Zero Friction Coatings Market Size 2026-2030

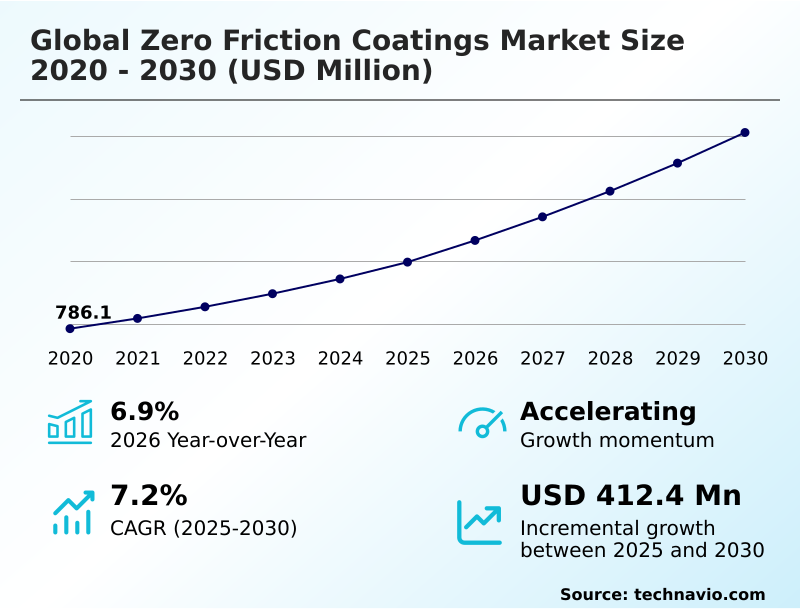

The zero friction coatings market size is valued to increase by USD 412.4 million, at a CAGR of 7.2% from 2025 to 2030. Increasing demand of zero friction coatings in end-user industries will drive the zero friction coatings market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 56.8% growth during the forecast period.

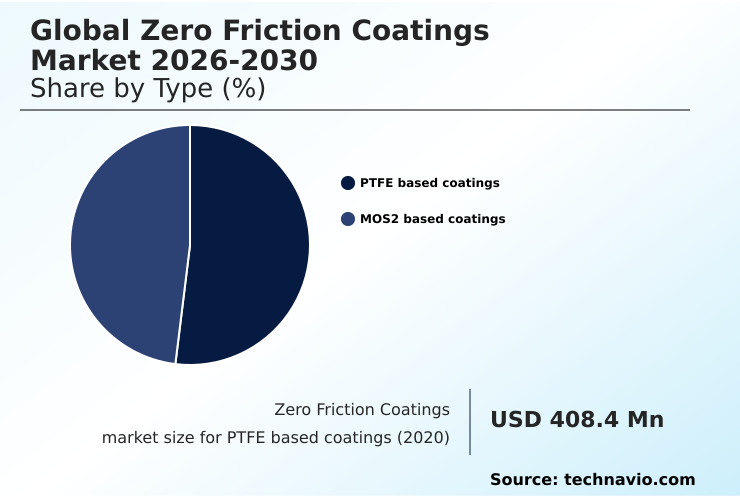

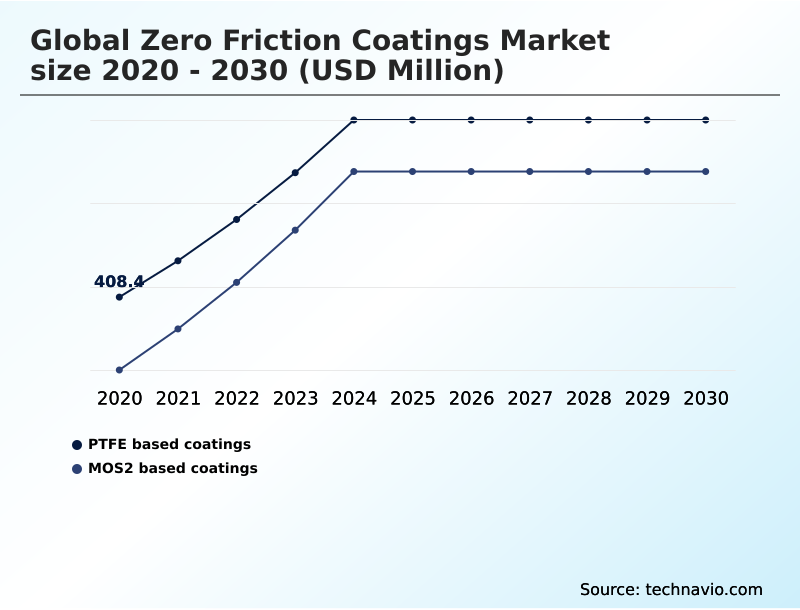

- By Type - PTFE based coatings segment was valued at USD 483 million in 2024

- By End-user - Automobile and transportation segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 624.1 million

