AI Voice Lab Market Size 2025-2029

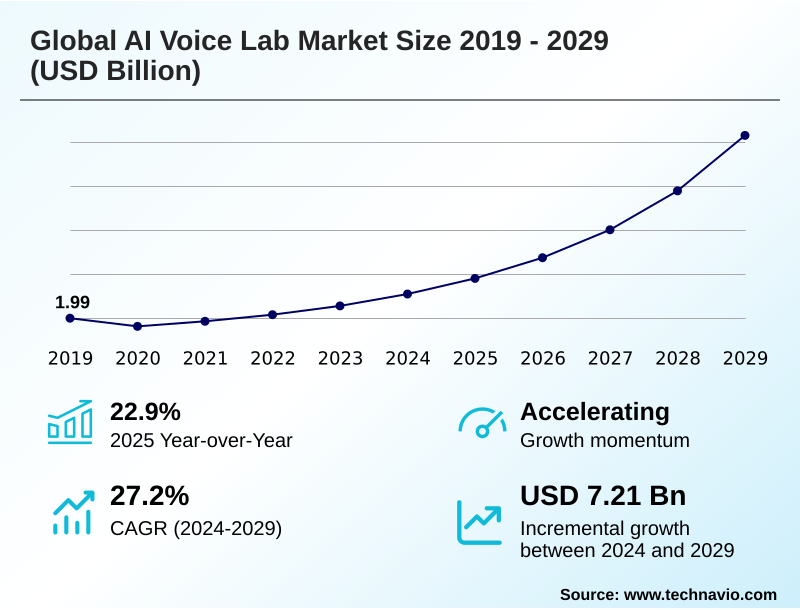

The ai voice lab market size is valued to increase by USD 7.21 billion, at a CAGR of 27.2% from 2024 to 2029. Proliferation of voice-enabled applications and conversational AI in consumer ecosystems will drive the ai voice lab market.

