Transcatheter Aortic Valve Replacement Market Size 2024-2028

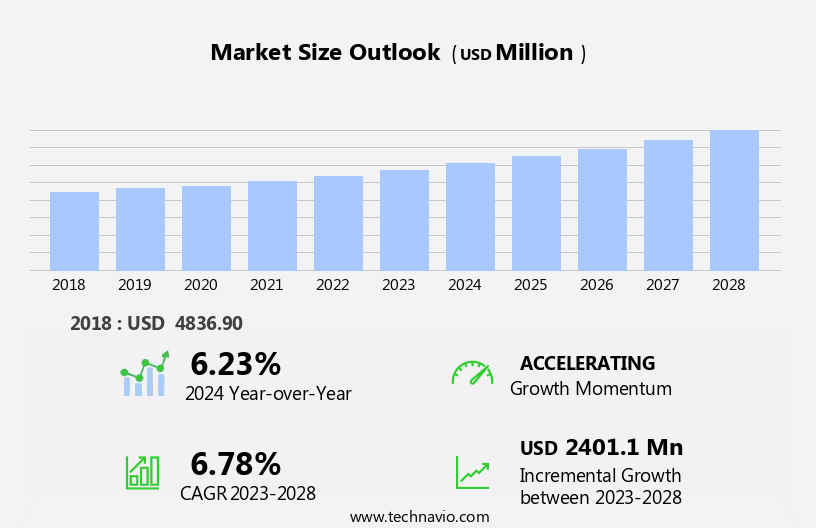

The transcatheter aortic valve replacement market size is forecast to increase by USD 2.4 billion, at a CAGR of 6.78% between 2023 and 2028.

- The Transcatheter Aortic Valve Replacement (TAVR) market is experiencing significant growth due to the expanding indications for the procedure and the increasing aging population worldwide. The aging demographic trend is driving the demand for TAVR as it offers a less invasive alternative to surgical aortic valve replacement for elderly patients, who often have other health issues that make open-heart surgery a riskier option. Diagnostic tests and blood tests are essential for determining the need for TAVR and monitoring patient outcomes. However, the high cost associated with TAVR procedures poses a significant challenge for market expansion. The expensive nature of the technology and the procedure itself can limit access to this life-saving treatment for many patients, particularly in developing countries and low-income populations.

- Despite this challenge, companies operating in the TAVR market can capitalize on the growing demand by focusing on cost reduction strategies, such as improving manufacturing efficiencies, negotiating favorable reimbursement rates, and collaborating with healthcare providers to offer bundled pricing for TAVR and related services. Additionally, expanding the indications for TAVR beyond the elderly population, such as for patients with severe aortic stenosis who are not ideal candidates for surgical valve replacement, can also help increase market penetration and revenue opportunities. Overall, the TAVR market presents a promising landscape for growth, with opportunities for companies to innovate and address the challenges of cost and access to expand their reach and capture market share.

What will be the Size of the Transcatheter Aortic Valve Replacement Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The transcatheter aortic valve replacement (TAVR) market continues to evolve, driven by advancements in technology and increasing adoption of minimally invasive procedures for the treatment of aortic valve diseases. The transfemoral approach, utilizing imaging guidance systems and valve delivery systems, has gained significant traction due to its ability to provide improved patient recovery and reduced hospital stay. However, the market dynamics are not without challenges. Annulus sizing methods and valve sizing techniques are crucial components of TAVR procedures, ensuring proper valve placement and reducing the risk of device-related complications such as paravalvular leak. Valve structural degeneration and valve thrombosis risk are ongoing concerns, necessitating continuous evaluation of valve durability assessment.

Surgical valve replacement remains an alternative for select patients, but TAVR's minimally invasive nature and procedural success rate continue to make it an attractive option. The transcarotid and endovascular approaches offer additional options for patients with complex anatomies, further expanding the market's reach. The hemodynamic assessment and percutaneous valve replacement procedures are becoming more common, with advancements in balloon-expandable and self-expanding valves, as well as refined valve deployment techniques. Post-dilation and post-procedural complications remain areas of focus for ongoing research and development. The TAVR market's continuous unfolding is shaped by these evolving patterns, with a focus on improving patient outcomes and reducing procedural risks.

The market's dynamics are shaped by advancements in technology, patient needs, and regulatory requirements, making it an exciting and dynamic space for innovation and growth.

How is this Transcatheter Aortic Valve Replacement Industry segmented?

