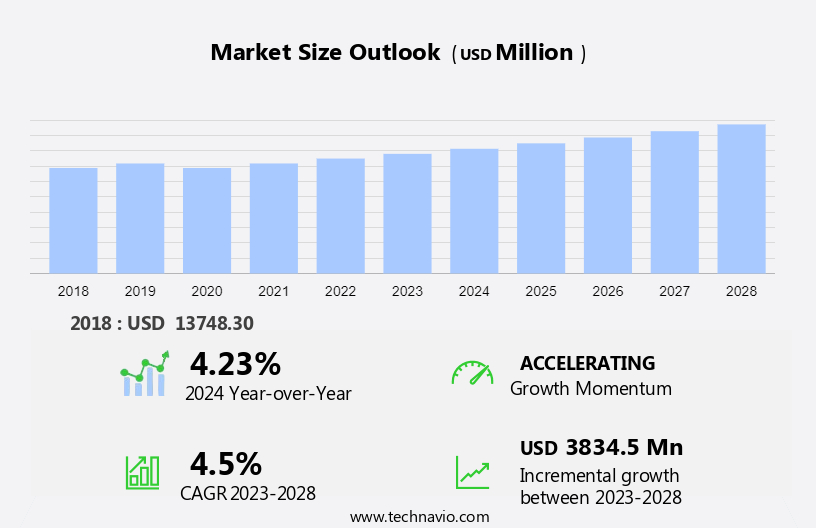

Wine Logistics Market Size 2024-2028

The wine logistics market size is estimated to grow by USD 3.83 billion at a CAGR of 4.5% between 2023 and 2028. The market is experiencing significant growth, driven by increasing demand in key markets such as China. According to the International Organisation of Vine and Wine, China is now the largest importer of wine in the world, with bulk shipments accounting for a significant portion of its imports. This trend is expected to continue as Chinese consumers show a growing appreciation for wine culture and sophistication. The global wine trade is responding to this demand by offering larger volumes at competitive prices. These factors make the global wine market an attractive proposition for producers, traders, and investors alike.

What will be the Size of the Market During the Forecast Period?

For More Highlights About this Report, Request Free Sample

Market Dynamic and Customer Landscape

The market is a crucial segment of the global wine industry, focusing on the transportation, storage, and distribution of grapes and wine from wineries to mass supplier and consumers. Temperature and moisture control are essential factors in wine logistics to maintain the quality of the product. Transit methods like conveyance vault and containers ensure the safe conveyance of wine, adhering to stringent temperature and moisture standards. Automation plays a significant role in wine logistics through logistics automations such as RFID, GPS, and barcoding for efficient transport management and inventory control. Winemakers, premium wine producers, and e-commerce platforms rely on these technologies to streamline supply chain operations and ensure timely delivery of their products. Wine logistics caters to various types of wines, including sparkling and fortified wines, and handles the wholesale distribution and online distribution channels. Wine growers and mass suppliers benefit from the convenience and cost-effectiveness offered by the market, enabling them to reach a broader consumer base and expand their businesses. Voice guided container collecting arrangement enhance course chain efficiency through organic and inorganic expansion procedures. Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Key Market Driver

Rising demand for wine in China is notably driving market growth. The global wine industry has experienced significant growth, particularly in China, where consumption has risen substantially since 2011. This increase in demand is expected to drive the need for efficient wine logistics solutions in the country. China's expanding wine production, currently ranking it among the top ten wine-producing economies worldwide, is insufficient to meet its growing consumption. Consequently, imports from key contributing countries like France and South Africa have surged since 2010. These imports primarily consist of full container loads and less than container loads, necessitating advanced logistics solutions for transit, temperature, and moisture control.

Furthermore, Wine producers and winery owners require adherence to stringent standards for their valuable products during conveyance in containers and vino repositories, often high bay warehouses. Logistics automations, such as transport management and inventory control systems, are essential to ensure the timely and secure delivery of red wine, white wine, rosé wine, fruit wine, sparkling wine, and fortified wine. The e-commerce boom and wholesale distribution channels further complicate supply chain operations, making logistics service providers indispensable. Bulk shipping via flexitank technology and ISO vessels is another trend gaining popularity in the industry for transporting crude oil and other combustible materials. The use of barcoding and advanced technology in wine logistics enhances the overall efficiency and value-added services for winemakers and premium wine suppliers. Thus, such factors are driving the growth of the market during the forecast period.