Major Market Trends & Insights

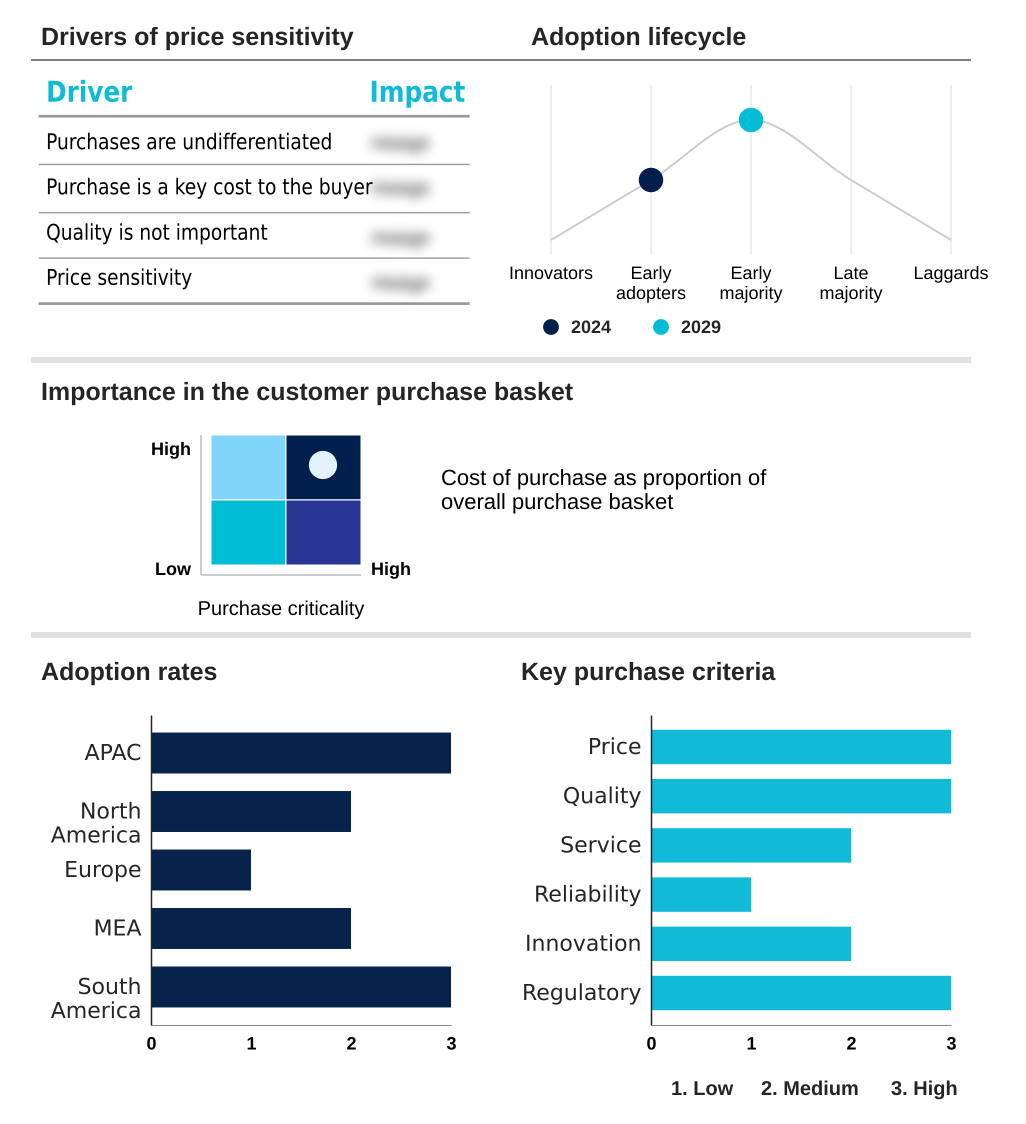

- APAC dominated the market and accounted for a 34.9% growth during the forecast period.

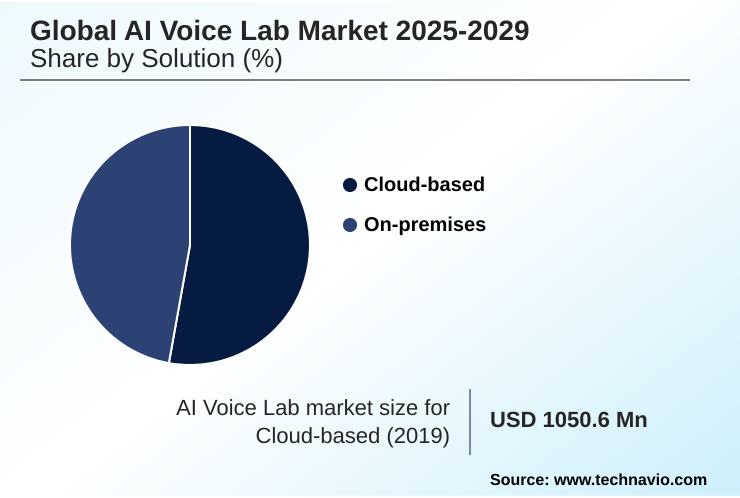

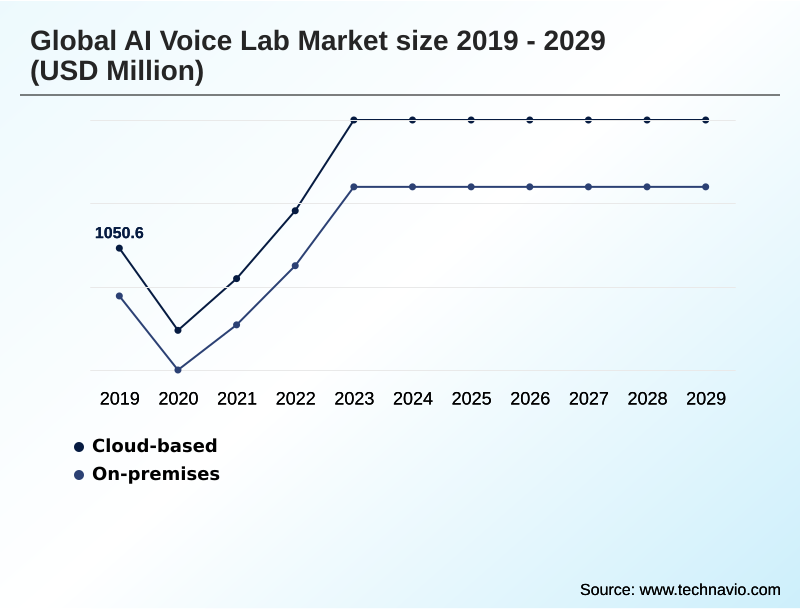

- By Solution - Cloud-based segment was valued at USD 1.35 billion in 2023

- By End-user - BFSI segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 8.31 billion

- Market Future Opportunities: USD 7.21 billion

- CAGR from 2024 to 2029 : 27.2%

Market Summary

- The AI voice lab market is rapidly evolving beyond basic text-to-speech (TTS) functionalities into a sophisticated ecosystem centered on hyper-realistic synthetic voice generation. This transformation is fueled by advancements in generative AI and large language models (LLMs), enabling the creation of custom branded voices with nuanced emotion detection and prosody modeling.