- Market Future Opportunities: USD 412.4 million

- CAGR from 2025 to 2030 : 7.2%

Market Summary

- The zero friction coatings market is expanding as industries prioritize operational excellence, component longevity, and energy efficiency. These advanced coatings, formulated with materials like PTFE and molybdenum disulfide, create surfaces with minimal resistance, significantly reducing wear and maintenance requirements. A key driver is the stringent regulatory environment pushing for sustainability.

- For instance, an automotive OEM might apply these coatings to engine pistons and bearings not just to enhance durability but to achieve a critical 5% improvement in fuel economy, helping meet government-mandated emission standards. The market trend is shifting toward eco-friendly, water-based formulations and the integration of nanotechnology to create smarter, more resilient surfaces.

- These nanotechnology-based coatings can enhance tribological performance and offer self-healing properties. However, the high initial cost of these advanced solutions compared to traditional lubricants remains a significant barrier to widespread adoption, compelling businesses to weigh upfront investment against long-term total cost of ownership and performance gains.

What will be the Size of the Zero Friction Coatings Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Zero Friction Coatings Market Segmented?

The zero friction coatings industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- PTFE based coatings

- MOS2 based coatings

- End-user

- Automobile and transportation

- Food and healthcare

- Energy

- General engineering

- Others

- Formulation

- Solvent based

- Water based

- Powder based

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Type Insights

The ptfe based coatings segment is estimated to witness significant growth during the forecast period.

PTFE based coatings are a critical segment, engineered for an extremely low coefficient of friction and superior tribological performance.

These non-stick surface coatings are defined by their chemical inertness properties and thermal stability enhancement, making them indispensable for industrial machinery coatings.

Applications in automotive engine components and aerospace component protection benefit from significant surface resistance reduction and friction and wear minimization.

The integration of advanced solid lubricant particles has improved performance, while emerging nanotechnology-based coatings promise further gains, with some formulations achieving up to a 25% reduction in engine friction.

This continuous innovation ensures PTFE coatings remain a vital solution for enhancing durability and efficiency across high-stakes industries.

The PTFE based coatings segment was valued at USD 483 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

