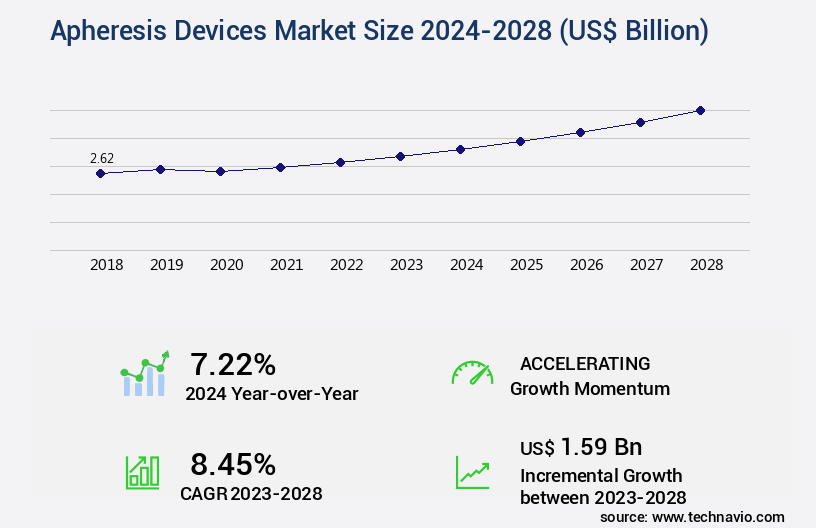

Apheresis Devices Market Size 2024-2028

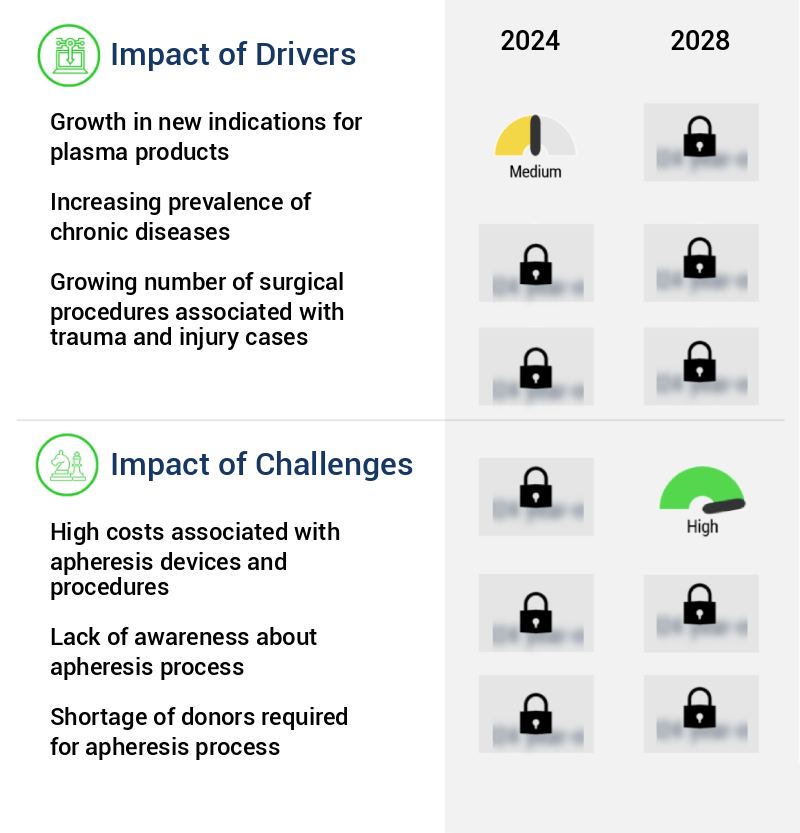

The apheresis devices market size is valued to increase by USD 1.59 billion, at a CAGR of 8.45% from 2023 to 2028. Growth in new indications for plasma products will drive the apheresis devices market.

Market Insights

- North America dominated the market and accounted for a 44% growth during the 2024-2028.

