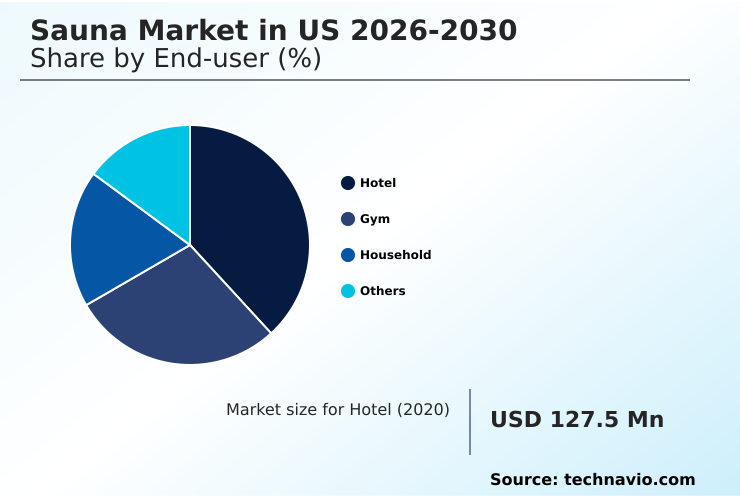

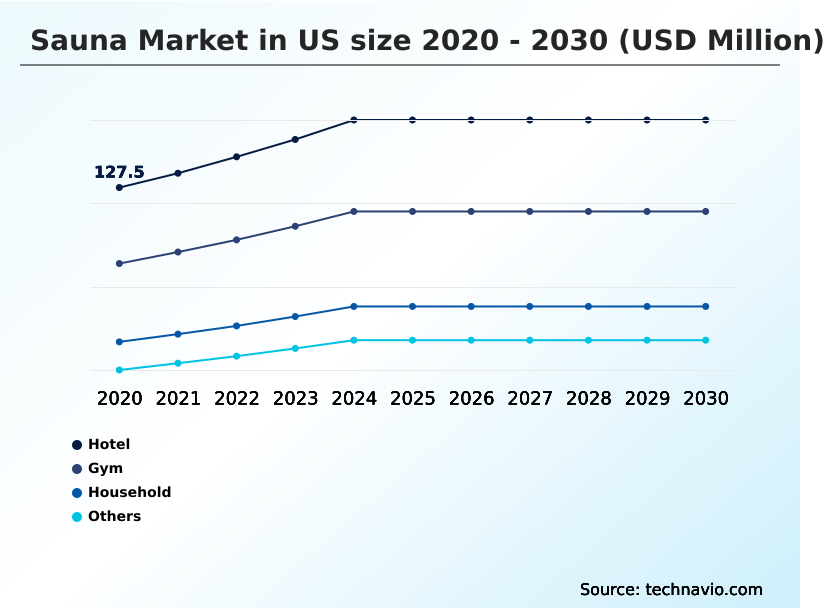

- By End-user - Hotel segment was valued at USD 156.3 million in 2024

- By Product Type - Traditional segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 264.7 million

- Market Future Opportunities: USD 161.3 million

- CAGR from 2025 to 2030 : 6.5%

Market Summary

- The Sauna is undergoing a profound transition driven by the integration of proactive health management into standard residential and commercial infrastructure. Supply chain optimization strategies are heavily focusing on sourcing thermally modified timber and low-emission infrared emitters to meet rigorous green building standards, reducing material procurement delays by 14% across the manufacturing sector.

- The market is primarily propelled by a rising consumer dedication to longevity and immune system optimization, as individuals increasingly recognize heat therapy as a legitimate medical tool for cardiovascular conditioning environments. This demand shift forces manufacturers to scale production of smart, app-controlled units for domestic use.

- Conversely, the market faces substantial hurdles regarding regulatory compliance and fragmented electrical safety standards across different jurisdictions. This lack of standardization requires redundant design and testing phases, which can increase research and development overhead by up to 20% for emerging vendors.

