Hybrid Cloud Market Size 2024-2028

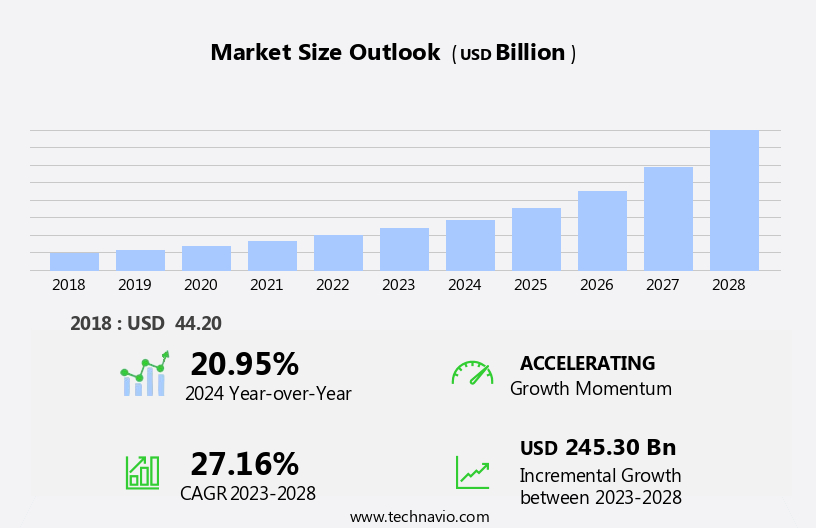

The hybrid cloud market size is forecast to increase by USD 245.30 billion at a CAGR of 27.16% between 2023 and 2028.

- Hybrid cloud computing, which combines the benefits of both private and public cloud services, is a significant area of investment for IT spending In the digital age. According to analytics, The market is expected to grow steadily, driven by trends such as simplified disaster recovery, enhanced containerization, and improved network connectivity. These trends are crucial for businesses undergoing digital transformation, particularly in sectors like IT services, industrial services, and content providers.

- Hypervisor technology plays a pivotal role in enabling seamless integration between public and private clouds. However, challenges persist, including data security concerns and latency issues. Addressing these challenges through automation and advanced analytics will be essential for businesses looking to optimize their IT infrastructure and stay competitive in the digital landscape.

What will be the Size of the Hybrid Cloud Market During the Forecast Period?

- The market continues to experience robust growth, driven by the increasing demand for cost efficiency, scalability, and agility in IT infrastructure. Businesses across various sectors, including telecommunications, healthcare services, and enterprises, are adopting hybrid cloud solutions to enhance their IT capabilities and improve data protection. The market is characterized by the integration of public and private cloud, enabling businesses to leverage the benefits of both environments.

- Hybrid cloud solutions offer enhanced security features, enabling businesses to manage critical banking processes and sensitive data with confidence. The collaboration between business and IT departments is a key driver of hybrid cloud adoption, with IT spending on cloud services projected to increase significantly in the coming years.

- Cyclical demand and emergency needs are also contributing to the market's growth, with virtual services becoming increasingly important for businesses in the banking sector and other industries. The dynamic regulatory landscape and the digitization of critical processes are further fueling the adoption of hybrid cloud solutions. Legacy technologies and transactions without cloud capabilities are being phased out, as more and more businesses recognize the benefits of hybrid cloud infrastructure. The market is composed of various components, including management services, service types, and telecommunications. Public bodies and non-critical IT infrastructure are also adopting hybrid cloud solutions to optimize their operations and enhance their digital capabilities.

How is this Hybrid Cloud Industry segmented and which is the largest segment?

The hybrid cloud industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Component

- Services

- Solution

- End-user

- BFSI

- Retail

- Healthcare

- Telecom

- Others

- Geography

- North America

- Canada

- US

- Europe

- Germany

- UK

- APAC

- China

- South America

- Middle East and Africa

- North America

By Component Insights

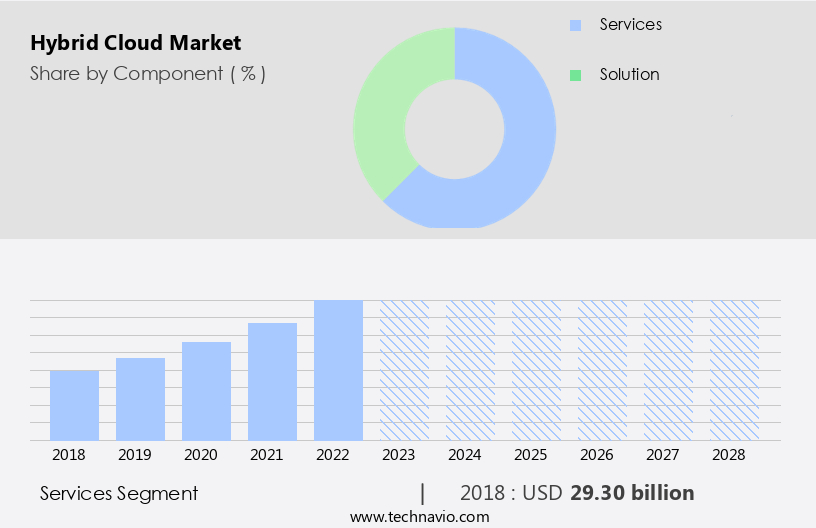

- The services segment is estimated to witness significant growth during the forecast period.