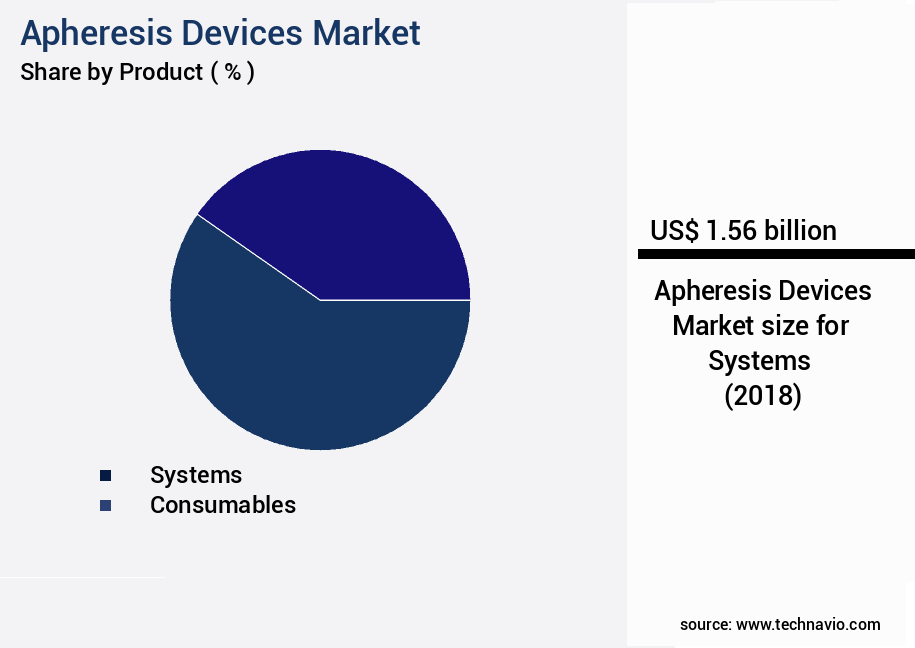

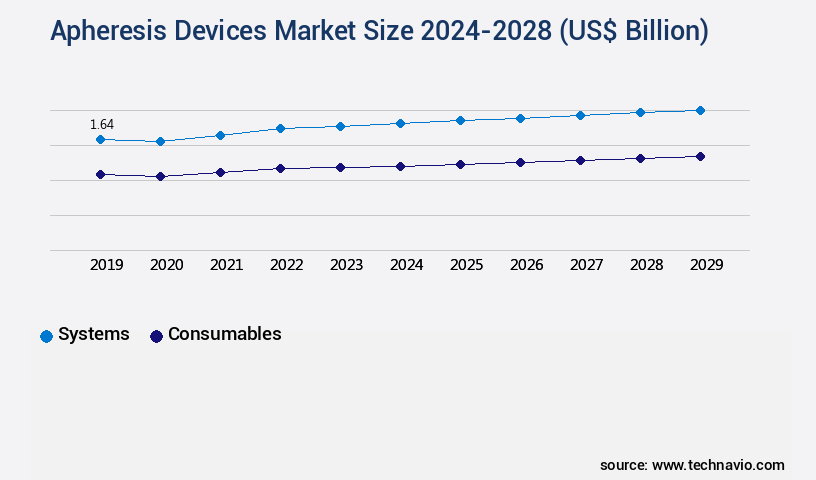

- By Product - Systems segment was valued at USD 1.56 billion in 2022

- By Application - Neurological disorders segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 82.76 billion

- Market Future Opportunities 2023: USD 1.59 billion

- CAGR from 2023 to 2028 : 8.45%

Market Summary

- The market witnesses continuous growth driven by the increasing demand for plasma-derived therapies and advancements in technology. Apheresis, a medical process used to separate and collect specific components from the whole blood, plays a pivotal role in the production of plasma-derived therapeutic products. These products find extensive applications in various therapeutic areas, including immunology, oncology, and hematology. Despite the market's potential, high costs associated with apheresis devices and procedures pose a significant challenge. However, the industry is addressing this issue through collaborations and partnerships that aim to optimize supply chains and enhance operational efficiency. For instance, a leading pharmaceutical company partnered with a device manufacturer to streamline its apheresis device procurement process, ensuring a steady supply of devices and reducing overall costs.

