Wound Care Biologic Market Size 2025-2029

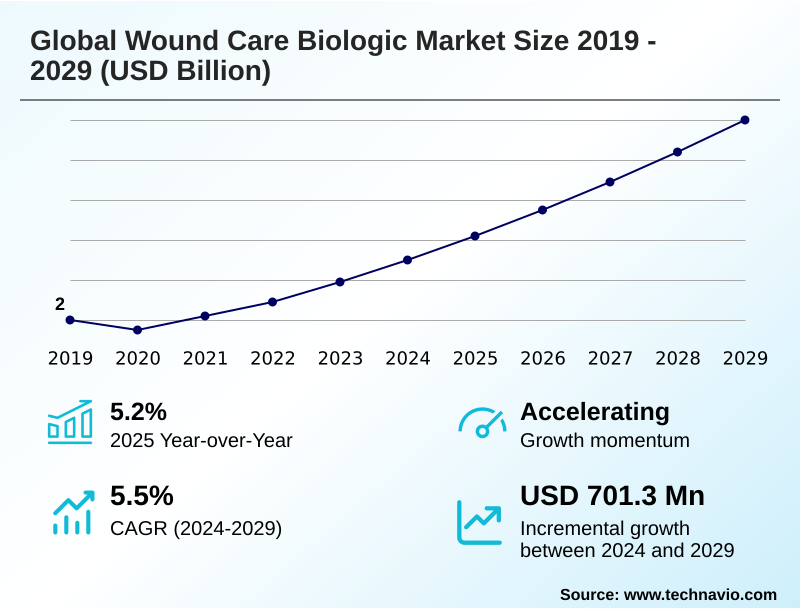

The wound care biologic market size is valued to increase by USD 701.3 million, at a CAGR of 5.5% from 2024 to 2029. Increasing prevalence of chronic diseases and aging population will drive the wound care biologic market.

Major Market Trends & Insights

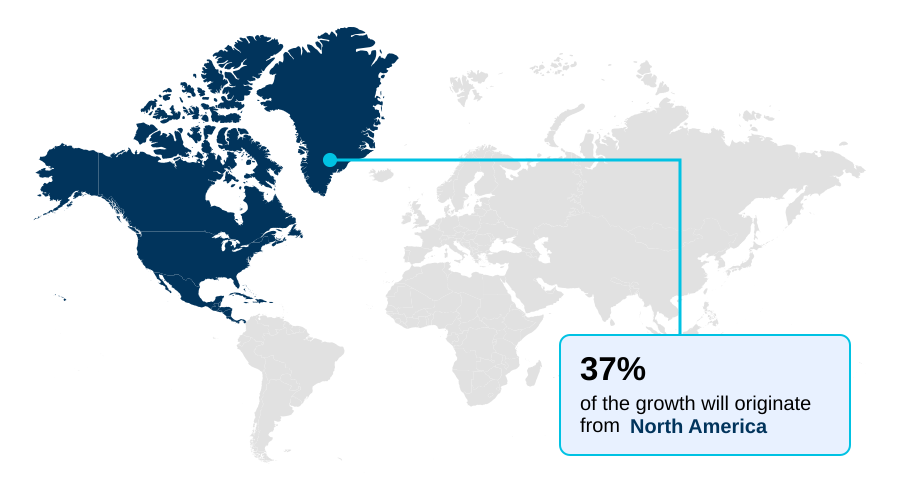

- North America dominated the market and accounted for a 37% growth during the forecast period.

