Addisons Disease Therapeutics Market Size 2024-2028

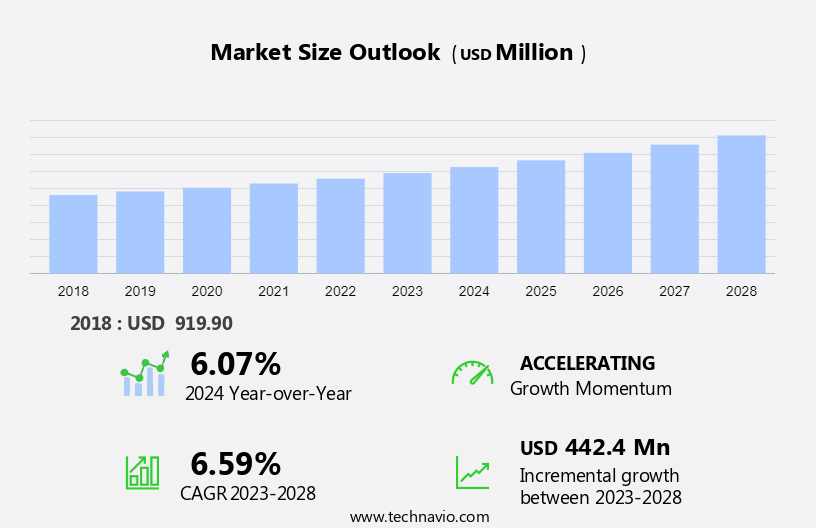

The addisons disease therapeutics market size is forecast to increase by USD 442.4 million at a CAGR of 6.59% between 2023 and 2028.

- Addison's Disease, a chronic and rare endocrine disorder, necessitates continuous medical attention due to its debilitating symptoms. The Addison's Disease Therapeutics Market for this condition is witnessing significant growth, driven by several factors, including the rise of telemedicine and digital health. One such factor is the expansion of research into the development of regenerative therapies. This innovative approach aims to replace the damaged cells In the adrenal glands, thereby offering a potential cure for Addison's Disease. Another growth factor is the increasing number of special drug designations for Addison's Disease treatments. These designations facilitate expedited regulatory approval processes, enabling faster access to effective therapies for patients. However, the delayed diagnosis of Addison's Disease remains a significant challenge, as it often leads to misdiagnosis and inappropriate treatment. This, in turn, increases the disease burden and healthcare costs. Despite these challenges, the market is expected to grow steadily, driven by unmet medical needs and ongoing research efforts.

What will be the Size of the Addisons Disease Therapeutics Market During the Forecast Period?

- The market caters to the unmet needs of chronic disease patients suffering from disorders of the adrenal system, specifically Addison's disease. This condition affects the functioning of the organ systems responsible for producing essential hormones, leading to symptoms such as extreme fatigue, salt cravings, abdominal pains, nausea, and lightheadedness, among others. The market is driven by the increasing prevalence of these disorders and the growing demand for effective treatments. The therapeutic landscape for Addison's disease includes various indications, with hormone replacement therapy being a primary treatment approach. Hospitals, ambulatory surgical centers, and office-based clinics are key end-users In the market.

- Central sleep apnea and obstructive sleep apnea are common comorbidities associated with Addison's disease, further expanding the market scope. The market is witnessing significant pipeline activity, with several potential treatments in various stages of development. The need for effective treatments for acute active infections and the prevention of the Addisonian crisis is a major focus for market participants. The market is not limited to healthcare businesses but also includes non-healthcare entities that cater to the unique needs of Addison's disease patients. Despite advancements In the field, challenges persist, including the need for personalized treatment approaches and the potential for severe gastrointestinal problems and hyperpigmentation as side effects of current treatments.

How is this Addisons Disease Therapeutics Industry segmented and which is the largest segment?

The industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Therapy

- Oral drugs

- Parenteral drugs

- End-user

- Hospitals and clinics

- Diagnostic laboratories

- Geography

- North America

- Canada

- US

- Europe

- Germany

- UK

- Asia

- Japan

- Rest of World (ROW)

- North America

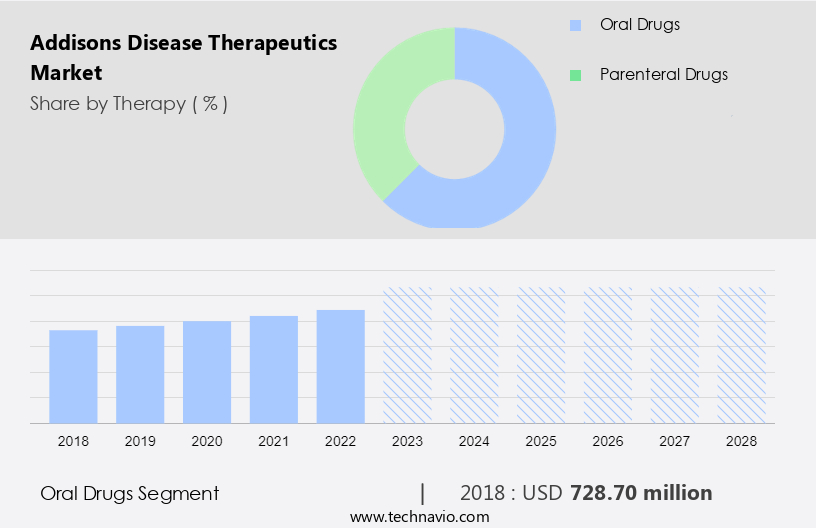

By Therapy Insights

- The oral drugs segment is estimated to witness significant growth during the forecast period.

The oral segment holds a significant market share In the market due to its ease of administration and good patient compliance. Corticosteroids, including hydrocortisone, prednisone, methylprednisone, and fludrocortisone acetate, are commonly used medications for treating adrenal insufficiency. Factors such as the wide availability and ease of administration contribute to the segment's growth. Although generic drugs dominate the market, the introduction of reformulated versions of existing corticosteroid preparations is anticipated to accelerate the segment's expansion. Chronic disease patients, including those with Addisons disease, often face challenges such as canceled or postponed appointments, underdiagnosis, and acute active infections leading to hospitalization. Rising incidences of adrenal insufficiency and growing awareness of the disease are also driving market growth.

However, lack of awareness and the inability to diagnose Addisons disease in its early stages remain significant challenges. Effective treatment is crucial to prevent adrenal crises, which can be life-threatening. The pipeline analysis of innovative drugs, including Recorlev, Levoketoconazole, Tildacerfont, and others, is expected to provide new treatment options for patients. The regulatory framework and rising healthcare expenditure are also influencing market growth. Adrenal tuberculosis, a rare form of tuberculosis affecting the adrenal gland, is a significant indication for the market. Diurnal, a healthcare infrastructure company, focuses on developing hormone replacement therapies for adrenal disorders. The adrenal gland, responsible for producing hormones such as cortisol, aldosterone, and androgens, can be damaged due to autoimmune disorders, infections, or other causes.

Get a glance at the Addisons Disease Therapeutics Industry report of share of various segments Request Free Sample

The oral drugs segment was valued at USD 728.70 million in 2018 and showed a gradual increase during the forecast period.

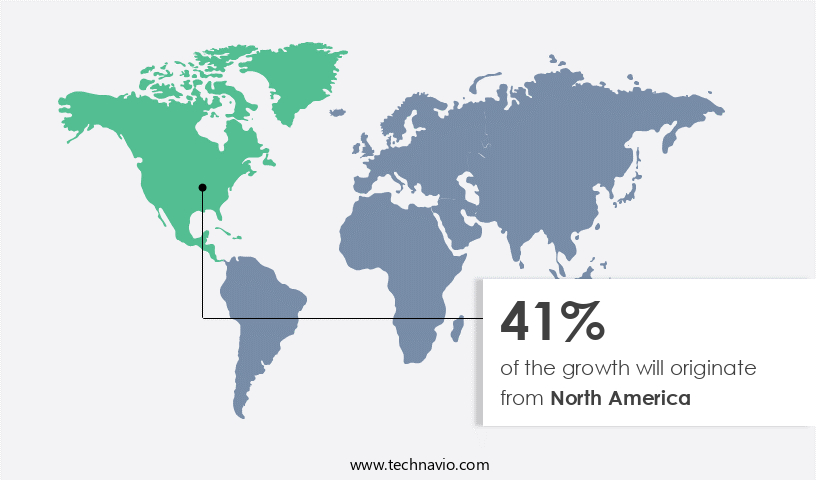

Regional Analysis

- North America is estimated to contribute 41% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