The transcatheter aortic valve replacement industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Hospitals

- Ambulatory surgical centers

- Others

- Type

- Balloon-expanding valve

- Self expanding valve

- Geography

- North America

- US

- Europe

- France

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

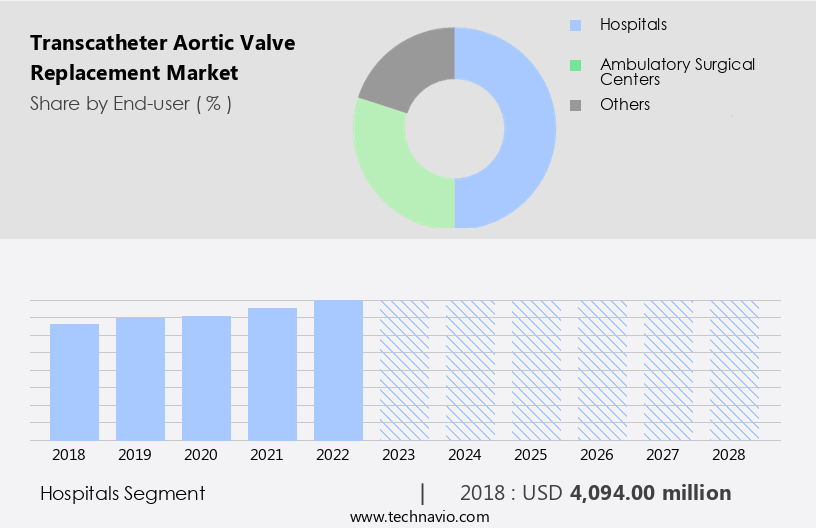

By End-user Insights

The hospitals segment is estimated to witness significant growth during the forecast period.

In the global Transcatheter Aortic Valve Replacement (TAVR) market, hospitals serve as the primary end-users for this minimally invasive cardiac procedure. Equipped with advanced infrastructure, including specialized cardiac catheterization labs and operating rooms, these healthcare facilities offer a skilled medical workforce capable of ensuring safe and effective TAVR implementation. Hospitals' comprehensive cardiac care services are vital, as they provide supporting technologies like imaging systems (echocardiography and fluoroscopy) and intensive care units, as well as experienced cardiac surgery and anesthesia teams. TAVR procedures require precise valve placement and deployment, which hospitals facilitate through their specialized facilities. These facilities enable the use of various techniques, such as transfemoral and transapical approaches, annulus sizing methods, and post-dilation techniques.

Hospitals also manage potential complications, including valve structural degeneration, valve thrombosis risk, and device-related complications, ensuring prompt hemodynamic assessment and patient survival. The TAVR market continues to evolve, with advancements in valve technologies, such as balloon-expandable and self-expanding valves, and procedural techniques, like imaging guidance systems and percutaneous valve replacement. These innovations contribute to improved patient recovery, reduced hospital stays, and long-term clinical outcomes. Despite these advancements, post-procedural complications and valve durability assessment remain essential considerations for hospitals and patients alike. Overall, the TAVR market's dynamics reflect the ongoing pursuit of minimally invasive solutions for aortic valve stenosis and the importance of hospitals in delivering these advanced cardiac care services.

The Hospitals segment was valued at USD 4.09 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