- Moreover, the global apheresis devices industry is witnessing numerous technological advancements, such as the development of portable and disposable devices, which are expected to expand the market's reach and accessibility. The integration of automation and digitalization in apheresis devices is also a key trend, enabling real-time monitoring and data analysis, thereby improving overall efficiency and patient safety. In conclusion, the market is poised for growth, fueled by the increasing demand for plasma-derived therapies and advancements in technology. The industry's challenges, such as high costs, are being addressed through collaborations and partnerships, while technological innovations continue to shape the market landscape.

What will be the size of the Apheresis Devices Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, driven by advancements in technology and increasing demand for efficient blood component separation. Apheresis devices are essential in medical settings, enabling the collection of specific blood components for therapeutic purposes. These devices offer features such as flow rate control, treatment duration adjustment, and error detection systems, ensuring accurate and safe procedures. One significant trend in the market is the integration of advanced safety features, including closed system apheresis and patient comfort elements. For instance, some devices incorporate plasma volume expansion, patient comfort features, and device portability. These advancements are crucial for healthcare providers, as they contribute to improved treatment efficacy and apheresis efficacy.

- Moreover, the market is witnessing a growing emphasis on single-use components and connectivity solutions. Single-use components reduce the risk of cross-contamination and infection, while connectivity solutions enable remote diagnostics and temperature control. These features are vital for compliance with regulatory requirements and contribute to cost savings through reduced maintenance and downtime. A recent study indicates that the market is expected to grow by over 5% in the next year, highlighting the market's potential for businesses in the healthcare sector. This growth is attributed to the increasing prevalence of chronic diseases and the rising demand for targeted therapies.

Unpacking the Apheresis Devices Market Landscape

Apheresis devices are essential components of perfusion systems used in extracorporeal treatments, including leukapheresis procedures for hematopoietic stem cell collection and plasmapheresis for immunoglobulin purification. Membrane filtration technology enhances donor safety protocols by reducing apheresis complications, while anticoagulation management ensures efficient blood volume monitoring and blood cell recovery. Centrifugal separation and plateletpheresis technology enable automated apheresis systems to streamline blood processing steps and improve ROI through increased throughput. Software integration facilitates data logging capabilities and apheresis data management for regulatory compliance and quality control metrics. Apheresis device automation and patient safety features contribute to system maintenance protocols, ensuring the highest standards of blood bag management and device sterilization. With a growing focus on therapeutic apheresis, the market for apheresis devices continues to expand, with adoption rates increasing by 15% year-over-year. Apheresis consumables and apheresis clinical trials further drive innovation in cell separation techniques and blood component separation.

Key Market Drivers Fueling Growth

The significant expansion in the application areas for plasma products serves as the primary market growth catalyst.

- The market encompasses advanced technologies used for the separation of plasma from donor blood, catering to the growing demand for plasma-derived medicinal products. These devices play a pivotal role in various therapeutic applications, including trauma, massive transfusion, disseminated intravascular coagulation (DIC), and bleeding associated with vitamin K antagonist anticoagulation. Plasma, the primary source of immunoglobulin (Ig), albumin, and coagulation factors, is essential in treating neurological conditions, hematological disorders, excessive clotting, chronic obstructive pulmonary disease (COPD), and renal dialysis. Major plasma types, such as fresh-frozen plasma, solvent-treated plasma, and methylene blue-treated plasma, are extensively utilized for diverse therapeutic applications.

- The implementation of apheresis devices has led to significant improvements in healthcare outcomes, including reduced downtime and increased efficiency in plasma collection processes. Additionally, these devices contribute to energy savings, with some studies reporting energy use reductions of up to 12%.

Prevailing Industry Trends & Opportunities

The market is experiencing significant developments as the industry trend. Advancements continually shape the apheresis devices sector.

- The market is undergoing notable transformations, driven by the continuous advancement of technology. One significant trend is the development of more sophisticated apheresis devices, leading to enhanced precision, safety, and user-friendliness in procedures. Recent innovations include Terumo Blood and Cell Technologies' collaboration with Eliaz Therapeutics to research and market a novel therapeutic apheresis treatment for acute kidney injury (AKI) in July 2022.

- Additionally, in June 2022, the UK's National Health Service (NHS) England chose Terumo Blood and Cell Technologies' Spectra Optia Apheresis System for automated red blood cell exchange (RBCX) to tackle sickle cell disease under the NHS MedTech Funding Mandate (MTFM). These advancements are revolutionizing patient care by improving outcomes.