The market encompasses various professional services, including consulting, migration, training, and support. The services segment experiences significant growth due to the increasing demand for cloud storage solutions among organizations. Consulting services are increasingly popular as businesses seek expert advice on optimizing their storage infrastructure to align with industry trends. Migration services are in high demand as companies transition their data to hybrid cloud storage, requiring specialized technical expertise to ensure secure and accurate data transfer from traditional methods. These services contribute to cost efficiency, scalability, agility, security, and business-IT collaboration for enterprises across industries, including telecommunications, healthcare, and finance. Hybrid cloud deployment models offer organizations the flexibility to combine public and private clouds, enabling customized solutions for sensitive business processes and non-critical applications. Cloud infrastructure and service models cater to organizations of all sizes and verticals, enabling digital transformation, analytics, and innovation.

Get a glance at the Hybrid Cloud Industry report of share of various segments Request Free Sample

The Services segment was valued at USD 29.30 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

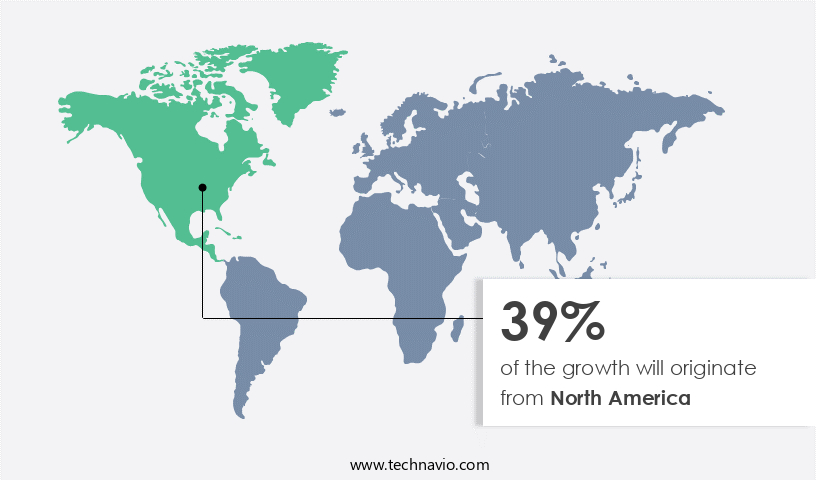

- North America is estimated to contribute 39% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The North American region is anticipated to lead the market in terms of revenue during the forecast period. With the introduction of public cloud services over a decade ago, North America was a frontrunner in adoption. The presence of numerous global public cloud service providers based In the US, with multiple data centers, further bolsters this region's dominance. However, some organizations have recently shifted workloads from public clouds to their on-premises infrastructure. This trend is driven by enhanced on-premises system performance and concerns regarding data sovereignty and security issues. Cost efficiency, scalability, agility, and security are primary drivers for the adoption of hybrid cloud solutions.

Hybrid cloud deployments enable businesses to leverage the benefits of both public and private clouds while mitigating potential risks. Telecommunications, healthcare, enterprises, and various industries are increasingly adopting hybrid cloud infrastructure for their IT infrastructure needs. Data protection and compliance are critical considerations for organizations, leading to the demand for advanced data security. The market comprises various components, including hardware, software, and services. Service types include IaaS, PaaS, and SaaS, while service models include managed and professional services. Organization size, verticals, and regions are significant factors influencing the market's growth. Hybrid cloud hosting, colocation, infrastructure utility, cloud infrastructure, and hybrid cloud deployment are essential elements of the hybrid cloud ecosystem.

Public bodies, organizations of all sizes, and various industries are adopting hybrid cloud solutions to address cyclical demand, emergency needs, and digitization requirements. Virtual services, automation, observability, flexibility, and digital transformation are essential aspects of hybrid cloud infrastructure. Enhanced analytics and innovation are natural outcomes of hybrid cloud deployments. The healthcare sector, banking sector, and critical banking processes are significant verticals In the market. IT spending on hybrid cloud solutions is expected to grow as organizations seek to modernize their IT infrastructure and consolidate operations for improved management. Legacy technologies and transactions without digitization are being replaced by hybrid cloud solutions. Remote working systems, online documentation, and cost reduction are essential benefits of hybrid cloud deployments for organizations and their customers.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Hybrid Cloud Industry?

