Amphibious Landing Craft Market Size 2026-2030

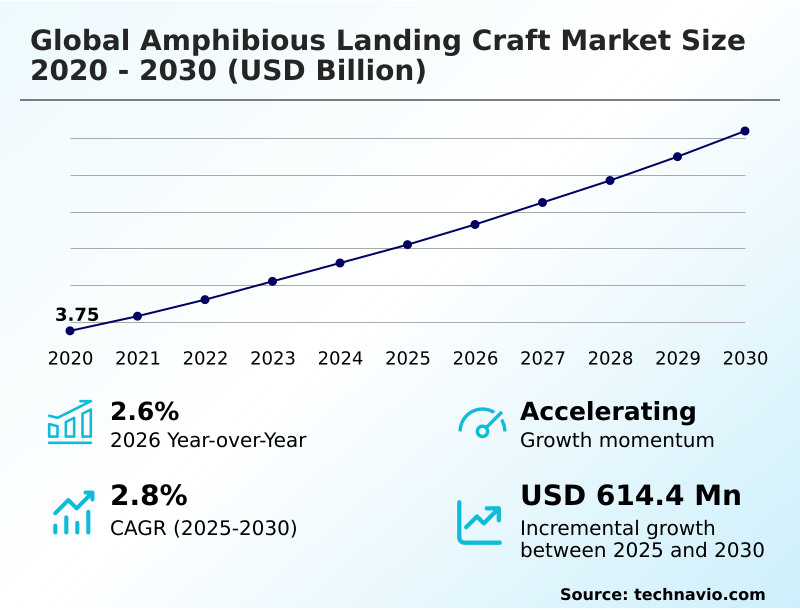

The amphibious landing craft market size is valued to increase by USD 614.4 million, at a CAGR of 2.8% from 2025 to 2030. Accelerating naval fleet modernization programs and aging asset replacement will drive the amphibious landing craft market.

Major Market Trends & Insights

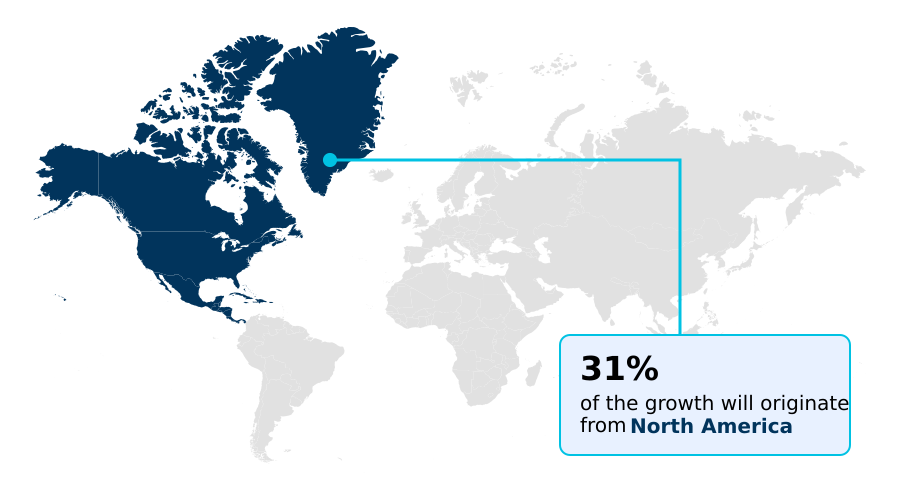

- North America dominated the market and accounted for a 31.1% growth during the forecast period.

