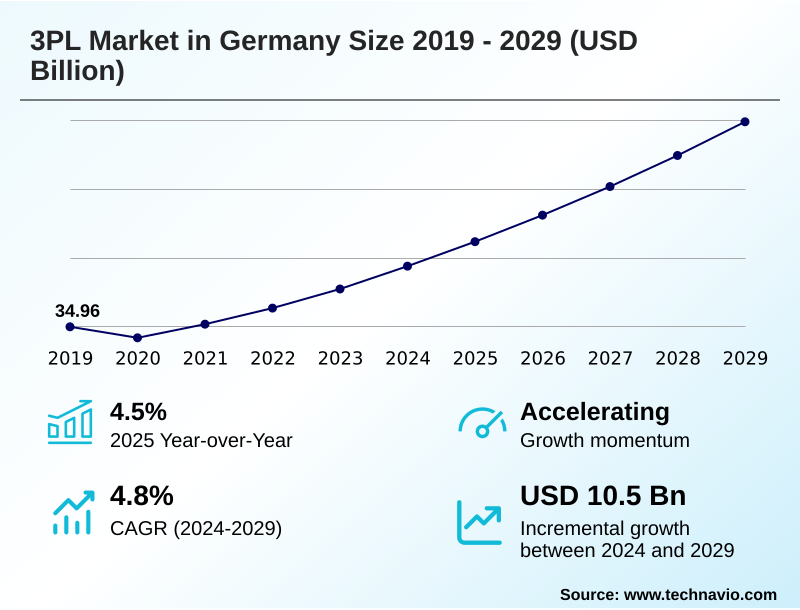

Germany 3PL Market Size 2025-2029

The germany 3pl market size is valued to increase by USD 10.50 billion, at a CAGR of 4.8% from 2024 to 2029. Proliferation of e-commerce and rising consumer expectations will drive the germany 3pl market.

Major Market Trends & Insights

- By End-user - Automotive segment was valued at USD 13.07 billion in 2023

- By Service - Transportation segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 14.91 billion

- Market Future Opportunities: USD 10.50 billion

- CAGR from 2024 to 2029 : 4.8%

Market Summary

- The 3PL Market in Germany is defined by its response to increasing supply chain complexity and the corporate imperative to focus on core business functions. Service providers are no longer just vendors but integral partners in enabling operational resilience and strategic flexibility.

- A key dynamic is the push towards digitalization, where investments in AI, machine learning, and advanced data analytics are becoming standard for optimizing logistics and providing clients with deep supply chain visibility.

- For instance, a manufacturer might leverage a 3PL's predictive analytics platform to anticipate a port delay, rerouting a critical shipment via multimodal transport to avoid a production stoppage, thereby saving significant costs. The market is also heavily influenced by the demands of e-commerce, which requires sophisticated fulfillment services and innovative last-mile delivery solutions.

- Concurrently, providers must navigate persistent challenges like geopolitical instability and capacity constraints, pushing them toward more agile and technologically advanced operational models. The emphasis is shifting from basic transportation and storage to providing intelligent, sustainable, and fully integrated supply chain solutions that drive competitive advantage for clients.

What will be the Size of the Germany 3PL Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Germany 3PL Market Segmented?

The germany 3pl industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Automotive

- Chemical

- Consumer goods

- Healthcare

- Others

- Service

- Transportation

- Warehousing and distribution

- Others

- Method

- Asset-light

- Asset-heavy

- Hybrid

- Geography

- Europe

- Germany

- Europe

By End-user Insights

The automotive segment is estimated to witness significant growth during the forecast period.

The automotive sector's reliance on 3PL for automotive industry is a primary growth drivers for logistics, driven by the need for precision just-in-time logistics and complex just-in-sequence logistics.

This segment demands sophisticated supply chain optimization to manage inbound-to-manufacturing flows from a global supplier base.

Providers are tasked with creating a resilient supply chain strategy and improving logistics efficiency through services like industrial warehousing services, detailed kitting and sequencing, and managing the entire end-to-end supply chain.

The shift to electric vehicles introduces new challenges in hazardous materials transport for batteries, requiring advanced supply chain risk management protocols.

Effective management in this segment has shown to reduce assembly line downtime by over 15%, highlighting the critical role of specialized logistics.

The Automotive segment was valued at USD 13.07 billion in 2023 and showed a gradual increase during the forecast period.

