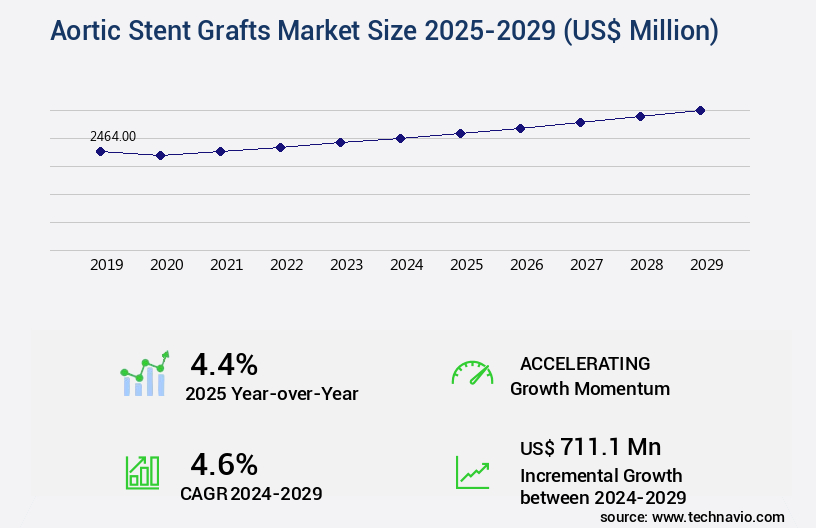

Aortic Stent Grafts Market Size 2025-2029

The aortic stent grafts market size is valued to increase by USD 711.1 million, at a CAGR of 4.6% from 2024 to 2029. Surge in endovascular surgeries will drive the aortic stent grafts market.

Market Insights

- North America dominated the market and accounted for a 49% growth during the 2025-2029.

