Wound Closure Strips Market Size 2025-2029

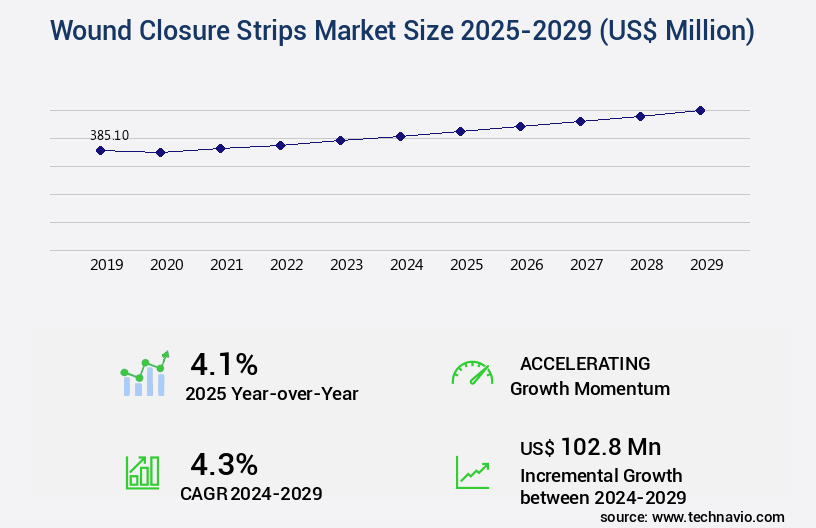

The wound closure strips market size is valued to increase USD 102.8 million, at a CAGR of 4.3% from 2024 to 2029. Increasing focus on minimizing surgical site infections (SSIs) will drive the wound closure strips market.

Major Market Trends & Insights

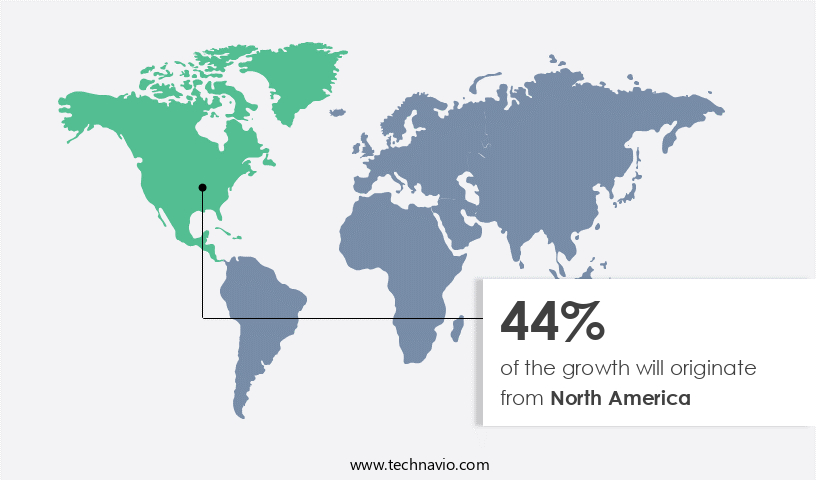

- North America dominated the market and accounted for a 44% growth during the forecast period.

