Wood Pellets Market Size 2026-2030

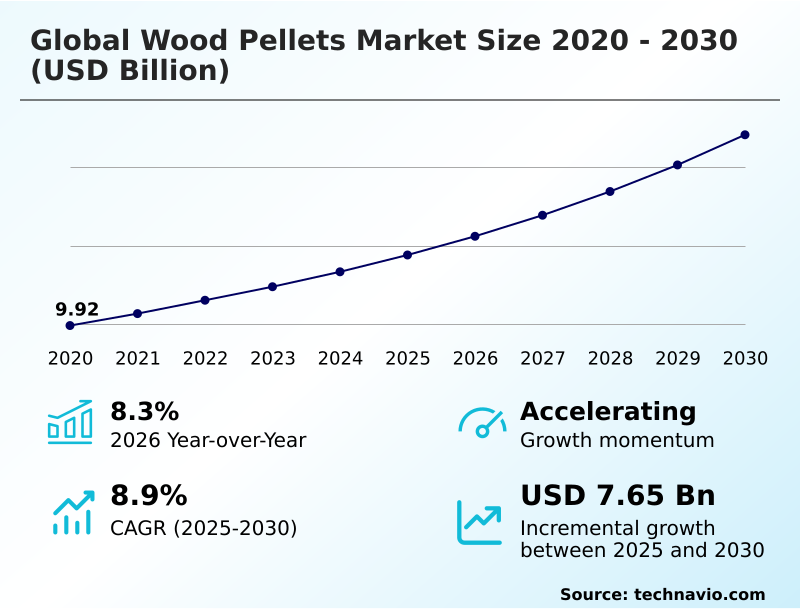

The wood pellets market size is valued to increase by USD 7.65 billion, at a CAGR of 8.9% from 2025 to 2030. Decarbonization mandates and industrialization of utility-scale biomass conversion will drive the wood pellets market.

Major Market Trends & Insights

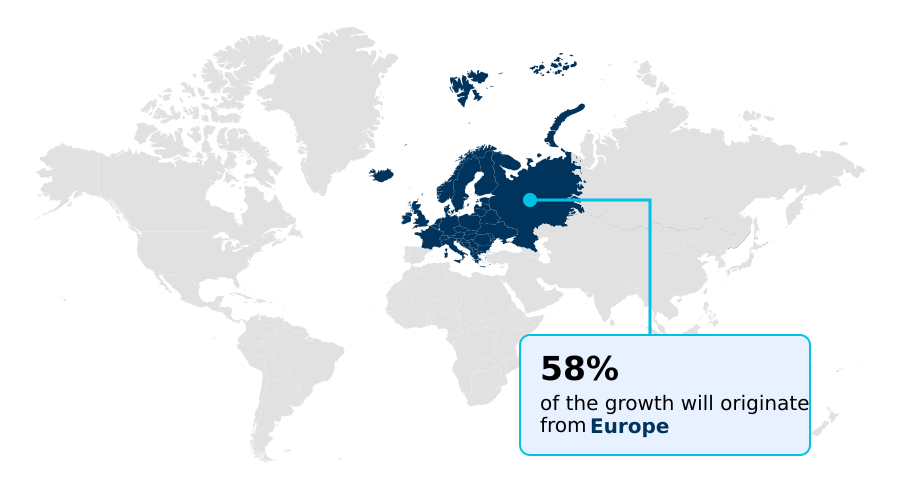

- Europe dominated the market and accounted for a 58.3% growth during the forecast period.

