Amorphous Silicon Solar Cell Market Size 2025-2029

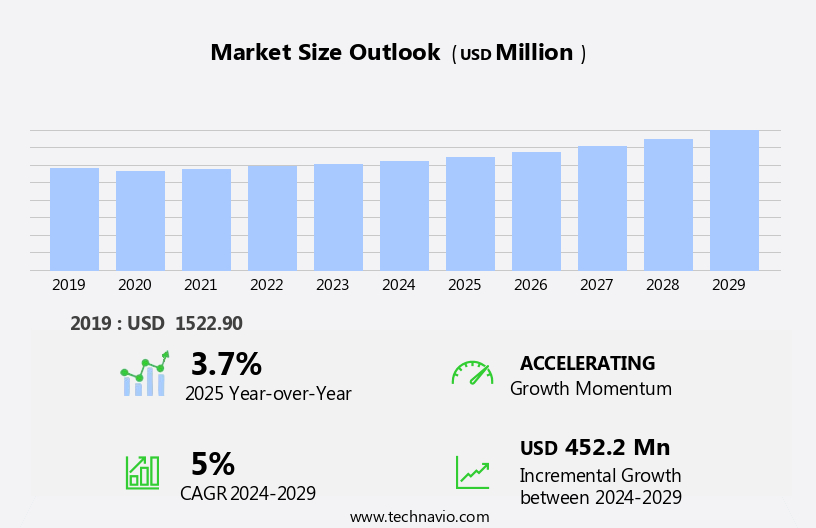

The amorphous silicon solar cell market size is forecast to increase by USD 452.2 million, at a CAGR of 5% between 2024 and 2029.

- The market is driven by the cost-effectiveness of amorphous silicon technology, making it an attractive alternative for manufacturers seeking to produce solar cells at lower costs compared to traditional crystalline silicon cells. This cost advantage is particularly significant in emerging economies where solar energy adoption is on the rise. Key players in the market, such as SolarWorld, SunPower, and Heliovolt, are investing in new product launches to expand their offerings and capture a larger market share. For instance, SolarWorld introduced its new thin-film module series, which combines amorphous silicon technology with advanced manufacturing techniques to improve efficiency and reduce costs.

- However, the market faces challenges, including the lower efficiency of amorphous silicon solar cells compared to crystalline silicon. Despite advancements in technology, amorphous silicon cells still lag behind crystalline silicon in terms of energy conversion efficiency. This efficiency gap limits the market potential for amorphous silicon solar cells in applications where high efficiency is a critical requirement, such as utility-scale solar power plants. Additionally, the market is also affected by the ongoing research and development efforts to improve the efficiency of amorphous silicon solar cells. These challenges create opportunities for companies to invest in research and development, innovate new technologies, and differentiate themselves from competitors.

- Companies that can successfully address these challenges and offer high-performing, cost-effective amorphous silicon solar cells will be well-positioned to capitalize on the market's growth potential.

What will be the Size of the Amorphous Silicon Solar Cell Market during the forecast period?

Amorphous silicon solar cells continue to evolve as a significant player in the solar energy market, with ongoing research and development driving advancements in design and performance. Solar cell design is a critical aspect of this evolution, with current-voltage measurements and next-generation solar cells under constant scrutiny to optimize efficiency and reduce costs. Anti-reflective coatings and chemical vapor deposition techniques are essential in enhancing the photovoltaic conversion efficiency of these cells. Cost optimization is a continuous priority, with silicon-based solar cells and thin-film technology offering potential solutions. Net metering and grid integration are essential for the widespread adoption of solar energy, with market penetration depending on the success of these initiatives.

Band gap engineering and stability testing are crucial in ensuring the longevity and reliability of these cells, with spectral response and power electronics playing essential roles in maximizing energy output. The solar industry's growth is driven by the need for sustainable development and the increasing demand for renewable energy sources. Solar energy applications span various sectors, from Rooftop Solar and ground-mounted solar to solar farms and solar water heating. The ongoing research in photovoltaic cells, including hydrogenated amorphous silicon and perovskite solar cells, promises further advancements in the field. Roll-to-roll manufacturing and plasma deposition techniques are essential in increasing production yield and reducing costs.

energy storage solutions, such as batteries, are becoming increasingly important in the solar energy landscape, with off-grid power systems offering potential for remote areas and developing countries. The solar industry's growth is influenced by various factors, including solar energy policy, feed-in tariffs, and environmental impact assessments. In summary, the market is a dynamic and evolving landscape, with continuous research and development driving advancements in design, performance, and cost optimization. The ongoing pursuit of higher efficiency, reliability, and affordability is essential in ensuring the widespread adoption of solar energy as a viable and sustainable energy source.