- Enterprises are increasingly leveraging these capabilities to differentiate their services and enhance user engagement. For instance, a global logistics firm can deploy a voice-directed warehousing system using automatic speech recognition (ASR) trained on domain-specific datasets.

- This application of voice-enabled workflows requires robust acoustic modeling to ensure functionality in noisy industrial environments and advanced natural language understanding (NLU) for interpreting commands from a diverse workforce. Such mission-critical deployments highlight the market's shift toward specialized solutions that demand high-quality, ethically sourced data and sophisticated technologies like voice cloning and deepfake detection to ensure both performance and security.

- This move from generic assistants to tailored conversational AI platforms underscores the strategic importance of unique vocal identities in modern digital interaction.

What will be the Size of the AI Voice Lab Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the AI Voice Lab Market Segmented?

The ai voice lab industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Solution

- Platform

- Services

- Managed services

- End-user

- BFSI

- Healthcare

- IT and Telecom

- Retail and e-commerce

- Others

- Deployment

- Cloud-based

- On-premises

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By Solution Insights

The platform segment is estimated to witness significant growth during the forecast period.

The platform segment is the foundational layer of the AI voice lab market, providing comprehensive software environments for creating bespoke conversational AI.

These integrated conversational AI platforms empower developers to manage the entire lifecycle, from audio dataset annotation and lexicon management to deployment.

A key focus is the development of domain-specific voice models for applications ranging from contact center automation to hands-free device control, necessitating robust acoustic modeling and precise wake word detection.

The advancement in voice user interface (VUI) design, supported by human-in-the-loop annotation, is critical for refining system accuracy.

For instance, integrated development toolkits have been shown to reduce voice application deployment times by up to 30% by streamlining workflows involving voice activity detection (VAD), conversational IVR scripting, and SSML.

The Platform segment was valued at USD 1.35 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 34.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Voice Lab Market Demand is Rising in APAC Request Free Sample

The global AI voice lab market exhibits a varied geographic landscape, with North America holding a significant share of approximately 31.57%, driven by advanced generative AI and large language models (LLMs) development.

This region’s maturity in enterprise applications like voice biometrics contrasts with the high-growth trajectory of APAC, which is expected to contribute nearly 35% of the market's incremental growth.

This expansion is fueled by the immense demand for multilingual speech synthesis to support diverse populations and the rise of voice-enabled workflows.

Innovations in text-to-speech (TTS) and edge AI speech processing are critical for delivering personalized audio content in mobile-first economies.

As the market expands, ethical data sourcing and speaker diarization for ambient computing interfaces have become key considerations for companies operating across these distinct regions.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The increasing sophistication of the AI voice lab market is evident in the push toward generative AI for realistic voice cloning, which is reshaping content creation and enabling the development of expressive voices for gaming characters. This progress, however, brings ethical considerations in synthetic voice generation to the forefront, demanding robust governance.

- In enterprise sectors, the technology is creating tangible value; voice biometrics for secure financial transactions are becoming an industry standard, while healthcare systems are adopting HIPAA-compliant ambient clinical documentation to begin reducing physician burnout with voice AI.

- The operational impact is equally significant, with businesses optimizing warehouse logistics with voice direction, a use case dependent on low-latency ASR for edge computing devices. Achieving global reach requires training voice models on diverse accents, a complex task critical to the future of voice as a user interface.

- To maintain a competitive edge, organizations are now focused on building custom brand voices with TTS, a strategy that has proven to increase user engagement at rates more than double that of generic voice systems. The impact of synthetic data on AI training continues to be a key area of research, with its potential to accelerate development cycles.

What are the key market drivers leading to the rise in the adoption of AI Voice Lab Industry?