Market Dynamics

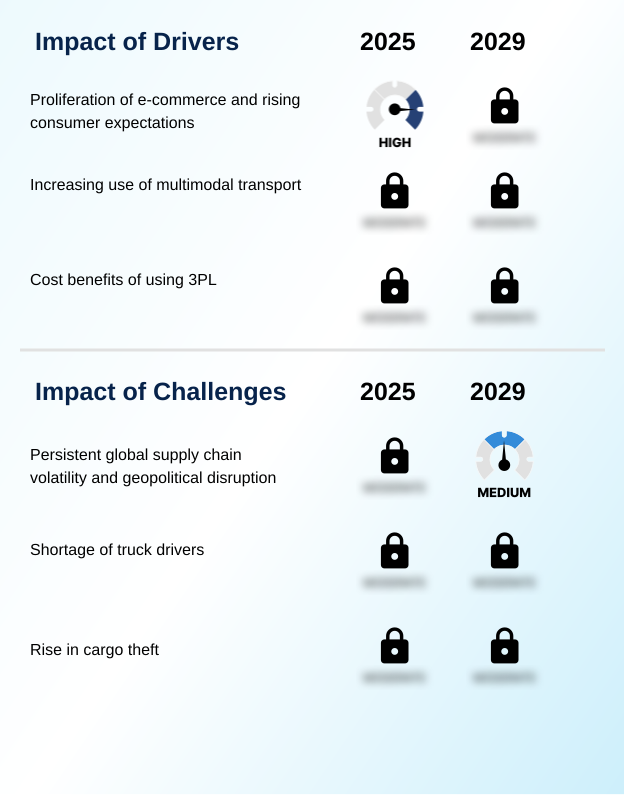

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the logistics sector increasingly revolves around complex questions, such as how does AI improve route optimization in logistics and understanding the benefits of using an asset-light 3PL model. Companies are exploring the best practices for implementing green logistics initiatives to meet both regulatory and consumer demands.

- Simultaneously, they must address the impact of geopolitical disruption on global supply chains by developing a resilient supply chain plan against disruptions. The role of 3PL providers in omnichannel retail success has become central, forcing an evaluation of emerging innovations in last-mile delivery services.

- Internally, operational teams tackle the challenges of implementing just-in-sequence delivery systems and debate choosing between asset-heavy and asset-light 3PL partners. Technology is a key enabler, with firms examining key technologies for achieving end-to-end supply chain visibility and learning how to automate warehouse picking and packing processes.

- The financial imperative is also strong, with a focus on calculating the cost benefits of shifting from unimodal to multimodal transport. For instance, analysis shows that a well-managed multimodal strategy can yield cost reductions upwards of 12% compared to solely relying on road freight for long-haul distribution.

- Specialized needs, such as 3PL solutions for electric vehicle battery transportation and specialized 3PL services for the healthcare and pharma sector, further highlight the market's complexity and the need for expert partners.

What are the key market drivers leading to the rise in the adoption of Germany 3PL Industry?

- The proliferation of e-commerce, coupled with escalating consumer expectations for speed and reliability, serves as the primary driver for market growth.

- The expansion of omnichannel retail logistics is a significant driver, compelling providers to offer sophisticated omnichannel fulfillment and order fulfillment capabilities.

- For the 3PL for consumer goods sector, this means providing integrated fulfillment solutions that seamlessly blend online and offline channels.

- The asset-light logistics model is gaining traction, with companies utilizing freight brokerage services to offer flexible capacity and focus on optimizing transportation costs. This approach has been shown to reduce capital expenditure by up to 40% for shippers.

- Demand for specialized value-added services and precise demand forecasting is also rising. Navigating these dynamics, including persistent challenges in 3PL market, requires providers to deliver adaptable and integrated logistics and freight forwarding solutions.

What are the market trends shaping the Germany 3PL Industry?

- The strategic integration of artificial intelligence and predictive analytics is emerging as a transformative market trend. This development is fundamentally reshaping operational efficiencies and value delivery across the logistics sector.

- A dominant trend is the strategic adoption of AI in logistics management, which is creating a data-driven supply chain focused on logistics cost reduction. The integration of predictive analytics enables proactive disruption management and dynamic routing, improving on-time performance by over 15%.

- In warehousing, the push for warehouse automation and smart warehouse technology is evident, with automated warehouse systems increasing pick-and-pack efficiency by up to 30%. Concurrently, digital freight matching platforms are transforming procurement through enhanced route optimization.

- In the final leg of the supply chain, continuous last-mile delivery innovations are critical for meeting consumer demands for speed and transparency, solidifying the importance of last-mile delivery as a key competitive differentiator.

What challenges does the Germany 3PL Industry face during its growth?

- Persistent global supply chain volatility, intensified by geopolitical disruptions, presents a significant challenge to industry growth and operational stability.

- Managing supply chain volatility remains a primary challenge, necessitating robust resilience planning and complete supply chain visibility. This is particularly critical for specialized sectors like pharmaceutical logistics providers, which depend on flawless cold chain logistics and reliable temperature-controlled shipping. These specialized services often see compliance costs account for 20% of their operational budget.

