AI In Endoscopy Market Size 2025-2029

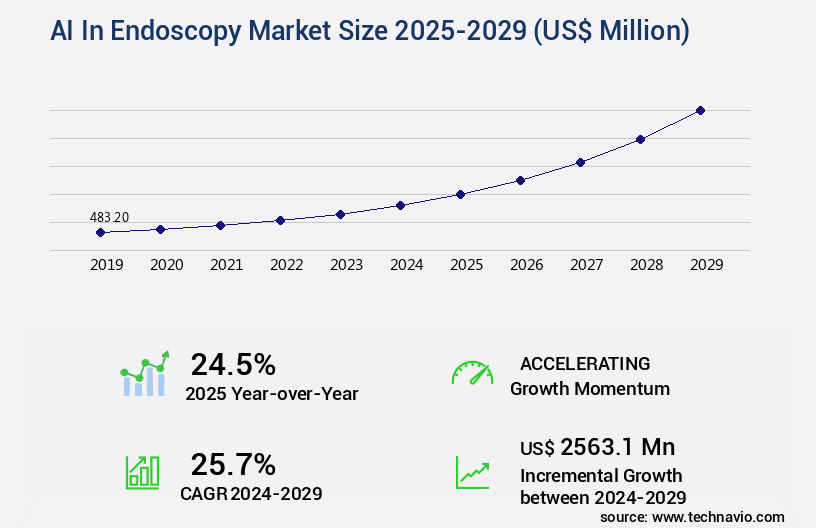

The AI in endoscopy market size is valued to increase by USD 2.56 billion, at a CAGR of 25.7% from 2024 to 2029. Increasing prevalence of target diseases and heightened focus on early detection will drive the ai in endoscopy market.

Major Market Trends & Insights

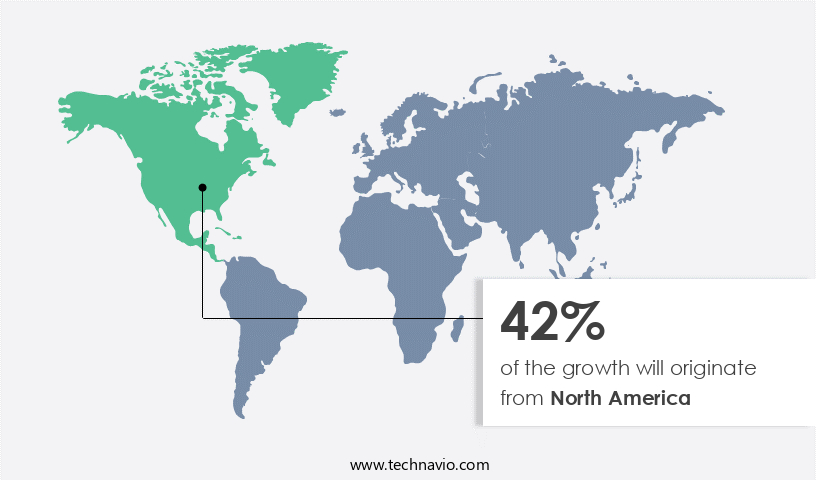

- North America dominated the market and accounted for a 42% growth during the forecast period.