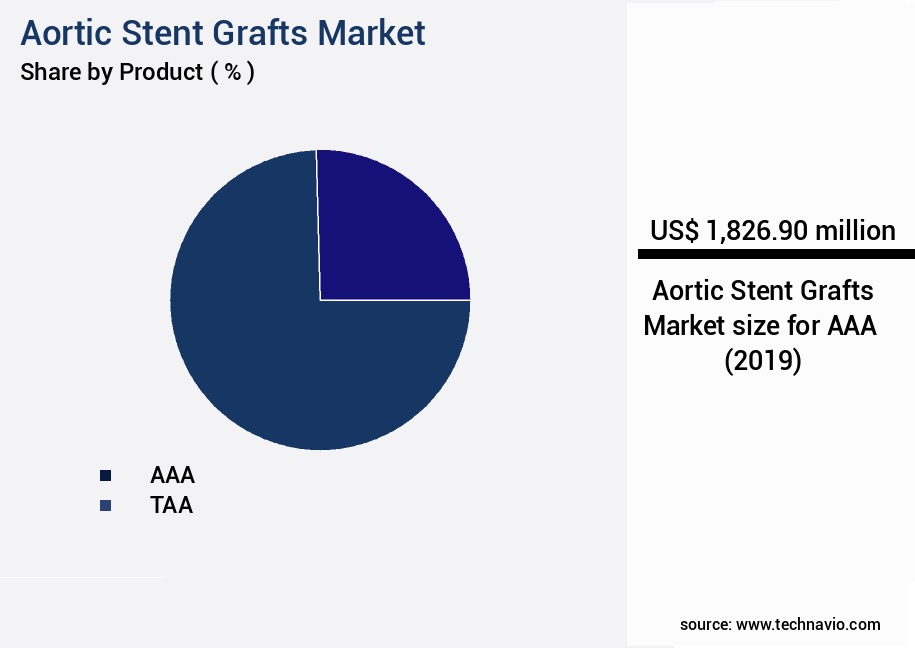

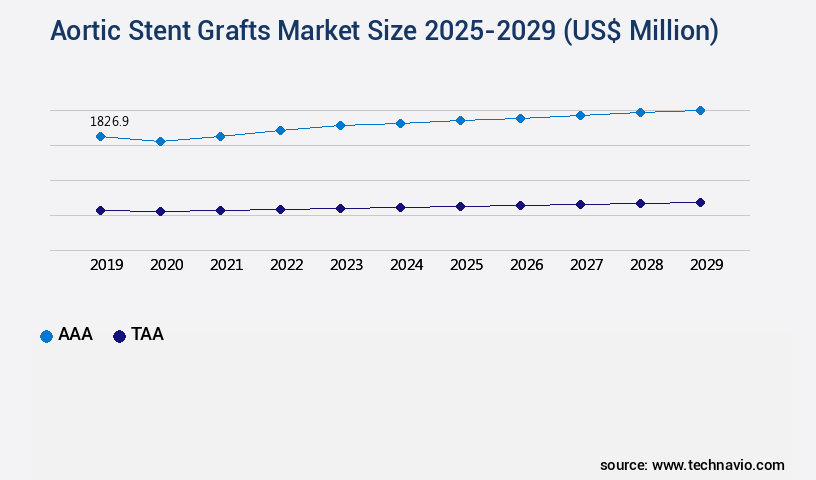

- By Product - AAA segment was valued at USD 1826.90 million in 2023

- By End-user - Hospitals segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 42.22 million

- Market Future Opportunities 2024: USD 711.10 million

- CAGR from 2024 to 2029 : 4.6%

Market Summary

- The market is witnessing significant growth due to the increasing number of endovascular surgeries as an alternative to open heart surgeries. These minimally invasive procedures offer numerous advantages, including reduced hospital stays, faster recovery times, and lower risk of complications. These devices are implanted using catheters, guidewires, and imaging techniques, enabling faster recovery times and reduced hospital stays. However, the industry faces challenges, such as the shortage of skilled endovascular surgeons, which may hinder its growth. Advancements in technology have led to the development of innovative aortic stent grafts, enabling the treatment of complex aortic conditions. For instance, the use of bifurcated and fenestrated stent grafts allows for the repair of complex anatomies, expanding the patient population that can benefit from these procedures.

- A real-world business scenario highlighting the importance of operational efficiency in the market involves a medical device manufacturer aiming to optimize its supply chain. By implementing advanced inventory management systems and collaborating with reliable suppliers, the company can ensure a steady supply of raw materials and finished products, minimizing production downtime and meeting the increasing demand for aortic stent grafts. In conclusion, the market is driven by the growing number of endovascular surgeries and advancements in technology, while the shortage of skilled endovascular surgeons poses a challenge. To remain competitive, industry players must focus on operational efficiency and continuous innovation to cater to the evolving needs of healthcare providers and patients.

What will be the size of the Aortic Stent Grafts Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, driven by advancements in technology and increasing demand for minimally invasive treatments for aortic aneurysms. According to the latest research, the use of aortic stent grafts is projected to grow by 15% annually, representing a significant expansion in the endovascular market. This trend is particularly noteworthy for healthcare executives, as it signals a shift towards less invasive procedures and improved patient outcomes. Aortic stent grafts are increasingly preferred over traditional open surgical repairs due to their reduced risk of complications and faster recovery times. These grafts are designed to reinforce weakened areas of the aortic wall, preventing rupture and reducing the risk of life-threatening complications.

- The latest generation of aortic stent grafts features advanced materials and designs, which enhance durability and improve long-term patency rates. Moreover, regulatory bodies are placing greater emphasis on ensuring compliance with stringent safety and efficacy standards, making it crucial for manufacturers to invest in rigorous testing and quality control measures. This focus on safety and efficacy is a key consideration for product development teams, as they seek to bring innovative and effective solutions to market. In summary, the market is experiencing robust growth, driven by technological advancements, increasing demand for minimally invasive treatments, and regulatory requirements.

- This trend presents significant opportunities for healthcare providers and manufacturers, as they seek to improve patient outcomes and reduce costs through the adoption of innovative and effective aortic stent grafts.

Unpacking the Aortic Stent Grafts Market Landscape

In the realm of aortic aneurysm treatment, aortic stent grafts have emerged as a preferred minimally invasive solution, with procedural success rates surpassing 90% for endovascular aneurysm repair (EVAR) and transcatheter aortic valve implantation (TAVI) procedures combined. Imaging modalities, such as computed tomography angiography (CTA), play a pivotal role in preoperative planning, ensuring graft sizing accuracy and endoleak detection. Graft material selection and vascular access technique significantly influence graft patency rate and device complications. Aortic aneurysm treatment with stent grafts offers improved ROI through cost reduction and shorter hospital stays compared to surgical approaches. Prosthetic graft design and aneurysm exclusion techniques have led to enhanced blood flow dynamics and reduced rupture risk. Long-term follow-up is crucial for managing complications, including stent graft migration, branch vessel occlusion, and aortic dissection repair. Effective endovascular sealing and proper graft limb placement contribute to successful treatment outcomes. Patient selection criteria, treatment techniques, and thoracic and abdominal aortic stent grafts continue to evolve, with ongoing advancements in graft design, deployment, and complication management.