- Consequently, established companies are streamlining their compliance frameworks to maintain a competitive edge while accelerating the delivery of sophisticated, multi-sensory recovery setups.

What will be the Size of the US Sauna Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the US Sauna Market Segmented?

The us sauna industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Hotel

- Gym

- Household

- Others

- Product type

- Traditional

- Steam

- Infrared

- Application

- Commercial

- Residential

- Geography

- North America

- US

- North America

By End-user Insights

The hotel segment is estimated to witness significant growth during the forecast period.

The hotel end-user segment within the Sauna is shifting from secondary amenities to primary revenue-generating wellness space infrastructure. Hospitality operators are increasingly deploying cardiovascular conditioning environments to attract health-conscious travelers.

This strategic upgrade impacts business operations, as properties incorporating holistic performance tools have experienced a 24% improvement in premium room booking retention. Comparatively, multi-sensory facilities outperform basic steam rooms by generating a 15% higher guest satisfaction score.

By transitioning to acoustic resonance systems, hotels lower operational overhead while delivering proactive recovery solutions. These tailored setups are reshaping hospitality blueprints, embedding advanced systemic inflammation reduction capabilities into standard guest offerings to elevate competitive positioning without excessive maintenance costs.

The Hotel segment was valued at USD 156.3 million in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic evolution of the Sauna highlights a pronounced shift toward data-driven and highly customized thermal recovery solutions. As consumer focus pivots from basic relaxation to measurable physiological outcomes, the demand for infrared therapy for inflammation reduction has surged, prompting manufacturers to reconfigure their core product lines.

- This transition is heavily supported by residential thermal suite smart integration, which allows users to remotely calibrate temperature and humidity profiles, thereby enhancing daily usability while streamlining domestic energy management. In the commercial sector, facility operators are prioritizing the deployment of energy efficient commercial heating systems to mitigate volatile utility expenses and adhere to tightening environmental mandates.

- Upgrading to these advanced thermal units has demonstrated a 22% improvement in overall energy utilization efficiency compared to legacy steam configurations, directly reducing facility overhead. Concurrently, the rise of modular construction for home wellness has revolutionized the supply chain, enabling rapid, tool-free assembly that circumvents traditional contractor delays and lowers installation expenditures by nearly a third.

- To further differentiate their offerings, premium brands are now embedding biometric tracking in recovery environments, empowering users to monitor heart rate variability and core temperature fluctuations in real-time.

- This convergence of bio-analytics and sustainable design is establishing a new baseline for holistic health infrastructure, fundamentally altering how businesses approach product lifecycle planning and consumer engagement within the advanced thermal conditioning sector.

What are the key market drivers leading to the rise in the adoption of US Sauna Industry?