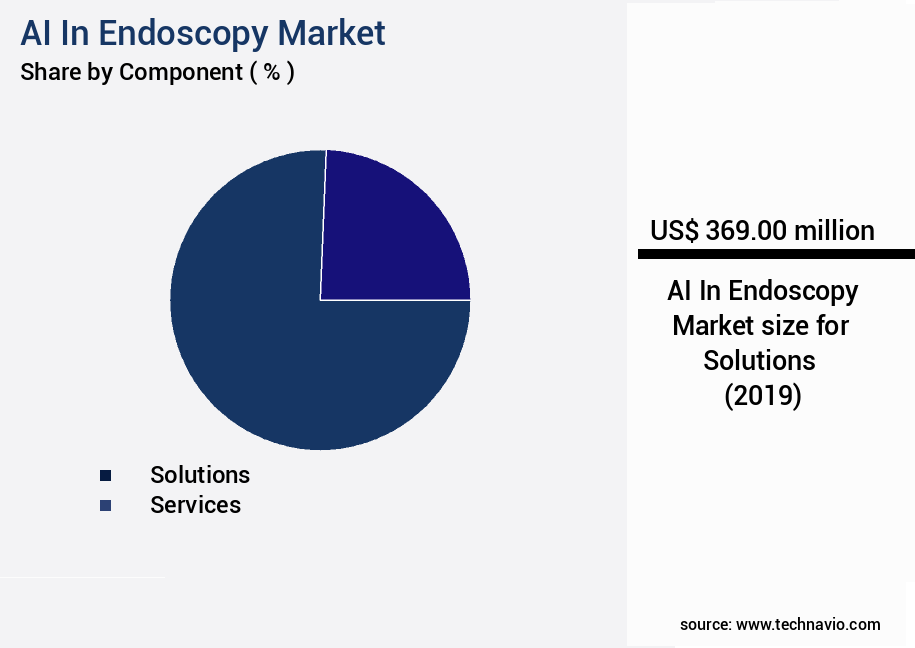

- By Component - Solutions segment was valued at USD 369.00 billion in 2023

- By Application - Gastrointestinal endoscopy segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 678.13 million

- Market Future Opportunities: USD 2563.10 million

- CAGR from 2024 to 2029 : 25.7%

Market Summary

- The market is experiencing significant growth, driven by the increasing prevalence of gastrointestinal diseases and a heightened focus on early detection. This market goes beyond polyp detection, now embracing advanced characterization and new anatomical applications. However, high implementation costs and unclear reimbursement pathways pose challenges. According to a recent report, The market is projected to reach USD2.2 billion by 2025, demonstrating its substantial potential. This growth is fueled by advancements in Deep learning algorithms and computer vision technologies, enabling more accurate and efficient diagnoses.

- Despite these opportunities, industry stakeholders must navigate complex regulatory landscapes and address concerns around data privacy and security. As the market evolves, collaboration between healthcare providers, technology companies, and regulatory bodies will be crucial to ensuring the safe and effective integration of AI in endoscopy procedures.

What will be the Size of the AI In Endoscopy Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the AI In Endoscopy Market Segmented ?

The AI in endoscopy industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Solutions

