Aerospace Composite Market Size 2024-2028

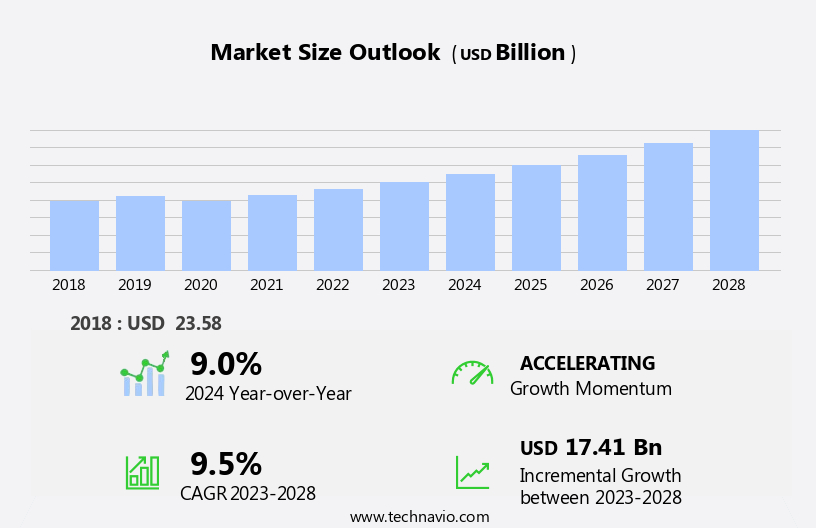

The aerospace composite market size is forecast to increase by USD 17.41 billion, at a CAGR of 9.5% between 2023 and 2028.

- The market is driven by the increasing demand for weight reduction and fuel efficiency in aircraft. This trend is propelled by the growing focus on reducing carbon emissions and improving overall aircraft performance. Another key driver is the rising adoption of carbon fiber-reinforced plastic composites in aircraft components. These materials offer superior strength-to-weight ratio, making them an ideal choice for manufacturing lightweight and durable aircraft parts. However, the market faces challenges as well. Complexity issues related to repair and maintenance of composite materials pose a significant obstacle. The intricate nature of these materials makes it difficult to identify and address damages, leading to prolonged downtime and increased operational costs for airlines.

- Companies seeking to capitalize on market opportunities must invest in developing innovative solutions for the repair and maintenance of composite materials. This will not only help them meet the growing demand for fuel-efficient and lightweight aircraft but also provide a competitive edge in the market.

What will be the Size of the Aerospace Composite Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by the relentless pursuit of performance enhancement and innovation in this dynamic industry. Vacuum bagging and high-modulus materials are essential tools in the production of aircraft fuselages, pushing the boundaries of corrosion resistance, fuel efficiency, and airworthiness certification. The integration of bio-based composites and smart composites adds a new dimension to this sector, with thermal stability and high-strength materials ensuring the longevity and reliability of components. In the realm of commercial aircraft, lightweight materials such as carbon fiber composites and epoxy resins are increasingly utilized, contributing to weight reduction and improved fuel efficiency.

Meanwhile, the aerospace supply chain benefits from design optimization and structural bonding, ensuring the efficient production of complex components. Satellite components, rotor blades, and aircraft wings are all reaping the benefits of advanced materials, with thermoset resins, thermoplastic resins, and aramid fiber composites playing crucial roles. The integration of resin transfer molding, filament winding, and layup techniques further enhances the versatility of these materials. The aerospace manufacturing landscape is characterized by rigorous testing, including mechanical testing, fatigue testing, and non-destructive testing, to ensure structural integrity and adherence to aerospace regulations. The ongoing development of recycling technologies and sustainability considerations underscores the industry's commitment to environmental responsibility.

Unmanned aerial vehicles, business jets, and aircraft tail sections are all part of the diverse applications of high-performance composites, pushing the boundaries of innovation and performance in the aerospace sector. The future of this market is marked by continuous evolution and the integration of new technologies and materials, ensuring its ongoing relevance and importance in the global economy.

How is this Aerospace Composite Industry segmented?

The aerospace composite industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Exteriors

- Interiors

- Application

- Commercial aircraft

- Military aircraft

- Business and general aviation

- Civil helicopters

- Fiber Type

- Carbon Fiber

- Glass Fiber

- Aramid Fiber

- Others

- Manufacturing Process

- ATL or AFP

- Filament Winding

- Resin Transfer Molding

- Hand Layup

- Others

- Geography

- North America

- US

- Europe

- France

- Germany

- APAC

- China

- Japan

- Rest of World (ROW).