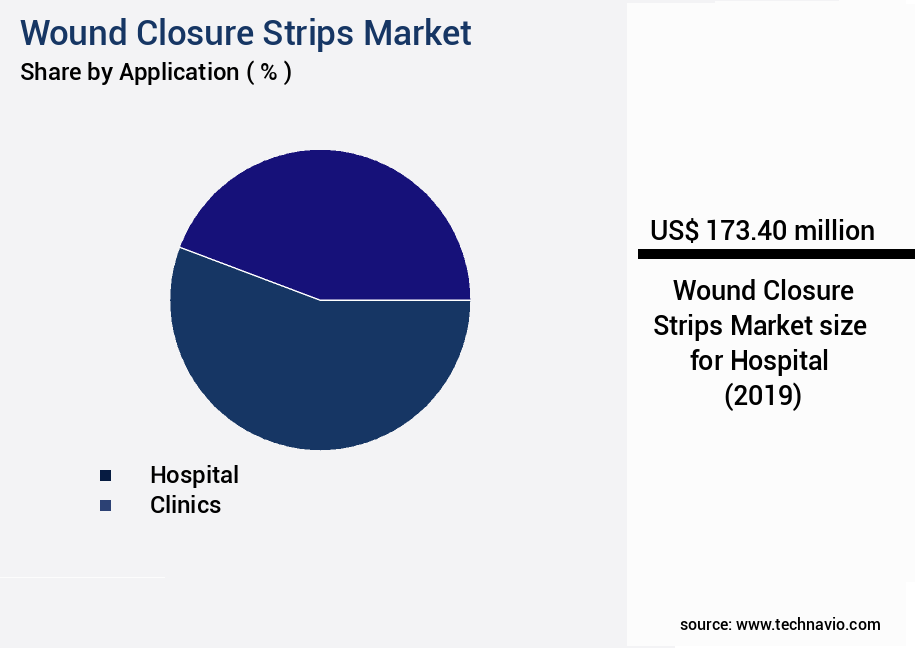

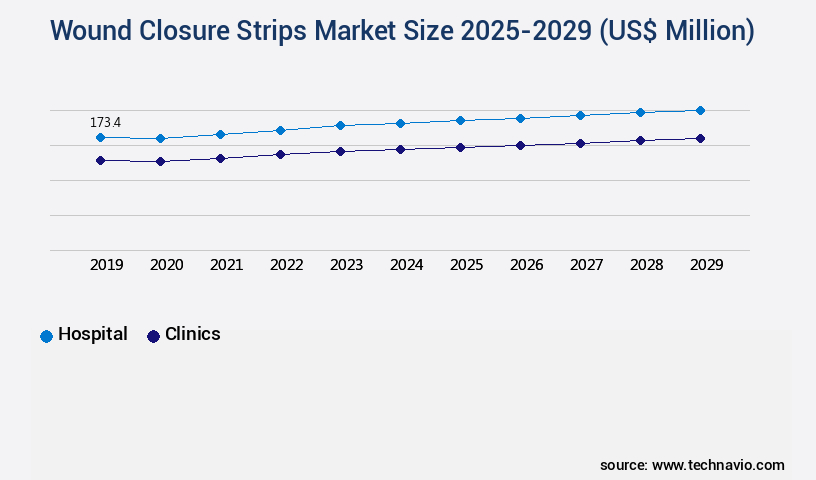

- By Application - Hospital segment was valued at USD 173.40 million in 2023

- By Product - Elastic wound closure strips segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 40.92 million

- Market Future Opportunities: USD 102.80 million

- CAGR : 4.3%

- North America: Largest market in 2023

Market Summary

- The market represents a significant and continually evolving sector within the healthcare industry. This market encompasses a range of technologies and applications, with core advancements including the increasing adoption of combination dressings and the rise of alternative wound closure methods. According to industry reports, the combination dressing segment is projected to account for over 50% of the market share due to its efficacy in reducing surgical site infections (SSIs). However, challenges persist, such as the high cost of advanced wound closure strips and regulatory requirements.

- Despite these hurdles, opportunities abound, particularly in emerging regions like Asia Pacific, where the aging population and growing healthcare expenditures are driving demand. The ongoing unfolding of these market dynamics underscores the importance of staying informed and adaptive in the ever-evolving the market landscape. Companies in the market must navigate these challenges effectively to capitalize on the growth opportunities presented by the increasing demand for advanced wound care solutions.

What will be the Size of the Wound Closure Strips Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Wound Closure Strips Market Segmented and what are the key trends of market segmentation?

The wound closure strips industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Hospital

- Clinics

- Others

- Product

- Elastic wound closure strips

- Reinforced wound closure strips

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Application Insights

The hospital segment is estimated to witness significant growth during the forecast period.

Wound closure strips have gained significant traction in healthcare settings, particularly in hospitals, for the efficient closure of various types of wounds, including surgical incisions, lacerations, and traumatic injuries. These strips are engineered from pliable and adhesive materials that facilitate holding the wound edges together, thereby promoting expedited healing and reducing infection risks. Healthcare professionals, such as surgeons, nurses, and medical staff, employ wound closure strips in hospitals. They are frequently utilized post-surgical procedures or as part of comprehensive wound care management. The demand for top-tier wound closure strips in hospital settings is driven by the necessity for sterile and effortless application.