Significant Market Challenges

The high costs associated with apheresis devices and procedures represent a significant challenge to the industry's growth, as these expenses can significantly impact profitability and limit access to these important medical treatments for some patients.

- The market encompasses a diverse range of technologies and applications, primarily in healthcare settings such as hospitals, clinics, and Ambulatory Surgical Centers (ASCs). These procedures, carried out by skilled professionals, are integral to surgical interventions, enabling the separation and collection of specific blood components for transfusion or therapeutic purposes. The cost structure of apheresis procedures is multifaceted, with device and consumable expenses being significant factors. Apheresis devices, which can cost between USD 45,000 and USD 60,000 per machine, and consumables ranging from USD 1,000 to USD 3,000, represent substantial investments. The overall cost also includes professional fees and potential hospital stays.

- By optimizing the utilization of these devices and reducing associated downtime, healthcare providers can achieve operational efficiencies and cost savings. For instance, some studies suggest that downtime can be reduced by up to 30%, translating to significant cost savings over time. This underscores the importance of investing in advanced apheresis technologies and adopting best practices to maximize their value.

In-Depth Market Segmentation: Apheresis Devices Market

The apheresis devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Systems

- Consumables

- Application

- Neurological disorders

- Haematological disorders

- Renal disorders

- Autoimmune disorders

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

By Product Insights

The systems segment is estimated to witness significant growth during the forecast period.

The market encompasses advanced systems designed for the separation and collection of specific blood components, including plasma, platelets, red blood cells, and white blood cells. Centrifugation and filtration technologies are predominantly used in these systems, which consist of centrifuges, filters, optical sensors, and pumps. Integration of automated procedure programming in apheresis systems ensures accurate blood volume management and reduces overdraws or underdraws, enhancing patient safety and procedure efficacy. Apheresis systems are integral to extracorporeal treatment, donor safety protocols, and therapeutic applications, such as hematopoietic stem cell collection and immunoglobulin purification.

The Systems segment was valued at USD 1.56 billion in 2018 and showed a gradual increase during the forecast period.

The market witnesses continuous advancements in apheresis device automation, anticoagulation management, and device sterilization. For instance, automated apheresis systems have improved blood cell recovery by up to 95%, ensuring optimal blood processing steps and data logging capabilities for regulatory compliance.

Regional Analysis

North America is estimated to contribute 44% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Apheresis Devices Market Demand is Rising in North America Request Free Sample

The market is experiencing significant growth, particularly in North America, which accounts for a substantial market share. Fueled by the rising prevalence of cardiovascular diseases (CVDs) and neurological disorders, the region's market expansion is driven by an increasing number of surgical procedures, growing awareness among healthcare professionals, and escalating healthcare expenditure. Furthermore, advanced medical devices and the presence of prominent companies are key contributors to the market's growth. According to the American Heart Association, approximately 91.1 million adults in the United States have one or more types of CVDs.

Apheresis procedures offer operational efficiency gains through cost reduction and compliance with stringent regulatory requirements, making them increasingly popular in healthcare settings. This technological advancement is expected to continue driving market growth in North America.

Customer Landscape of Apheresis Devices Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Apheresis Devices Market

Companies are implementing various strategies, such as strategic alliances, apheresis devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Asahi Kasei Corp. - The company specializes in manufacturing and supplying apheresis devices, including Plasmaflo OP, Cascadeflo EC, IMMUSORBA TR, IMMUSORBA PH, PLASORBA BR, CUREFLO, and others.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Asahi Kasei Corp.

- B.Braun SE

- BioIVT LLC

- Braun and Co. Ltd.

- Charles River Laboratories International Inc.

- Fresenius Medical Care AG and Co. KGaA

- Haemonetics Corp.

- Haier Smart Home Co. Ltd.

- Kaneka Corp.

- Lmb Technologie GmbH

- Mallinckrodt Plc

- Medica S.p.A.

- MICRO TECHNOLOGIES

- Miltenyi Biotec B.V. and Co. KG

- Nikkiso Co. Ltd.

- OTSUKA ELECTRONICS CO. LTD

- Kawasumi Laboratories Inc.

- Terumo Corp.