How is this Amorphous Silicon Solar Cell Industry segmented?

The amorphous silicon solar cell industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Technology

- Single-junction

- Multi-junction

- End-user

- Residential

- Commercial

- Industrial

- Geography

- North America

- US

- Europe

- France

- Germany

- Italy

- UK

- APAC

- Australia

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Technology Insights

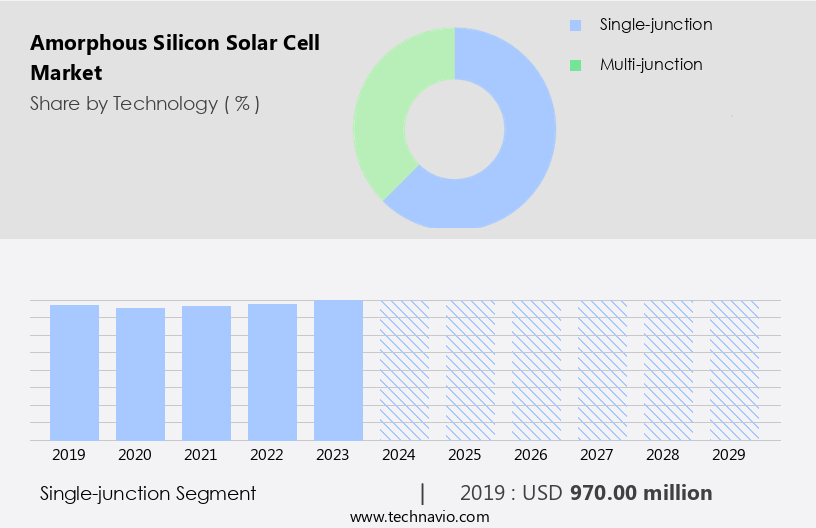

The single-junction segment is estimated to witness significant growth during the forecast period.

Amorphous silicon (a-Si) solar cells, characterized by a single layer of amorphous silicon material, offer a cost-effective and simple design for converting sunlight into electrical energy. These cells, which are the basis for single-junction a-Si solar technology, are widely used in various applications due to their cost efficiency. They are particularly popular in smaller, budget-conscious products, such as portable solar chargers, consumer electronics, and building-integrated photovoltaics (BIPV). Solar simulators are essential tools for evaluating the performance of a-Si solar cells. Degradation, specifically light-induced degradation, is a significant challenge in the a-Si solar cell market. Thin-film solar cells, including a-Si cells, employ silicon nitride passivation to mitigate degradation and enhance efficiency.

Solar energy applications, such as solar farms and rooftop installations, are expanding, driving demand for solar cell development. Battery storage and grid integration are crucial components of renewable energy systems. Solar energy policy and net metering incentives influence market penetration. Solar panel efficiency, a key performance metric, is continually improving through research on quantum efficiency, band gap engineering, and photovoltaic conversion. Flexible solar cells and building-integrated photovoltaics (BIPV) are emerging trends in the solar industry. Solar cell manufacturing processes, such as plasma deposition, chemical vapor deposition, and roll-to-roll manufacturing, are essential for optimizing production yield and reducing costs.

The Single-junction segment was valued at USD 970.00 million in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