- North America

By Type Insights

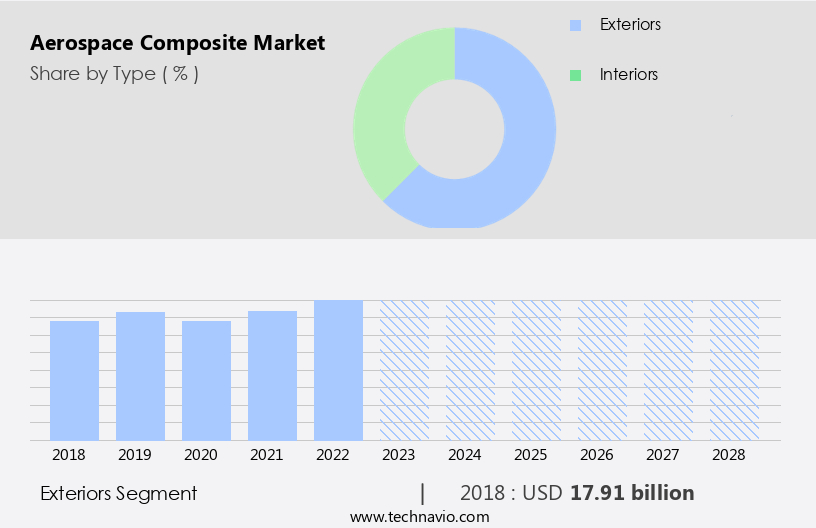

The exteriors segment is estimated to witness significant growth during the forecast period.

Composites are a crucial element in enhancing the exterior structures of aircraft, leading to increased efficiency, performance, and durability. Carbon fiber-reinforced composites, with their high strength-to-weight ratio, are extensively utilized in fuselages, such as Boeing's 787 Dreamliner. These advanced composite materials significantly reduce overall aircraft weight, contributing to improved fuel efficiency. Composites also find extensive applications in wings and wing components, like Airbus' A350 XWB, which boasts a substantial percentage of composite materials. This application ensures the necessary structural strength while maintaining lightweight wings. Moreover, composites are frequently employed in aircraft tail sections, including horizontal and vertical stabilizers, due to their structural benefits, contributing to enhanced overall performance and fuel efficiency.

Additionally, composites are utilized in various other aerospace components, such as rotor blades, satellite components, and aircraft repair, among others. Innovations in composites include high-modulus materials, self-healing composites, smart composites, and recycling technologies, which further expand their applications in the aerospace industry. The aerospace supply chain relies on design optimization, structural bonding, and non-destructive testing to ensure the highest standards of airworthiness certification. Composites undergo rigorous mechanical testing, including fatigue testing, impact testing, and environmental testing, to maintain structural integrity. The aerospace manufacturing process incorporates advanced techniques like resin transfer molding, autoclave processing, filament winding, and 3D printing to create high-performance composites.

The use of composites in commercial and military aircraft, business jets, and unmanned aerial vehicles continues to evolve, with a focus on sustainability considerations and weight reduction.

The Exteriors segment was valued at USD 17.91 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

