Agriculture Equipment Market Size 2024-2028

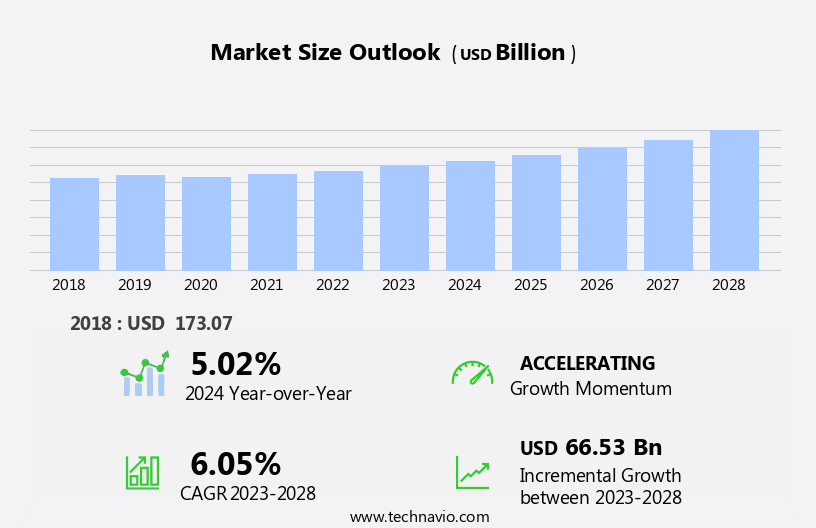

The agriculture equipment market size is forecast to increase by USD 66.53 billion at a CAGR of 6.05% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing demand for labor-saving technologies as a result of the persistent labor shortage in the agricultural sector. This trend is driving the market as farmers seek to increase productivity and efficiency on their farms. Another key driver is the implementation of Artificial Intelligence (AI) in agriculture equipment, which is revolutionizing farming practices by enabling precision farming, automated crop monitoring, and real-time analysis of soil and weather conditions. Furthermore, the growing availability of rental agricultural equipment is providing farmers with flexible access to advanced technology and reducing the upfront costs of equipment ownership.

- However, the market faces challenges such as high initial investment costs for advanced technology and the need for significant infrastructure upgrades to support the integration of AI in farming operations. Additionally, regulatory compliance and data security concerns pose challenges for market players, requiring them to invest in robust IT systems and adhere to strict data privacy regulations. Companies seeking to capitalize on market opportunities and navigate challenges effectively should focus on developing innovative solutions that address the specific needs of farmers, while also ensuring compliance with regulatory requirements and maintaining strong cybersecurity measures.

What will be the Size of the Agriculture Equipment Market during the forecast period?

- The market continues to evolve, driven by advancements in technology and shifting farming practices. Commercial farms and small-scale operations alike embrace precision agriculture technology, integrating GPS guidance, variable rate application, and satellite imagery for optimized crop production. Organic farming practices gain traction, with the adoption of no-till farming and conservation tillage promoting soil health and sustainability. Remote sensing and agricultural robotics revolutionize land management, enabling real-time crop health monitoring and emissions reduction. Irrigation systems and crop science advancements contribute to increased farm efficiency and food security. The dealer network adapts to these changes, offering financing options and parts and service for the latest equipment.

- Farm labor and agricultural finance remain crucial components, with farm management software streamlining operations and agricultural research driving innovation. Sustainable farming practices, including sustainable agriculture and sustainable farming practices, gain importance in the face of evolving regulations and consumer demand. Emissions reduction and fuel efficiency are key concerns, with the integration of machine learning and artificial intelligence in agricultural development. The ongoing unfolding of market activities reveals a dynamic industry that seamlessly integrates crop science, farm efficiency, and agricultural research to meet the needs of modern farming operations.

How is this Agriculture Equipment Industry segmented?

