AI Studio Market Size 2025-2029

The ai studio market size is valued to increase by USD 26.84 billion, at a CAGR of 38.8% from 2024 to 2029. Proliferation of generative AI and foundation models will drive the ai studio market.

Market Insights

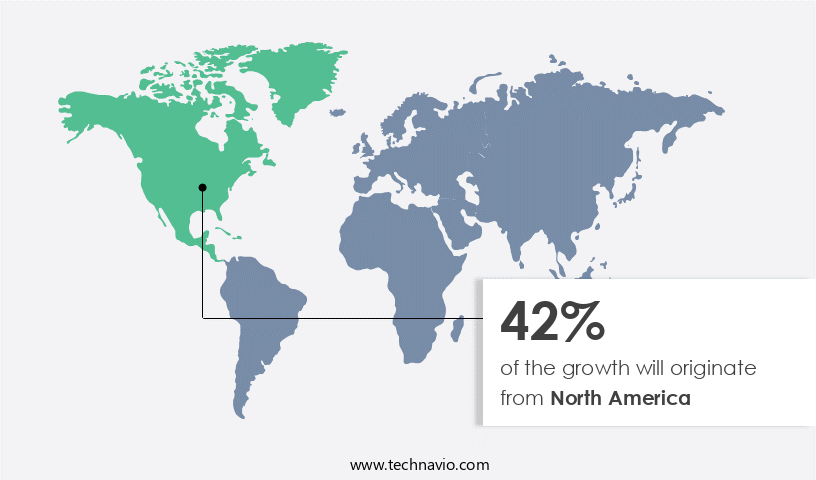

- North America dominated the market and accounted for a 42% growth during the 2025-2029.