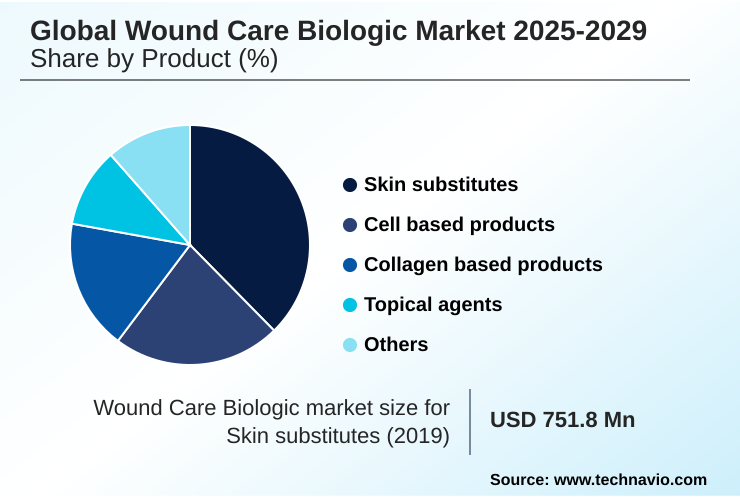

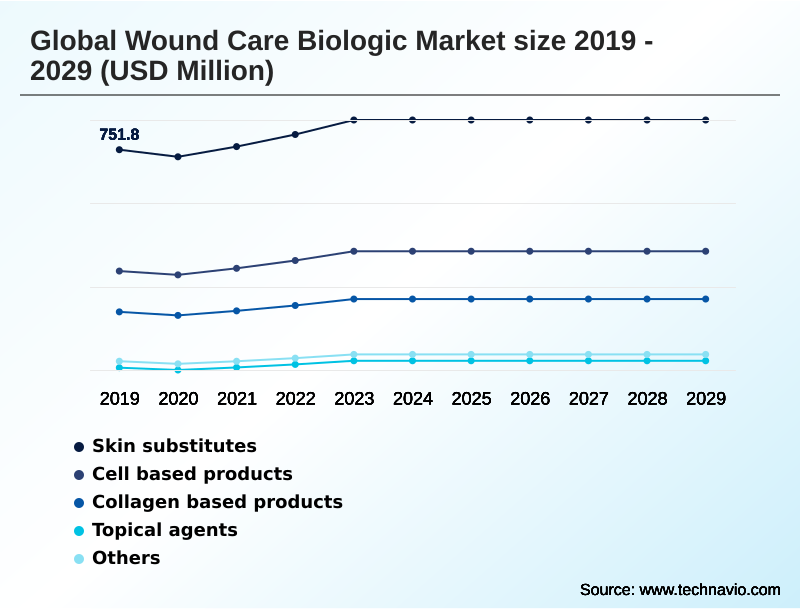

- By Product - Skin substitutes segment was valued at USD 825.2 million in 2023

- By Application - Ulcers segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 1.00 billion

- Market Future Opportunities: USD 701.3 million

- CAGR from 2024 to 2029 : 5.5%

Market Summary

- The wound care biologic market is defined by a continuous push toward therapies that actively participate in the healing process. Unlike passive dressings, these solutions, which include placental biologic products and advanced dermal repair technologies, are designed to address the biological deficits in chronic wounds such as diabetic foot ulcers and pressure ulcers.

- Key drivers include the global rise in chronic diseases and an aging population, creating a sustained need for more effective treatments. A major trend is the shift in the point of care from hospitals to home settings, spurring innovation in user-friendly products for advanced wound management, such as portable negative pressure wound therapy systems.

- For instance, a hospital's value analysis committee might evaluate a new cryopreserved placental membrane based not just on its higher upfront cost but on its demonstrated ability to reduce total treatment duration and prevent readmissions, impacting overall budget allocation.

- However, market adoption faces challenges from the high cost of therapies like bioengineered tissues and complex, evolving reimbursement frameworks that can create uncertainty for providers and limit patient access to these critical innovations.

What will be the Size of the Wound Care Biologic Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Wound Care Biologic Market Segmented?

The wound care biologic industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Skin substitutes

- Cell based products

- Collagen based products

- Topical agents

- Others

- Application

- Ulcers

- Surgical and traumatic wounds

- Burns

- Others

- End-user

- Hospitals and clinics

- ASCs

- Burn centers and wound clinics

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Product Insights

The skin substitutes segment is estimated to witness significant growth during the forecast period.

The skin substitutes segment is a dynamic component of the market, engineered to mimic natural skin function for severe wounds like burns and chronic ulcers.

This segment includes both cellular substitutes with living cells and acellular options that provide a decellularized scaffold. North America's dominance is driven by high healthcare spending and favorable reimbursement.

Innovation is demonstrated by products like lyophilized human amniotic fluid allograft, a liquid biologic for topical application. These advancements in allogeneic cell-based therapies and human cells tissues are critical.

The focus is on creating clinically effective and convenient bioengineered tissues for various care settings, which can improve healing rates in venous leg ulcers by over 30% compared to traditional methods, showcasing the value of advanced dermal repair and biomimetic matrix technology.

The Skin substitutes segment was valued at USD 825.2 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Wound Care Biologic Market Demand is Rising in North America Get Free Sample

North America leads the market, accounting for 37% of the opportunity, driven by sophisticated healthcare infrastructure and high demand for advanced wound bioactives for conditions like diabetic foot ulcers.