- Furthermore, complexities in customs brokerage and customs clearance services create significant hurdles in international trade. Managing reverse logistics efficiently is another growing pressure point. Providers must balance asset-heavy logistics investments with flexible hybrid logistics model approaches to offer sustainable supply chain solutions while improving logistics efficiency in a turbulent environment.

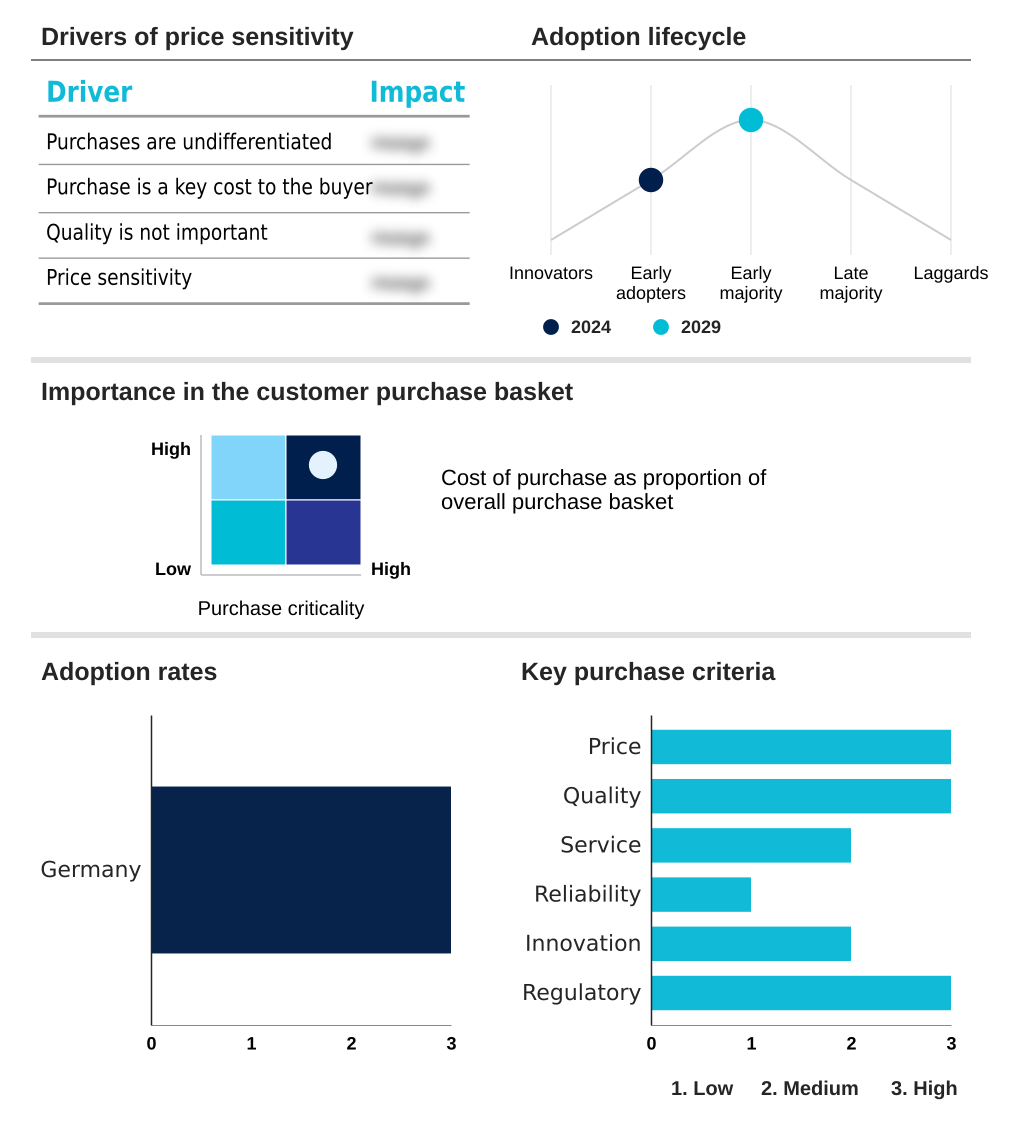

Exclusive Technavio Analysis on Customer Landscape

The germany 3pl market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the germany 3pl market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Germany 3PL Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, germany 3pl market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Agility Public Warehousing Co. - Provides integrated sea, air, and road logistics, including customs services and specialized supply chain solutions tailored to specific industry requirements.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agility Public Warehousing Co.

- AP Moller Maersk AS

- C H Robinson Worldwide Inc.

- CEVA Logistics SA

- CJ Logistics Corp.