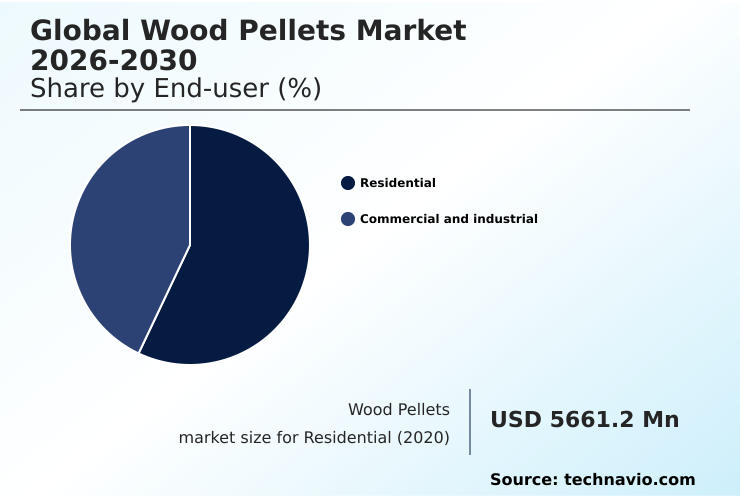

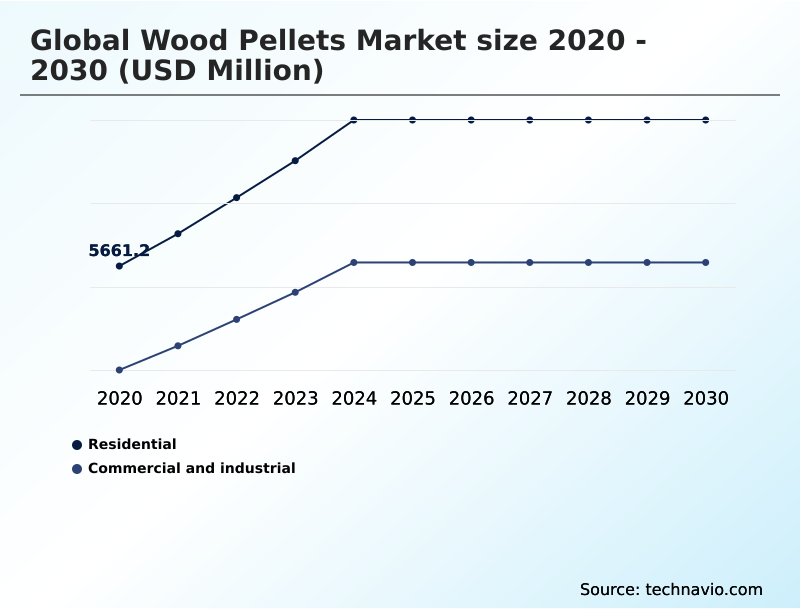

- By End-user - Residential segment was valued at USD 7.63 billion in 2024

- By Application - Power generation segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 12.13 billion

- Market Future Opportunities: USD 7.65 billion

- CAGR from 2025 to 2030 : 8.9%

Market Summary

- The wood pellets market is undergoing a structural expansion, becoming a critical component of the international renewable energy matrix. This growth is driven by a global mandate for carbon neutrality, which has positioned densified biomass as a versatile, low-carbon alternative for utility-scale power generation and industrial combined heat and power sectors.

- A key business scenario involves utilities retrofitting legacy coal assets to use industrial wood pellets, a strategy that leverages existing infrastructure to reduce capital expenditure while meeting stringent emissions targets. This transition necessitates a resilient supply chain focused on sustainable sourcing and feedstock diversification, incorporating agricultural residues and purpose-grown energy crops.

- The industry is also seeing a move toward transparency and sustainability certification, with advanced tracking technologies ensuring provenance and addressing environmental concerns. In emerging economies, government incentives are accelerating the development of domestic manufacturing, reducing reliance on imported energy and establishing biomass as a foundational element for future decarbonization efforts in sectors like aviation and maritime transport.

What will be the Size of the Wood Pellets Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Wood Pellets Market Segmented?

The wood pellets industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Residential

- Commercial and industrial

- Application

- Power generation

- Combined heat and power

- Heating

- Grade type

- Utility grade

- Standard grade

- Premium grade

- Geography

- Europe

- UK

- Germany

- France

- North America

- US

- Canada

- Mexico

- APAC

- Japan

- China

- South Korea

- Middle East and Africa

- Turkey

- South Africa

- Saudi Arabia

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- Europe

By End-user Insights

The residential segment is estimated to witness significant growth during the forecast period.

The residential segment is a critical pillar for the market, driven by demand for sustainable residential heating solutions that offer energy security and autonomy.

Homeowners are incentivized by renewable heating incentives to adopt modern biomass boiler systems, leading to the displacement of fossil fuels.

This trend is supported by a preference for premium grade pellets meeting ENplus A1 certification standards, which guarantee a low ash content fuel and high calorific value biomass.

The convenience of these systems is enhanced by features like automated ash removal, which, combined with the use of low moisture biofuel, ensures efficient operation and contributes to air quality improvement by reducing particulate emissions.

In some key European markets, this segment now accounts for over 50% of total volume consumption, highlighting its role in the clean energy transition.

The Residential segment was valued at USD 7.63 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 58.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Wood Pellets Market Demand is Rising in Europe Get Free Sample

The global geographic landscape is dominated by Europe, which accounts for over 58% of total consumption, driven by mandates like the renewable energy directive III that promote renewable thermal energy.