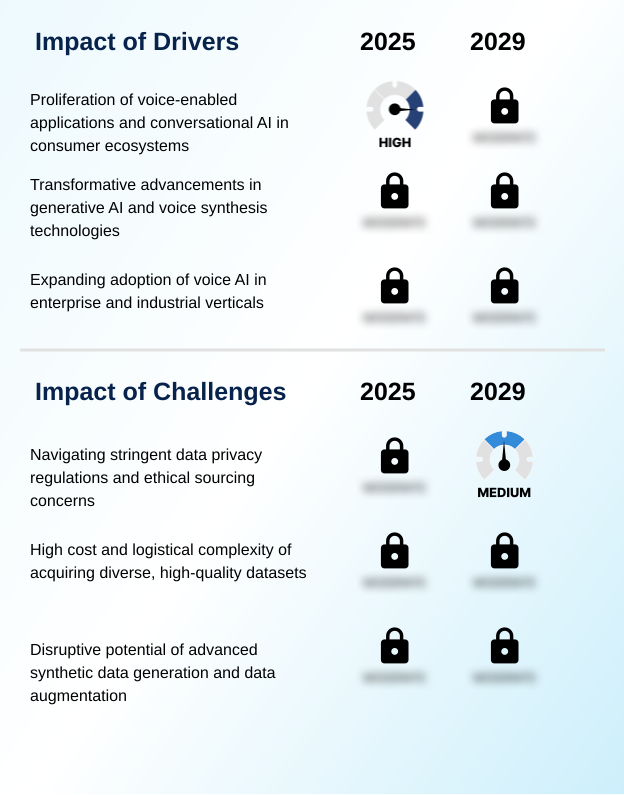

- The proliferation of voice-enabled applications and conversational AI across consumer ecosystems serves as a fundamental driver for market growth.

- Market growth is significantly driven by the enterprise adoption of voice AI to enhance operational efficiency and the rapid advancement of generative AI capabilities.

- The integration of automatic speech recognition (ASR) and natural language understanding (NLU) into core business processes is creating substantial value.

- For instance, logistics companies are achieving a 20% increase in picking accuracy by implementing voice-directed warehousing systems that utilize advanced noise suppression algorithms.

- In customer-facing roles, real-time transcription and context-aware voice AI are powering real-time agent assist tools that improve service quality.

- The proliferation of powerful speech-to-text (STT) models and sophisticated intonation modeling is also enabling more natural in-vehicle voice assistant interactions and fueling the market for AI-powered dubbing and other speech analytics solutions that require low-latency voice AI.

What are the market trends shaping the AI Voice Lab Industry?

- A primary market trend is the move toward hyper-personalization, driven by the commercialization of custom voice clones. This shift enables unique, brand-aligned sonic identities across various digital touchpoints.

- Key market trends are centered on hyper-personalization and emotional nuance, shifting focus toward expressive speech synthesis and advanced voice persona creation. The demand for custom branded voices is surging as companies adopt unique sonic branding strategies, with some reporting brand recall increases of over 25%.

- This is driven by breakthroughs in neural text-to-speech and voice cloning, allowing for the creation of unique vocal avatar generation. Furthermore, the integration of emotion detection is transforming user interactions, with systems capable of interpreting and reflecting sentiment improving customer satisfaction scores by up to 15%.

- This pursuit of more engaging experiences is also fueling the growth of automated dubbing solutions and making personalized voice AI for accessibility a commercial reality, moving beyond generic outputs to deliver truly lifelike synthetic voice generation.

What challenges does the AI Voice Lab Industry face during its growth?

- Navigating stringent data privacy regulations and ethical sourcing concerns poses a significant challenge to industry expansion and widespread adoption.

- Navigating data complexity and regulatory hurdles presents a significant market challenge. The high cost of ethical and GDPR voice data compliance can add 15-20% to project overheads, particularly for applications requiring sensitive emotional speech corpora or voice biomarker analysis.

- While the use of synthetic data for training offers a potential solution, its ability to replicate the nuances needed for technologies like ambient clinical intelligence or phoneme analysis remains limited. The rise of sophisticated zero-shot voice cloning and voice conversion technologies also introduces a critical need for robust deepfake detection frameworks to maintain trust.

- Moreover, achieving high-fidelity performance in multimodal AI and creating realistic generative voice skins requires overcoming significant technical obstacles related to data synchronization and model complexity, especially for HIPAA compliant voice data in healthcare.