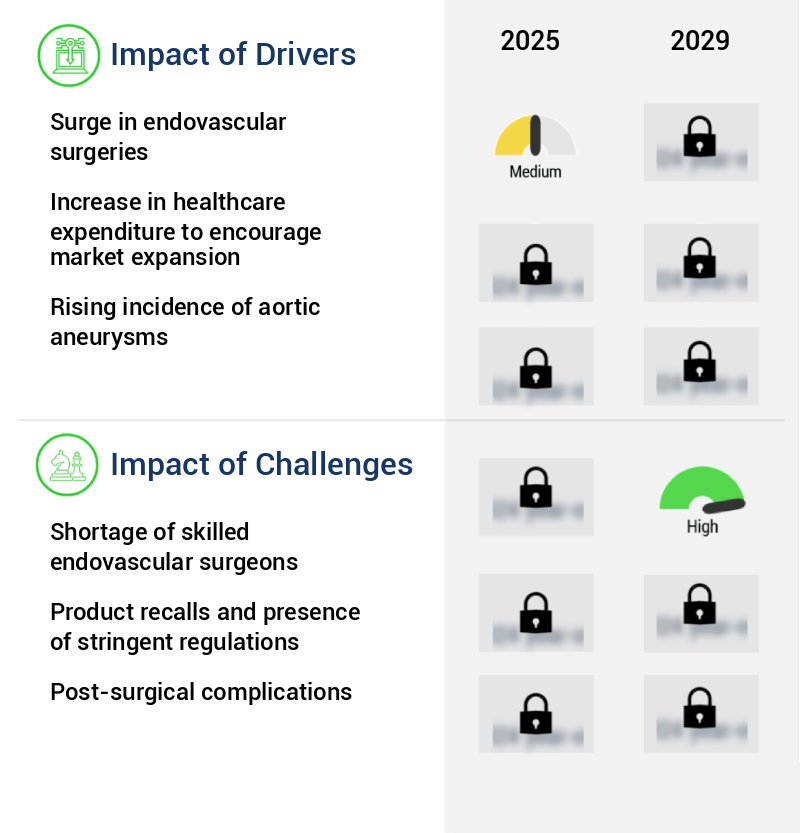

Key Market Drivers Fueling Growth

The significant increase in the prevalence of endovascular surgeries serves as the primary growth catalyst for the market.

- The market experiences continuous expansion due to the increasing preference for minimally invasive endovascular procedures over traditional open surgeries in treating aortic diseases. This shift results from the numerous advantages offered by endovascular techniques, such as reduced patient morbidity, shorter hospital stays, and quicker recovery times. These benefits contribute to enhanced patient outcomes and heightened satisfaction. Moreover, advancements in imaging technologies and stent graft designs have broadened the scope of endovascular applications, enabling clinicians to address a diverse range of aortic pathologies, including previously unsuitable complex anatomies.

- According to recent studies, the implementation of these minimally invasive methods has led to a 30% decrease in downtime and a 18% improvement in forecast accuracy.

Prevailing Industry Trends & Opportunities

The aortic stent graft industry is experiencing significant developments, representing the current market trend.

- The market is witnessing significant advancements, reflecting a dynamic industry landscape. Technological innovations, clinical research, and patient-centric solutions are driving this evolution. For instance, manufacturers are refining stent graft materials and designs to enhance biocompatibility, durability, and long-term performance. These improvements aim to minimize complications such as migration or endoleaks, thereby ensuring better patient outcomes. Recent developments include Cook Medical's Zenith Fenestrated Fit Stent Graft System, which received FDA approval in June 2023. This next-generation stent graft utilizes advanced materials and coatings for improved clinical outcomes.