The agriculture equipment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

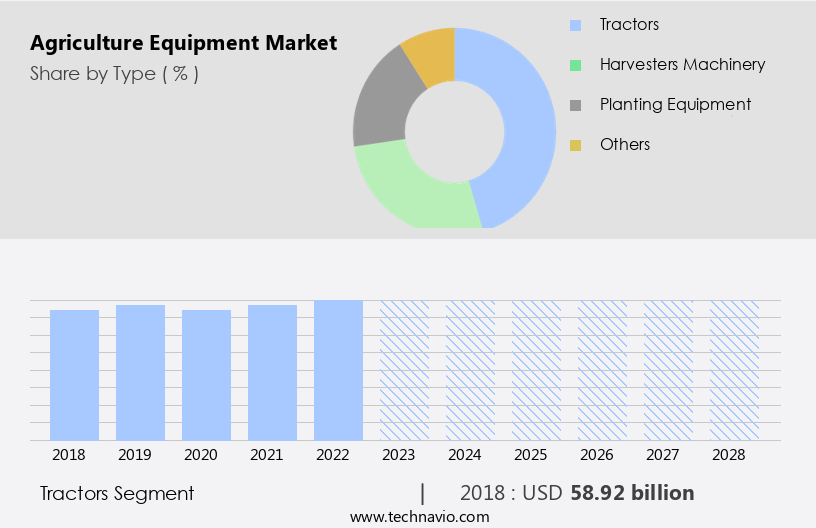

- Type

- Tractors

- Harvesters machinery

- Planting equipment

- Others

- Product Type

- Manual

- Automatic

- Semi-automatic

- Application

- Land Development

- Crop Cultivation

- Harvesting

- Post-Harvest Processing

- End-User

- Large-Scale Farms

- Small and Medium Farms

- Agricultural Cooperatives

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Type Insights

The tractors segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant trends as farmers adopt advanced technologies to enhance crop health monitoring, comply with agricultural regulations, and improve weather forecasting for optimal land management. Small farms are increasingly adopting precision agriculture practices, including variable rate application, GPS guidance, satellite imagery, and conservation tillage, to boost farm efficiency and reduce emissions. Commercial farms are investing in large-scale equipment for planting, harvesting, and irrigation systems, while family farms focus on sustainable agriculture practices, such as organic farming and crop rotation, to maintain farmland values and promote food security. Advancements in precision farming technology, including remote sensing, agricultural robotics, and farm management software, are driving the demand for sophisticated, larger, and more powerful tractors.

However, the market is also witnessing a rise in demand for smaller, specialized tractors for specific applications, such as no-till farming and hay equipment, which can fit into tight spaces and narrow rows. These tractors, including wheeled and crawler types, offer advantages in certain conditions due to their simplicity and maneuverability. Farmers are also adopting new technologies to optimize crop production, such as genetically modified organisms, seed technology, and yield monitoring, to enhance crop science and improve yield optimization. Additionally, farmers are focusing on reducing fuel efficiency and implementing sustainable farming practices, such as conservation tillage and crop rotation, to minimize their environmental footprint and promote long-term agricultural development.

The dealer network plays a crucial role in the market, providing parts and service to farmers and ensuring equipment maintenance and safety. Agricultural finance and lease agreements are also essential for farmers to acquire the latest equipment and technology, enabling them to remain competitive and profitable in the industry. Overall, the market is evolving to meet the changing needs of farmers, with a focus on innovation, sustainability, and efficiency.

The Tractors segment was valued at USD 58.92 billion in 2018 and showed a gradual increase during the forecast period.

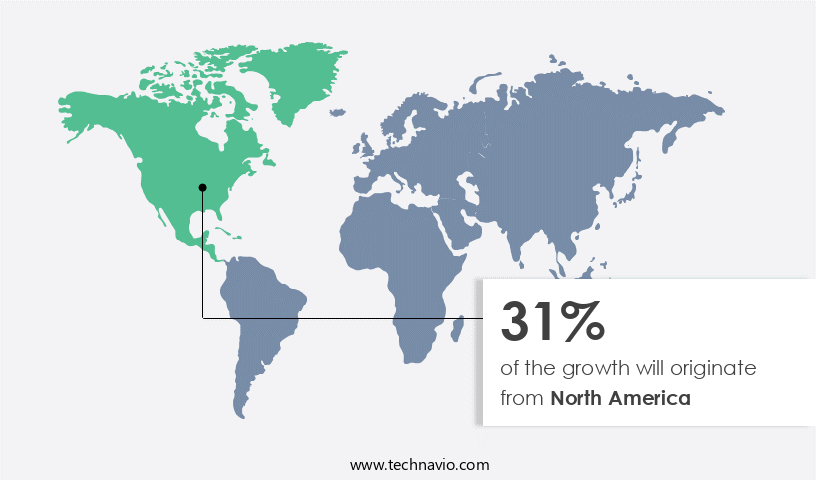

Regional Analysis

North America is estimated to contribute 31% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America, encompassing the United States and Canada, experiences significant growth driven by government initiatives and labor shortages. Farmers in these countries receive financial assistance from various agricultural bodies and governments, including the USDA's Farm Service Agency, which offers direct farm operating loans of up to USD400,000. This mechanization of agriculture is further facilitated by advancements in technology, such as precision agriculture, remote sensing, and agricultural robotics. These technologies enable farmers to optimize crop yields, reduce emissions, and improve farm efficiency through practices like variable rate application, GPS guidance, satellite imagery, and soil sensors.