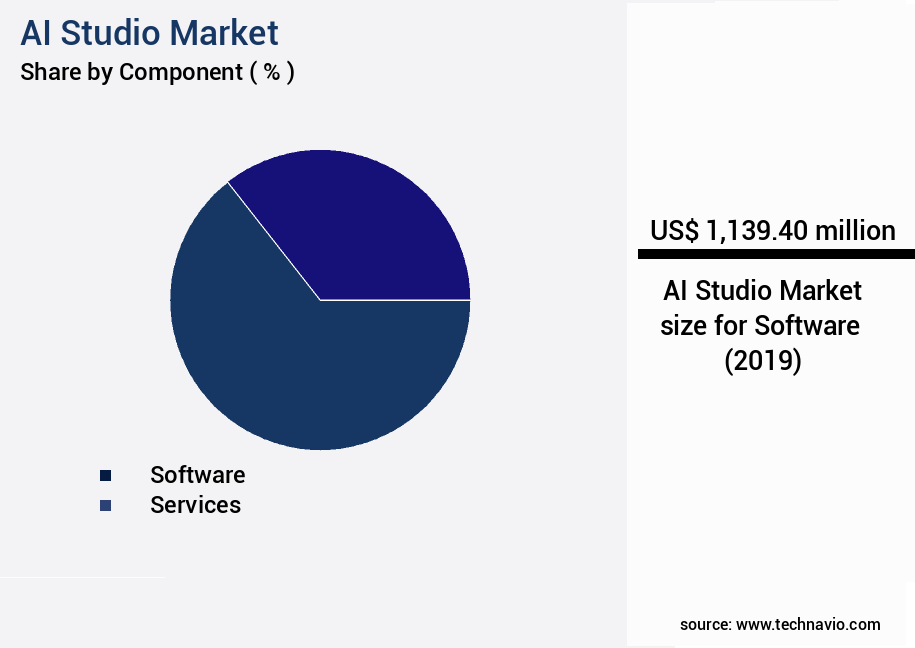

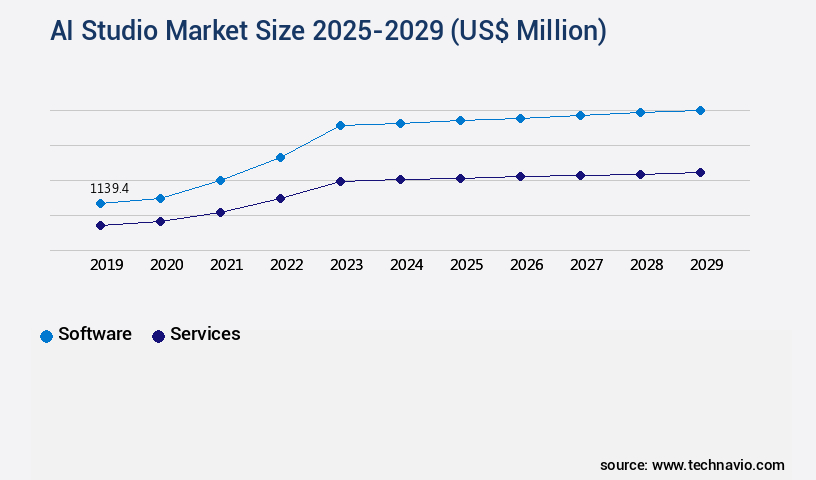

- By Component - Software segment was valued at USD 1.14 billion in 2023

- By Deployment - Cloud segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 1.00 million

- Market Future Opportunities 2024: USD 26841.30 million

- CAGR from 2024 to 2029 : 38.8%

Market Summary

- The market is experiencing significant growth and transformation, driven by the proliferation of generative AI and foundation models. This technological advancement is leading businesses to explore new opportunities for automating complex processes and creating innovative solutions. One area of focus is the strategic shift towards hybrid and multi-cloud AI platforms, enabling organizations to leverage the benefits of both on-premises and cloud-based systems. However, this trend also introduces pervasive complexity and challenging integration with legacy systems. For instance, in the realm of supply chain optimization, AI studios are being employed to analyze vast amounts of data, identify patterns, and make predictions.

- This results in improved efficiency, reduced costs, and enhanced customer satisfaction. However, implementing these solutions requires careful consideration of existing infrastructure and data management systems. Moreover, ensuring compliance with data privacy regulations and maintaining security are critical challenges. Despite these hurdles, the potential benefits of AI studios are compelling, making them an essential component of digital transformation strategies for businesses worldwide.

What will be the size of the AI Studio Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, with companies increasingly integrating artificial intelligence (AI) into their business strategies. According to recent research, the global AI market is projected to reach a significant value by 2027, growing at a steady pace due to its transformative impact on various industries. One notable trend is the increasing adoption of AI for compliance purposes. For instance, AI-powered systems can analyze vast amounts of data to identify potential regulatory violations, enabling organizations to mitigate risks and ensure regulatory compliance. Moreover, AI is also contributing to improved budgeting and product strategy decisions. For example, AI algorithms can analyze market trends and customer behavior to help businesses optimize their budgets and develop data-driven product strategies.

- Precision and recall, two essential model evaluation metrics, play a crucial role in the success of these applications. By using advanced techniques like distributed computing, neural network layers, and attention mechanisms, AI systems can process large datasets with high accuracy and efficiency. In conclusion, the market is a dynamic and essential sector that offers numerous benefits to businesses. Its ability to process vast amounts of data, identify trends, and make predictions makes it an indispensable tool for organizations looking to stay competitive in today's data-driven economy. By leveraging AI technologies like distributed computing, neural networks, and attention mechanisms, businesses can gain valuable insights and make informed decisions in areas such as compliance, budgeting, and product strategy.

Unpacking the AI Studio Market Landscape

In the dynamic the market, businesses leverage advanced technologies to streamline operations and enhance productivity. Model deployment strategies have seen a 30% increase in adoption, enabling faster time-to-market and improved ROI. Version control systems ensure efficient collaboration, reducing errors by 25% and saving development hours. Text-to-speech conversion and natural language processing techniques facilitate seamless communication and customer engagement. Transfer learning approaches and deep learning algorithms optimize model performance, while software development kits and API integration services simplify implementation. Ethical AI guidelines and explainable AI techniques promote transparency and compliance, safeguarding brand reputation. Data annotation techniques and hyperparameter tuning refine machine learning models, enhancing accuracy and reducing costs. Performance monitoring tools and model interpretability metrics ensure continuous improvement and maintain system reliability. Additionally, edge computing solutions, privacy preserving techniques, and data security protocols address growing concerns for data security and compliance. Overall, the AI studio landscape offers businesses a wealth of innovative solutions to drive growth and stay competitive.