Addison's disease, an endocrine disorder affecting the adrenal gland and resulting in adrenal insufficiency, is gaining significant attention due to rising incidences and growing awareness. Chronic disease patients experience various symptoms such as extreme fatigue, salt craving, abdominal pains, nausea, and Addisonian crisis. Adrenal gland damage can be caused by autoimmune disorders, infections, or tuberculosis, including adrenal tuberculosis. The adrenal system, responsible for producing hormones like cortisol, aldosterone, and androgens, can be affected by various organ systems, leading to acute active infection and hospitalization. The lack of awareness and inability to diagnose Addison disease in its early stages can result in canceled or postponed appointments, underdiagnosis, and adrenal crises.

The market is witnessing growth due to rising healthcare expenditure, innovative drugs, and pipeline analysis. Pharmaceutical companies are developing effective treatment medications, such as corticosteroids like hydrocortisone, prednisone, methylprednisone, and fludrocortisone acetate. Biotech companies are also exploring vaccine development and vaccine candidates, such as hydroxychloroquine, for Addison disease. The regulatory framework is supportive of new drug approvals, with fast-track designation for drugs like Recorlev and Levoketoconazole. Drug delivery systems, genetic testing, and biomarker identification are also being explored to improve patient compliance and outcomes.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Addisons Disease Therapeutics Industry?

Special drug designations is the key driver of the market.

- Addison's Disease, an endocrine disorder characterized by adrenal insufficiency, affects a small population, making it a rare disease. Chronic disease patients suffering from this condition experience symptoms such as extreme fatigue, salt cravings, abdominal pains, nausea, and Addisonian crisis. The disease can be caused by damage to the adrenal gland due to autoimmune disorders, infections, or tuberculosis. However, underdiagnosis remains a significant issue due to the lack of awareness and inability to diagnose in its early stages.

- Effective treatment for Addison's Disease includes hormone replacement therapy with corticosteroids such as hydrocortisone, prednisone, methylprednisone, fludrocortisone acetate, and aldosterone. In some cases, adrenal cortex hypertrophy due to long-term steroid use can lead to granulomas and adrenal crises. The oral segment holds a significant market share In the market, with companies developing innovative drugs using drug delivery systems and genetic testing for better patient compliance and outcomes. The rising incidences of tuberculosis cases and latent tuberculosis infection can lead to adrenal tuberculosis, a significant cause of Addison's Disease.

What are the market trends shaping the Addisons Disease Therapeutics Industry?

Expanding research into the development of regenerative therapy is the upcoming market trend.

- Addison's Disease, a chronic adrenal system disorder, affects the organ systems that produce hormones essential for the body's response to stress and maintaining normal blood pressure. Acute active infections or canceled/postponed appointments can lead to undiagnosed cases, resulting in adrenal insufficiency and potential adrenal crises. The disease is more prevalent in rare disease patients, with rising incidences and growing awareness leading to increased healthcare expenditure. Tuberculosis cases and latent tuberculosis infection are common causes of Addison's disease due to adrenal tuberculosis. Effective treatment involves hormone replacement therapy, including corticosteroids such as hydrocortisone, prednisone, methylprednisone, and fludrocortisone acetate. However, the long-term use of these medications can lead to side effects like muscle weakness, weight loss, and fatigue.

- To address these challenges, researchers are focusing on regenerative therapies, such as hormonal disorder treatments like Recorlev, Levoketoconazole, Tildacerfont, and Hormone replacement therapy. These innovative drugs aim to reduce the duration of treatment and minimize side effects. The regulatory framework for these treatments is evolving, with Fast Track designation and Drug delivery systems like Antares Pharma's Vai auto-injector platform. The market for Addison's Disease therapeutics is significant, with pharmaceutical companies investing in pipeline analysis and vaccine development for various indications, including Central Sleep and Obstructive Sleep Apnea. The market is expected to grow due to rising healthcare expenditure, increasing awareness, and the need for effective treatments for chronic diseases.