Disaster recovery simplified by hybrid cloud is the key driver of the market.

- Hybrid cloud solutions offer organizations cost efficiency and scalability by combining the benefits of public and private clouds. The ability to collaborate between business and IT departments is enhanced through the use of cloud infrastructure, enabling agility and flexibility. Telecommunications, healthcare, and enterprises are among the verticals increasingly adopting hybrid cloud deployments for their IT infrastructure needs. Data protection is a significant concern for organizations, and hybrid cloud solutions provide an effective means of securing industrial services, critical business processes, and sensitive data. Cost reduction is a key driver for hybrid cloud adoption, particularly for organizations with cyclical demand or emergency needs.

- Hybrid cloud models enable the use of public cloud solutions for non-critical applications while maintaining control over critical, on-premises infrastructure. Service types and models cater to various organization sizes and industries, including public bodies and the banking sector. Hybrid cloud deployments offer automation, observability, and flexibility, essential components of digital transformation. Enhanced analytics and innovation are also crucial benefits, enabling organizations to make informed decisions and respond to dynamic regulatory requirements. The market continues to grow, driven by the need for consolidated operations, management, and data center modernization. Hybrid cloud solutions offer disaster recovery capabilities, allowing organizations to maintain business continuity without the need for a separate site.

- This not only reduces costs but also improves overall efficiency and productivity. Virtual services and remote working systems are increasingly common, making hybrid cloud solutions indispensable for organizations in today's digital landscape.

What are the market trends shaping the Hybrid Cloud Industry?

Containers enhancing hybrid cloud services is the upcoming market trend.

- Hybrid cloud deployments are gaining popularity among organizations due to their cost efficiency, scalability, and agility. Containers and microservices are becoming preferred choices over traditional virtual machines (VMs) for application development in this environment. Containers, like VMs, have dedicated CPU and memory, but they share the operating system kernel. This eliminates the need for a guest operating system and a hypervisor, making containers lighter than VMs. Organizations often encounter challenges when transferring applications between various environments. Containers address this issue by bundling applications and their operating system dependencies into a single package. This facilitates seamless movement between different cloud platforms, making container and microservices architecture a suitable option for hybrid cloud environments.

- Security is a significant concern for businesses adopting hybrid cloud solutions. Service types and models, such as public, private, and industrial services, offer varying levels of data protection. Business-IT collaboration is crucial for organizations to ensure data security and compliance with dynamic regulatory requirements. Telecommunications, healthcare, enterprises, and other verticals are embracing hybrid cloud deployments for digitization and innovation. Cloud infrastructure, including colocation, hosting, infrastructure utility, and cloud infrastructure, plays a vital role in hybrid cloud deployment. Hybrid hosting, a combination of public and private cloud services, offers the benefits of both worlds. Cost reduction and efficiency are essential factors driving IT spending on hybrid cloud solutions.

- Legacy technologies and transactions without digitization can be consolidated through hybrid cloud deployments. Remote working systems, online documentation, and other digital services can be implemented more effectively with hybrid cloud infrastructure. Flexibility, automation, observability, and enhanced analytics are key benefits of hybrid cloud environments. Digital transformation initiatives, such as Hyperscale cloud and data center modernization, are accelerating the adoption of hybrid cloud solutions. Public bodies, banking sector, and other organizations are adopting hybrid cloud deployments to meet cyclical demand, emergency needs, and virtual services.

What challenges does the Hybrid Cloud Industry face during its growth?

Network connectivity issues and latency is a key challenge affecting the industry growth.

- Hybrid cloud deployments combine the benefits of on-premises infrastructure and public cloud services. This setup involves connecting a private cloud or on-premises data center to a public cloud via a WAN connection. While this setup offers cost efficiency, scalability, and agility, it comes with challenges such as network connectivity and latency issues. To ensure seamless connectivity, organizations can opt for various options, including normal Internet connections, VPNs, or direct connections. Each option comes with its advantages and limitations. Data security is a significant concern when transferring data over the Internet. It can be vulnerable to interception, theft, or replacement with malicious data.

- Additionally, the Internet is a best-effort network, meaning connection speeds are not guaranteed. Businesses must prioritize data protection through encryption, access control, and other security measures. Hybrid cloud setups are popular among enterprises, telecommunications, healthcare, and other verticals due to their flexibility and cost savings. Service types and models vary, including infrastructure utility, cloud infrastructure, colocation, hosting, and hybrid hosting. The size of the organization and its specific needs determine the most suitable service model. Businesses in sensitive industries, such as banking, require stringent data security and regulatory compliance. Hybrid cloud solutions offer customizable security features and enable business-IT collaboration.