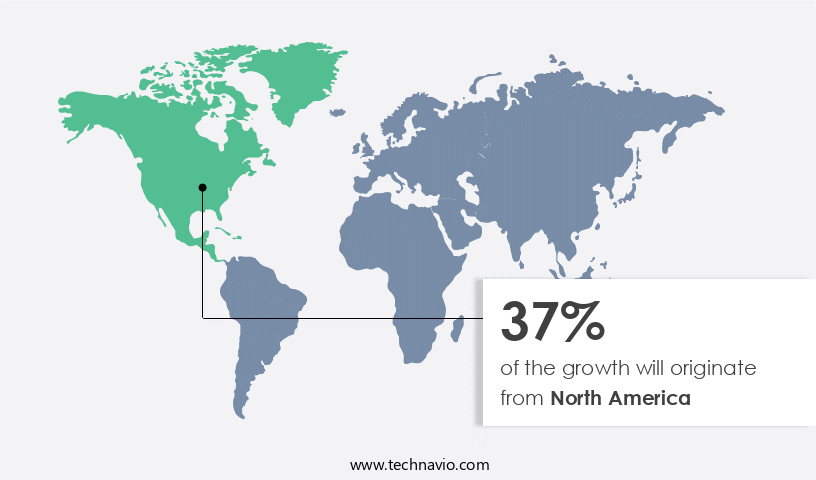

North America is estimated to contribute 37% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is driven by the widespread adoption of composite materials in the production of aircraft and spacecraft components. North America, specifically the US and Canada, lead this market due to the emphasis on lightweight, high-strength composites for improved fuel efficiency and performance in aviation. Key players in the region, such as Boeing and Lockheed Martin, are major consumers of composite materials, with Boeing's B787 Dreamliner being a prime example. This aircraft utilizes extensive composite usage, contributing to its structural integrity, thermal stability, and reduced weight. The aerospace industry in North America is at the forefront of technological innovation, with advancements in high-modulus materials, prepreg technologies, and vacuum bagging techniques.

Additionally, the use of smart composites, self-healing materials, and recycling technologies is gaining traction. The market also encompasses the manufacturing of satellite components, rotor blades for helicopters and wind turbines, and aircraft tail sections. Aerospace regulations mandate rigorous testing for airworthiness certification, including fatigue testing, impact testing, and environmental testing, to ensure structural integrity. Innovation in composites continues through processes like resin transfer molding, compression molding, filament winding, and 3D printing. The integration of bio-based composites and thermoplastic resins further expands the market's scope. Sustainability considerations are increasingly important, with a focus on reducing weight and optimizing design for fuel efficiency.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Aerospace Composite Industry?

- The escalating need for weight reduction and enhanced fuel efficiency in the aviation industry serves as the primary market driver.

- The market is experiencing significant growth due to the increasing demand for lighter and more fuel-efficient aircraft. This trend is driven by the need to comply with environmental regulations and reduce the environmental impact of air travel. Aerospace composites, such as glass fiber and aramid fiber composites, offer superior strength-to-weight ratios, making them ideal for manufacturing lighter aircraft components while maintaining structural integrity. Performance enhancement is a key focus area, with composite materials being used in the production of aircraft fuselages, rotor blades, and other critical components. Mechanical testing and life cycle analysis are essential in ensuring the durability and airworthiness certification of these components.

- Prepreg materials are widely used in the production of aerospace composites due to their consistency and ease of use. Additionally, composite repair technologies are gaining popularity for their ability to extend the life of existing aircraft components and reduce the need for costly replacements. Overall, the market is expected to continue growing as manufacturers seek to improve the fuel efficiency and sustainability of their aircraft offerings.

What are the market trends shaping the Aerospace Composite Industry?

- The use of carbon fiber-reinforced plastic composites in aircraft components is a significant market trend, gaining increasing adoption due to their lightweight and high-strength properties. This material's growing popularity is expected to drive market growth in the aerospace industry.

- The market is experiencing significant growth due to the increasing adoption of carbon fiber-reinforced polymer (CFRP) composites in aircraft manufacturing. CFRP composites offer superior thermal stability and high strength, making them an ideal choice for producing lightweight and durable components for commercial aircraft. These composites provide design flexibility, enabling the creation of complex and aerodynamic structures that optimize component efficiency and performance. Moreover, the use of CFRP composites contributes to weight reduction, which is a critical factor in reducing fuel consumption and emissions. This aligns with the aviation industry's focus on environmental sustainability.

- Additionally, the development of advanced materials such as high-modulus fibers, smart composites, and bio-based composites is further driving market growth. These materials offer enhanced properties, such as self-healing capabilities and improved thermal stability, making them suitable for use in satellite components and other aerospace applications. Structural bonding and vacuum bagging techniques are also gaining popularity in the aerospace supply chain, as they enable the production of high-quality, strong bonds between composite materials. The use of these techniques facilitates the production of complex components with intricate geometries and high-performance requirements. Overall, the market is expected to continue growing due to the increasing demand for lightweight, high-performance materials in the aviation industry.

What challenges does the Aerospace Composite Industry face during its growth?

- The growth of the industry is impeded by the intricate complexities surrounding the repair and maintenance of composite materials. These challenges, which are of significant concern to professionals, necessitate ongoing research and innovation to ensure efficient and effective solutions are implemented.

- The market faces complexities in repair and maintenance due to the intricate structure of composite materials, such as carbon fiber composites and epoxy resins, used in aerospace manufacturing for high-performance applications. These materials offer advantages like high strength-to-weight ratios and corrosion resistance, but their non-destructive testing poses challenges. Unlike metals, composites can conceal internal damage, including delamination and cracks, which may go undetected without advanced inspection techniques like ultrasonic or thermographic methods. This complicates the maintenance process in the aerospace industry.

