AI For Debt Collection Market Size 2025-2029

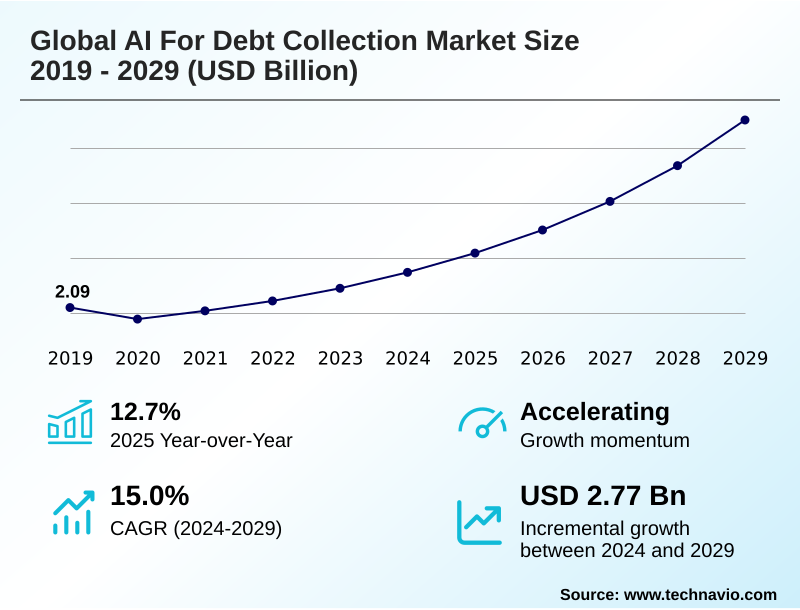

The ai for debt collection market size is valued to increase by USD 2.77 billion, at a CAGR of 15% from 2024 to 2029. Increasing operational efficiency and cost reduction will drive the ai for debt collection market.

Major Market Trends & Insights

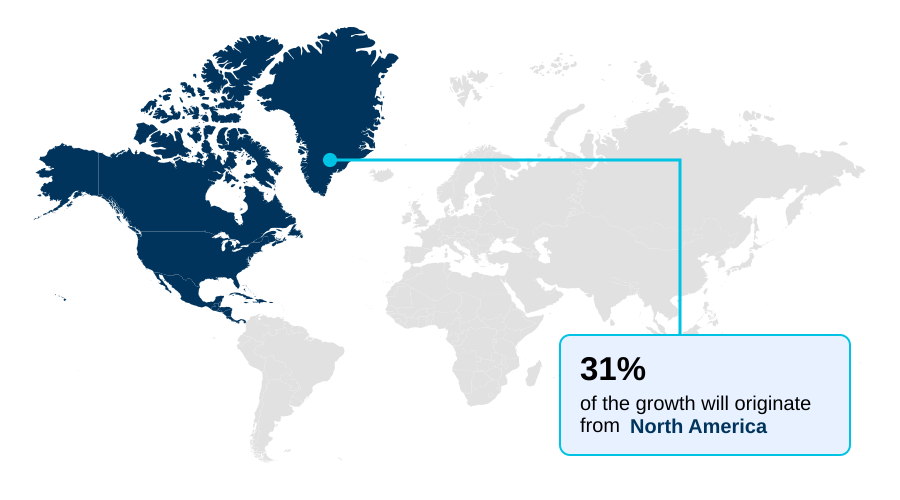

- North America dominated the market and accounted for a 31.3% growth during the forecast period.