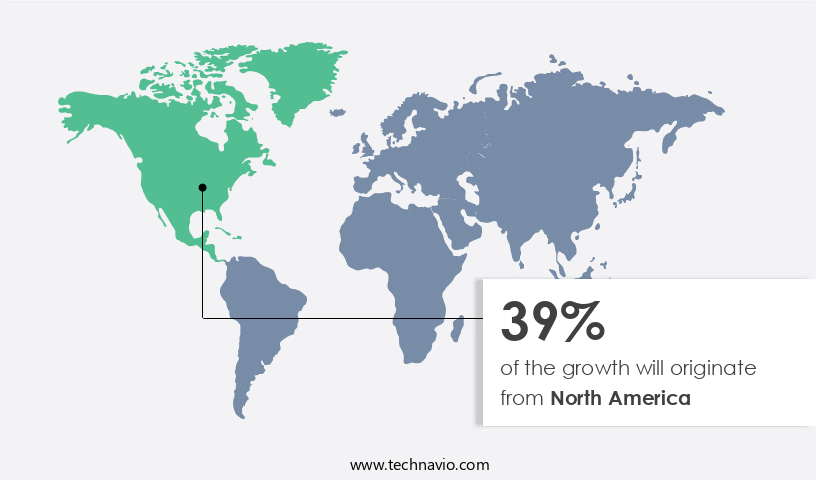

North America is estimated to contribute 39% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The Transcatheter Aortic Valve Replacement (TAVR) market in North America is experiencing notable growth due to the escalating prevalence of heart conditions, including valve diseases, stenosis, and atresia. The adoption of suture-less valves, tissue valves, and minimal invasive procedures is surging, particularly in the older adult population, who are more susceptible to heart-related issues. The US and Canada are the primary contributors to the TAVR market's expansion in North America, with the US being the largest and most influential market globally. Its advanced healthcare system and substantial aging population have significantly fueled the market's growth. The TAVR procedure involves the use of imaging guidance systems for precise valve placement, reducing the risk of device-related complications.

Valve structural degeneration and thrombosis risk are concerns, necessitating continuous valve durability assessments. The market encompasses various approaches, such as transfemoral, transapical, transcarotid, and endovascular, each with unique advantages. Percutaneous valve replacement, transcatheter valve implantation, and post-dilation techniques are integral to the procedure. The TAVR process offers improved patient recovery, hemodynamic assessment, and reduced hospital stay, making it an attractive alternative to surgical valve replacement. Long-term clinical outcomes are closely monitored to ensure optimal patient care.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Transcatheter Aortic Valve Replacement Industry?

- The global market is significantly driven by the growing aging population, representing a key demographic trend shaping various industries.

- The Transcatheter Aortic Valve Replacement (TAVR) market is experiencing significant growth due to the increasing global aging population. According to UN data, approximately 10% of the world's population, or 771 million people, were over 65 years of age in 2022. This percentage is projected to increase to 16% by 2050. The aging population's higher prevalence of aortic valve disease, particularly aortic stenosis, is driving the demand for TAVR procedures. TAVR is a minimal invasive procedure that utilizes a transfemoral approach for valve replacement. Imaging guidance systems, such as fluoroscopy, are employed to ensure precise valve placement.

- The procedure's minimally invasive nature and the use of advanced technologies, like valve delivery systems, minimize the risk of complications, such as paravalvular leak and valve thrombosis. The TAVR market's growth is also attributed to the advancements in technology, which enable the procedure to be performed in high-risk patients, such as those with severe comorbidities. These advancements have made TAVR a more viable alternative to surgical aortic valve replacement for a larger patient population. The procedure's benefits, including shorter hospital stays, quicker recovery times, and reduced risk of complications, make it an attractive option for both patients and healthcare providers.

What are the market trends shaping the Transcatheter Aortic Valve Replacement Industry?

- The expanding indications for Transcatheter Aortic Valve Replacement (TAVR) procedures represent a significant market trend in the cardiology industry. This growth is driven by advancements in technology and clinical research, enabling TAVR to be considered a viable option for an increasing number of patients with aortic valve disease.

- The Transcatheter Aortic Valve Replacement (TAVR) market is experiencing significant growth due to the expanding indications for the procedure. Initially, TAVR was limited to high-risk or inoperable patients with severe aortic stenosis. However, recent clinical evidence and technological advancements have led to a shift in eligibility criteria. The safety and efficacy of TAVR are demonstrated through numerous clinical trials and real-world studies. These studies show positive outcomes, including reduced mortality, symptom improvement, and improved quality of life for patients. The annulus sizing method and valve sizing technique have evolved, enabling better fit and reducing device-related complications. Two common approaches for TAVR are the transcarotid and endovascular methods.

- Both methods offer advantages and are chosen based on individual patient needs. The procedural success rate for TAVR is high, making it an increasingly popular alternative to surgical valve replacement. Despite the advancements, there are challenges, such as procedural complexities and ongoing research to optimize outcomes. The focus remains on improving patient selection, reducing complications, and enhancing procedural success. The TAVR market is poised for continued growth as it transforms the landscape of interventional cardiology.

What challenges does the Transcatheter Aortic Valve Replacement Industry face during its growth?

- The high cost of Transcatheter Aortic Valve Replacement (TAVR) procedures represents a significant challenge to the industry's growth trajectory. This financial hurdle, which is a common theme in the medical device sector, necessitates ongoing efforts to contain costs and improve efficiency in TAVR procedures.

- The transcatheter aortic valve replacement (TAVR) market holds promise for addressing aortic valve stenosis, a debilitating cardiovascular condition. TAVR offers several advantages over traditional surgical aortic valve replacement (SAVR), such as improved patient recovery and reduced hospital stays. However, the high cost of TAVR procedures poses a significant challenge to market growth. In the US, the cost of a TAVR procedure ranges from USD 30,000 to USD 70,000 or more, influenced by factors like the chosen TAVR valve brand, hospital location, and patient health. This financial burden, even with insurance coverage, can deter many patients from undergoing the procedure. The primary cost driver for TAVR is the expense of the devices themselves.