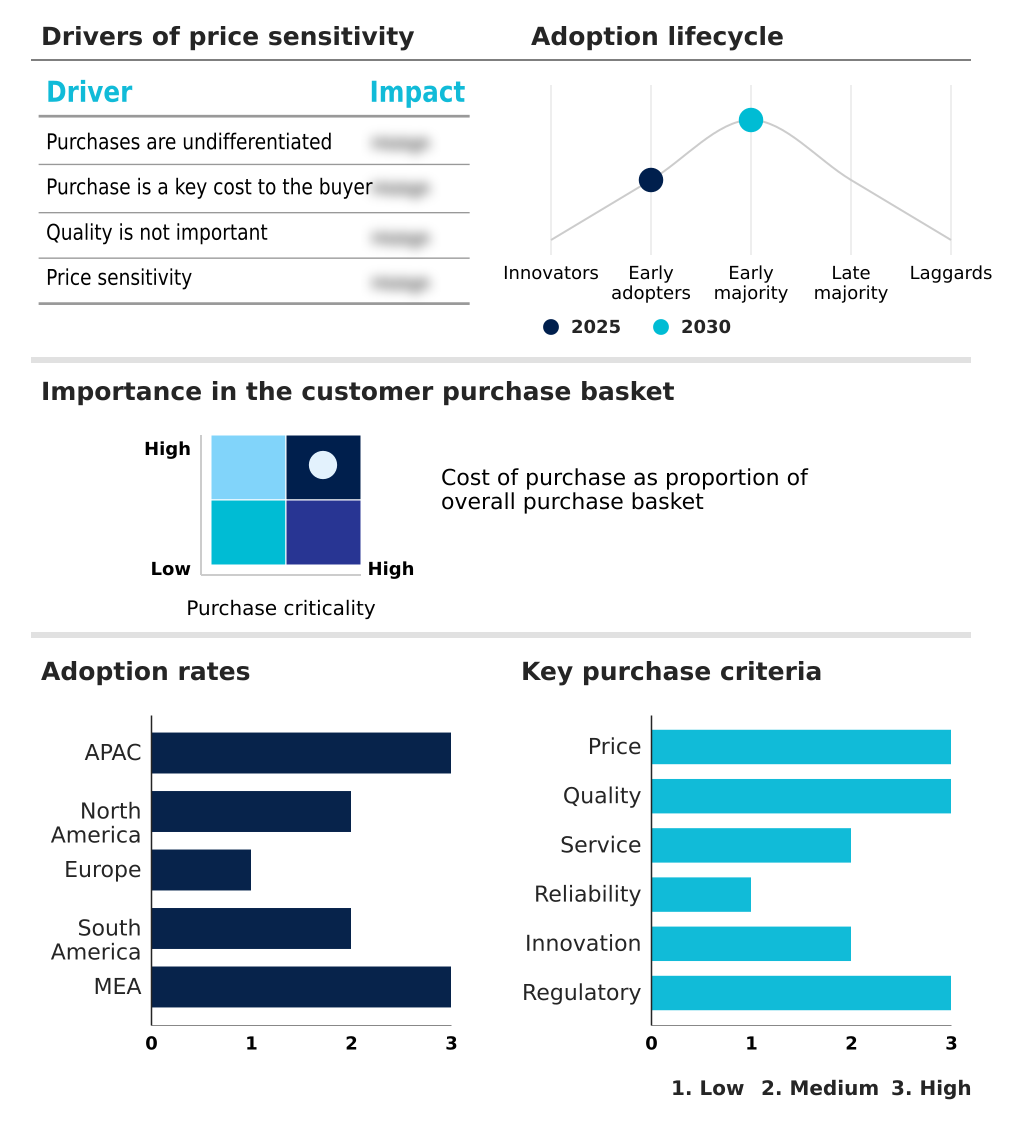

APAC is estimated to contribute 56.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Zero Friction Coatings Market Demand is Rising in APAC Get Free Sample

The geographic landscape is led by APAC, which is set to capture over 56% of the market's incremental growth due to rapid industrialization.

North America follows, accounting for nearly 22% of the opportunity, driven by technological innovation in sectors like aerospace and automotive.

Success in these regions hinges on adopting advanced surface modification techniques and perfecting the coating application process to ensure superior performance. The global shift toward sustainability is accelerating the adoption of powder-based coatings and advanced water-based formulations.

Innovations in thin-film coating technology and smart coating materials are becoming key competitive differentiators, especially as regional regulations around environmental compliance become more stringent.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the market requires a detailed cost-benefit analysis of zero friction surface coatings. For instance, the choice between ptfe vs mos2 for high temperature applications is critical in the aerospace and defense sectors, where thermal stability of coatings in defense applications is non-negotiable for components like turbines.

- In contrast, for automotive powertrain systems, the primary goal is improving fuel efficiency with engine component coatings. The benefits of nanotechnology in zero friction coatings are transformative, enabling the development of advanced formulations that enhance the wear resistance of coatings in heavy industrial machinery and optimize tribological performance in bearing assemblies.

- Application methods for solvent based friction coatings are being refined for precision, while concerns over the environmental impact of powder based low-friction coatings are driving innovation in water based low friction formulations. The role of carbon nanotubes in low friction materials is expanding, enhancing the durability of general engineering parts.

- In specialized fields, self-lubricating coatings for medical implant devices and dry film lubricants for food processing equipment must meet stringent safety and performance standards. Similarly, zero friction solutions for renewable energy systems focus on long-term reliability with minimal maintenance.

- The selection process, whether for high-load industrial gears or for corrosion protection using non-stick surface coatings, increasingly relies on comprehensive performance data. Proper surface preparation for long-lasting friction reduction is universally acknowledged as a critical factor, ensuring coatings perform as specified.

- The focus on reducing friction in aerospace turbine components, where next-generation materials deliver performance gains nearly double that of legacy systems, underscores the high-stakes nature of this field.

What are the key market drivers leading to the rise in the adoption of Zero Friction Coatings Industry?