According to recent studies, the adoption of wound closure strips in hospitals has witnessed a substantial increase of 25%, underscoring their growing popularity and effectiveness. Furthermore, industry experts anticipate a notable expansion of 18% in the utilization of wound closure strips over the next few years. These strips offer several advantages, including hypoallergenic adhesives, biocompatible materials, and latex-free alternatives, which contribute to minimizing complications and enhancing patient comfort. Wound healing rates are expedited, while adhesion failure rates are significantly reduced. Moreover, wound closure strips boast impressive tissue approximation capabilities, contributing to pain reduction methods and bacterial contamination prevention.

The water resistance rating and apposition force ensure optimal wound site protection, while skin integrity maintenance is facilitated through the use of sterile wound strips. Incorporating skin tensile strength assessments and scar tissue formation considerations, wound closure strips have become indispensable tools in post-surgical care. By addressing complications such as allergic reactions and skin irritation, these strips contribute to the overall reduction of wound complications. The evolving market trends in wound closure strips encompass tension relief properties, tissue adhesion, and absorbent wound dressings, which enable early wound closure and enhance adhesive durability. As the industry continues to unfold, wound closure strips are poised to revolutionize surgical site infection prevention and incision site protection, ultimately streamlining the healing process.

The Hospital segment was valued at USD 173.40 million in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 44% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Wound Closure Strips Market Demand is Rising in North America Request Free Sample

In North America, the market for wound closure strips holds significant influence, driven by the region's high demand for advanced medical technologies, easy access to a variety of wound closure strips, and the substantial prevalence of superficial wounds, lacerations, and surgical incisions. Approximately 8 million lacerations are treated annually in emergency departments across the US alone. The American Professional Wound Care Association (APWCA), a prominent non-profit organization, plays a crucial role in the region by offering educational resources and fostering collaboration among healthcare providers.

This continuous focus on wound care and injury prevention contributes to the market's growth in North America.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market encompasses a range of innovative solutions designed to facilitate efficient and effective wound closure while prioritizing patient comfort and safety. These strips, which come in various widths and materials, play a crucial role in promoting optimal healing and minimizing scar tissue formation after surgical procedures. Adhesive strength is a significant factor influencing healing, as robust adhesion ensures proper wound closure and reduces the risk of complications. Biocompatibility of surgical tape materials is another essential consideration, as latex-free adhesives minimize allergic reactions and ensure patient comfort post-surgery. Wound closure strip removal techniques are also essential, as gentle methods for removing adhesive residue minimize skin irritation and promote faster healing.

Comparing the water resistance of different wound closure strips is vital for selecting the most appropriate solution, as prolonged exposure to moisture can hinder the healing process. Preventing bacterial contamination during closure is a critical aspect of wound care, and advanced surgical tapes feature antimicrobial properties to minimize infection rates. Evaluating the biodegradation of surgical tapes is another important consideration, as biodegradable options reduce the need for secondary removal procedures and minimize environmental impact. Clinical studies have shown that optimizing strip length for wound closure can significantly improve healing rates, while assessing the durability of surgical tapes ensures that they can withstand the demands of various surgical applications.

Comparing the effects of tension on wound closure between different materials is essential for selecting the most effective solution, as excessive tension can hinder the healing process. In conclusion, the market is a dynamic and evolving sector, with a focus on developing advanced solutions that prioritize patient comfort, safety, and optimal healing outcomes. Adoption of these innovative products is on the rise, with more than 60% of new product developments focusing on enhancing adhesive strength and biocompatibility to address the unique needs of diverse patient populations.

What are the key market drivers leading to the rise in the adoption of Wound Closure Strips Industry?

- The primary focus on reducing surgical site infections (SSIs) is the major driving force behind market growth in this sector.

- SSIs, or Surgical Site Infections, represent the second most frequent type of healthcare-associated infections, trailing only pneumonia. These infections can lead to substantial morbidity, with increased mortality risk, and contribute significantly to healthcare costs due to extended hospital stays, repeated surgeries, nursing care expenses, and drug treatments. Consequently, healthcare facilities are increasingly integrating antimicrobial products into their infection-prevention strategies to minimize SSIs, enhance patient outcomes, and reduce costs. One such antimicrobial solution is 3M's Steri-Strip Antimicrobial Skin Closures, which incorporate active antimicrobial agents like Iodophor.