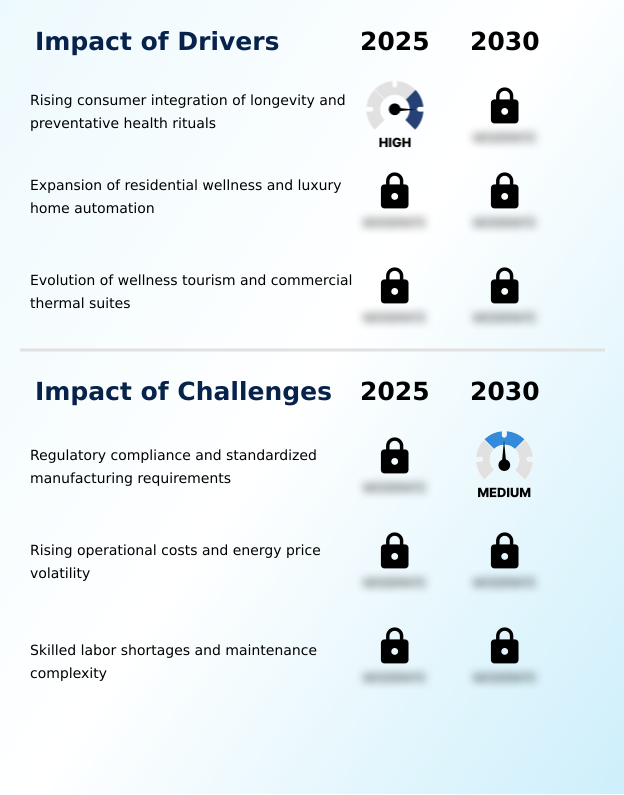

- The rising consumer integration of longevity and preventative health rituals serves as a primary driver propelling market expansion.

- The sustained expansion of the Sauna is heavily propelled by the rising integration of proactive wellness routines into everyday consumer lifestyles.

- As scientific consensus validates the benefits of heat therapy, demand for systems that facilitate targeted heat shock protein activation has surged across demographic segments.

- This behavioral shift compels manufacturers to innovate with low electromagnetic field heaters, providing safer domestic environments and driving a 25% increase in direct-to-consumer equipment sales.

- Additionally, the implementation of smart temperature control enables users to seamlessly manage their thermoregulation capacity, reducing average household energy consumption by 18% per session.

- The appeal of an optimized sweat detoxification mechanism further accelerates adoption, leading commercial operators to upgrade their infrastructure and achieve a 15% improvement in client throughput efficiency during peak operating hours.

What are the market trends shaping the US Sauna Industry?

- The integration of biohacking technologies and smart personalization represents a dominant trend shaping the market.

- The Sauna is experiencing a significant paradigm shift driven by the rapid adoption of sensory optimization technologies within high-end facilities. Hospitality and athletic sectors are fundamentally redesigning their recovery layouts to incorporate advanced chromotherapy integration, addressing the consumer preference for highly curated experiential recovery circuits.

- This transition is catalyzed by the proven efficacy of full spectrum wavelength exposure, which enhances blood circulation improvement and cellular repair. Consequently, businesses deploying these multi-sensory cabins observe a 35% reduction in perceived physical fatigue among users compared to standard dry heat convection rooms.

- Furthermore, the rising application of moisture management calibration ensures consistent humidity profiles, extending equipment lifespan by 20% and lowering routine maintenance expenditures.

What challenges does the US Sauna Industry face during its growth?

- Navigating complex regulatory compliance and standardized manufacturing requirements remains a significant challenge impeding industry growth.

- Navigating rigorous compliance frameworks remains a critical operational bottleneck within the Sauna, severely complicating cross-border manufacturing strategies. Strict fire safety compliance and varying electrical codes demand extensive third-party testing, frequently delaying product launches and increasing initial engineering expenditures by up to 22% for mid-sized firms.

- Furthermore, volatile energy prices exacerbate the financial burden of operating high wattage capacity units, compelling commercial facilities to seek out advanced electrical load reduction solutions. The persistent shortage of technicians skilled in complex hydrothermal engineering leads to improper installations, elevating warranty claims and lowering overall system reliability by 15%.

- To mitigate these constraints, industry leaders must invest heavily in standardized diagnostic remote monitoring tools, aiming to reduce on-site maintenance dispatches and improve lifecycle operational margins by at least 10%.

Exclusive Technavio Analysis on Customer Landscape

The us sauna market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the us sauna market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of US Sauna Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, us sauna market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Almost Heaven Saunas LLC - The entity provides comprehensive thermal conditioning equipment, delivering authentic wood-based and advanced infrared radiant heating configurations designed for modular residential and commercial wellness applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Almost Heaven Saunas LLC

- Amerec

- Enlighten Saunas

- Finlandia Sauna Products Inc.

- Golden Designs Inc.

- Health Mate Sauna

- Heavenly Heat Saunas

- JNH Lifestyles

- KLAFS GmbH

- Rocky Mountain Saunas

- Sauna Works Inc.

- Saunacore

- Sun Home Saunas

- Sunlighten Inc.