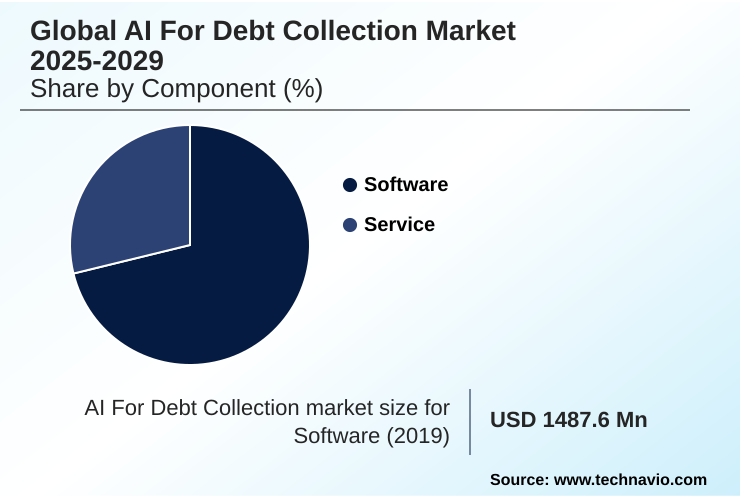

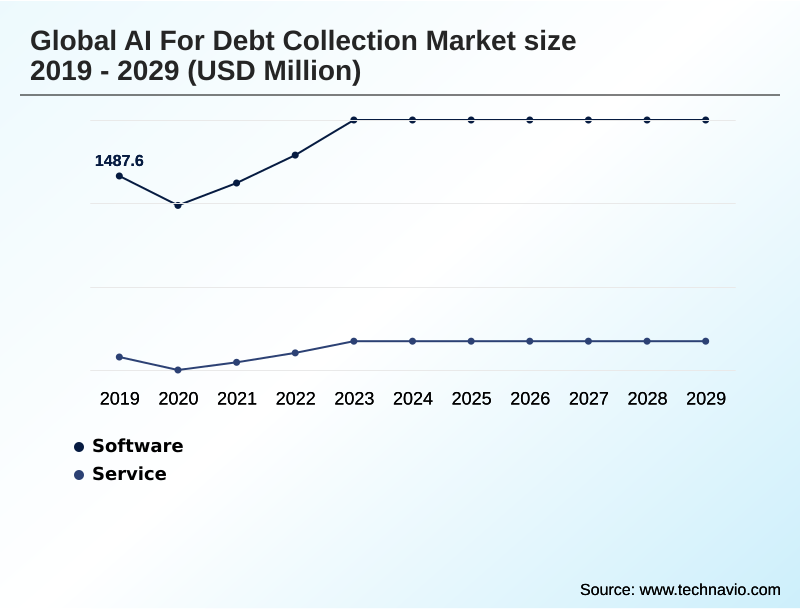

- By Component - Software segment was valued at USD 1.76 billion in 2023

- By Deployment - Cloud-based segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 3.41 billion

- Market Future Opportunities: USD 2.77 billion

- CAGR from 2024 to 2029 : 15%

Market Summary

- The AI For Debt Collection Market is rapidly evolving, driven by the need for financial institutions to enhance operational efficiency and adopt more customer-centric recovery strategies. The market leverages artificial intelligence technologies like machine learning models and natural language processing to transform traditional, labor-intensive collection processes.

- Key drivers include the significant cost reductions achieved through AI-driven automation of routine tasks and the ability to improve customer experience with personalized debt collection communication. Trends such as the increasing sophistication of predictive analytics for debt collection and generative AI in debt collection are enabling more accurate debtor behavior prediction and empathetic engagement.

- For instance, a financial institution can utilize AI for debt collection platforms to analyze a debtor's communication history and financial patterns, automatically offering a tailored repayment plan through a debt collection chatbot instead of a generic notice, significantly increasing the likelihood of successful resolution.

- However, the market faces challenges related to data privacy, integration complexity with legacy systems, and the critical need for ethical AI deployment in debt collection to avoid algorithmic bias and maintain regulatory compliance. This focus on AI compliance in financial services is crucial for sustainable growth.

What will be the Size of the AI For Debt Collection Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI For Debt Collection Market Segmented?

The ai for debt collection industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Software

- Service

- Deployment

- Cloud-based

- On-premises

- Sector

- Large enterprises

- SME

- Application

- BFSI

- Telecom

- Healthcare

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Japan

- Europe

- UK

- Germany

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- South Africa

- UAE

- Saudi Arabia

- Rest of World (ROW)

- North America

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

The software segment is defined by significant innovation in machine learning models and data processing capabilities. Advanced AI for debt collection platforms leverage predictive analytics and natural language processing to enable personalized debt collection communication and optimize recovery.

The use of intelligent process automation and AI-driven automation in AI for accounts receivable is critical for managing non-performing loans (NPLs). For instance, AI models for loan default prediction have improved accuracy by over 15% compared to traditional methods.

The application of intelligent document processing and AI-powered negotiation tools is also central to reducing operational costs, alongside the rise of generative AI in debt collection. This evolution underscores a strategic shift toward more efficient and data-centric collection methodologies.

The Software segment was valued at USD 1.76 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 31.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI For Debt Collection Market Demand is Rising in North America Get Free Sample

The geographic landscape is led by North America, which accounts for over 31% of the incremental growth, driven by advanced technological adoption and a focus on compliance automation.

The US, in particular, leverages AI-powered virtual assistants and behavioral analytics to manage high volumes of consumer debt.