The region is a hub for innovation in dermal regeneration technologies and placental biologics.

Meanwhile, Asia is the fastest-growing region, with its market expanding faster than the 5.5% global average, fueled by rising healthcare expenditure and a large patient population requiring burn care biologics.

The adoption of biologic scaffolds and biologically active dressings is increasing. Europe, representing 26% of the landscape, shows steady demand for collagen-based products and engineered tissue products.

The Rest of World (ROW) focuses on cost-effective solutions, with gradual adoption of advanced wound dressings and marine-derived grafts for surgical and traumatic wounds.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic application of advanced therapies is becoming increasingly specific to wound etiology, influencing treatment pathways and procurement decisions. For instance, biologics for diabetic foot ulcers treatment are selected based on their ability to address underlying ischemia and neuropathy, moving beyond simple moisture management.

- In burn units, skin substitutes for burn care management are critical when autografting is limited, providing life-saving temporary coverage. The use of a collagen matrix for surgical wounds prevention is becoming standard in high-risk patients to mitigate dehiscence and infection.

- Similarly, the application of an amniotic membrane for chronic wounds healing provides a rich source of growth factors to restart a stalled inflammatory process. In cases of persistent venous leg ulcers, cell-based therapy for venous leg ulcers offers a regenerative approach where other modalities have failed.

- The focus on advanced dressings for pressure ulcer care is driven by the need to reduce both patient suffering and the high costs associated with these preventable injuries. This is part of a broader shift toward biologics in home healthcare wound management, which requires products that are both effective and easy for non-specialists to apply.

- Extracellular matrix for soft tissue reconstruction provides a robust scaffold for complex trauma cases, while managing complex wounds with biologic therapies is now a core competency in specialized centers.

- The cost-effectiveness of wound care biologics is a central consideration, with studies showing that while initial costs are higher, the reduction in healing time and complication rates, sometimes by over 25%, can lead to significant overall savings.

What are the key market drivers leading to the rise in the adoption of Wound Care Biologic Industry?

- The increasing prevalence of chronic diseases, compounded by a globally aging population, serves as a fundamental driver for the wound care biologic market.

- The market's primary driver is the confluence of rising chronic disease prevalence and an aging global population.

- By 2030, one in six people will be over 60, increasing susceptibility to chronic wounds and demand for tissue-based dressings and advanced wound bioactives.

- The expanding diabetic population directly correlates with a growing patient base requiring specialized treatments for diabetic foot ulcers. Technological innovation is another critical engine, with R&D yielding advanced skin substitutes and cellular and tissue-based therapies.

- This innovation pipeline is demonstrated by companies achieving 18% net sales growth on placental biologic products.

- These proactive therapies, including three-dimensional resorbable wound matrix and solutions for surgical and traumatic wounds, can shorten healing times and reduce the overall economic burden of chronic wound care.

What are the market trends shaping the Wound Care Biologic Industry?

- A prominent trend is the rise of combination therapies and bioactive dressings. These sophisticated solutions address multiple facets of the complex wound healing process simultaneously.

- A dominant trend is the shift toward combination therapies and bioactive dressings, moving beyond single-action products. Innovations in cryopreserved placental membrane and hydrofiber and silver technologies create solutions that address inflammation and microbial load simultaneously. This is seen in products offering a 31% higher healing rate for venous leg ulcers.

- Another key trend is the decentralization of care from hospitals to home settings, driving demand for user-friendly systems for negative pressure wound therapy and advanced wound management. This shift alters how biologics are distributed and used.

- Furthermore, market consolidation through mergers and acquisitions is reshaping the landscape, as major players acquire firms with unique technologies like intact fish skin technology and flowable graft technology to expand their portfolios in areas like complex wound surgery.

What challenges does the Wound Care Biologic Industry face during its growth?

- The high cost of wound care biologics, coupled with inconsistent and evolving reimbursement frameworks, presents a significant challenge to widespread market adoption and growth.

- A primary impediment is the high cost of wound care biologics and inconsistent reimbursement, which limits access. The complex manufacturing of biologic dressings and polymer-assisted scaffolds contributes to prices substantially higher than traditional dressings. Navigating reimbursement is a critical challenge, exemplified by a 3.37% reduction in the Medicare physician fee schedule conversion factor, impacting provider payment.

- Stringent regulatory pathways also pose hurdles. The FDA's classification of products like AXIOFILL as needing a full biologics license application, rather than being regulated as a human cells tissues product, can add significant cost and delay market entry.