Significant Market Trends

Growing online wine retailing is the key trend in the market. The global wine industry is experiencing a significant shift towards online distribution channels, driven by the demand for fast delivery services and competitive pricing. This trend is particularly prominent in the wine logistics market, where the focus is on ensuring the safe and efficient transit of grapes and wine products. Temperature and moisture control are crucial considerations in wine logistics, with standards strictly adhered to by wineries, wine growers, and mass suppliers. Logistics automations, such as conveyance vaults and high bay warehouses, are increasingly being adopted to streamline transportation and warehousing processes. Value-added services, including barcoding and inventory control, are also essential to maintain the quality of red wine, white wine, rose wine, fruit wine, sparkling wine, and fortified wine during the supply chain operations.

Furthermore, flexitank technology and bulk shipping in ISO vessels are used for the transportation of large quantities of wine, making it an economical option for winemakers producing premium wines. Logistics service providers play a vital role in managing transportation, inventory control, and ensuring the safe handling of combustible materials like wine. The growing e-commerce sector and online distribution channels are expanding the reach of small and local wineries, making their products available to a global audience. The wine logistics market is expected to witness continued growth, with an increasing focus on automation, temperature control, and value-added services to meet the demands of consumers and wine producers alike. The transportation and warehousing of wine require specialized expertise and infrastructure, making it a complex and dynamic industry. Thus, such trends will shape the growth of the market during the forecast period.

Major Market Challenge

Volatile fuel prices is the major challenge that affects the growth of the market. The market is influenced by various factors, including transit and storage conditions for temperature-sensitive wine products. Wine growers and wineries rely on logistics automations and value-added services to ensure the safe and efficient transportation and warehousing of grape harvest and finished wines, such as red, white, rose, fruit wines, sparkling, and fortified varieties. Logistics service providers utilize high bay warehouses, conveyance vaults, and containers to maintain optimal temperature and moisture levels during transit and storage. Flexitank technology and bulk shipping via ISO vessels are also employed for the transportation of wine, particularly for mass suppliers and wholesale distribution channels.

However, volatility in fuel prices, driven by crude oil prices, poses a significant challenge to the market. An increase in fuel costs leads to higher freight charges, which can negatively impact the profitability of winemakers and logistics providers in the global wine industry. Additionally, the emergence of e-commerce and online distribution channels necessitates advanced transport management and inventory control systems to ensure efficient and timely delivery to consumers. Barcoding and other technology solutions are essential for effective supply chain operations and ensuring the authenticity and quality of premium wines. Hence, the above factors will impede the growth of the market during the forecast period

Key Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

CTI Logistics Ltd.- The company offers wine storage and Temperature Controlled Storage services for Perth and Western Australia.

The market research and growth report also includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- CTI Logistics Ltd.

- CWT Pte. Ltd.

- DB Schenker

- Deutsche Post AG

- Gordon Logistics

- GPC Logistics

- Hellmann Worldwide Logistics SE and Co KG

- Kane Logistics

- KAN-HAUL

- Kerry Logistics Network Ltd.

- Kuehne Nagel Management AG

- Portavin Integrated Wine Services

- RS Express

- TIBA

- Vintage Road Haulage

- Wine Logistics International BVBA

- Wine Storage and Logistics Pty Ltd.

- WineCare Logistics Inc.

- Wineshipping LLC.