In contrast, APAC is the fastest-expanding region, with growth outpacing North America by nearly 0.4 percentage points, fueled by demand for carbon-neutral industrial fuel in Japan and South Korea.

South America is emerging as a critical supplier, leveraging its expertise in biomass densification process to produce high-density biomass fuel for export.

Across regions, there is a growing use of biomass gasification technology to produce syngas from wood pellets for combined heat and power (CHP) applications and to support district heating networks.

The natural binding properties of lignin are essential for producing durable standard grade pellets, facilitating rural electrification support and the growth of a global bio-based economy.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the global wood pellets market is increasingly complex, shaped by a confluence of economic, regulatory, and technological factors. Businesses must evaluate the cost of coal-to-biomass conversion against the long-term benefits of using a carbon-neutral fuel source.

- A key consideration is the efficiency of torrefied wood pellets, as the difference between black pellets vs white pellets can significantly alter operational outcomes. The challenges of EUDR compliance are forcing a re-evaluation of supply chains, with a new focus on geospatial tracking for feedstock to ensure transparency.

- Simultaneously, the potential for BECCS for negative carbon emissions is creating new value streams, as adopting these frameworks can improve carbon credit monetization by over 20% compared to standard biomass combustion. Residential pellet stove efficiency and the availability of ENplus certification for residential use remain critical for the consumer segment, which requires automating residential biomass heating systems.

- On the supply side, feedstock competition with the pulp industry and the logistics of transoceanic pellet shipping influence pricing. As the market diversifies, the viability of using agricultural residue for pellets and designing multi-feedstock pellet plant designs becomes paramount.

- Understanding the impact of subsidy removal on biomass and the overall carbon footprint of wood pellets is essential for assessing the utility-scale biomass plant economics. Furthermore, the role of biomass for sustainable aviation fuel is an emerging frontier, dependent on the fuel requirements of CHP plants and the use of advanced drying for low moisture content.

What are the key market drivers leading to the rise in the adoption of Wood Pellets Industry?

- Decarbonization mandates, coupled with the industrialization of utility-scale biomass conversion, are key drivers of market growth.

- Market growth is fundamentally driven by the global decarbonization of power generation and the push for industrial boiler retrofitting.

- The industrialization of coal-to-biomass conversion is accelerating, with utilities utilizing industrial wood pellets and utility-grade biomass fuel for co-firing in power plants.

- These initiatives are supported by biomass co-firing mandates and the need to comply with frameworks like the EU green deal.

- This transition to base-load renewable power is made possible by a robust sustainable sourcing infrastructure and advanced drying technologies that ensure pulverized fuel compatibility.

- New densification lines for industrial process heat are projected to add over twelve million metric tons of incremental capacity, expanding feedstock sources by more than 10% in key production zones.

- In the residential sector, government subsidies are accelerating adoption, leading to a 30% reduction in payback periods for household energy upgrades in some areas.

What are the market trends shaping the Wood Pellets Industry?

- The institutionalization of torrefaction technology is a key market trend. This is leading to the increased adoption of high-density black pellets with superior energy properties.

- Key market trends are redefining the bioenergy value chain through advanced biofuel development and a focus on a circular bio-based economy. The institutionalization of torrefaction technology is central to this shift, with black pellets production using thermal-chemical conversion to create hydrophobic biomass fuel. This is driving a 9% higher adoption rate in industrial applications seeking high-performance alternatives to coal.

- Concurrently, the expansion of bioenergy carbon capture storage (BECCS) frameworks is positioning biomass as a negative emissions technology, enabling carbon credit monetization. Furthermore, the diversification into multi-feedstock processing, including agricultural residue pelletization, is expanding the feedstock base significantly.

- This integration of sustainable agriculture could account for up to 14% of the total bioenergy supply, creating new waste-to-energy solutions and enhancing supply chain resilience.

What challenges does the Wood Pellets Industry face during its growth?

- A key challenge affecting industry growth is the regulatory compliance and technical complexity associated with international deforestation standards.

- Navigating market challenges requires managing regulatory complexities and supply chain pressures to build a resilient energy infrastructure. The implementation of EU deforestation regulation compliance demands rigorous geospatial feedstock tracking and carbon intensity verification, increasing operational expenditures by up to 15% for some exporters and disrupting the biomass supply chain logistics.

- Concurrently, feedstock scarcity is intensified by competition for sawdust and wood chips from other industries, impacting pellet mill extrusion operations and highlighting the importance of sustainable forest management and forest residue utilization.