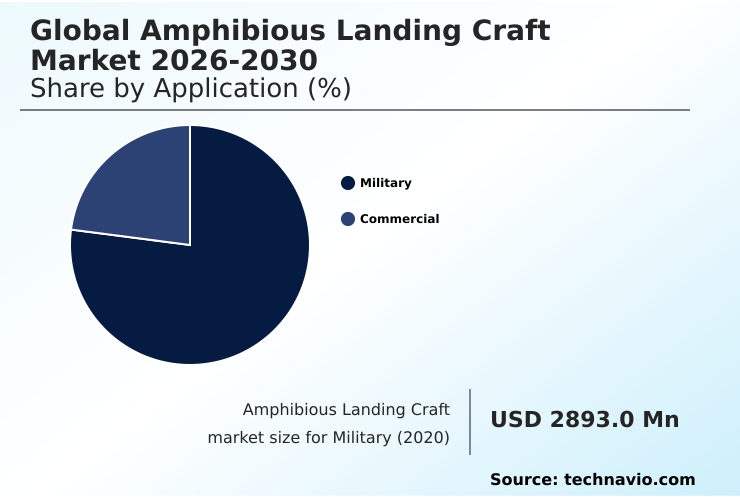

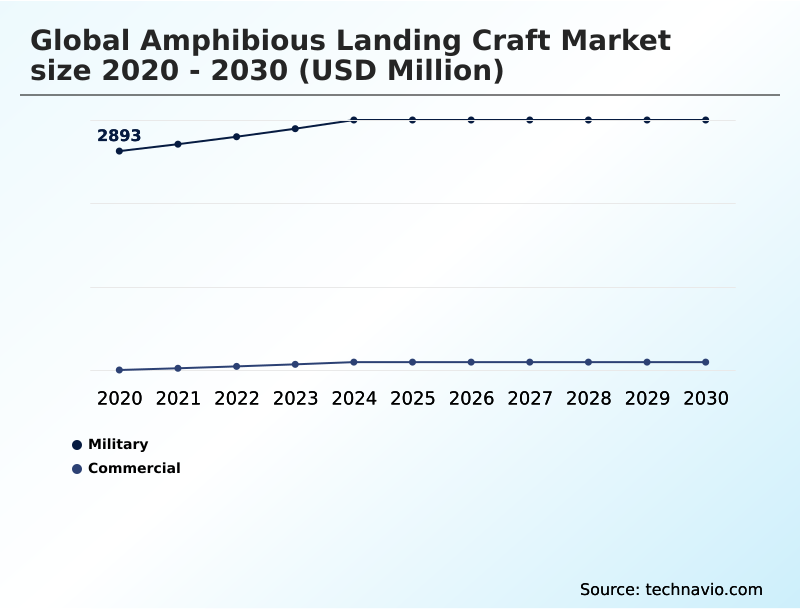

- By Application - Military segment was valued at USD 3.18 billion in 2024

- By Type - Amphibious ACVs and APCs segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1.08 billion

- Market Future Opportunities: USD 614.4 million

- CAGR from 2025 to 2030 : 2.8%

Market Summary

- The amphibious landing craft market is defined by the strategic need to project force and sustain operations in coastal and riverine environments. Central to this is the evolution of platforms designed for expeditionary warfare, enabling the seamless transition of troops and equipment from sea to land.

- Key drivers include widespread naval fleet modernization and geopolitical tensions, which demand more capable ship-to-shore connector assets. A significant trend involves the integration of autonomous navigation systems to reduce human risk during over-the-horizon assault missions. For instance, a naval task force can utilize unmanned surface vessels for initial reconnaissance and logistics, reducing exposure of crewed platforms by over 40%.

- This shift toward technologically advanced, multi-role vessels capable of operating in contested littoral warfare scenarios, such as landing craft air cushion (LCAC) and landing craft utility (LCU) types, underscores the market's focus on speed, survivability, and operational flexibility to support distributed maritime operations and maintain a credible defense posture.

What will be the Size of the Amphibious Landing Craft Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Amphibious Landing Craft Market Segmented?

The amphibious landing craft industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Military

- Commercial

- Type

- Amphibious ACVs and APCs

- Air cushion vehicle

- LCU and LCM

- Usage

- Amphibious operations

- Naval operations

- Maritime security

- Others

- End-user

- Vehicle transportation

- Infantry transportation

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Application Insights

The military segment is estimated to witness significant growth during the forecast period.

The military segment is the primary force in the amphibious landing craft market, where mission-critical demands for force projection capabilities and maritime power projection drive procurement.