- Aerospace regulations mandate strict structural integrity for aircraft wings and spacecraft structures, necessitating rigorous fatigue testing and environmental testing to ensure safety. Hybrid composites, which combine the benefits of multiple materials, are gaining popularity to address these challenges. Innovation in composites continues to drive advancements in the industry, with ongoing research focused on improving inspection techniques and developing more durable and sustainable materials.

Exclusive Customer Landscape

The aerospace composite market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the aerospace composite market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, aerospace composite market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Albany International Corp. - The company specializes in the production of advanced aerospace composite materials. Our product portfolio encompasses Composite Cans and Tubes, Fan Blade Platforms, Fan Blades, Fan Cases, Fuselage Frames, Waste Tanks, Airstrut, and Hydraulic Pressure Accumulators. These components cater to the aviation industry's demanding requirements for lightweight, durable, and high-performance solutions. Our commitment to innovation drives US to continually refine and improve our offerings, enhancing their functionality and contributing to the overall efficiency of aircraft designs.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Albany International Corp.

- Bally Ribbon Mills

- General Electric Co.

- Hexcel Corp.

- Kineco Kaman Composites

- Lee Aerospace Inc.

- Materion Corp.

- Mitsubishi Chemical Group Corp.

- Owens Corning

- Plastic Reinforcement Fabrics Ltd.

- Renegade Materials Corp.

- Rolls Royce Holdings Plc

- SGL Carbon SE

- Sunshield Chemicals Ltd.

- Spirit AeroSystems Inc.

- Teijin Ltd.

- Toray TCAC Holding B.V.

- Victrex Plc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Aerospace Composite Market

- In February 2024, Boeing and Hexcel Corporation announced a significant collaboration to increase the production capacity of composite materials for Boeing's 787 Dreamliner aircraft. This strategic partnership aimed to enhance Boeing's supply chain resilience and meet the growing demand for composite materials in the aerospace industry (Boeing Press Release, 2024).

- In May 2024, Airbus and Safran announced the successful first flight of their new-generation regional jet, the A220, featuring advanced composite materials in its fuselage and wings. This technological advancement reduced the aircraft's weight, improved fuel efficiency, and increased passenger comfort (Airbus Press Release, 2024).

- In August 2024, Teijin Limited, a leading Japanese composite materials manufacturer, announced a strategic investment of USD100 million in its US subsidiary, Teijin Carbon Fibers, Inc. This investment aimed to expand the company's carbon fiber production capacity and strengthen its position in the North American the market (Teijin Limited Press Release, 2024).

Research Analyst Overview

- The market experiences continuous evolution, driven by stringent safety regulations and the pursuit of lighter, stronger, and more sustainable materials. Quality control plays a crucial role in ensuring consistency and reliability in manufacturing processes, while environmental impact and sustainability assessment are increasingly important considerations. Maintenance procedures, including vibration analysis and life cycle management, are essential for optimizing fleet performance and reducing downtime. Failure analysis and damage tolerance are critical for understanding the root causes of composite part failures and designing safer, more robust structures. Safety regulations mandate rigorous testing and certification, driving the adoption of advanced simulation tools, manufacturing automation, and joining technologies.

- Carbon footprint reduction is a key focus, with industry standards promoting the use of circular economy principles, fatigue life prediction, and production efficiency. Manufacturing cost optimization is achieved through process automation, material characterization, and the implementation of industry-standard stress analysis and composite design software. Surface finishing, acoustic analysis, and thermal analysis are essential for optimizing composite part performance and reducing noise and heat emissions. Fastening systems and joining technologies are continually evolving to meet the demands of high-performance aerospace applications, while sustainability initiatives are driving the development of new, eco-friendly manufacturing methods. Overall, the market is characterized by dynamic innovation and a relentless focus on safety, efficiency, and sustainability.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Aerospace Composite Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

160 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 9.5% |

|

Market growth 2024-2028 |

USD 17.41 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

9.0 |

|

Key countries |

US, China, Japan, Germany, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Aerospace Composite Market Research and Growth Report?

- CAGR of the Aerospace Composite industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the aerospace composite market growth of industry companies

We can help! Our analysts can customize this aerospace composite market research report to meet your requirements.

RIA -

RIA -