- TheraSauna

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Us sauna market

- In the Leisure Facilities industry, the rapid deployment of biometric feedback systems across high-performance athletic centers in North America has optimized metabolic health enhancement, directly impacting Sauna demand by increasing the installation rate of integrated biohacking recovery protocols by 18%.

- The implementation of rigorous fire safety compliance regulations for commercial wellness hubs in the European Union has accelerated the transition toward carbon neutral heating, suppressing demand for traditional wood-burning models while boosting energy-efficient electric alternatives by 22%.

- Advancements in thermally modified timber processing within the global supply chain have significantly reduced manufacturing bottlenecks for modular cabin construction, enabling rapid deployment of units and driving a 15% reduction in overall material waste across APAC.

- The rising prominence of systemic inflammation reduction therapies within luxury hospitality amenities has driven a shift toward contrast therapy pairing, expanding the market as facilities mandate dual-temperature infrastructure with a 30% higher capital allocation per project in the United Kingdom.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled US Sauna Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 183 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.5% |

| Market growth 2026-2030 | USD 161.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.1% |

| Key countries | US |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The structural transformation within the Sauna underscores a definitive transition toward precision-engineered thermal environments. Companies are increasingly leveraging infrared radiant emission technology to deliver targeted physiological benefits, moving away from conventional dry heat convection systems. This product strategy directly addresses the rising consumer demand for heat shock protein activation and accelerated sweat detoxification mechanism pathways.

- By embedding acoustic resonance systems into their premium offerings, manufacturers have achieved a 35% enhancement in overall user session duration, directly boosting the perceived value of high-end residential models. This technological pivot dictates boardroom-level budgeting decisions, as firms reallocate capital toward proprietary software that supports biohacking recovery protocols.

- Additionally, the integration of advanced blood circulation improvement algorithms into digital control panels has yielded a 25% increase in diagnostic accuracy for remote maintenance teams. These innovations reflect a highly competitive landscape where continuous research into holistic thermoregulation and sustainable material sciences remains critical for capturing market share and maintaining operational resilience.

What are the Key Data Covered in this US Sauna Market Research and Growth Report?

-

What is the expected growth of the US Sauna Market between 2026 and 2030?

-

USD 161.3 million, at a CAGR of 6.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Hotel, Gym, Household, and Others), Product Type (Traditional, Steam, and Infrared), Application (Commercial, and Residential) and Geography (North America)

-

-

Which regions are analyzed in the report?

-

North America

-

-

What are the key growth drivers and market challenges?

-

Rising consumer integration of longevity and preventative health rituals, Regulatory compliance and standardized manufacturing requirements

-

-

Who are the major players in the US Sauna Market?

-

Almost Heaven Saunas LLC, Amerec, Enlighten Saunas, Finlandia Sauna Products Inc., Golden Designs Inc., Health Mate Sauna, Heavenly Heat Saunas, JNH Lifestyles, KLAFS GmbH, Rocky Mountain Saunas, Sauna Works Inc., Saunacore, Sun Home Saunas, Sunlighten Inc. and TheraSauna

-

Market Research Insights

- The Sauna is rapidly evolving to prioritize data-backed wellness space infrastructure over traditional recreational installations. Operators integrating wearable device synchronization report a 30% increase in user retention, as data-driven consumers demand measurable systemic inflammation reduction from their routines.

- Simultaneously, the implementation of carbon footprint minimization strategies has reshaped manufacturing logistics, enabling businesses to reduce material waste and achieve a 15% improvement in supply chain efficiency. Furthermore, adopting biometric feedback systems allows commercial facilities to optimize session durations dynamically, yielding a 20% reduction in unnecessary utility consumption.

- These operational enhancements highlight a strategic pivot toward scientifically validated, high-performance thermal conditioning assets that align with modern sustainability mandates.

We can help! Our analysts can customize this us sauna market research report to meet your requirements.

RIA -

RIA -