- The potential retraction of subsidies, such as the review of renewable energy certificate weighting, threatens the economic viability of new projects, potentially impacting over 40% of planned capacity expansions in certain APAC markets. This uncertainty affects commercial biomass heating and efforts to ensure grid stability with biomass.

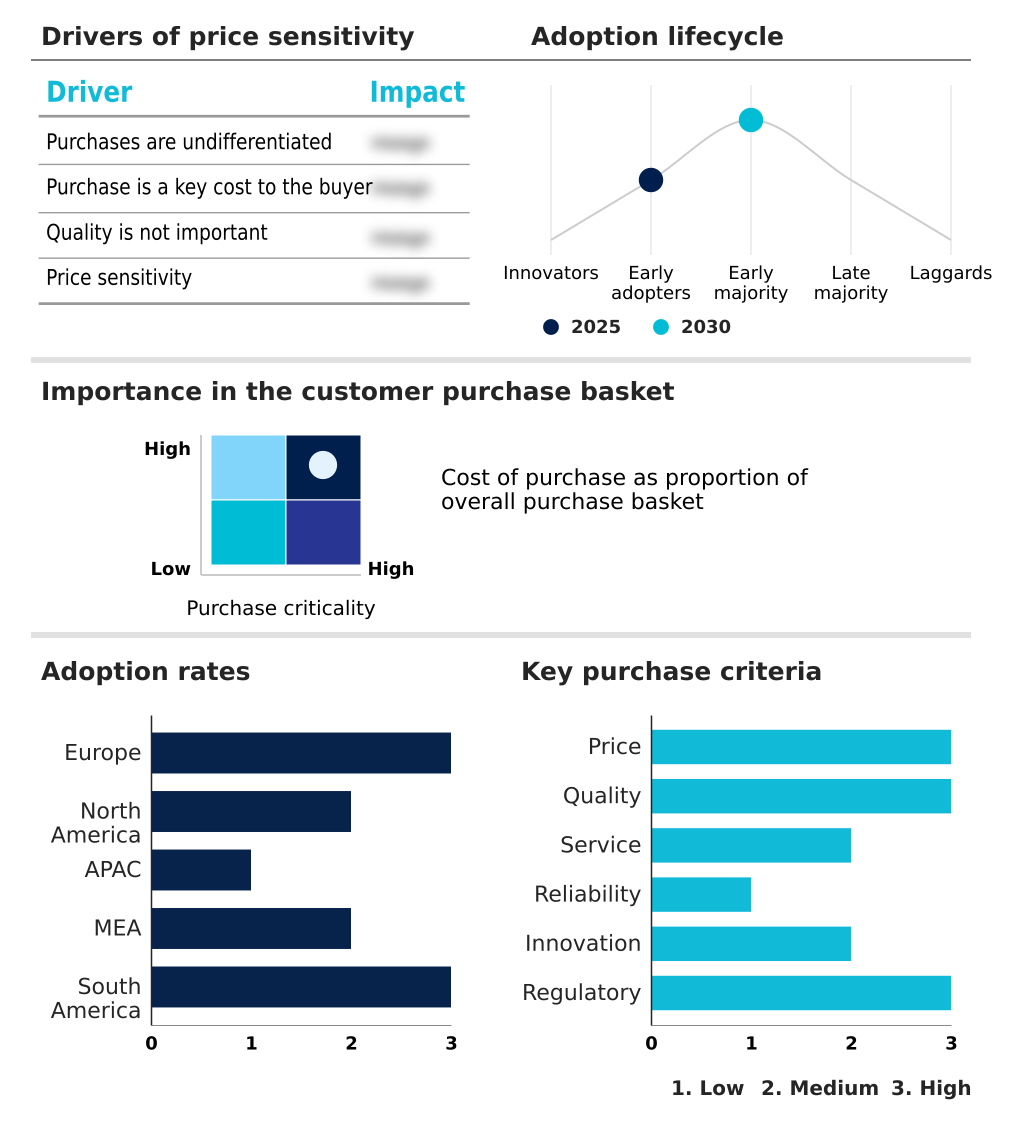

Exclusive Technavio Analysis on Customer Landscape

The wood pellets market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the wood pellets market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Wood Pellets Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, wood pellets market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AS Graanul Invest - Focuses on sustainably sourced biomass fuels, enabling large-scale production of industrial and premium pellets for the global sustainable energy transition.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AS Graanul Invest

- Binderholz GmbH

- Bio Eneco

- BioPower Sustainable Energy

- BrasPine Madeiras Ltda

- CT Pellet

- ECARE

- Energy Pellets of America

- Enviva Inc.