APAC is the fastest-growing region, with a projected CAGR of 16.1%, fueled by digitalization in countries like China and India, where alternative data analysis is crucial for assessing creditworthiness.

Europe, contributing over 20% to market growth, navigates a complex regulatory environment by deploying explainable AI and ethical AI in collections to adhere to data privacy regulations.

The use of AI-based risk scoring and risk segmentation is becoming standard across these key regions to improve the efficiency of digital debt collection efforts.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic implementation of AI is revolutionizing debt recovery, with organizations increasingly focused on using AI to improve recovery rates. The core of this transformation lies in leveraging predictive analytics for debt collection to forecast default risks and optimize outreach.

- By automating debt collection with AI, financial institutions can significantly reduce manual effort and operational overhead, realizing one of the key benefits of AI in debt collection. This automation is coupled with AI-powered customer engagement for collections, which utilizes tools like chatbots and personalized messaging to create a more cooperative resolution process.

- A paramount concern is ensuring AI for debt collection compliance, as regulatory scrutiny intensifies globally. The principles of ethical AI deployment in debt collection are central to building trust and avoiding algorithmic bias. Decisions around cloud vs on-premises AI collection are often dictated by data security needs and scalability requirements.

- Sector-specific applications are also maturing, particularly AI for BFSI debt collection and AI for telecom debt collection. The AI for healthcare debt collection segment focuses on empathetic communication, while AI for SME debt collection requires scalable platforms.

- Advanced AI-driven debt negotiation strategies and real-time decisioning in debt recovery allow for dynamic adjustments, while AI-based risk segmentation for debtors enables tailored interventions. The rise of generative AI in debt collection is further enhancing personalized debt collection communication, with some firms reporting that AI-driven strategies are twice as effective in establishing payment plans compared to traditional methods.

- Finally, AI models for loan default prediction and a focus on AI compliance in financial services are proving critical for reducing operational costs and ensuring sustainable growth.

What are the key market drivers leading to the rise in the adoption of AI For Debt Collection Industry?

- The imperative to increase operational efficiency and reduce costs serves as a key driver for market growth.

- A primary driver is the need for enhanced operational efficiency, which AI debt recovery solutions directly address.

- By leveraging predictive analytics and advanced debtor behavior prediction, organizations are achieving significant gains; for example, proactive interventions have reduced accounts progressing to severe delinquency by 12%.

- The use of sentiment analysis within customer engagement platforms has improved customer satisfaction scores by 15%. Granular risk segmentation and AI-based risk segmentation for debtors allow for tailored predictive outreach strategies, leading to a 15% increase in overall recovery rates.

- This data-driven approach is particularly impactful in AI for BFSI debt collection and AI for B2B collections, where real-time decisioning in debt recovery is critical for managing complex portfolios and using AI to improve recovery rates.

What are the market trends shaping the AI For Debt Collection Industry?

- The escalating digital transformation across financial services is accelerating automation, a primary trend shaping the market's trajectory.

- The market is increasingly defined by a digital-first debt collection approach, where AI for debt collection platforms are central to strategy. A key trend is the rise of agentic AI and conversational AI, with some systems delivering 96% clinically accurate empathetic responses, making them nearly indistinguishable from human agents.

- The use of generative AI voicebots and other forms of generative AI in debt collection for automated payment reminders and initial outreach has resulted in recovery rate improvements of up to 30%. This focus on empathetic debt collection AI is not just enhancing customer experience but also proving effective, with AI-driven debt negotiation strategies leading to better outcomes.

- The integration of advanced AI-based risk scoring is enabling more personalized debt collection communication, which is crucial for effective AI-driven debt management and reducing operational costs.

What challenges does the AI For Debt Collection Industry face during its growth?

- Navigating complex regulatory compliance requirements and ensuring ethical AI deployment present a key challenge to industry growth.

- A significant challenge is navigating the complex regulatory landscape, demanding robust AI for debt collection compliance and ethical AI deployment in debt collection. The deployment of an AI-powered compliance platform and dedicated compliance monitoring systems is now essential.

- For instance, some firms have reduced reconciliation-related labor by 20% through robotic process automation, yet ensuring these systems are fair is a hurdle. The need for explainable AI is growing, especially in sensitive areas like AI for healthcare debt collection.

- High implementation costs and integration complexities, particularly with cloud vs on-premises AI collection decisions, act as barriers for AI for SME debt collection. Firms must invest heavily in AI-driven compliance tools and adaptive analytics to ensure their machine learning models remain compliant and unbiased.