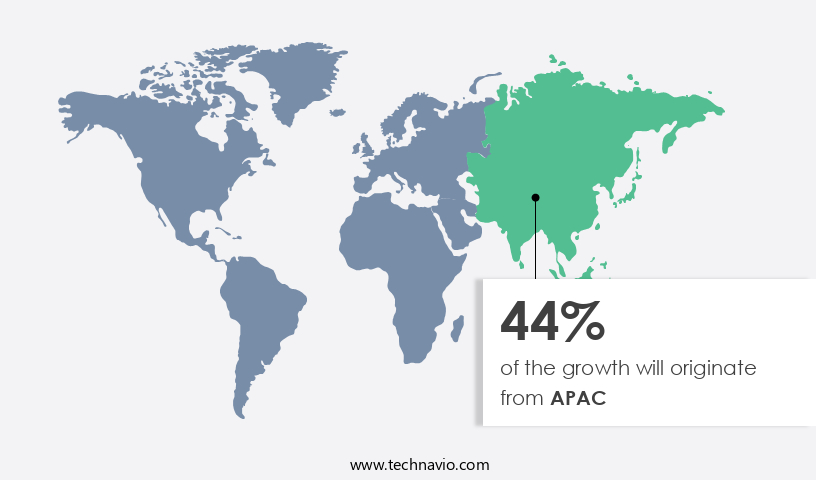

APAC is estimated to contribute 44% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in the Asia-Pacific (APAC) region is experiencing significant growth due to substantial investments and technological advancements in solar energy. Key contributors to this growth include China, India, Japan, and Australia, which are leading the way in the solar energy sector. In 2023, China saw a remarkable 55% increase in solar capacity installations compared to the previous year, making it a global leader in solar technology, accounting for over 40% of global solar panel production. Amorphous silicon solar cells are extensively used in both residential and commercial applications, reflecting China's commitment to renewable energy. Japan and India are also making strides in solar energy, with Japan focusing on Building Integrated Photovoltaics and India investing in rooftop solar installations.

Australia, with its abundant sunlight, is a significant market for ground-mounted solar farms. The region's commitment to sustainable development is further evidenced by the widespread adoption of solar energy for solar water heating and grid integration. Solar cell research and development continue, with a focus on improving solar panel efficiency, reducing environmental impact, and increasing production yield through technologies like plasma deposition, roll-to-roll manufacturing, and hydrogenated amorphous silicon. The solar industry is also exploring next-generation solar cells, such as perovskite solar cells and organic solar cells, to enhance efficiency and reduce costs. Solar energy policy, including feed-in tariffs and net metering, is driving market penetration and grid-tied solar systems.

The solar cell market is expected to continue growing, with a focus on cost optimization, band gap engineering, and photovoltaic conversion.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Amorphous Silicon Solar Cell Industry?

- Amorphous silicon technology's cost-effectiveness is a primary factor driving market growth. This technology's affordability sets it apart from other alternatives, making it an attractive choice for various applications.

- Amorphous silicon (a-Si) solar cells offer an economical alternative to traditional crystalline silicon solar cells in the global market. The cost-effectiveness of a-Si technology is primarily attributed to its simpler and less expensive manufacturing process. Utilizing thin-film deposition techniques, a-Si solar cells require less material and energy compared to crystalline silicon cells, leading to reduced production costs. Moreover, a-Si solar cells have gained popularity due to their versatility in various applications, especially in cost-sensitive markets. Grid-tied solar systems and solar water heating systems are some of the major applications where a-Si solar cells are used due to their environmental benefits and efficiency.

- Solar energy research continues to focus on improving the solar cell lifetime, production yield, and environmental impact of a-Si solar cells. Technological advancements in amorphous silicon deposition, such as plasma deposition, have led to significant improvements in the performance and durability of a-Si solar cells. Furthermore, the integration of a-Si solar cells with energy storage systems and off-grid power systems has expanded their applications, contributing to the growth of the solar industry. Transparent conductive oxides are also being used to enhance the performance of a-Si solar cells, making them suitable for use in building-integrated photovoltaics.

- In conclusion, the cost-effective manufacturing process, versatility, and ongoing research and development efforts make amorphous silicon solar cells a compelling option in the solar energy market.

What are the market trends shaping the Amorphous Silicon Solar Cell Industry?

- The trend in the market is toward new product launches by companies. This is a mandatory development in the business world, reflecting innovation and competition.

- The market is experiencing notable progress due to the introduction of advanced solar cell designs. One recent example is Panasonic Industry's launch of the Amorton series of hydrogenated amorphous silicon (a-Si:H) solar cells. These new solar cells, including the AMG-1401C and AMG-1701C models, are specifically engineered for indoor energy harvesting applications. They offer improved efficiency and an aesthetically pleasing design, making them suitable for various consumer electronics, IoT devices, and sensor nodes. The Amorton series' cost-optimized design is a significant market differentiator. This cost optimization is achieved through the use of advanced manufacturing techniques such as chemical vapor deposition and sputtering deposition.