Modernization is focused on enhancing expeditionary warfare assets to support joint amphibious operations and maintain dominance in littoral combat operations. These platforms are essential for ship-to-shore logistics, enabling the deployment of naval infantry units and equipment.

Military applications steer over 75% of procurement decisions, focusing on vessels that ensure access and presence in contested environments.

The integration of advanced combat systems and robust designs for high-threat scenarios underscores the segment's strategic importance in national defense and expeditionary strike group readiness.

The Military segment was valued at USD 3.18 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 31.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Amphibious Landing Craft Market Demand is Rising in North America Get Free Sample

The geographic landscape of the market is shaped by distinct regional priorities and strategic investments in sea-based logistics. North America leads, accounting for nearly 31% of incremental growth, driven by extensive modernization programs for its expeditionary advanced base operations.

The APAC region follows closely, representing over 23% of the opportunity, fueled by escalating geopolitical tensions that necessitate robust coastal defense strategies. Vessels in this region increasingly feature advanced C4ISR integration to manage complex maritime domains.

In Europe, the focus is on interoperability within allied amphibious task forces, while nations in the Middle East and Africa invest in platforms to secure sea lines of communication and support anti-piracy missions, highlighting a global demand for specialized, high-performance amphibious assets.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The development of next-generation platforms is a complex process, with high speed landing craft design being a primary focus for planners. A key debate centers on LCU vs LCM operational differences, weighing heavy-lift capacity against speed and deployability.

- Modern amphibious vehicle survivability features, such as advanced ballistic protection for landing craft and signature reduction technologies, are non-negotiable in the face of sophisticated anti access area denial countermeasures. The shift towards modular landing craft for HADR is gaining traction, allowing for rapid reconfiguration of non-combat missions.

- Technologically, hybrid propulsion in landing craft is becoming a standard requirement to enhance range and stealth. Concurrently, the development of autonomous amphibious assault craft and unmanned surface vessel for logistics is accelerating, influenced heavily by strategic frameworks like the US marine corps force design.

- This initiative re-evaluates everything from LCAC payload and range limitations to the integration of C4ISR systems for amphibious forces. The ultimate goal is to achieve superior high speed transit for expeditionary forces, overcoming sea state limitations for landing craft through innovations like hydrodynamic hull design for efficiency.

- These platforms must support diverse mission sets, incorporating a modular payload for expeditionary missions and enabling effective beachhead insertion tactics and technology within the broader context of littoral combat ship mission modules and amphibious assault ship capabilities.

What are the key market drivers leading to the rise in the adoption of Amphibious Landing Craft Industry?

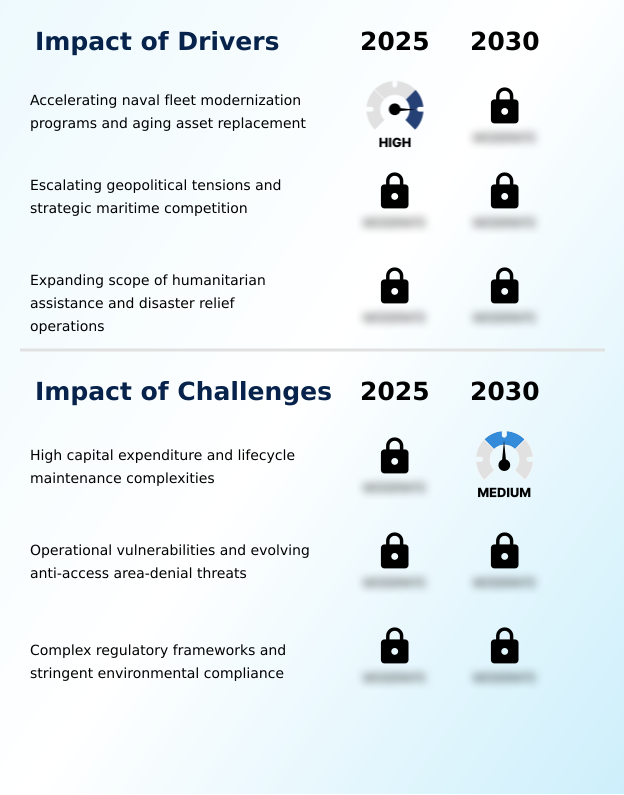

- Accelerating naval fleet modernization programs and the replacement of aging assets are key drivers of the market.