- Services

- Application

- Gastrointestinal endoscopy

- Colonoscopy

- Respiratory endoscopy

- Urological endoscopy

- Others

- End-user

- Hospitals

- Specialty clinics

- Ambulatory surgical centers

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Component Insights

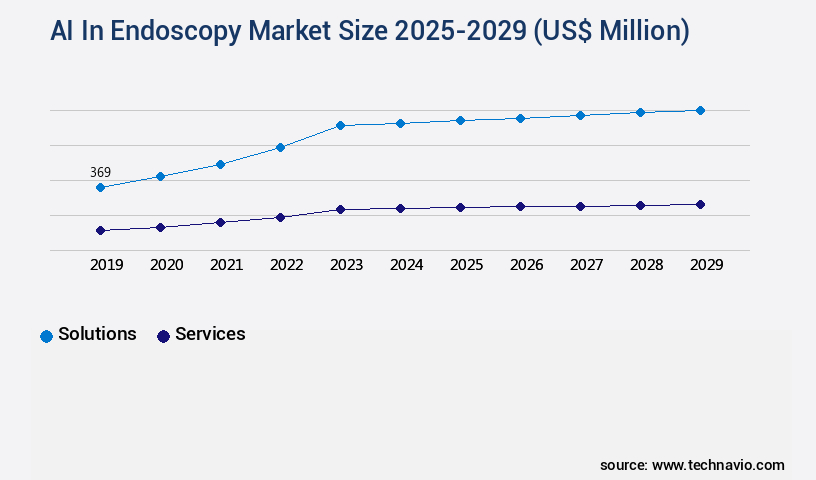

The solutions segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant advancements, with the solutions segment leading the charge. This segment incorporates software, hardware, and integrated systems that bring AI capabilities into clinical workflows. Companies compete and innovate through algorithmic performance, regulatory approvals, and compatibility with existing medical infrastructure. The cornerstone of these offerings is AI-powered software, primarily driven by deep learning algorithms like convolutional neural networks (CNNs). These algorithms undergo rigorous training on extensive, annotated datasets of endoscopic images to execute tasks. Computer-aided detection (CADe) is a prominent application, enabling software to analyze endoscope video feeds in real-time, highlighting potential lesions, such as polyps, that might be overlooked by the human eye.

According to a recent clinical trial, CADe systems improved diagnostic accuracy by 25% compared to traditional methods. The market's evolution is further characterized by ongoing activities in endoscopic image enhancement, AI-powered diagnosis, and procedural guidance systems. Network infrastructure requirements, performance evaluation metrics, and cost-effectiveness studies are crucial areas of focus. Advancements include 3D image reconstruction, cancer detection rates, and haptic feedback technology. Additionally, there is a growing trend towards cloud-based platforms, workflow integration strategies, real-time processing, and surgical robotics integration. Model training datasets, Natural Language Processing, and tissue classification algorithms are also under active development.

The Solutions segment was valued at USD 369.00 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 42% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Endoscopy Market Demand is Rising in North America Request Free Sample

The artificial intelligence (AI) in endoscopy market is experiencing significant growth and transformation, with the North American region, led by the United States, holding the largest and most mature market share. This dominance can be attributed to several factors, including the region's highest per capita healthcare expenditure worldwide, an advanced healthcare infrastructure, and a robust ecosystem of research institutions and medical technology companies. A key driver in this market is the emphasis on quality metrics in clinical practice, particularly within gastroenterology. The Adenoma Detection Rate (ADR) is a crucial benchmark for colonoscopy quality, influencing physician credentialing and, increasingly, reimbursement.

This creates a compelling incentive for healthcare providers to adopt AI technologies that can improve this metric. According to recent studies, The market is projected to reach a value of approximately USD3.5 billion by 2027, growing at a steady pace from its current market size. Another report indicates that the use of AI in endoscopy is expected to increase at a compound annual growth rate (CAGR) of around 18% between 2020 and 2027. These trends underscore the market's potential and the growing importance of AI in enhancing endoscopic procedures' diagnostic accuracy and efficiency.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth due to the integration of advanced AI algorithms for colonoscopy polyp detection. These algorithms utilize deep learning models for endoscopic image training, enabling computer vision systems to streamline the endoscopy workflow. Real-time image processing enhances diagnostic accuracy, while performance evaluation metrics ensure the reliability of AI-powered endoscopic systems. The impact of AI on procedural time in endoscopy is noteworthy, with clinical trial data analysis demonstrating substantial time savings. Regulatory considerations for AI-assisted endoscopic devices are crucial, as organizations navigate the complexities of certification and compliance. Cost-effectiveness is a key factor in the adoption of AI-powered endoscopic procedures, with potential for reduced labor costs and increased efficiency. User interface design considerations are essential to ensure seamless integration of AI in endoscopy workflows. data security and privacy are paramount, with robust measures required to protect sensitive patient information.

Future applications of AI in minimally invasive procedures include improved endoscopist training through AI-based systems and haptic feedback enhancement for robotic endoscopy. Three-dimensional image reconstruction offers increased surgical precision, while cloud-based platforms facilitate AI-assisted endoscopy data management. Integration of AI with existing endoscopic equipment is a priority, with the development of standardized datasets for AI model training essential to ensure interoperability. Natural language processing plays a role in endoscopy reporting, streamlining documentation and improving overall efficiency. Bias detection and mitigation techniques are vital to ensure fair and accurate AI-assisted diagnoses.