- Additionally, these solar cells undergo rigorous stability testing, spectral response analysis, and current-voltage measurement to ensure optimal performance. These next-generation solar cells also incorporate anti-reflective coatings to maximize photovoltaic conversion efficiency. Furthermore, power electronics are integrated into the design to facilitate seamless net metering and grid connectivity. In summary, the market is driven by continuous innovation, with companies focusing on improving efficiency, design, and cost optimization. Panasonic Industry's Amorton series is a prime example of these advancements, offering a cost-effective, efficient, and visually appealing solution for indoor energy harvesting applications.

What challenges does the Amorphous Silicon Solar Cell Industry face during its growth?

- The lower efficiency of solar technologies other than crystalline silicon poses a significant challenge to the growth of the solar industry.

- Amorphous silicon solar cells face a significant challenge in the global market due to their lower energy conversion efficiency compared to crystalline silicon solar cells. This efficiency gap impacts the competitiveness of a-Si technology, particularly in large-scale solar energy applications. Amorphous silicon solar cells typically achieve energy conversion efficiencies of 6% to 9%, while crystalline silicon solar cells, which include monocrystalline and polycrystalline types, have significantly higher efficiencies, ranging from 15% to 22%. The substantial difference in efficiency means that a-Si cells generate less electricity from the same amount of sunlight, making them less effective for applications where maximizing energy output is crucial.

- However, amorphous silicon solar cells offer advantages such as lower manufacturing costs and flexibility in design, making them suitable for specific applications, such as solar simulator testing and solar cell research. To address the efficiency challenge, researchers are focusing on improving the quality of the thin-film layers, including the tco layer, and implementing silicon nitride passivation. Additionally, solar energy policy incentives and advancements in battery storage technology are expanding the market for a-Si solar cells in solar energy applications, including rooftop solar and ground-mounted solar. Light-induced degradation and solar cell degradation are other challenges that require ongoing research and development efforts to ensure the longevity and reliability of a-Si solar cells.

- Despite these challenges, the market for a-Si solar cells is expected to grow due to their unique advantages and the increasing demand for renewable energy sources.

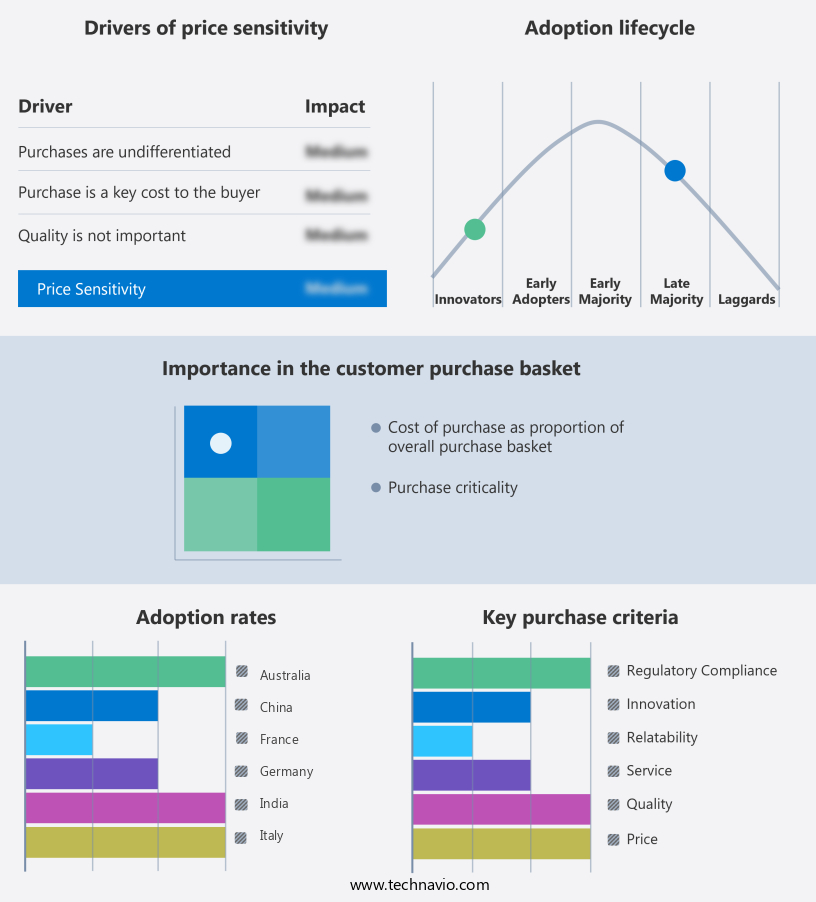

Exclusive Customer Landscape

The amorphous silicon solar cell market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the amorphous silicon solar cell market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, amorphous silicon solar cell market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Canadian Solar Inc.