Additionally, the market is influenced by the increasing trend towards sustainable farming practices, including no-till farming, conservation tillage, and organic farming. Farmers are also adopting advanced farm management software, crop production techniques, and agricultural data management systems to enhance their operations. Commercial and family farms alike invest in farm machinery, lease agreements, and equipment maintenance to keep up with the demands of modern agriculture. The market for agriculture equipment is vast, encompassing planting and harvesting equipment, irrigation systems, fuel efficiency technologies, and livestock farming equipment. As the market continues to evolve, agricultural research, plant breeding, and artificial intelligence play crucial roles in driving innovation and improving farm productivity.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Agriculture Equipment Industry?

- The labor shortage leading to a surge in demand for agricultural equipment serves as the primary market driver.

- The agricultural sector, a significant employer for the global rural population, faces a labor shortage issue. This trend is prevalent in countries like India and South Africa, where urban migration has led to a decrease in the availability of agricultural labor. In the US, rural areas, particularly in Ohio and Pennsylvania, experience acute labor shortages, with many local workers disinterested in farm-related work. Consequently, labor costs have risen, driving small farm holders to invest in agriculture machinery. Advancements in technology are also influencing the agriculture sector. Precision farming, crop protection, and livestock farming have seen significant growth due to the adoption of farm management software, agricultural data management, and sustainable farming practices.

- Artificial intelligence, machine learning, and data analytics are being integrated into farming operations to optimize crop production and improve farmland values. Moreover, the implementation of sustainable farming practices is gaining traction, with farmers focusing on crop rotation and other eco-friendly methods to reduce their carbon footprint. Farm equipment financing options are also becoming more accessible, making it easier for farmers to invest in modern machinery. Overall, the agriculture sector is undergoing a transformation, driven by labor shortages, technological advancements, and a shift towards sustainable farming practices.

What are the market trends shaping the Agriculture Equipment Industry?

- The integration of artificial intelligence (AI) technology in agriculture equipment is an emerging market trend. This innovation aims to enhance the efficiency and productivity of farming operations.

- Artificial intelligence (AI) is revolutionizing the agriculture sector with advanced equipment that enhances crop production and real-time monitoring. AI technology enables automated systems, such as self-driving tractors and drones, to optimize land management through variable rate application, GPS guidance, satellite imagery, and weather forecasting. These technologies promote sustainable agriculture practices like no-till farming, conservation tillage, and organic farming. AI implementation in self-driving combines ensures safety and continuous learning through self-collected data. Crop health monitoring and soil content sensing improve overall farm productivity.

- Agricultural regulations are increasingly emphasizing the importance of these advanced technologies to maintain crop health and ensure regulatory compliance. Farm subsidies and incentives may encourage small farm adoption of AI-based agriculture equipment. AI technology is a game-changer in agriculture, offering significant benefits to farmers through increased efficiency, productivity, and sustainability.

What challenges does the Agriculture Equipment Industry face during its growth?

- The expansion of rental agricultural equipment options poses a significant challenge to the industry's growth trajectory.

- Agriculture equipment plays a vital role in the productivity and efficiency of commercial farms, encompassing a range of machinery such as tractors, harvesting tools, mower conditioners, tillage tools, and irrigation systems. However, the high cost of purchasing and maintaining this equipment poses a challenge for farmers, particularly those employing organic farming practices and focusing on farm efficiency, emissions reduction, and agricultural development. To address this challenge, the rental market for agriculture equipment has gained traction. Farmers can rent equipment for specific periods, enabling them to offset the expense of maintenance and obtain the latest precision agriculture technology, including remote sensing and agricultural robotics, to optimize crop science and farm labor.