- The market is propelled by a convergence of strategic imperatives, including comprehensive naval fleet modernization efforts.

- As aging assets reach the end of their service life, there is a sustained push for next-generation platforms that enhance maritime power projection and support an amphibious readiness group.

- Escalating geopolitical tensions, particularly in contested maritime zones, are fueling demand for vessels that can ensure control over vital sea lines of communication, with regional defense spending increasing by an average of 8% in key hotspots.

- Furthermore, the expanding scope of humanitarian assistance and disaster relief (HADR) operations has broadened the mission profile for these assets. Such missions now account for 15% of annual deployments in some fleets, underscoring the dual-use value of modern amphibious craft.

What are the market trends shaping the Amphibious Landing Craft Industry?

- Technological advancements, including autonomous and remote-controlled navigation systems, are a significant emerging trend shaping the market.

- Key trends are reshaping the market, with a strong emphasis on technological superiority and operational flexibility. The development of advanced autonomous navigation systems is critical, with pilot programs demonstrating a 30% reduction in crew workload during complex littoral maneuvers.

- Another significant shift is the adoption of hybrid-electric propulsion, which enables silent running capabilities for stealthy beachhead insertion and can lower fuel consumption by up to 25%. The demand for modular vessel architectures is also rising, as modular payload bay designs allow for mission reconfiguration in less than 24 hours, compared to weeks for legacy platforms.

- These innovations in roll-on/roll-off capability and unmanned surface vessel technology are setting new standards for expeditionary fast transport and over-the-beach logistics.

What challenges does the Amphibious Landing Craft Industry face during its growth?

- High capital expenditure and complex lifecycle maintenance present a key challenge affecting industry growth.

- The market faces significant challenges, primarily stemming from the high capital expenditure required for modern amphibious platforms. Lifecycle maintenance costs can exceed 60% of a vessel's total ownership cost, straining defense budgets.

- Operationally, the proliferation of advanced anti-access/area-denial (A2/AD) threats creates a formidable challenge, with modern coastal defense systems capable of creating exclusion zones extending over 200 nautical miles, making ship-to-shore transit increasingly perilous. This A2/AD environment heightens the vulnerability of assets like the landing craft air cushion (LCAC).

- Additionally, complex regulatory frameworks and stringent environmental compliance standards add layers of cost and time to development, demanding solutions like hybrid propulsion in landing craft and adherence to strict emissions protocols for expeditionary warfare platforms.

Exclusive Technavio Analysis on Customer Landscape

The amphibious landing craft market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the amphibious landing craft market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Amphibious Landing Craft Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, amphibious landing craft market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abu Dhabi Ship Building PJSC - Key offerings include specialized Landing Craft Utility and Vehicle Personnel variants, delivering robust troop and vehicle transport solutions for modern naval operations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abu Dhabi Ship Building PJSC

- Almaz Shipbuilding Company

- Austal Ltd.

- BAE Systems Plc

- CNIM SA

- Damen Shipyards Group

- Fincantieri Spa

- General Dynamics NASSCO

- Goa Shipyard Ltd.

- Griffon Hoverwork Ltd.

- Huntington Ingalls Industries

- Iveco Defence Vehicles

- Marine Alutech Oy Ab

- Marine Inland Fabricators

- Mitsubishi Heavy Industries

- Naval Group

- Navantia SA

- ST Engineering Ltd.

- Strategic Marine S Pte Ltd.

- Textron Systems

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Amphibious landing craft market

- In September, 2024, Damen Shipyards Group announced a strategic partnership with a leading automation software firm to develop an advanced autonomous navigation module for its Landing Craft Utility (LCU) series, aiming to reduce crew risk in contested environments.