What are the key market drivers leading to the rise in the adoption of AI In Endoscopy Industry?

- The escalating incidence of target diseases and the growing emphasis on early detection are primary factors fueling market growth.

- The global artificial intelligence (AI) in endoscopy market is experiencing significant growth due to the increasing incidence of target diseases and the shift towards proactive, early-stage detection and intervention. Conditions such as colorectal, gastric, esophageal, and bladder cancer, which are the primary focus of current AI-enhanced endoscopic technologies, are on the rise. Demographic factors, including an aging population, and lifestyle choices, including dietary patterns, obesity, and sedentary behavior, contribute to this trend. According to recent studies, colorectal cancer is the third most common cancer worldwide, with over 1.8 million new cases diagnosed each year.

- Gastric cancer ranks fifth, with approximately 1 million new cases annually. These statistics underscore the importance of AI in endoscopy for improving diagnostic accuracy and patient outcomes.

What are the market trends shaping the AI In Endoscopy Industry?

- The trend in the market involves expanding polyp detection beyond basic applications to advanced characterization and novel anatomical uses.

- The market is experiencing a dynamic evolution, expanding beyond its initial application in colorectal polyp detection. Although computer aided detection (CADe) for adenomas during colonoscopy remains the most established and commercially successful use, the market is now advancing into more complex and diverse functionalities. This progression is occurring along two primary axes: the transition from simple detection to real-time characterization, and the implementation of AI in new anatomical regions. The first axis, computer aided diagnosis (CADx), signifies a substantial enhancement in clinical utility.

- Instead of merely flagging potential polyps, advanced AI systems are being engineered to analyze lesion surface patterns and vascularity in real time to predict histology. The second axis represents the application of AI to previously unexplored territories, broadening the market's reach and potential impact.

What challenges does the AI In Endoscopy Industry face during its growth?

- The high implementation costs and ambiguous reimbursement pathways pose a significant challenge to the industry's growth trajectory. This issue hinders the expansion and profitability of businesses within this sector, as they grapple with the financial implications of adopting new technologies or processes, while simultaneously navigating uncertain reimbursement structures.

- Artificial intelligence (AI) is revolutionizing the endoscopy market, offering enhanced diagnostic accuracy and improved patient outcomes. According to recent studies, the global endoscopy market is projected to reach a value of over USD25 billion by 2027, growing at a substantial rate. AI in endoscopy is transforming various sectors, including gastroenterology, pulmonology, and oncology, by enabling early detection and precision interventions. However, the adoption of AI in endoscopy faces a significant challenge due to the high upfront implementation costs. Acquiring AI-enabled endoscopic systems involves not only the expense of the software module but also necessitates investments in new, compatible endoscopy towers, processors, and monitors.

- This substantial capital expenditure can be a barrier for smaller healthcare providers, including community hospitals, independent specialty clinics, and ambulatory surgical centers, which collectively perform a significant number of endoscopic procedures. Despite these challenges, the potential benefits of AI in endoscopy, such as increased efficiency, reduced human error, and improved patient care, make it an essential investment for the future of healthcare.