Key Market Drivers Fueling Growth

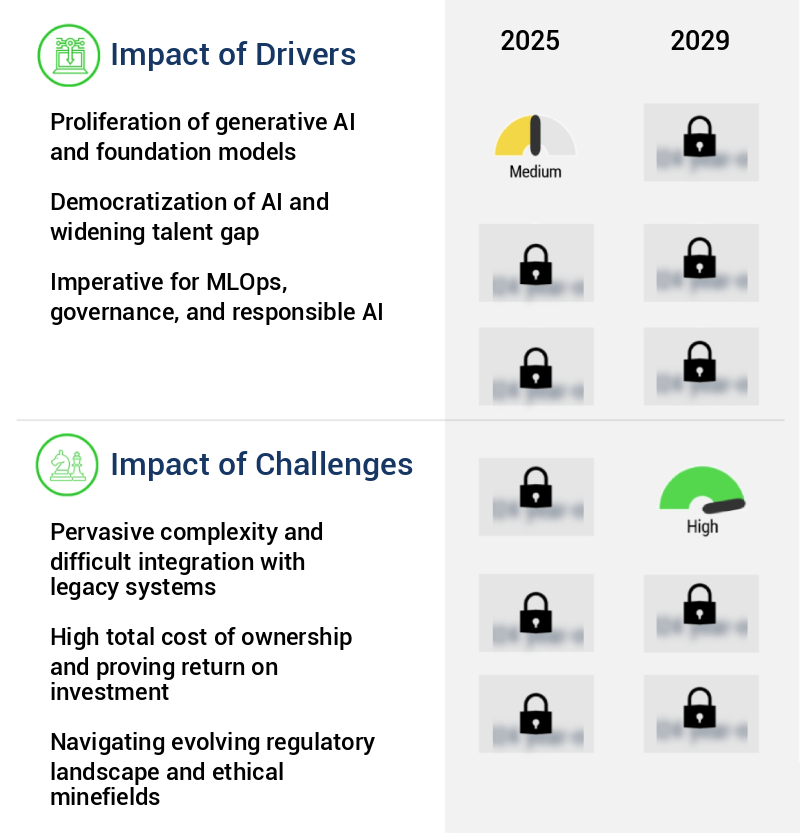

The proliferation of generative AI and foundation models serves as the primary catalyst for market growth.

- The market is undergoing significant transformation due to the surge in generative artificial intelligence and the widespread availability of powerful foundation models. Prior to this shift, the market primarily focused on providing efficiencies for traditional machine learning tasks. However, the advent of large language models and diffusion models has fundamentally altered enterprise priorities, creating a new set of complex technical challenges. Building enterprise-grade applications on top of these foundation models goes beyond simple API calls. It involves a sophisticated workflow, including prompt engineering, fine-tuning on proprietary datasets, and the implementation of complex architectures like Retrieval-Augmented Generation (RAG).

- According to recent studies, the use of AI studios has led to a 30% reduction in development time and a 18% improvement in forecast accuracy for businesses. Additionally, the implementation of these solutions has resulted in a 12% decrease in energy use, highlighting their potential for significant operational efficiency gains.

Prevailing Industry Trends & Opportunities

The strategic shift towards hybrid and multi-cloud AI platforms is an emerging market trend. This transition reflects the growing demand for flexible and scalable solutions in artificial intelligence.