Exclusive Technavio Analysis on Customer Landscape

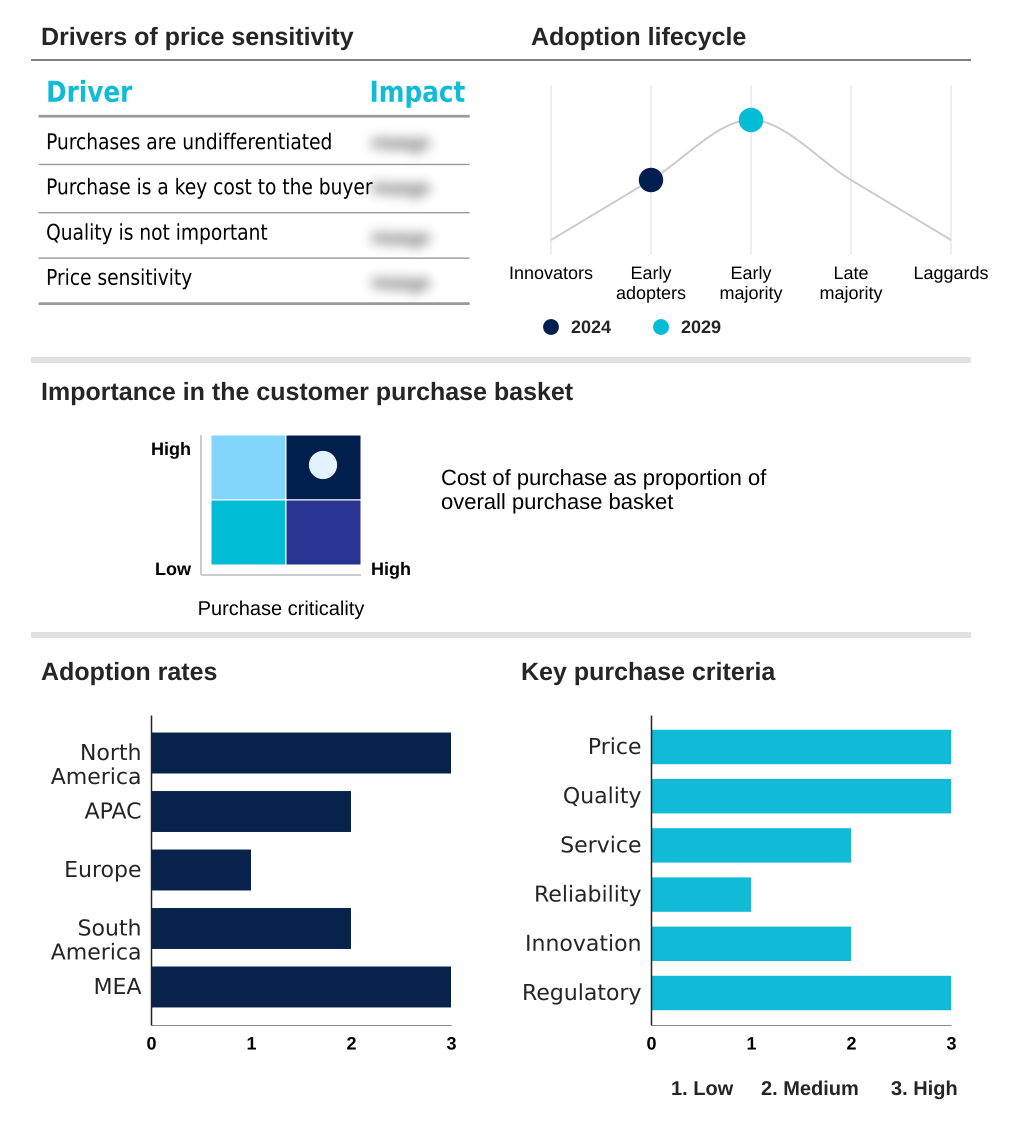

The ai for debt collection market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai for debt collection market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI For Debt Collection Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai for debt collection market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Analog Legalhub Technology Solutions Pvt. Ltd. - AI for Debt Collection solutions incorporate GenAI voicebots and predictive analytics to create personalized, automated borrower journeys, enhancing recovery strategies.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Analog Legalhub Technology Solutions Pvt. Ltd.

- Chetu Inc.

- collect Artificial Intelligence GmbH

- Debtist GmbH

- Experian Plc

- Fair Isaac Corp.