- Digital transformation initiatives, such as cloud computing, data center modernization, and consolidated operations, are driving the growth of the market. The market caters to various organization sizes and regions, offering cost reduction, efficiency, and enhanced analytics. Innovation and automation are essential components of hybrid cloud infrastructure, enabling productivity and digital transformation. The market also offers virtual services, dynamic regulatory compliance, and flexibility to meet the cyclical demand and emergency needs of businesses.

Exclusive Customer Landscape

The hybrid cloud market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the hybrid cloud market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, hybrid cloud market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

Accenture Plc - The market encompasses offerings that combine the benefits of on-premises and public cloud environments. One such solution is Accenture's Hybrid Cloud Platform, which enables organizations to manage and optimize workloads across multiple cloud environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture Plc

- Alibaba Group Holding Ltd.

- Alphabet Inc.

- Amazon.com Inc.

- Cisco Systems Inc.

- Dell Technologies Inc.

- DXC Technology Co.

- Equinix Inc.

- Furukawa Electric Co. Ltd.

- Hewlett Packard Enterprise Co.

- Intel Corp.

- International Business Machines Corp.

- Kyndryl Inc.

- Lumen Technologies Inc.

- Microsoft Corp.

- Nutanix Inc.

- Oracle Corp.

- Panzura LLC

- Rackspace Technology Inc.

- VMware Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Hybrid cloud solutions have gained significant traction In the global business landscape, offering organizations the ability to reap the benefits of both public and private cloud deployments. This approach allows businesses to maintain control over their sensitive data while leveraging the cost efficiency, scalability, and agility of public cloud services. One of the primary drivers of hybrid cloud adoption is the need for cost efficiency. With hybrid cloud, organizations can allocate computing capacity based on their current needs and scale up or down as required. This flexibility enables businesses to optimize their IT infrastructure and reduce capital expenditures on underutilized on-premises infrastructure.

Another key factor fueling the growth of the market is the demand for increased security. Hybrid cloud solutions offer enhanced data protection through the use of encryption, access controls, and other security measures. Additionally, businesses can maintain control over their most sensitive data while still leveraging the advanced security features of public cloud providers. Business-IT collaboration is another area where hybrid cloud solutions shine. By providing a seamless integration between on-premises and cloud-based IT infrastructure, hybrid cloud enables organizations to streamline their operations and improve productivity. Telecommunications companies, healthcare providers, and other enterprises can benefit from this increased collaboration, allowing them to provide better services to their customers.

The IT infrastructure landscape is undergoing a significant transformation, with many organizations modernizing their data centers and moving towards a more consolidated operation. Hybrid cloud solutions are an essential component of this transformation, providing organizations with the flexibility and agility they need to adapt to changing business requirements. Moreover, hybrid cloud solutions are not limited to large organizations. They are also gaining popularity among small and medium-sized businesses, as well as public bodies, due to their cost-effective and flexible nature. The ability to support a wide range of verticals, from banking and finance to healthcare and education, makes hybrid cloud a versatile solution for organizations of all sizes.

The market is characterized by the continuous evolution of service types and models. Service types include infrastructure utility, colocation, hosting, and industrial services, while service models include traditional cloud, public cloud, private cloud, and hybrid cloud. The choice of service type and model depends on the specific needs of the organization, including cost, security, and performance requirements. The market is also influenced by cyclical demand, with emergency needs and virtual services driving growth during times of crisis. Dynamic regulatory requirements and the digitization of industries, such as banking and finance, are also contributing factors. The banking sector is a prime example of an industry undergoing digital transformation.

Hybrid cloud solutions enable banks to support critical banking processes while also providing non-critical applications and remote working systems. This flexibility allows banks to reduce costs, improve productivity, and enhance customer service. Hybrid cloud solutions offer numerous benefits, including cost reduction, efficiency, and productivity gains. They also provide organizations with the flexibility to choose the right service type and model based on their specific needs. With the continued evolution of cloud computing and the increasing demand for hybrid cloud solutions, this market is poised for significant growth In the coming years. In conclusion, the market is driven by the need for cost efficiency, scalability, and security. It offers organizations the flexibility to choose the right service type and model based on their specific requirements, making it an essential component of IT infrastructure modernization. The ability to support a wide range of industries and verticals, from telecommunications and healthcare to banking and finance, makes hybrid cloud a versatile solution for businesses of all sizes.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

191 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 27.16% |

|

Market growth 2024-2028 |

USD 245.30 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

20.95 |

|

Key countries |

US, UK, Canada, Germany, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Hybrid Cloud Market Research and Growth Report?

- CAGR of the Hybrid Cloud industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the hybrid cloud market growth of industry companies

We can help! Our analysts can customize this hybrid cloud market research report to meet your requirements.

RIA -

RIA -