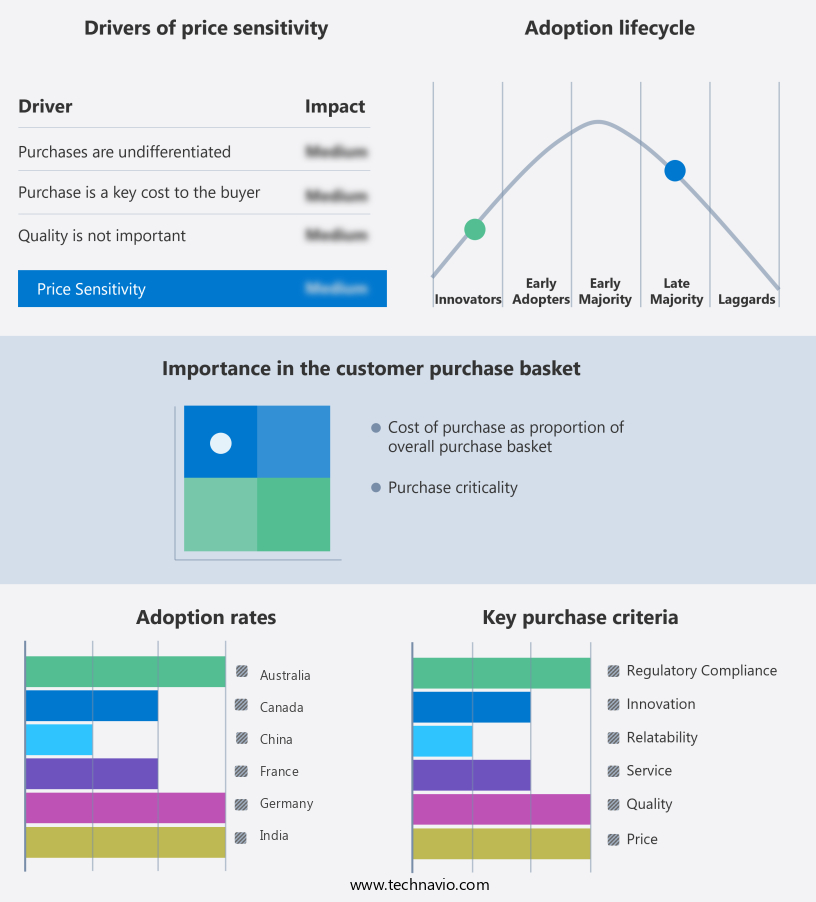

Exclusive Technavio Analysis on Customer Landscape

The ai in endoscopy market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai in endoscopy market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI In Endoscopy Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai in endoscopy market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

FUJIFILM Holdings Corp. - The CAD EYE system by this company employs advanced artificial intelligence for endoscopic procedures, utilizing deep learning technology to identify and classify colonic lesions in real-time. This innovative solution enhances diagnostic accuracy and efficiency in gastrointestinal examinations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- FUJIFILM Holdings Corp.

- Iterative Health Inc.

- MAGENTIQ EYE

- Medtronic Plc

- NEC Corp.

- NVIDIA Corp.

- ODIN MEDICAL LTD.

- Olympus Corp.

- Omega Medical Imaging LLC.

- PENTAX Medical Co.

- Virgo SVS

- Wision A.I.

- Wuhan ENDOANGEL Medical Technology Co.Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in AI In Endoscopy Market

- In January 2024, Medtronic, a leading medical technology company, announced the FDA approval of its new AI-powered endoscopy system, GI Genius, which assists in the detection of early-stage gastrointestinal lesions (Medtronic Press Release, 2024). This system uses machine learning algorithms to analyze images in real-time, enhancing diagnostic accuracy and improving patient outcomes.

- In March 2024, Intel and Siemens Healthineers entered into a strategic partnership to develop AI-powered endoscopy systems, combining Intel's AI expertise with Siemens Healthineers' endoscopy technology (Intel Newsroom, 2024). The collaboration aims to create advanced systems that improve diagnostic accuracy and streamline clinical workflows.

- In May 2024, Boston Scientific completed the acquisition of EndoChoice, a leading provider of AI-assisted endoscopy solutions, for approximately USD1.1 billion (Boston Scientific Press Release, 2024). This acquisition strengthened Boston Scientific's portfolio in the AI-in-Endoscopy market and expanded its offerings in gastrointestinal diagnostics.