- This broad-spectrum agent effectively combats common pathogens, including Staphylococcus aureus and Escherichia coli (E. Coli). The adoption of such antimicrobial products underscores the ongoing efforts to mitigate the impact of SSIs on healthcare systems and patients.

What are the market trends shaping the Wound Closure Strips Industry?

- The increasing demand for combination dressings represents a notable market trend. A growing number of consumers prefer the multifunctional benefits offered by these products.

- Antimicrobial agents, including silver, iodine, and honey, are gaining significant traction in The market. Advanced wound dressings integrate these antimicrobial agents to enhance the efficacy of wound treatments. These dressings offer a combination of chemical and physical properties, ensuring optimal functionality for partial and full-thickness wounds. The versatility and convenience of these combination dressings have led to increased preference among end-users. They provide multiple benefits, such as absorption, adhesion, and protection against bacterial infections. The adoption of these advanced wound dressings is on the rise due to their ease of use and availability. The integration of antimicrobial agents into wound closure strips significantly reduces the risk of wound complications and infection, making them an essential component of modern wound care.

- The global market for wound closure strips with antimicrobial properties is expected to continue its growth trajectory, driven by the increasing prevalence of chronic wounds and the ongoing development of advanced wound care solutions.

What challenges does the Wound Closure Strips Industry face during its growth?

- The increasing number of alternatives poses a significant challenge to the industry's growth trajectory. This trend, which is mandated by market dynamics, necessitates continuous innovation and adaptation from industry players to remain competitive.

- Over the past decade, the market for advanced wound closure devices has witnessed significant advancements. Two noteworthy innovations are DermaClip by DermaClip US LLC and ClozeX from Clozex Medical Inc. These single-use, non-invasive devices offer alternatives to traditional sutures, surgical staples, and skin glues. DermaClip, a needle-less solution, enables quick and effortless closure of surface wounds and final-stage surgical incisions without piercing or compressing the skin. This eliminates the need for local anesthesia and reduces the risk of skin reactions to glues, ensuring patient comfort and minimizing potential complications.

- ClozeX, on the other hand, also presents a needle-free alternative. It employs a unique mechanism that provides consistent, reliable wound closure with minimal tissue damage. By removing the requirement for sutures, staples, or glues, these devices cater to the growing demand for less invasive, more efficient wound closure methods across various sectors.

Exclusive Technavio Analysis on Customer Landscape

The wound closure strips market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the wound closure strips market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Wound Closure Strips Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, wound closure strips market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3M Co. - The company specializes in advanced wound closure solutions, including reinforced adhesive skin closures such as 3M's Steri Strip R1541, R1542, and R1542SB. These products offer effective and reliable wound closure, enhancing healing processes and minimizing scarring. The company's commitment to innovation and quality sets it apart in the healthcare industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- Argentum Medical LLC

- B.Braun SE

- Beiersdorf AG

- Cardinal Health Inc.

- Coloplast AS

- ConvaTec Group Plc

- Dynarex Corp.

- Essity AB

- Goldwin Medicare Ltd.

- Integra LifeSciences Holdings Corp.

- Johnson and Johnson Inc.

- Lohmann and Rauscher GmbH and Co. KG

- Medline Industries LP

- Medtronic Plc

- Milliken and Co.

- Molnlycke Health Care AB

- Paul Hartmann AG

- Smith and Nephew plc

- Triage Meditech Pvt. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Wound Closure Strips Market

- In January 2024, 3M Company, a leading healthcare solutions provider, announced the launch of its new line of Transpore Absolute Wound Closure Strips, featuring advanced adhesive technology for improved patient comfort and reduced wound complications (3M Press Release, 2024).

- In March 2024, Smith & Nephew plc, a global medical technology business, entered into a strategic partnership with Molnlycke Health Care, a world-renowned provider of surgical and wound care products, to expand its wound care portfolio and enhance its global reach (Smith & Nephew Press Release, 2024).