- In February, 2025, BMT and Japan Marine United secured a contract from Japan's Acquisition, Technology, and Logistics Agency to design the Caimen, a next-generation high-speed landing craft tailored for complex island chain geographies.

- In March, 2025, Textron Systems initiated testing for the next-generation Landing Craft Air Cushion (LCAC) 100 with the US Navy, a platform offering increased payload and improved reliability for over-the-horizon missions.

- In May, 2025, BAE Systems Plc received a follow-on contract from the US Marine Corps for the full-rate production of additional Amphibious Combat Vehicle (ACV) variants, enhancing ship-to-shore mobility and troop protection.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Amphibious Landing Craft Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 318 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 2.8% |

| Market growth 2026-2030 | USD 614.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 2.6% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The amphibious landing craft market is undergoing a strategic realignment, shifting from monolithic platforms to a more distributed and technologically advanced fleet architecture. This evolution is driven by the need to conduct expeditionary warfare in highly contested A2/AD environments.

- Key vendors are focused on developing next-generation assets, including the ship-to-shore connector and advanced amphibious combat vehicle (ACV) models, which emphasize speed, survivability, and C4ISR integration. A crucial trend is the incorporation of a modular payload bay, which allows for rapid mission reconfiguration.

- For instance, platforms with this feature can reduce refit times by up to 30%, a critical factor influencing boardroom decisions on lifecycle costs and operational flexibility. The move towards high-speed transit and over-the-horizon assault capabilities is redefining vessel requirements, with an emphasis on advanced hydrodynamic hull designs and hybrid-electric propulsion.

- This push for innovation ensures that naval forces can maintain effective littoral warfare capabilities, from beachhead insertion using landing craft air cushion (LCAC) technology to sustained logistics with landing craft utility (LCU) and landing craft mechanized (LCM) platforms. The market is also heavily influenced by the need for enhanced sea state tolerance and robust ballistic protection.

What are the Key Data Covered in this Amphibious Landing Craft Market Research and Growth Report?

-

What is the expected growth of the Amphibious Landing Craft Market between 2026 and 2030?

-

USD 614.4 million, at a CAGR of 2.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Military, and Commercial), Type (Amphibious ACVs and APCs, Air cushion vehicle, and LCU and LCM), Usage (Amphibious operations, Naval operations, Maritime security, and Others), End-user (Vehicle transportation, Infantry transportation, and Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Accelerating naval fleet modernization programs and aging asset replacement, High capital expenditure and lifecycle maintenance complexities

-

-

Who are the major players in the Amphibious Landing Craft Market?

-

Abu Dhabi Ship Building PJSC, Almaz Shipbuilding Company, Austal Ltd., BAE Systems Plc, CNIM SA, Damen Shipyards Group, Fincantieri Spa, General Dynamics NASSCO, Goa Shipyard Ltd., Griffon Hoverwork Ltd., Huntington Ingalls Industries, Iveco Defence Vehicles, Marine Alutech Oy Ab, Marine Inland Fabricators, Mitsubishi Heavy Industries, Naval Group, Navantia SA, ST Engineering Ltd., Strategic Marine S Pte Ltd. and Textron Systems

-

Market Research Insights

- Market dynamics are increasingly influenced by the need for enhanced operational effectiveness in complex maritime security operations. The adoption of platforms with hybrid-electric propulsion is a key factor, with some systems demonstrating a 20% reduction in acoustic signatures, crucial for stealth in coastal surveillance.

- Furthermore, the integration of autonomous navigation systems can improve mission success rates in contested environments by over 25% compared to manned-only operations, enabling safer ship-to-shore logistics.

- This focus on technological superiority supports everything from anti-piracy missions to large-scale humanitarian assistance and disaster relief (HADR), reflecting a strategic shift toward versatile assets that bolster force projection capabilities while optimizing performance for rapid deployment forces.

We can help! Our analysts can customize this amphibious landing craft market research report to meet your requirements.

RIA -

RIA -