- Ziegler Group Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Segmentation

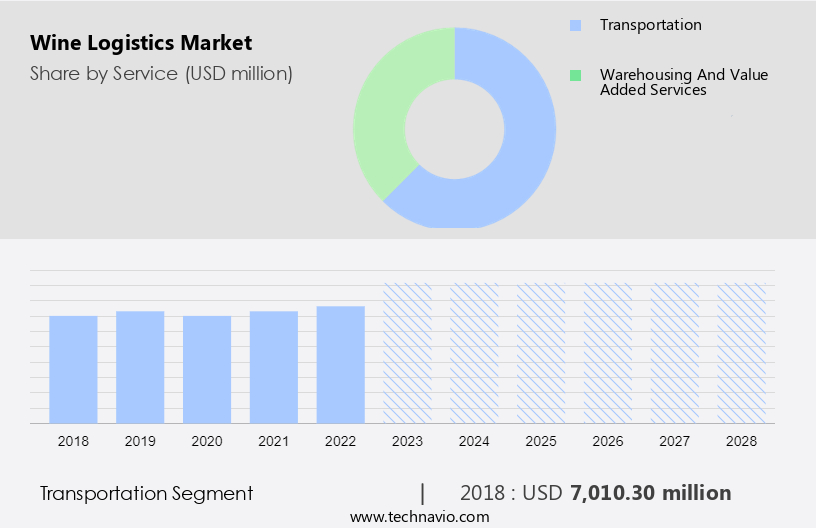

By Service

The market share growth of the Transportation segment will be significant during the forecast period. The wine logistics market encompasses the transit, temperature, and moisture control of grapes and wine from wineries to supermarkets, on-trade establishments, and convenience stores. Temperature and moisture standards are crucial in ensuring the quality of red wine, white wine, rose wine, fruit wine, sparkling wine, and fortified wine during conveyance.

Get a glance at the market share of various regions Download the PDF Sample

The transportation segment was the largest and was valued at USD 7.01 billion in 2018. Vino repositories, such as high bay warehouses, employ logistics automations and automation for efficient inventory control and value-added services. Roadway logistics service providers play a significant role in this sector, as supermarkets, on-trade sales, and convenience stores are the primary retail sales channels for wine. In the US, supermarkets account for a substantial share of wine sales. The on-trade sales channel is projected to expand rapidly in developing countries due to evolving consumer preferences. In this distribution channel, wineries, grape wine growers, mass suppliers, and wine producers collaborate with logistics service providers to ensure the safe and timely delivery of wine. Bulk shipping via flexitank technology and ISO vessels is common for mass wine suppliers, while premium wines are often transported in specialized containers. Transport management systems and inventory control are essential for optimizing supply chain operations in the wine industry. E-commerce and online distribution channels have also emerged as significant growth drivers in the global wine industry. Barcoding and other technologies facilitate efficient tracking and traceability throughout the wine logistics process. The wine logistics market requires adherence to stringent regulations due to the combustible nature of wine, which is similar to crude oil. Therefore, it is essential to collaborate with experienced logistics service providers to ensure the safe and efficient handling of wine.

By Region

For more insights on the market share of various regions Download PDF Sample now!