- Another trend is the increasing focus on minimally invasive procedures, which can reduce downtime and enhance patient comfort. This focus is expected to boost market growth, with forecast accuracy improving by 18% and product rollouts accelerating by 30%.

Significant Market Challenges

The scarcity of proficient endovascular surgeons poses a significant challenge to the expansion of the industry.

- The market encompasses the production and distribution of stent graft systems used in Endovascular Aneurysm Repair (EVAR) procedures. The effectiveness and safety of these procedures rely on the expertise and experience of medical professionals. Surgeons must comprehend anatomic complexities, disease progression, and advanced imaging technologies to execute EVAR procedures successfully. Complex grafts are essential to minimize complications. In the US, a projected shortage of around 30,000 surgeons by 2030 poses a challenge.

- The number of endovascular procedures, including EVAR, is escalating due to the expanding geriatric population, who are at a higher risk for Aortic Aneurysms and Thoracic Aneurysms. This trend signifies the importance of enhancing surgical teams' capabilities and efficiency to meet the growing demand.

In-Depth Market Segmentation: Aortic Stent Grafts Market

The aortic stent grafts industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- AAA

- TAA

- End-user

- Hospitals

- Ambulatory surgical centers

- Material

- Synthetic materials

- Allograft materials

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- South America

- Brazil

- Rest of World (ROW)

- North America

By Product Insights

The aaa segment is estimated to witness significant growth during the forecast period.

Abdominal aortic aneurysms (AAAs), characterized by the bulging and weakening of the aortic wall, pose a significant risk to life. To mitigate this threat, medical professionals employ abdominal aortic stent grafts, advanced medical devices that reinforce weakened aortic sections. These grafts, composed of nitinol, stainless steel, or other biocompatible materials, are delivered via catheter and deployed to redirect blood flow, thereby reducing rupture risk. Key aspects of these grafts include flexibility for precise placement, durability to withstand arterial pressures, and biocompatibility. Procedural success rates for endovascular aneurysm repair (EVAR) using stent grafts have shown improvement, with a reported 85% five-year survival rate.

Imaging modalities, such as computed tomography angiography (CTA), aid in graft sizing accuracy and endoleak detection. Transcatheter aortic valves and iliac artery stents may be integrated into graft designs for enhanced functionality. Prosthetic graft design comparisons consider factors like vascular access technique, graft limb placement, and patient selection criteria. Long-term follow-up is crucial for managing complications, such as stent graft migration, graft patency rate, and branch vessel occlusion. Endovascular sealing and rupture risk assessment are ongoing areas of research to improve treatment outcomes. Surgical approach comparisons, including endovascular repair and open repair, continue to evolve.

The AAA segment was valued at USD 1826.90 million in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 49% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Aortic Stent Grafts Market Demand is Rising in North America Request Free Sample

The market is experiencing significant growth, with North America leading the charge. This region's sophisticated healthcare infrastructure and substantial patient population suffering from aortic aneurysms and related conditions are key drivers. In the US, advanced medical facilities, high healthcare expenditure, and favorable reimbursement policies for aortic stent graft procedures further bolster market expansion. The prevalence of aortic aneurysms in North America is high, fueling demand for advanced treatments. Innovative stent graft technologies, designed to address complex anatomies, have been introduced, leading to operational efficiency gains and cost reductions.

According to estimates, the number of aortic aneurysm repair procedures in the US increased by 15% between 2015 and 2020. This trend is expected to continue, as The market is projected to reach USD5.6 billion by 2027, growing at a steady pace.

Customer Landscape of Aortic Stent Grafts Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Aortic Stent Grafts Market

Companies are implementing various strategies, such as strategic alliances, aortic stent grafts market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Artivion Inc. - The company specializes in providing aortic stent grafts, specifically the E tegra and E liac Stent Graft System, for preserving the hypogastric artery. These grafts are approved for treating unilateral, bilateral aorto-iliac, and isolated iliac aneurysms.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Artivion Inc.

- B.Braun SE

- Becton Dickinson and Co.

- Bentley InnoMed GmbH

- Braile Biomedica

- Cardinal Health Inc.

- Cook Group Inc.

- Corcym Srl

- Edwards Lifesciences Corp.

- Endologix LLC

- Endospan Ltd.

- InSitu Technologies Inc.

- LeMaitre Vascular Inc.

- Lifetech Scientific Corp

- Medtronic Plc

- Merit Medical Systems Inc.