- Lease agreements offer farmers the flexibility to access advanced farm machinery without the need for substantial upfront payments. Agricultural finance institutions facilitate the leasing process, providing farmers with financial solutions tailored to their unique needs. This not only enhances farm efficiency but also ensures farmers can invest in other areas crucial to their business growth. Overall, the agriculture equipment rental market caters to the evolving needs of farmers, allowing them to stay competitive while maintaining financial stability.

Exclusive Customer Landscape

The agriculture equipment market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the agriculture equipment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, agriculture equipment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Deere & Company (United States) - The company specializes in agriculture equipment, providing innovative solutions through renowned brands such as Challenger, Fendt, Massey Ferguson, Valtra, Fella, White Planters, and Sunflower. Our extensive product range includes tractors and feeders, catering to diverse farming needs. These brands are recognized globally for their quality, reliability, and advanced technology. By offering these solutions, we aim to enhance agricultural productivity and efficiency, ultimately contributing to sustainable farming practices.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Deere & Company (United States)

- CNH Industrial (United Kingdom)

- AGCO Corporation (United States)

- Kubota Corporation (Japan)

- Mahindra & Mahindra (India)

- CLAAS KGaA (Germany)

- Escorts Limited (India)

- Yanmar Holdings (Japan)

- Bucher Industries (Switzerland)

- SDF Group (Italy)

- Alamo Group (United States)

- Iseki & Co. (Japan)

- Daedong Industrial (South Korea)

- Lovol Heavy Industry (China)

- Exel Industries (France)

- JCB (United Kingdom)

- Tafe (India)

- Zoomlion Heavy Industry (China)

- Argo Tractors (Italy)

- Kinze Manufacturing (United States)

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Agriculture Equipment Market

- In January 2024, John Deere, a leading agriculture equipment manufacturer, introduced its new precision farming solution, "SmartFarm 3.0." This advanced technology offers real-time data analysis and predictive maintenance, aiming to boost farm productivity and efficiency (John Deere Press Release).

- In March 2025, AGCO and CNH Industrial, two major agriculture equipment players, announced a strategic partnership to jointly develop electric and autonomous farm equipment. This collaboration aims to reduce emissions and enhance farming efficiency, setting new industry standards (CNH Industrial & AGCO Press Release).

- In July 2024, Trimble, a technology provider, acquired MuleSoft for approximately USD1.4 billion. This acquisition will enable Trimble to integrate its agriculture software solutions with other business systems, providing farmers with a more comprehensive and seamless digital farming experience (Trimble Press Release).

- In October 2025, the European Union approved the new Common Agricultural Policy (CAP) for the 2023-2027 period. The new policy includes a significant investment in digital agriculture, with a focus on precision farming, satellite technology, and data management, aiming to increase the competitiveness and sustainability of European agriculture (European Commission Press Release).

Research Analyst Overview

In the dynamic agriculture sector, digital agriculture is revolutionizing farming practices with advanced technologies such as robotic harvesting, gene editing, and agricultural analytics. Soil health monitoring is a critical aspect of digital agriculture, ensuring sustainable food production through the use of agricultural sensor networks and IoT. Agricultural biotechnology, including crop genomics and yield prediction, is another key trend, driving innovation in climate-smart agriculture. Farm automation, urban agriculture, and vertical farming are transforming the agricultural landscape, enabling local food production and reducing the carbon footprint of the agricultural supply chain. Smart farming, farm management apps, and agricultural data platforms are streamlining farm operations, improving farm risk management, and enhancing farm insurance offerings.

Precision spraying, variable rate seeding, and carbon sequestration are essential components of sustainable farming practices, ensuring efficient use of resources and reducing environmental impact. Regenerative agriculture and food security solutions are gaining traction as farmers seek to mitigate climate risks and ensure long-term sustainability. The integration of greenhouse technology, farm automation, and agricultural IoT is enabling farmers to optimize crop growth and minimize waste, while farm management apps and agricultural data platforms provide real-time insights into farm operations. Overall, these trends are shaping the future of agricultural economics and ensuring a more resilient and sustainable food production system.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Agriculture Equipment Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

160 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.05% |

|

Market growth 2024-2028 |

USD 66.53 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.02 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Egypt, Oman, Argentina, KSA, UAE, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Agriculture Equipment Market Research and Growth Report?

- CAGR of the Agriculture Equipment industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the agriculture equipment market growth of industry companies

We can help! Our analysts can customize this agriculture equipment market research report to meet your requirements.

RIA -

RIA -