- Finally, competition from traditional products, which still command a market segment representing several billion in annual sales, and a lack of clinician awareness about advanced therapies remain significant barriers to adoption.

Exclusive Technavio Analysis on Customer Landscape

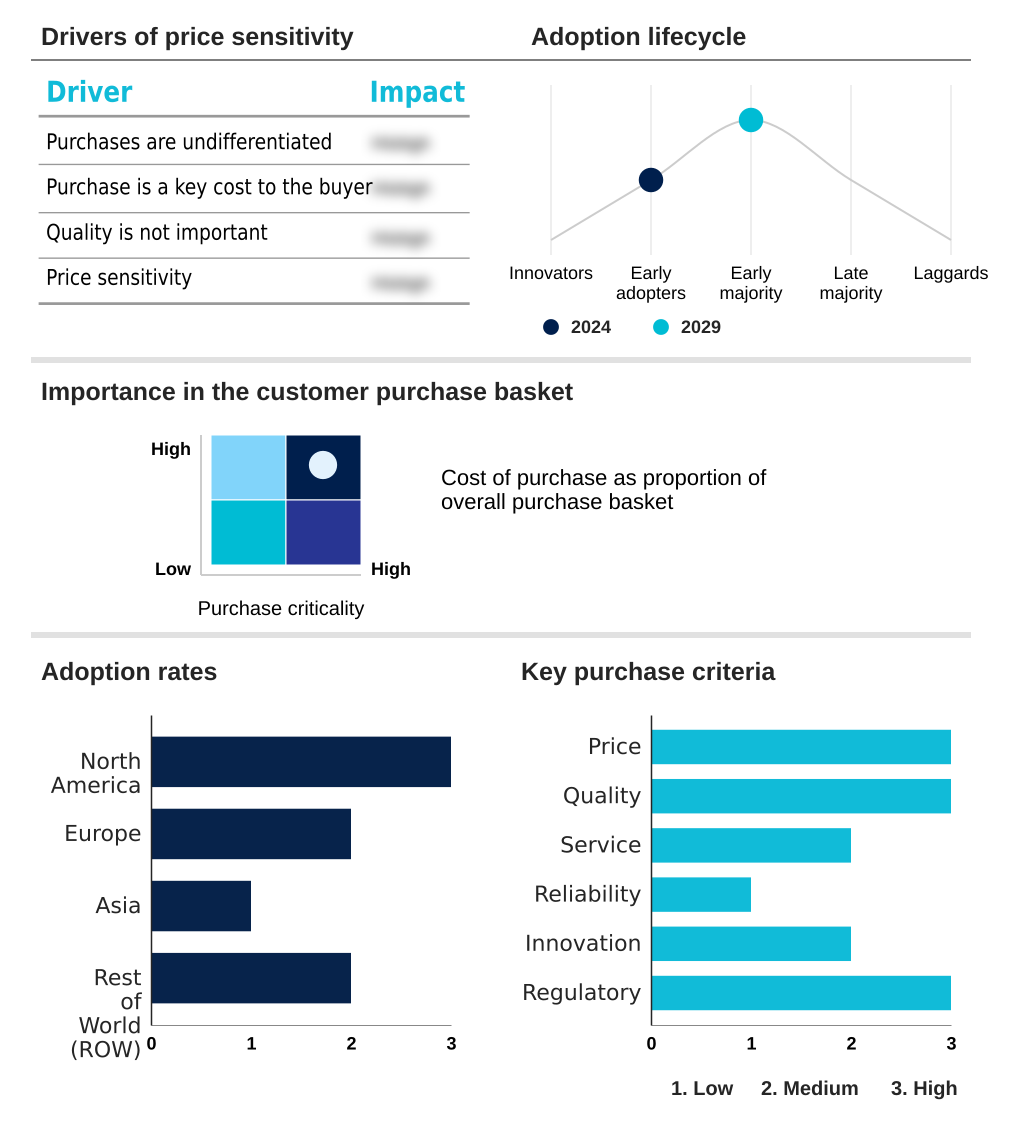

The wound care biologic market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the wound care biologic market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Wound Care Biologic Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, wound care biologic market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amnio Technology LLC - Offers wound care biologics derived from amniotic tissues and membranes, providing biologic matrices designed to support healing and modulate inflammation in advanced wound care applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amnio Technology LLC

- Aroa Biosurgery Ltd.

- Avita Medical Inc.

- B.Braun SE

- Celularity Inc.