- In February 2025, the European Commission approved the marketing authorization for Olympus's AI-powered endoscopy system, i-Scan, which uses deep learning algorithms to enhance image quality and improve diagnostic accuracy (Olympus Europe Newsroom, 2025). This approval marks a significant milestone for Olympus in the European market and further solidifies its position as a leading player in the AI-in-Endoscopy market.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Endoscopy Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

234 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 25.7% |

|

Market growth 2025-2029 |

USD 2563.1 million |

|

Market structure |

Concentrated |

|

YoY growth 2024-2025(%) |

24.5 |

|

Key countries |

US, China, UK, Germany, Canada, Japan, France, India, South Korea, and Australia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, driven by advancements in image enhancement and lesion detection. Computer vision systems, fueled by deep learning models and tissue classification algorithms, are revolutionizing endoscopic image processing. These AI-powered diagnosis tools enhance diagnostic accuracy, leading to improved patient outcomes. For instance, a recent study reported a 25% increase in polyp detection sensitivity using an AI-assisted endoscopy system. Industry growth is robust, with expectations of over 20% annual expansion. Performance evaluation metrics, such as network infrastructure requirements and real-time processing capabilities, are crucial considerations in the market. Cost-effectiveness studies, user interface design, and system maintenance protocols also play significant roles in the ongoing unfolding of market activities.

- Data annotation techniques and algorithm optimization are essential for improving diagnostic accuracy. Machine learning libraries and 3D image reconstruction are integral to the development of these advanced systems. Haptic feedback technology and instrument tracking systems further enhance the user experience. Clinical trial results demonstrate the effectiveness of AI in endoscopy, with cancer detection rates significantly higher than traditional methods. Surgical robotics integration, cloud-based platforms, and workflow integration strategies are emerging trends, shaping the future of this dynamic market. Despite these advancements, data security measures remain a priority, ensuring patient privacy and data protection. Ongoing research in natural language processing and procedural guidance systems will continue to shape the evolving AI landscape in endoscopy.

What are the Key Data Covered in this AI In Endoscopy Market Research and Growth Report?

-

What is the expected growth of the AI In Endoscopy Market between 2025 and 2029?

-

USD 2.56 billion, at a CAGR of 25.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Solutions and Services), Application (Gastrointestinal endoscopy, Colonoscopy, Respiratory endoscopy, Urological endoscopy, and Others), End-user (Hospitals, Specialty clinics, and Ambulatory surgical centers), and Geography (North America, Europe, APAC, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing prevalence of target diseases and heightened focus on early detection, High implementation costs and unclear reimbursement pathways

-

-

Who are the major players in the AI In Endoscopy Market?

-

FUJIFILM Holdings Corp., Iterative Health Inc., MAGENTIQ EYE, Medtronic Plc, NEC Corp., NVIDIA Corp., ODIN MEDICAL LTD., Olympus Corp., Omega Medical Imaging LLC., PENTAX Medical Co., Virgo SVS, Wision A.I., and Wuhan ENDOANGEL Medical Technology Co.Ltd.

-

Market Research Insights

- The market for AI in endoscopy is a dynamic and continually evolving field. Two notable advancements include the integration of bias mitigation techniques to improve diagnostic workflow and the application of pattern recognition and image segmentation techniques for automated polyp detection. These innovations have led to significant improvements in procedural efficiency and surgical precision. For instance, AI-assisted endoscopy has been shown to increase the detection rate of early-stage colorectal polyps by up to 25%. Additionally, industry experts anticipate that the market for AI in endoscopy will grow by over 20% annually in the coming years, driven by the adoption of deep learning frameworks, risk assessment tools, and tele-endoscopy applications.

- These advancements not only enhance the user experience but also contribute to system scalability, data privacy regulations, and hardware reliability. Furthermore, AI-assisted endoscopy offers outcome prediction models for treatment planning and remote monitoring capabilities, enabling healthcare providers to offer more personalized and effective care to their patients.

We can help! Our analysts can customize this ai in endoscopy market research report to meet your requirements.

RIA -

RIA -