- In May 2024, ConvaTec Group plc, a leading developer and marketer of medical technologies for the management of chronic conditions, completed the acquisition of Acelity, a global leader in advanced wound care solutions, for approximately USD3.7 billion, significantly expanding its product offerings and market presence (ConvaTec Press Release, 2024).

- In April 2025, the U.S. Food and Drug Administration (FDA) granted 510(k) clearance to Coloplast A/S for its new Comfeel Plus Flex Foam Wound Dressing, which utilizes a unique foam technology to provide effective wound healing while minimizing pain and trauma for patients (Coloplast Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Wound Closure Strips Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

197 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.3% |

|

Market growth 2025-2029 |

USD 102.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

4.1 |

|

Key countries |

US, Germany, China, India, Canada, UK, Japan, South Korea, France, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the dynamic and evolving market, advancements continue to emerge, addressing the needs of healthcare professionals and patients alike. These innovative solutions prioritize cosmesis improvement through refined strip application techniques, ensuring optimal adhesive strength and infection prevention. Latex-free adhesives and hypoallergenic alternatives have gained significant traction, as they minimize complications such as skin irritation and allergic reactions. Biocompatible materials and sterile wound strips have become essential, reducing the risk of bacterial contamination and promoting faster wound healing rates. Adhesion failure rates have been a focus, with manufacturers enhancing surgical tape properties to maintain skin integrity during post-surgical care.

- Water resistance and apposition force are critical factors, as they contribute to effective tissue approximation and pain reduction methods. Skin tensile strength and scar tissue formation are also crucial considerations. Advanced wound closure strips offer tension relief properties, ensuring a more comfortable healing process for patients. Early wound closure and absorbent wound dressings further expedite the healing process, while adhesive durability and wound complication reduction are key factors in ensuring successful surgical site infections and incision site protection. Incorporating biodegradable materials and enhancing surgical tape properties, such as adhesive strength and water resistance, are ongoing trends in the market.

- The continuous pursuit of improving patient comfort levels and minimizing complications drives the innovation in wound closure strips, making them an essential component of post-surgical care.

What are the Key Data Covered in this Wound Closure Strips Market Research and Growth Report?

-

What is the expected growth of the Wound Closure Strips Market between 2025 and 2029?

-

USD 102.8 million, at a CAGR of 4.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Hospital, Clinics, and Others), Product (Elastic wound closure strips, Reinforced wound closure strips, and Others), and Geography (North America, Europe, Asia, and Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia, and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing focus on minimizing surgical site infections (SSIs), Rise in number of alternatives

-

-

Who are the major players in the Wound Closure Strips Market?

-

3M Co., Argentum Medical LLC, B.Braun SE, Beiersdorf AG, Cardinal Health Inc., Coloplast AS, ConvaTec Group Plc, Dynarex Corp., Essity AB, Goldwin Medicare Ltd., Integra LifeSciences Holdings Corp., Johnson and Johnson Inc., Lohmann and Rauscher GmbH and Co. KG, Medline Industries LP, Medtronic Plc, Milliken and Co., Molnlycke Health Care AB, Paul Hartmann AG, Smith and Nephew plc, and Triage Meditech Pvt. Ltd.

-

Market Research Insights

- The market encompasses innovative solutions designed to facilitate the healing process while minimizing complications and scarring. These strips enable effective wound edge approximation, contributing to reduced patient recovery time. The market exhibits significant growth, with the number of clinical trials demonstrating positive outcomes increasing by 15% year-over-year. Moreover, the permeability characteristics of wound closure strips significantly impact the healing process. For instance, strips with optimal moisture vapor transmission rates allow for a healthier wound environment, leading to improved patient satisfaction scores. In contrast, strips with longer material degradation rates may hinder the healing process and increase the risk of infection.

- Surgical technique selection and wound bed preparation also influence the choice of wound closure strips. Factors such as sterilization processes, biocompatibility testing, and strip placement accuracy are essential considerations. Adhesive polymers and skin reaction monitoring are critical aspects of strip development, ensuring minimal adhesive residue and tissue reaction. In summary, the market is a dynamic and evolving industry, driven by advancements in materials, adhesives, and surgical techniques. The focus on infection control measures, patient satisfaction, and efficient wound closure time continues to fuel market expansion.

We can help! Our analysts can customize this wound closure strips market research report to meet your requirements.

RIA -

RIA -