- Highland Pellets LLC

- JP Green Fuels

- Land Energy Girvan Ltd.

- Lignetics Inc.

- Pfeifer Holding GmbH

- PREMIUM PELLETS sro

- PRODESA

- SNOW ENTITIES

- VIRIDIS ENERGY INC.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Wood pellets market

- In December 2024, Enviva Inc. confirmed its strategic focus on completing new production facilities after emerging from financial restructuring, aiming to enhance the supply of industrial and residential pellets.

- In February 2025, the government of South Korea initiated a formal review of Renewable Energy Certificate (REC) weightings for biomass co-firing, creating significant uncertainty for exporters targeting this key APAC market.

- In October 2024, PowerWood Canada Corp. finalized a multi-million-dollar agreement to construct two specialized black pellet facilities in Alberta, designed to convert wildfire-damaged timber into high-density torrefied pellets for export.

- In September 2024, several North American exporters suspended certain industrial-grade pellet shipments to European utilities due to persistent ambiguities in the new EU Deforestation Regulation (EUDR) geolocation requirements.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Wood Pellets Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 283 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.9% |

| Market growth 2026-2030 | USD 7648.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.3% |

| Key countries | UK, Germany, France, Italy, The Netherlands, Spain, US, Canada, Mexico, Japan, China, South Korea, India, Indonesia, Australia, Turkey, South Africa, Saudi Arabia, UAE, Israel, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's evolution is defined by a sophisticated interplay of technology and regulation. The core biomass densification process relies on pellet mill extrusion and advanced drying technologies to produce a low moisture biofuel.

- Products range from industrial wood pellets for co-firing in power plants, requiring pulverized fuel compatibility, to premium grade pellets with low ash content fuel for residential biomass boiler systems featuring automated ash removal. Key standards include ENplus A1 certification and compliance with the renewable energy directive III.

- The rise of torrefied wood pellets, also known as black pellets production, involves a thermal-chemical conversion to create a hydrophobic biomass fuel with high calorific value biomass and high-density biomass fuel characteristics. Advanced applications include biomass gasification technology to create syngas from wood pellets and bioenergy carbon capture storage, a negative emissions technology.

- Sustainable sourcing infrastructure is critical, with an emphasis on sustainable forest management, geospatial feedstock tracking, and carbon intensity verification to meet EU deforestation regulation compliance. Diversification is occurring through agricultural residue pelletization, multi-feedstock processing, and energy crop cultivation to meet biomass co-firing mandates and evolving renewable energy certificate weighting.

What are the Key Data Covered in this Wood Pellets Market Research and Growth Report?

-

What is the expected growth of the Wood Pellets Market between 2026 and 2030?

-

USD 7.65 billion, at a CAGR of 8.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Residential, and Commercial and industrial), Application (Power generation, Combined heat and power, and Heating), Grade Type (Utility grade, Standard grade, and Premium grade) and Geography (Europe, North America, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

Europe, North America, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Decarbonization mandates and industrialization of utility-scale biomass conversion, Regulatory compliance and technical complexity of international deforestation standards

-

-

Who are the major players in the Wood Pellets Market?

-

AS Graanul Invest, Binderholz GmbH, Bio Eneco, BioPower Sustainable Energy, BrasPine Madeiras Ltda, CT Pellet, ECARE, Energy Pellets of America, Enviva Inc., Highland Pellets LLC, JP Green Fuels, Land Energy Girvan Ltd., Lignetics Inc., Pfeifer Holding GmbH, PREMIUM PELLETS sro, PRODESA, SNOW ENTITIES and VIRIDIS ENERGY INC.

-

Market Research Insights

- Market dynamics are shaped by the strategic pursuit of decarbonization of power generation and the need for resilient energy infrastructure. The adoption of advanced biofuel development is accelerating, with combined heat and power (CHP) systems achieving operational efficiencies exceeding 80%, providing a significant incentive for industrial boiler retrofitting.

- In the power sector, the shift toward a bio-based economy is evident as the demand for torrefied pellets for coal-to-biomass conversion grows, with adoption rates for these specialized fuels increasing by 9% in key industrial applications. This transition not only supports net-zero emissions targets but also enhances grid stability with biomass as a source of base-load renewable power.

- These shifts reflect a broader sustainable energy transition, where biomass plays an integral role in achieving both environmental compliance and energy security.

We can help! Our analysts can customize this wood pellets market research report to meet your requirements.

RIA -

RIA -