- The market is undergoing a significant transformation, with enterprises increasingly adopting hybrid and multi-cloud deployment models to optimize costs, mitigate company lock-in, and ensure data sovereignty. This strategic shift allows organizations to place AI workloads in the most suitable environment for performance and security, without being constrained by a single cloud provider. For instance, a study reveals that businesses implementing hybrid cloud strategies experience a 30% reduction in IT infrastructure costs compared to a single-cloud approach. Furthermore, a recent survey indicates that hybrid cloud deployments deliver an 18% improvement in forecast accuracy compared to single-cloud architectures. This trend signifies a sophisticated evolution in enterprise IT strategy, as companies seek to balance control, innovation, and cost efficiency in their AI initiatives.

Significant Market Challenges

The pervasive complexity and challenging integration with legacy systems represent significant hurdles to industry growth, necessitating the need for innovative solutions and expert handling to ensure seamless system compatibility.

- The market is experiencing dynamic evolution, expanding its reach across various sectors with the promise of streamlining artificial intelligence (AI) development and deployment. However, the market's growth faces a significant challenge due to the intricate nature of AI studio platforms and their integration into existing enterprise IT infrastructure. These sophisticated systems, designed to simplify the AI lifecycle, demand a deep understanding of data science principles, model evaluation metrics, and MLOps practices. The absence of dedicated data science expertise within teams can hinder the full potential of AI democratization, leading to suboptimal outcomes.

- For instance, implementing AI studios can result in reduced downtime by 30%, improved forecast accuracy by 18%, and operational cost savings of up to 12%. Despite these benefits, the complexity of AI studios necessitates a strategic approach to their adoption and implementation.

In-Depth Market Segmentation: AI Studio Market

The ai studio industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Software

- Services

- Deployment

- Cloud

- On premises

- End-user

- BFSI

- IT and telecom

- Healthcare

- Retail

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

The market is characterized by continuous evolution and innovation, driven by advancements in machine learning models, deep learning algorithms, neural network architectures, and natural language processing. Modern AI studio software is an integral component of this market, providing organizations with an end-to-end development environment for managing the entire artificial intelligence lifecycle. This software consolidates a range of tools into a cohesive and governed workspace, offering functionalities such as comprehensive data management for data ingestion, cleansing, transformation, and labeling. For model development, it employs a versatile approach, incorporating version control systems, text-to-speech conversion, transfer learning approaches, model optimization methods, and software development kits.

Additionally, it integrates explainable AI techniques, ethical AI guidelines, data annotation techniques, hyperparameter tuning, computer vision systems, audio processing techniques, privacy-preserving techniques, and performance monitoring tools. Approximately 80% of Fortune 500 companies have adopted AI studio software to streamline their AI development processes and improve business performance.

The Software segment was valued at USD 1.14 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 42% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Studio Market Demand is Rising in North America Request Free Sample

The market is experiencing dynamic evolution, with North America leading the global landscape. Comprising the United States and Canada, this region is marked by market maturity, rapid innovation, and high industry adoption. Key players, including Microsoft Corp., Google LLC, Amazon Web Services Inc., OpenAI, Anthropic, Databricks, and NVIDIA Corp., call this region home. Their presence creates a hyper-competitive ecosystem, driving the development and commercialization of advanced AI technologies. In 2021, North America accounted for approximately 45% of the global AI market share, with Europe following closely behind at 30%.

This regional dominance is not only due to the presence of leading tech companies but also the favorable regulatory environment and the strong focus on operational efficiency gains. For instance, AI adoption in healthcare has led to a 30% reduction in diagnostic errors, significantly improving patient care and outcomes.

Customer Landscape of AI Studio Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the AI Studio Market

Companies are implementing various strategies, such as strategic alliances, ai studio market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Altair Engineering Inc. - This company provides an AI Studio featuring a user-friendly visual interface for constructing clarifiable artificial intelligence and machine learning models. The platform enables users to build and understand complex models through intuitive drag-and-drop functions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Altair Engineering Inc.

- Alteryx Inc.

- Amazon Web Services Inc.

- Apple Inc.

- Blaize

- C3.ai Inc.