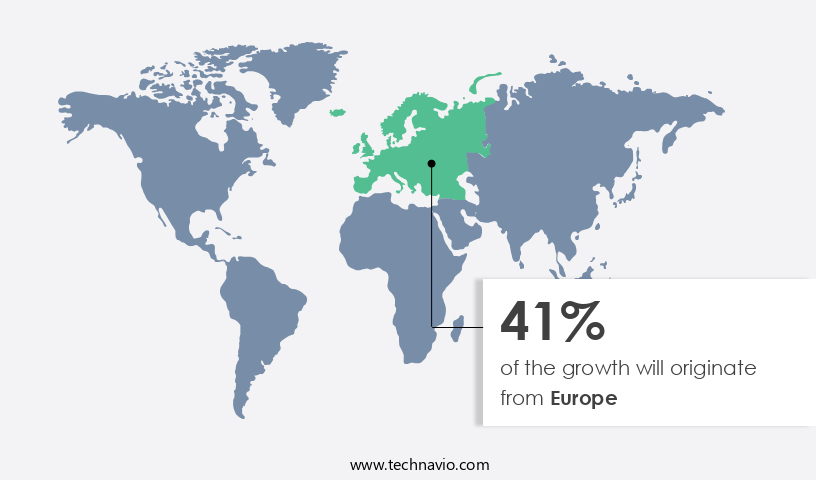

Europe is estimated to contribute 41% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market encompasses the transit, storage, and value-added services involved in moving grapes from wineries to consumers. Temperature and moisture control are crucial during transit to preserve the quality of the wine. Wine growers and producers rely on logistics automations and conveyance vaults to ensure the safe transport of containers filled with red wine, white wine, rose wine, fruit wine, and other varieties. Flexitank technology and bulk shipping via ISO vessels are used for transporting large quantities of wine, while adhering to the standards for handling combustible materials. Transport management and inventory control are essential components of the wine supply chain operations. Winemakers rely on logistics service providers to ensure the timely delivery of premium wines to mass suppliers, wholesalers, and e-commerce platforms. The global wine industry leverages technology such as barcoding and transportation and warehousing solutions to streamline operations. Additionally, logistics providers offer value-added services such as temperature-controlled warehousing in high bay vino repositories for storing and aging sparkling wine, fortified wine, and other specialty wines.

Segment Overview

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion " for the period 2024-2028, as well as historical data from 2018 - 2022 for the following segments.

- Service Outlook

- Transportation

- Warehousing and value added services

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- The U.K.

- Germany

- France

- Rest of Europe

- APAC

- China

- India

- Middle East & Africa

- Saudi Arabia

- South Africa

- Rest of the Middle East & Africa

- South America

- Argentina

- Brazil

- Chile

- North America

You may also interested in below market reports:

-

India Wine Market: India Wine Market by Type and Product - Forecast and Analysis

-

Wine Market: Wine Market Analysis Europe, APAC, North America, South America, Middle East and Africa - US, China, Germany, Canada, France - Size and Forecast

-

Wine E-commerce Market: Wine E-commerce Market Analysis Europe,North America,APAC,South America,Middle East and Africa - US,China,France,UK,Italy - Size and Forecast

Market Analyst Overview

The global wine industry has seen significant growth in recent years, leading to an increased focus on efficient and effective wine logistics. Wine producers and winery owners require reliable transit and warehousing solutions to ensure the quality of their products during transportation and storage. Temperature and moisture control are crucial factors in wine logistics. Wine is a perishable commodity, and exposure to extreme temperatures or moisture can negatively impact its quality. Winemakers rely on specialized logistics solutions, such as conveyance vaults and high bay vino repositories, to maintain the ideal conditions for different types of wine, including red, white, rose, fruit, sparkling, and fortified varieties.

Furthermore, Logistics automation plays a vital role in the wine industry. Automation in transportation and inventory control helps wineries and mass suppliers manage their supply chain operations more efficiently. Flexitank technology and bulk shipping in ISO vessels are popular options for transporting large quantities of wine, while combustible material regulations ensure safe transportation of wine. Value-added services, such as barcoding and e commerce integration, have become essential for wine logistics providers. Winery partnerships with logistics service providers offer transportation management, inventory control, and online distribution channel, enabling winemakers to reach a broader market and premium wine consumers.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

141 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.5% |

|

Market growth 2024-2028 |

USD 3.83 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.23 |

|

Regional analysis |

Europe, North America, APAC, South America, and Middle East and Africa |

|

Performing market contribution |

Europe at 41% |

|

Key countries |

US, Germany, France, UK, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

CTI Logistics Ltd., CWT Pte. Ltd., DB Schenker, Deutsche Post AG, Gordon Logistics, GPC Logistics, Hellmann Worldwide Logistics SE and Co KG, Kane Logistics, KAN-HAUL, Kerry Logistics Network Ltd., Kuehne Nagel Management AG, Portavin Integrated Wine Services, RS Express, TIBA, Vintage Road Haulage, Wine Logistics International BVBA, Wine Storage and Logistics Pty Ltd., WineCare Logistics Inc., Wineshipping LLC., and Ziegler Group Corp. |

|

Market dynamics |

Parent market analysis, Market Forecasting, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for market forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across Europe, North America, APAC, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

RIA -

RIA -