Exclusive Technavio Analysis on Customer Landscape

The ai voice lab market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai voice lab market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI Voice Lab Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai voice lab market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon Web Services Inc. - Offering lifelike multilingual voices through GenAI-powered streaming synthesis, enabling dynamic text-to-speech applications with extensive customization for enterprise needs.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon Web Services Inc.

- CandyVoice

- Capacity

- Cisco Systems Inc.

- Descript

- Eleven Labs Inc.

- Google LLC

- IBM Corp.

- LOVO Inc

- Meta Platforms Inc.

- Microsoft Corp.

- Murf AI

- Nuance Communications Inc.

- NVIDIA Corp.

- ReadSpeaker B.V

- Resemble AI

- Synthesia Ltd.

- VoiceLab

- WellSaid Labs Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai voice lab market

- In November 2024, Eleven Labs Inc. announced a new funding round to scale its generative AI platform, focusing on advanced voice cloning and real-time automated dubbing solutions for media and entertainment clients.

- In January 2025, Volkswagen announced a strategic partnership with Cerence to integrate a ChatGPT-powered voice assistant into its production vehicles, aiming for a more natural, conversational in-cabin experience.

- In March 2025, Microsoft Corp. launched an expanded version of its Azure AI Speech services, featuring enhanced ambient clinical intelligence capabilities with over 98% accuracy for medical terminology transcription in real-world clinical settings.

- In May 2025, the European Commission introduced new guidelines for the ethical development and use of synthetic voice generation and voice biometrics, establishing a certification framework to ensure GDPR compliance for AI voice services in the EU.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Voice Lab Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 305 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 27.2% |

| Market growth 2025-2029 | USD 7212.6 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 22.9% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, UAE, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI voice lab market is defined by a rapid evolution from foundational automatic speech recognition (ASR) to advanced generative AI, fundamentally altering how organizations create and deploy vocal interfaces. This progression involves parallel innovations in speech-to-text (STT) for applications like real-time transcription and ambient clinical intelligence, alongside breakthroughs in text-to-speech (TTS) for synthetic voice generation.

- Core technical pillars include sophisticated acoustic modeling, prosody modeling for natural intonation, and reliable wake word detection. The integration of large language models (LLMs) is enhancing natural language understanding (NLU), making conversational IVR systems more effective. Key applications such as voice biometrics and voice-directed warehousing are becoming mainstream.

- Furthermore, technologies like zero-shot voice cloning are enabling the instant creation of custom branded voices, with deployments demonstrating customer engagement uplifts of over 20% compared to generic assistants. This complex landscape requires expertise in speaker diarization, emotion detection, and audio dataset annotation, while also addressing the security challenge of deepfake detection to ensure trust in all voice persona creation.

What are the Key Data Covered in this AI Voice Lab Market Research and Growth Report?

-

What is the expected growth of the AI Voice Lab Market between 2025 and 2029?

-

USD 7.21 billion, at a CAGR of 27.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Solution (Cloud-based, and On-premises), End-user (BFSI, Healthcare, IT and Telecom, Retail and E-commerce, and Others), Deployment (Platform, Services, and Managed Services) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Proliferation of voice-enabled applications and conversational AI in consumer ecosystems, Navigating stringent data privacy regulations and ethical sourcing concerns

-

-

Who are the major players in the AI Voice Lab Market?

-

Amazon Web Services Inc., CandyVoice, Capacity, Cisco Systems Inc., Descript, Eleven Labs Inc., Google LLC, IBM Corp., LOVO Inc, Meta Platforms Inc., Microsoft Corp., Murf AI, Nuance Communications Inc., NVIDIA Corp., ReadSpeaker B.V, Resemble AI, Synthesia Ltd., VoiceLab and WellSaid Labs Inc.

-

Market Research Insights

- Market dynamics are defined by a strategic pivot toward highly specialized applications, such as expressive speech synthesis and context-aware voice AI. This shift is creating significant value in niche areas, with adoption of HIPAA compliant voice data solutions climbing by 40% in healthcare for ambient intelligence applications.

- Concurrently, deployments of integrated voice-enabled workflows have increased operational efficiency in contact center automation by over 25%, driven by real-time agent assist features. The development of in-vehicle voice assistant systems and personalized audio content is further propelled by advances in edge AI speech processing, which enables low-latency interactions.

- These advancements are integral to creating sophisticated sonic branding strategies and delivering seamless user experiences across a growing range of connected devices.

We can help! Our analysts can customize this ai voice lab market research report to meet your requirements.

RIA -

RIA -