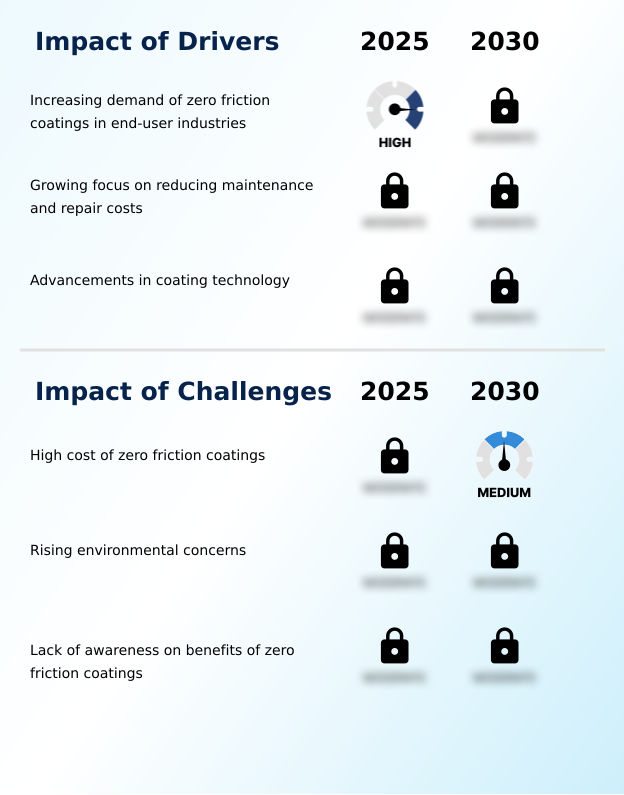

- The primary driver for market growth is the increasing demand for zero friction coatings across key end-user industries seeking enhanced operational efficiency and component longevity.

- Demand from end-user industries for operational efficiency improvement and maintenance cost reduction is the primary market driver.

- The adoption of advanced anti-friction coating formulation technologies is critical for meeting stringent regulatory standards, such as automotive fleet-wide fuel averages of 49 MPG and CO2 emission caps below 93.6 g/km.

- Integrating a high-performance dry film lubricant extends component lifespan, a key objective in aerospace and industrial sectors.

- These coatings provide essential corrosion resistance and high-load bearing capacity, enabling machinery to operate reliably in high-temperature applications and other extreme environments, thereby maximizing asset uptime and reducing total cost of ownership.

What are the market trends shaping the Zero Friction Coatings Industry?

- The increasing utilization of nanotechnology in coating formulations is a significant upcoming market trend, promising enhanced performance and durability.

- The market is increasingly defined by the trend toward nanotechnology and advanced material science. Innovations in self-lubricating coatings and durable coating solutions now offer an 80% reduction in component wear, which is a transformative gain for heavy-duty machinery protection.

- Concurrently, the push for eco-friendly coating alternatives is driving the development of water-based formulations that improve transportation system efficiency, contributing to a 5% gain in fuel economy in some applications. The convergence of these trends is creating smart coating materials with enhanced tribological performance, meeting the complex demands of precision engineering coatings and the growing electric vehicle (EV) components market.

What challenges does the Zero Friction Coatings Industry face during its growth?

- The high cost associated with zero friction coatings presents a key challenge to wider market adoption and overall industry growth.

- The high initial investment for advanced surface engineering solutions remains a significant market challenge. Premium graphene-based coatings and formulations with carbon nanotube additives can cost up to ten times more than conventional lubricants, with prices reaching $200 per gallon versus $20 for standard oil.

- This cost disparity complicates operational cost optimization and slows adoption, despite proven benefits like energy loss minimization and enhanced component reliability. Businesses must therefore conduct rigorous evaluations, weighing the upfront expense of superior surface treatment technologies against long-term gains in asset longevity and performance, which currently limits their use in more price-sensitive applications.

Exclusive Technavio Analysis on Customer Landscape

The zero friction coatings market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the zero friction coatings market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Zero Friction Coatings Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, zero friction coatings market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3M Co. - Offerings include specialized anti-friction and low-friction coatings, such as PTFE and dry film lubricants, designed to enhance durability and performance across industrial applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- AFT Fluorotec Ltd.

- Akzo Nobel NV

- ASV Multichemie Pvt. Ltd.

- Axalta Coating Systems Ltd.

- Carl Bechem GmbH

- DuPont de Nemours Inc.

- Endura Coatings

- Henkel AG and Co. KGaA

- IKV Tribology Ltd.

- Master Bond Inc.

- Nippon Paint Holdings Co Ltd.

- Poeton Industries Ltd.

- PPG Industries Inc.

- RPM International Inc.

- Sandwell UK Ltd.

- The Chemours Co.