- Coloplast AS

- ConvaTec Group Plc

- Derma Sciences Inc.

- Integra LifeSciences Corp.

- Kerecis Ltd.

- Marine Polymer Technologies Inc.

- Medline Industries LP

- MiMedx Group Inc.

- Molnlycke Health Care AB

- Organogenesis Holdings Inc.

- Skye Biologics Holdings LLC

- Smith and Nephew plc

- Stryker Corp.

- Vericel Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Wound care biologic market

- In April, 2024, Smith and Nephew plc launched its RENASYS EDGE negative pressure wound therapy system in the US, a lightweight and compact device designed for patients receiving wound care at home.

- In May, 2024, ConvaTec Group Plc announced results from a multinational randomized controlled trial showing its AQUACEL Ag plus Extra dressing was 31% more likely to heal venous leg ulcers compared to standard care.

- In July, 2025, Gel4Med, Inc. announced it received a small business innovation research award from the National Institutes of Health to advance its portfolio of advanced wound care and surgical reconstruction products.

- In August, 2025, Gel4Med, Inc. announced its G4Derm Plus, a biomimetic matrix technology, was assigned a unique HCPCS Level II code by the Centers for Medicare and Medicaid Services, facilitating reimbursement.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Wound Care Biologic Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 311 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.5% |

| Market growth 2025-2029 | USD 701.3 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 5.2% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Russia, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Singapore, Indonesia, Thailand, Brazil, Saudi Arabia, UAE, Australia, South Africa and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The wound care biologic market is characterized by a dynamic innovation cycle focused on bioactive acellular biomaterials and cellular and tissue-based products. These advanced solutions, including everything from a three-dimensional resorbable wound matrix to topical growth factors, are designed to actively intervene in the healing process.

- Boardroom-level strategy is increasingly influenced by the trend of shifting care to home settings, which necessitates the development of user-friendly products like autologous blood clot systems and flowable graft technology that do not require complex clinical oversight. This requires rethinking product design around enzymatic debridement and wound bed preparation for non-specialist use.

- The development of advanced materials such as porcine small intestine submucosa, processed human tissue allografts, and decellularized marine-derived matrices is driven by the need for more effective tissue regeneration scaffolds. Evidence demonstrating that certain hydrofiber and silver technologies can improve healing rates by over 30% directly impacts budgeting and procurement decisions, justifying the higher cost of these therapies.

- This clinical validation is essential for market penetration of placental extracellular matrix devices, bioengineered tissues, and other innovations like intact fish skin technology.

What are the Key Data Covered in this Wound Care Biologic Market Research and Growth Report?

-

What is the expected growth of the Wound Care Biologic Market between 2025 and 2029?

-

USD 701.3 million, at a CAGR of 5.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Skin substitutes, Cell based products, Collagen based products, Topical agents, and Others), Application (Ulcers, Surgical and traumatic wounds, Burns, and Others), End-user (Hospitals and clinics, ASCs, Burn centers and wound clinics, and Others) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing prevalence of chronic diseases and aging population, High cost and inconsistent reimbursement frameworks

-

-

Who are the major players in the Wound Care Biologic Market?

-

Amnio Technology LLC, Aroa Biosurgery Ltd., Avita Medical Inc., B.Braun SE, Celularity Inc., Coloplast AS, ConvaTec Group Plc, Derma Sciences Inc., Integra LifeSciences Corp., Kerecis Ltd., Marine Polymer Technologies Inc., Medline Industries LP, MiMedx Group Inc., Molnlycke Health Care AB, Organogenesis Holdings Inc., Skye Biologics Holdings LLC, Smith and Nephew plc, Stryker Corp. and Vericel Corp.

-

Market Research Insights

- The market is shaped by a push for clinical efficacy and economic value. The adoption of advanced therapies is accelerating, with some biologic dressings demonstrating a 31% improvement in healing rates for venous leg ulcers compared to standard care. This evidence supports their use in specialized settings focused on surgical reconstruction products and complex wound surgery.

- Demand for placental biologics is robust, reflected in some vendors reporting 18% year-over-year sales growth. This dynamism is further driven by the shift toward outpatient care, increasing the need for regenerative scaffold technologies and biologically compatible matrices that are easy to apply.

- However, budget-conscious providers must balance the high cost of advanced wound dressings against their long-term benefits, influencing procurement of both amniotic membrane allograft and polymer-assisted scaffolds.

We can help! Our analysts can customize this wound care biologic market research report to meet your requirements.

RIA -

RIA -