- Despite these challenges, the market continues to evolve with advancements in technology, such as balloon-expandable valves and transapical and transcatheter valve implantation approaches. Hemodynamic assessment plays a crucial role in determining the most suitable valve replacement method for individual patients, ensuring optimal outcomes.

Exclusive Customer Landscape

The transcatheter aortic valve replacement market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the transcatheter aortic valve replacement market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, transcatheter aortic valve replacement market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

4C Medical Technologies Inc. - The company introduces Navitor, a transcatheter aortic valve replacement solution for addressing aortic stenosis, expanding the market for minimally invasive heart valve treatments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 4C Medical Technologies Inc.

- Abbott Laboratories

- Anteris Technologies Ltd.

- Artivion Inc.

- Biosensors International Group Ltd.

- Boston Scientific Corp.

- Colibri Heart Valve LLC

- Edwards Lifesciences Corp.

- Genesis Medtech International Pvt. Ltd.

- HighLife SAS

- JenaValve Technology Inc.

- LifeNet Health Inc.

- LivaNova PLC

- Medinol Ltd.

- Medtronic Plc

- Meril Life Sciences Pvt. Ltd.

- MicroPort Scientific Corp.

- Shockwave Medical Inc.

- Siemens AG

- Venus Medtech Hangzhou Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Transcatheter Aortic Valve Replacement Market

- In January 2024, Medtronic plc, a leading medical technology company, announced the US Food and Drug Administration (FDA) approval of its Evolut PRO+ Transcatheter Aortic Valve Replacement (TAVR) system. This approval expanded the indications for the Evolut R and Evolut PRO systems, making them suitable for a broader range of patients (Medtronic Press Release, 2024).

- In March 2024, Edwards Lifesciences Corporation, another major player in the TAVR market, entered into a strategic partnership with the University of California, San Francisco (UCSF) Health to establish a TAVR Center of Excellence. This collaboration aimed to advance research and clinical expertise in TAVR procedures (Edwards Lifesciences Press Release, 2024).

- In May 2024, Abbott Laboratories completed the acquisition of St. Jude Medical, a leading medical device manufacturer. This acquisition expanded Abbott's offerings in the cardiovascular space, including the addition of St. Jude Medical's Portico and Intrepid TAVR systems (Abbott Laboratories Press Release, 2024).

- In April 2025, Boston Scientific Corporation received CE Mark approval for its Lotus Edge Transcatheter Aortic Valve. This approval marked the first TAVR system with a trileaflet design, offering improved durability and performance compared to earlier generation TAVRs (Boston Scientific Press Release, 2025).

Research Analyst Overview

- The Transcatheter Aortic Valve Replacement (TAVR) market is experiencing significant advancements, driven by innovations in pre-operative assessment and valve design. Pre-operative assessment, including valve stability assessment and patient selection criteria, is crucial for optimal device compatibility and reducing procedural complications rate. Multislice CT angiography and transesophageal echocardiogram are essential imaging modalities for accurate valve area measurement and peri-procedural complications evaluation. Valve anticoagulation therapy and bioprosthetic valve material are critical factors influencing implant durability testing and risk stratification model development. Device compatibility issues, such as valve leaflet thickness and contrast echocardiography, are continually addressed through advancements in endovascular imaging technology.

- Mechanical valve durability and long-term echocardiography (ECG) evaluations are essential for assessing valve performance and patient outcomes. Magnetic resonance imaging and computed tomography imaging provide valuable insights into aortic valve calcification and valve performance evaluation, contributing to the overall success of the TAVR market. Ongoing research and development efforts focus on addressing procedural complications, improving patient selection protocols, and enhancing valve design to meet the evolving needs of the patient population.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Transcatheter Aortic Valve Replacement Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

172 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.78% |

|

Market growth 2024-2028 |

USD 2401.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.23 |

|

Key countries |

US, UK, Germany, China, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Transcatheter Aortic Valve Replacement Market Research and Growth Report?

- CAGR of the Transcatheter Aortic Valve Replacement industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the transcatheter aortic valve replacement market growth of industry companies

We can help! Our analysts can customize this transcatheter aortic valve replacement market research report to meet your requirements.

RIA -

RIA -