- DHL International GmbH

- DSV AS

- Expeditors International Inc.

- FedEx Corp.

- GEODIS

- GXO Logistics Inc.

- J B Hunt Transport Services Inc.

- Kuehne Nagel Management AG

- Nippon Express Holdings Inc.

- Penske Corp.

- Ryder System Inc.

- Schenker AG

- United Parcel Service Inc.

- XPO Inc.

- YUSEN LOGISTICS CO. LTD.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Germany 3pl market

- In September 2024, Schenker AG announced a strategic partnership with a leading AI firm to deploy a predictive analytics platform across its European road freight network, aiming to reduce transit times by 15%.

- In November 2024, DHL International GmbH completed its acquisition of a mid-sized cold-chain logistics specialist, significantly expanding its capabilities for pharmaceutical and healthcare clients in Germany.

- In February 2025, DSV AS launched a new sustainable logistics service featuring a fleet of electric trucks for last-mile delivery in major German metropolitan areas, offering clients a certified low-carbon shipping option.

- In April 2025, C H Robinson Worldwide Inc. opened a new large-scale fulfillment center near the Port of Hamburg, enhancing its e-commerce and omnichannel distribution capacity for the Northern European market.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Germany 3PL Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 190 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.8% |

| Market growth 2025-2029 | USD 10501.8 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 4.5% |

| Key countries | Germany |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's evolution is driven by the integration of advanced technology and a strategic shift towards comprehensive service offerings. Boardroom decisions are increasingly influenced by the need for a resilient end-to-end supply chain, moving beyond cost-cutting to focus on resilience planning and risk mitigation.

- The adoption of predictive analytics for demand forecasting is a critical trend, enabling companies to proactively manage inventory management and optimize operations. Providers are differentiating through specialized capabilities like just-in-time logistics, just-in-sequence logistics, and inbound-to-manufacturing services, supported by robust transportation management systems and warehouse management systems.

- Technologies like digital freight matching and dynamic routing are central to supply chain optimization and route optimization, with some platforms demonstrating the ability to improve asset utilization by over 20%. The market encompasses everything from freight forwarding and customs brokerage to complex contract logistics and lead logistics.

- Specialized areas such as cold chain logistics, green logistics, and reverse logistics are growing in importance, as are value-added services like kitting and sequencing.

- The choice between asset-light logistics, asset-heavy logistics, and a hybrid logistics model is a key strategic consideration for both providers and their clients, who demand integrated logistics and seamless order fulfillment to support cross-border e-commerce and omnichannel fulfillment.

- This requires deep expertise in supply chain consulting and the technological backbone to ensure supply chain visibility and execute efficient last-mile delivery and warehouse automation.

What are the Key Data Covered in this Germany 3PL Market Research and Growth Report?

-

What is the expected growth of the Germany 3PL Market between 2025 and 2029?

-

USD 10.50 billion, at a CAGR of 4.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Automotive, Chemical, Consumer goods, Healthcare, and Others), Service (Transportation, Warehousing and distribution, and Others), Method (Asset-light, Asset-heavy, and Hybrid) and Geography (Europe)

-

-

Which regions are analyzed in the report?

-

Europe

-

-

What are the key growth drivers and market challenges?

-

Proliferation of e-commerce and rising consumer expectations, Persistent global supply chain volatility and geopolitical disruption

-

-

Who are the major players in the Germany 3PL Market?

-

Agility Public Warehousing Co., AP Moller Maersk AS, C H Robinson Worldwide Inc., CEVA Logistics SA, CJ Logistics Corp., DHL International GmbH, DSV AS, Expeditors International Inc., FedEx Corp., GEODIS, GXO Logistics Inc., J B Hunt Transport Services Inc., Kuehne Nagel Management AG, Nippon Express Holdings Inc., Penske Corp., Ryder System Inc., Schenker AG, United Parcel Service Inc., XPO Inc. and YUSEN LOGISTICS CO. LTD.

-

Market Research Insights

- The market is characterized by a strategic shift towards data-driven supply chain models and sustainable supply chain solutions. Third-party logistics providers are leveraging logistics technology platforms to meet the demand for improving logistics efficiency, with leading firms reporting a 15% reduction in fuel consumption through optimized routing.

- The intense focus on logistics cost reduction has accelerated the adoption of outsourced warehousing solutions, which can lower fixed overhead for shippers by over 25%. Furthermore, as companies navigate the challenges in 3PL market, the demand for specialized providers, such as pharmaceutical logistics providers and experts in 3PL for consumer goods, is increasing.

- This specialization is critical for managing complex requirements like temperature-controlled shipping and intricate omnichannel retail logistics.

We can help! Our analysts can customize this germany 3pl market research report to meet your requirements.

RIA -

RIA -