- Finvi

- IC System Inc

- InDebted Holdings Pty Ltd

- Intellect Design Arena Ltd.

- Intelligent Contacts Inc

- LexisNexis Risk Solutions.

- Loxon Solutions Zrt.

- PAIR Finance Group

- Pegasystems Inc.

- QUALCO

- Temenos AG

- Tesorio Inc

- TransUnion

- TrueAccord

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai for debt collection market

- In August, 2024, Ant Group announced the integration of generative AI into its debt recovery operations to craft nuanced, emotionally intelligent messages tailored to each borrower's financial situation.

- In October, 2024, Neowise, in collaboration with Sarvam AI, launched NeoBot and NeoSight, India's first generative AI-powered debt collection tools that automate voice-based outreach and call analytics.

- In March, 2025, Cedar partnered with Twilio to enhance its AI-driven billing communications, using a voice AI engine to automate inbound billing calls and offer tailored payment options.

- In May, 2025, Synchrony Financial entered a partnership with Credgenics to implement AI-powered predictive analytics across its consumer debt portfolios, using over 200 data points to optimize outreach.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI For Debt Collection Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 317 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 15% |

| Market growth 2025-2029 | USD 2771.5 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 12.7% |

| Key countries | US, Canada, Mexico, China, India, Japan, Australia, South Korea, Singapore, UK, Germany, France, Italy, The Netherlands, Spain, Brazil, Argentina, Colombia, South Africa, UAE, Saudi Arabia, Egypt and Kenya |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI for debt collection market is undergoing a significant transformation, driven by the integration of advanced technologies designed to optimize recovery processes. At the core of this shift are machine learning models and predictive analytics, which enable sophisticated debtor behavior prediction and risk segmentation.

- The adoption of AI-driven automation and robotic process automation for routine tasks allows collection agents to focus on more complex negotiations, supported by insights from sentiment analysis and behavioral analytics. We are seeing a move towards more interactive and personalized engagement through conversational AI, AI-powered virtual assistants, and generative AI voicebots.

- These tools facilitate automated communication that is both efficient and empathetic. For boardroom decisions, the focus on compliance automation and explainable AI is critical for navigating complex regulatory landscapes and mitigating risks. Platforms are increasingly using adaptive analytics and reinforcement learning for real-time decisioning, with some achieving a 15% improvement in promise-to-pay rates.

- The use of alternative data analysis and automated skip tracing enhances the effectiveness of digital debt collection, while AI-led credit scoring and intelligent process automation are becoming standard. Ultimately, solutions featuring virtual negotiators and sophisticated AI-based risk scoring are defining the next generation of debt management.

What are the Key Data Covered in this AI For Debt Collection Market Research and Growth Report?

-

What is the expected growth of the AI For Debt Collection Market between 2025 and 2029?

-

USD 2.77 billion, at a CAGR of 15%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, Service), Deployment (Cloud-based, On-premises), Sector (Large enterprises, SME), Application (BFSI, Telecom, Healthcare, Others) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing operational efficiency and cost reduction, Regulatory compliance and ethical AI deployment

-

-

Who are the major players in the AI For Debt Collection Market?

-

Analog Legalhub Technology Solutions Pvt. Ltd., Chetu Inc., collect Artificial Intelligence GmbH, Debtist GmbH, Experian Plc, Fair Isaac Corp., Finvi, IC System Inc, InDebted Holdings Pty Ltd, Intellect Design Arena Ltd., Intelligent Contacts Inc, LexisNexis Risk Solutions., Loxon Solutions Zrt., PAIR Finance Group, Pegasystems Inc., QUALCO, Temenos AG, Tesorio Inc, TransUnion and TrueAccord

-

Market Research Insights

- Market dynamics are increasingly shaped by the adoption of sophisticated AI for debt collection platforms that deliver significant operational advantages. These AI debt recovery solutions are proving essential for managing non-performing loans, with some institutions reporting a 15% increase in recovery rates.

- The deployment of a dedicated debt collection chatbot and automated payment reminders has led to a 30% reduction in inbound calls for routine inquiries. As the focus shifts toward ethical AI in collections, customer engagement platforms are being enhanced with features for behavior-based personalization.

- This push for digital-first debt collection is evident in the performance of compliance monitoring systems, which have reduced compliance breaches significantly. The move towards omnichannel communication automation and AI for accounts receivable is reshaping strategies, making processes more efficient and consumer-friendly.

We can help! Our analysts can customize this ai for debt collection market research report to meet your requirements.

RIA -

RIA -