- The Sherwin Williams Co.

- VITRACOAT

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Zero friction coatings market

- In October 2024, DuPont de Nemours Inc. announced the launch of a new line of MOLYKOTE anti-friction coatings specifically formulated for electric vehicle (EV) components, designed to reduce energy loss in powertrains and extend battery range.

- In January 2025, Akzo Nobel NV completed its acquisition of a German specialty coatings firm, strengthening its portfolio of powder-based zero friction coatings and expanding its footprint in the European automotive and industrial markets.

- In March 2025, The Chemours Co. entered into a strategic partnership with an aerospace manufacturer to co-develop next-generation Teflon-based coatings for turbine engine components, aiming to improve thermal stability and reduce maintenance cycles.

- In May 2025, PPG Industries Inc. received regulatory approval for a new series of environmentally compliant, water-based low-friction coatings, meeting stringent VOC emission standards for use in food processing and medical device applications.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Zero Friction Coatings Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 295 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.2% |

| Market growth 2026-2030 | USD 412.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.9% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is undergoing a significant transformation, moving beyond simple surface resistance reduction to embrace holistic low-friction surface engineering. Boardroom decisions now hinge on adopting advanced surface technologies that ensure long-term operational efficiency improvement and maintenance cost reduction. Innovations in anti-friction coating formulation are critical, with ptfe based coatings and mos2 based coatings leading the way.

- The use of nanotechnology-based coatings, incorporating graphene-based coatings and carbon nanotube additives, is revolutionizing tribological performance. These self-lubricating coatings, composed of solid lubricant particles, deliver a low coefficient of friction and superior lubricity enhancement. A key business case is the 80% reduction in wear for critical components, which proves the value of creating wear-resistant surfaces.

- Formulations are evolving from traditional solvent-based formulations to cleaner water-based formulations and powder-based coatings. High-performance polymers and advanced composite materials are essential for achieving thermal stability enhancement, chemical inertness properties, and corrosion resistance.

- The goal is to provide a comprehensive surface engineering solution, from adhering to surface preparation standards and mastering the coating application process to achieving energy loss minimization and component lifespan extension. A dry film lubricant must also provide a high-load bearing capacity, resulting in non-stick surface coatings that fundamentally improve asset performance through advanced surface modification techniques.

What are the Key Data Covered in this Zero Friction Coatings Market Research and Growth Report?

-

What is the expected growth of the Zero Friction Coatings Market between 2026 and 2030?

-

USD 412.4 million, at a CAGR of 7.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (PTFE based coatings, and MOS2 based coatings), End-user (Automobile and transportation, Food and healthcare, Energy, General engineering, and Others), Formulation (Solvent based, Water based, and Powder based) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand of zero friction coatings in end-user industries, High cost of zero friction coatings

-

-

Who are the major players in the Zero Friction Coatings Market?

-

3M Co., AFT Fluorotec Ltd., Akzo Nobel NV, ASV Multichemie Pvt. Ltd., Axalta Coating Systems Ltd., Carl Bechem GmbH, DuPont de Nemours Inc., Endura Coatings, Henkel AG and Co. KGaA, IKV Tribology Ltd., Master Bond Inc., Nippon Paint Holdings Co Ltd., Poeton Industries Ltd., PPG Industries Inc., RPM International Inc., Sandwell UK Ltd., The Chemours Co., The Sherwin Williams Co. and VITRACOAT

-

Market Research Insights

- The market landscape is driven by the need for durable coating solutions across diverse sectors. In transportation system efficiency, coatings for automotive engine components and electric vehicle (EV) components can improve fuel economy by over 5%. For aerospace component protection and heavy-duty machinery protection, these coatings ensure component reliability enhancement.

- Advanced material science is enabling smart coating materials, including self-healing coatings and those with hydrophobic surface treatment and oleophobic surface treatment properties. In sectors from food processing equipment to medical device coatings, precision engineering coatings are vital. The focus is on holistic friction management strategies and tribo-system optimization to achieve operational cost optimization and asset longevity improvement.

- Eco-friendly coating alternatives and sustainable surface solutions are gaining traction, supported by advancements in thin-film coating technology. Evaluating coating performance metrics, including coating adhesion properties, is crucial for high-temperature applications and general engineering solutions, ensuring surface treatment technologies deliver their promised benefits in the energy sector applications and beyond.

We can help! Our analysts can customize this zero friction coatings market research report to meet your requirements.

RIA -

RIA -