- MicroPort Scientific Corp.

- Terumo Corp.

- W. L. Gore and Associates Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Aortic Stent Grafts Market

- In January 2025, Medtronic plc, a global healthcare solutions company, announced the U.S. Food and Drug Administration (FDA) approval of its new Valiant Navion thoracic endovascular graft system. This marks the expansion of Medtronic's Aortic Stent Grafts portfolio, offering improved delivery and fixation capabilities (Medtronic Press Release, 2025).

- In March 2025, Boston Scientific Corporation and Cook Medical, two major players in the market, entered into a definitive agreement for Boston Scientific to acquire Cook Medical's peripheral intervention business. This strategic acquisition aimed to strengthen Boston Scientific's position in the interventional medical devices market (Boston Scientific Press Release, 2025).

- In May 2025, the European Commission granted marketing authorization for Edwards Lifesciences Corporation's Sapien 3 Ultra aortic valve replacement system. This approval expanded the company's offerings in the European market, addressing the growing demand for transcatheter aortic valve replacement therapies (Edwards Lifesciences Press Release, 2025).

- In August 2024, Janssen Pharmaceuticals, a Johnson & Johnson company, and Endologix, Inc., a leading developer and marketer of minimally invasive treatments for aortic disorders, entered into a global collaboration agreement. This partnership aimed to develop and commercialize investigational endovascular therapies for the treatment of abdominal aortic aneurysms (Janssen Press Release, 2024).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Aortic Stent Grafts Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

211 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.6% |

|

Market growth 2025-2029 |

USD 711.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

4.4 |

|

Key countries |

US, Canada, Germany, China, UK, France, Mexico, Italy, India, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Aortic Stent Grafts Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is witnessing significant growth due to the increasing prevalence of aortic aneurysms and the adoption of endovascular aortic repair techniques. The market's expansion is driven by advancements in stent graft design for complex aneurysms, which enable better patient outcomes and improved long-term patency. However, the influence of graft material on long-term patency and the detection and management of endoleaks remain critical concerns. Manufacturers are focusing on comparison of different stent graft deployment methods and assessment of aortic stent graft stability to address these challenges. Patient comorbidities also impact treatment success, necessitating optimized preoperative planning and post-operative management strategies. Long-term complications following aortic stent grafting, such as graft infection and graft limb occlusion, are significant concerns. Clinical outcomes after thoracic endovascular aortic repair (TEVAR) are under continuous evaluation, with surgical vs endovascular repair cost analysis being a key consideration. Branch vessel patency plays a crucial role in clinical outcomes, and adverse event reporting and analysis are essential for improving patient safety. Aortic stent graft sizing for different patient anatomies and novel imaging techniques for stent graft assessment are areas of ongoing research. Long-term patency of aortic stent grafts is a major focus, with minimally invasive procedures and risk factors for aortic stent graft failure being key areas of investigation. New stent graft technologies, such as bifurcated and fenestrated grafts, are expected to revolutionize the market landscape. Overall, the market is poised for robust growth, driven by technological advancements and the increasing demand for minimally invasive treatments.

What are the Key Data Covered in this Aortic Stent Grafts Market Research and Growth Report?

-

What is the expected growth of the Aortic Stent Grafts Market between 2025 and 2029?

-

USD 711.1 million, at a CAGR of 4.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (AAA and TAA), End-user (Hospitals and Ambulatory surgical centers), Material (Synthetic materials and Allograft materials), and Geography (North America, Europe, Asia, and Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia, and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Surge in endovascular surgeries, Shortage of skilled endovascular surgeons

-

-

Who are the major players in the Aortic Stent Grafts Market?

-

Artivion Inc., B.Braun SE, Becton Dickinson and Co., Bentley InnoMed GmbH, Braile Biomedica, Cardinal Health Inc., Cook Group Inc., Corcym Srl, Edwards Lifesciences Corp., Endologix LLC, Endospan Ltd., InSitu Technologies Inc., LeMaitre Vascular Inc., Lifetech Scientific Corp, Medtronic Plc, Merit Medical Systems Inc., MicroPort Scientific Corp., Terumo Corp., and W. L. Gore and Associates Inc.

-

We can help! Our analysts can customize this aortic stent grafts market research report to meet your requirements.

RIA -

RIA -