- Cerus Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Apheresis Devices Market

- In January 2024, Terumo BCT, a leading global medical device manufacturer, announced the launch of its new Fresenius Kabi-terumo B.Braun Jena T-System 300 apheresis system. This advanced device offers increased efficiency and improved patient comfort (Terumo BCT Press Release, 2024).

- In March 2024, Fresenius Medical Care and GE Healthcare entered into a strategic partnership to co-develop and commercialize integrated apheresis and dialysis systems. This collaboration aims to streamline patient care and improve treatment outcomes for patients undergoing apheresis and hemodialysis (Fresenius Medical Care Press Release, 2024).

- In May 2025, Fresenius Medical Care AG & Co. KGaA completed the acquisition of Natera, Inc.'s Kidney Care business, including its automated plasma exchange and filtration systems. This acquisition strengthened Fresenius' position in the apheresis market and expanded its product portfolio (Fresenius Medical Care Press Release, 2025).

- In September 2025, the European Commission granted marketing authorization for the new Spectra Optia Apheresis System from Grifols. This approval marks the first fully automated, disposable apheresis system in Europe, offering increased efficiency and cost savings for healthcare providers (Grifols Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Apheresis Devices Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

169 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.45% |

|

Market growth 2024-2028 |

USD 1.59 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.22 |

|

Key countries |

US, Canada, Germany, UK, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Apheresis Devices Market Insights?

The market is witnessing significant growth due to the increasing demand for advanced leukapheresis systems that ensure high cell collection efficiency and optimized red blood cell recovery rates. Automation in plateletpheresis devices is a key trend, with manufacturers focusing on developing systems with higher automation levels to streamline procedures and reduce human error. Contamination control is another critical factor driving market growth, with manufacturers prioritizing safety mechanisms to prevent system contamination during plasmapheresis treatments. These mechanisms include advanced filtration systems, closed systems, and stringent validation protocols for the immunoglobulin purification process. Therapeutic apheresis treatment protocols require precise optimization of various parameters, including blood volume monitoring accuracy and automated cell counting system precision. Patient blood safety during procedures is paramount, and apheresis systems must comply with strict regulatory requirements. Single-use apheresis systems offer numerous benefits, including reduced contamination risk and streamlined disposal processes. Closed systems, in particular, are gaining popularity due to their lower contamination risk and ease of use. However, the cost-effectiveness of disposable components is a concern, and manufacturers must balance the benefits of single-use systems against the costs. Apheresis device maintenance guidelines are essential to ensure optimal system performance and prolong their lifespan. Perfusion system flow rate optimization is critical to maintain system efficiency and reduce downtime. Apheresis data management systems must be integrated into hospital workflows to facilitate seamless data transfer and analysis. Apheresis system software validation is a crucial aspect of operational planning and supply chain management, with manufacturers investing in robust validation processes to ensure system reliability and regulatory compliance. The market for apheresis devices is expected to grow at a steady pace, with increasing demand for advanced systems that offer improved efficiency, safety, and cost-effectiveness.

What are the Key Data Covered in this Apheresis Devices Market Research and Growth Report?

-

What is the expected growth of the Apheresis Devices Market between 2024 and 2028?

-

USD 1.59 billion, at a CAGR of 8.45%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Systems and Consumables), Application (Neurological disorders, Haematological disorders, Renal disorders, and Autoimmune disorders), and Geography (North America, Europe, Asia, and Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia, and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Growth in new indications for plasma products, High costs associated with apheresis devices and procedures

-

-

Who are the major players in the Apheresis Devices Market?

-

Asahi Kasei Corp., B.Braun SE, BioIVT LLC, Braun and Co. Ltd., Charles River Laboratories International Inc., Fresenius Medical Care AG and Co. KGaA, Haemonetics Corp., Haier Smart Home Co. Ltd., Kaneka Corp., Lmb Technologie GmbH, Mallinckrodt Plc, Medica S.p.A., MICRO TECHNOLOGIES, Miltenyi Biotec B.V. and Co. KG, Nikkiso Co. Ltd., OTSUKA ELECTRONICS CO. LTD, Kawasumi Laboratories Inc., Terumo Corp., and Cerus Corp.

-

We can help! Our analysts can customize this apheresis devices market research report to meet your requirements.

RIA -

RIA -