What challenges does the Addisons Disease Therapeutics Industry face during its growth?

Delayed diagnosis is a key challenge affecting the industry's growth.

- Addison's disease, a chronic condition affecting the adrenal system, can lead to significant health complications due to the deficiency of cortisol and mineralocorticoids. This endocrine disorder, which primarily affects rare disease patients, can manifest with subtle and nonspecific symptoms such as hyperpigmentation, fatigue, anorexia, orthostasis, nausea, muscle and joint pain, and salt cravings. The gradual onset of these symptoms often results in misdiagnosis, with the disease being mistaken for other conditions. Diagnostic delays can occur at various levels, including the patient, primary care, or secondary care, leading to increased morbidity and mortality due to adrenal crises. The lack of awareness about the disease and its symptoms, as well as the inability to diagnose it promptly, contribute to its underdiagnosis.

- The rising incidences of Addison's disease and growing awareness of the condition are driving the demand for effective treatment medications. The therapeutic market for Addison's disease includes various treatment options such as hydrocortisone, prednisone, methylprednisone, fludrocortisone acetate, and cortisol and aldosterone replacement therapies. The oral segment holds a significant market share, with corticosteroids being the most commonly used medications. However, the high costs and self-reacting autoimmune cells pose challenges to patient compliance and outcomes. The pipeline analysis of Addison's disease therapeutics includes innovative drugs from various pharmaceutical companies. The regulatory framework for these drugs is evolving, with some receiving Fast Track designation and others undergoing clinical trials.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, addisons disease therapeutics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- Actiza Pharmaceutical Pvt. Ltd.

- Akorn Operating Co LLC

- Amgen Inc.

- Amneal Pharmaceuticals Inc.

- Bayer AG

- Bio Techne Corp.

- Biogen Inc.

- Boehringer Ingelheim International GmbH

- Bristol Myers Squibb Co.

- BTL Biotechno Labs Pvt. Ltd.

- Eli Lilly and Co.

- GlaxoSmithKline Plc

- Hikma Pharmaceuticals Plc

- Lupin Ltd.

- Merck and Co. Inc.

- Neurocrine Biosciences Inc.

- Novartis AG

- Pfizer Inc.

- Takeda Pharmaceutical Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Addison's disease, an endocrine disorder characterized by the malfunctioning of the adrenal glands, results in a deficiency of cortisol and aldosterone. This condition can significantly impact an individual's metabolism, immune function, and blood pressure. The disease can manifest in various symptoms, including extreme fatigue, salt cravings, abdominal pains, nausea, and weight loss. The therapeutic market for Addison's disease is driven by several factors. The growing awareness of rare diseases and chronic conditions has led to an increasing focus on effective treatment options. Moreover, the rising healthcare expenditure and the need for hormone replacement therapy have fueled the demand for innovative drugs in this space.

Moreover, the market dynamics of Addison's disease therapeutics are influenced by several factors. The lack of awareness and inability to diagnose the condition in its early stages can lead to complications, including adrenal crises. The disease's complex nature and the need for personalized treatment regimens make it a challenging therapeutic area. The therapeutic landscape for Addison's disease includes various treatment options. Corticosteroids, such as hydrocortisone, prednisone, and methylprednisone, are commonly used to replace the deficient cortisol. Mineralocorticoids, like fludrocortisone acetate, are used to replace aldosterone. Androgens and other medications may also be used to manage symptoms. The market is witnessing significant growth due to the development of innovative drugs.

Despite the progress being made In the development of new treatments, several challenges persist. The high costs of treatment and reimbursement policies can limit access to care for some patients. The self-reacting autoimmune cells that contribute to the disease can make treatment challenging, and drug misuse can further complicate matters.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

166 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.59% |

|

Market Growth 2024-2028 |

USD 442.4 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.07 |

|

Key countries |

US, Germany, UK, Japan, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the industry during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the market growth of industry companies

We can help! Our analysts can customize this market research report to meet your requirements.

RIA -

RIA -