- First Solar Inc.

- GCL System Integration Technology Co. Ltd.

- Global Solar Energy

- Hanergy Thin Film Power EME BV

- Hanwha Corp.

- HelioVolt Corp.

- JinkoSolar Holding Co. Ltd.

- MiaSole Hi-Tech Corp.

- Risen Energy Co. Ltd.

- Sharp Corp.

- Solar Frontier Europe GmbH

- Solarworld Energy Solutions

- Soltecture GmbH

- SunPower Corp.

- Tokyo Electron Ltd.

- Trina Solar Co. Ltd.

- United Solar Ovonic Inc.

- Wuxi Suntech Power Co. Ltd.

- Yingli Solar

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Amorphous Silicon Solar Cell Market

- In February 2023, Hanergy Holding Group, a leading amorphous silicon solar cell manufacturer, announced the launch of its new high-performance amorphous silicon solar module, achieving a record-breaking conversion efficiency of 16.2%. This breakthrough development underscores Hanergy's commitment to pushing the boundaries of amorphous silicon solar technology (Hanergy press release, 2023).

- In November 2024, Panasonic Corporation and First Solar, Inc. Entered into a strategic partnership to jointly develop and commercialize amorphous silicon thin-film solar cells. This collaboration combines Panasonic's expertise in amorphous silicon technology with First Solar's manufacturing capabilities, aiming to enhance their respective product offerings and competitiveness in the solar market (First Solar press release, 2024).

- In March 2025, Merck KGaA, a leading science and technology company, secured a â¬100 million investment from the European Investment Bank to expand its production capacity for amorphous silicon solar cells. This funding will enable Merck to increase its production capacity by 50%, strengthening its position as a key player in the European solar market (European Investment Bank press release, 2025).

- In June 2025, the Indian government announced the National Solar Mission 4.0, which includes a significant focus on the deployment of amorphous silicon solar cells. The initiative aims to install 60 GW of solar capacity by 2030, with amorphous silicon cells contributing at least 10 GW. This policy shift presents a significant opportunity for amorphous silicon solar cell manufacturers to expand their market presence in India (Ministry of New and Renewable Energy press release, 2025).

Research Analyst Overview

- Amorphous silicon solar cells have emerged as a significant player in the solar energy market, offering cost-effective and flexible solar energy solutions for various applications. The integration of amorphous silicon technology into solar energy systems has led to the development of thin-film solar panels, solar cell arrays, and modules, contributing to the growth of the solar energy industry. Silicon crystal growth and purification processes are crucial for enhancing solar cell reliability and efficiency, driving innovation in silicon-based photovoltaics. Solar Energy Storage and policy initiatives are key factors propelling the renewable energy market forward, with amorphous silicon solar cells playing a pivotal role in solar power generation and conversion.

- Solar energy innovations continue to shape the landscape of the solar energy industry, with a focus on improving solar cell materials and applications to boost efficiency and reduce costs. The solar energy market is witnessing substantial investment, with stakeholders recognizing the potential of amorphous silicon technology to revolutionize solar energy infrastructure and power systems. Solar energy technologies are poised to disrupt traditional energy sources, offering sustainable and green energy solutions for businesses and consumers alike.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Amorphous Silicon Solar Cell Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

199 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5% |

|

Market growth 2025-2029 |

USD 452.2 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

3.7 |

|

Key countries |

US, China, Japan, South Korea, Germany, India, France, Italy, UK, and Australia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Amorphous Silicon Solar Cell Market Research and Growth Report?

- CAGR of the Amorphous Silicon Solar Cell industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the amorphous silicon solar cell market growth of industry companies

We can help! Our analysts can customize this amorphous silicon solar cell market research report to meet your requirements.

RIA -

RIA -