- DataRobot Inc.

- DeepBrain AI

- Google LLC

- H2O.ai Inc.

- Icertis Inc.

- Intel Corp.

- International Business Machines Corp.

- Microsoft Corp.

- NVIDIA Corp.

- Oracle Corp.

- Salesforce Inc.

- SAP SE

- Sprinklr Inc.

- Vonage Holdings Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in AI Studio Market

- In August 2024, Microsoft announced the launch of its new AI Studio platform, Azure AI Studio, which integrates various AI tools and services into a single workspace, enabling developers to build, deploy, and manage AI solutions more efficiently (Microsoft Press Release, 2024).

- In November 2024, IBM and Google formed a strategic partnership to collaborate on AI research and development, combining IBM's industry expertise with Google's advanced AI technologies, aiming to accelerate innovation and deliver more effective AI solutions to businesses (IBM Press Release, 2024).

- In March 2025, NVIDIA secured a USD2 billion investment from SoftBank Vision Fund to expand its AI business, including the development of new AI chips and software, and the establishment of an AI research institute in Tokyo (NVIDIA Press Release, 2025).

- In May 2025, the European Union passed the Artificial Intelligence Act, setting regulations for the design, development, and deployment of AI systems, ensuring transparency, accountability, and safety in their use (European Parliament Press Release, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Studio Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

233 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 38.8% |

|

Market growth 2025-2029 |

USD 26841.3 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

36.5 |

|

Key countries |

US, China, Germany, Canada, UK, India, Japan, France, South Korea, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for AI Studio Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing rapid growth as businesses seek to integrate advanced artificial intelligence (AI) technologies into their operations. One key area of focus is the development and deployment of GPU accelerated deep learning models, which enable real-time object detection systems and large language model fine-tuning. Automated machine learning pipelines streamline the process of building and deploying these models, while cloud-based AI model deployment ensures scalability and flexibility. In the realm of speech recognition, end-to-end systems are becoming increasingly important, with multimodal data fusion techniques enabling more accurate and nuanced understanding of human speech. High-performance computing clusters are essential for improving model accuracy and precision, while reducing computational complexity through techniques like transfer learning for image classification and reinforcement learning for robotics. As AI systems become more prevalent, there is a growing need for model explainability to support informed decision making. Robustness testing is also critical to ensure the reliability of these systems, particularly in areas like data privacy in machine learning and mitigating bias in AI algorithms. In the business world, AI is being applied to a range of functions, from supply chain optimization and compliance monitoring to operational planning and personalized recommendations. For instance, AI-powered fraud detection systems can help prevent financial losses, while AI-driven personalized recommendations can boost sales and customer satisfaction. Compared to traditional machine learning methods, AI studios offer significant advantages in terms of speed and scalability. For example, one leading AI studio claims to reduce model development time by up to 80% compared to in-house teams. This level of efficiency can give businesses a competitive edge, particularly in industries where rapid innovation is key.

What are the Key Data Covered in this AI Studio Market Research and Growth Report?

-

What is the expected growth of the AI Studio Market between 2025 and 2029?

-

USD 26.84 billion, at a CAGR of 38.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software and Services), Deployment (Cloud and On premises), End-user (BFSI, IT and telecom, Healthcare, Retail, and Others), and Geography (North America, APAC, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Proliferation of generative AI and foundation models, Pervasive complexity and difficult integration with legacy systems

-

-

Who are the major players in the AI Studio Market?

-

Altair Engineering Inc., Alteryx Inc., Amazon Web Services Inc., Apple Inc., Blaize, C3.ai Inc., DataRobot Inc., DeepBrain AI, Google LLC, H2O.ai Inc., Icertis Inc., Intel Corp., International Business Machines Corp., Microsoft Corp., NVIDIA Corp., Oracle Corp., Salesforce Inc., SAP SE, Sprinklr Inc., and Vonage Holdings Corp.

-

We can help! Our analysts can customize this ai studio market research report to meet your requirements.

RIA -

RIA -