Apparel Logistics Market Size 2026-2030

The apparel logistics market size is valued to increase by USD 52.35 billion, at a CAGR of 7.1% from 2025 to 2030. Fast replenishment cycle in apparel industry will drive the apparel logistics market.

Major Market Trends & Insights

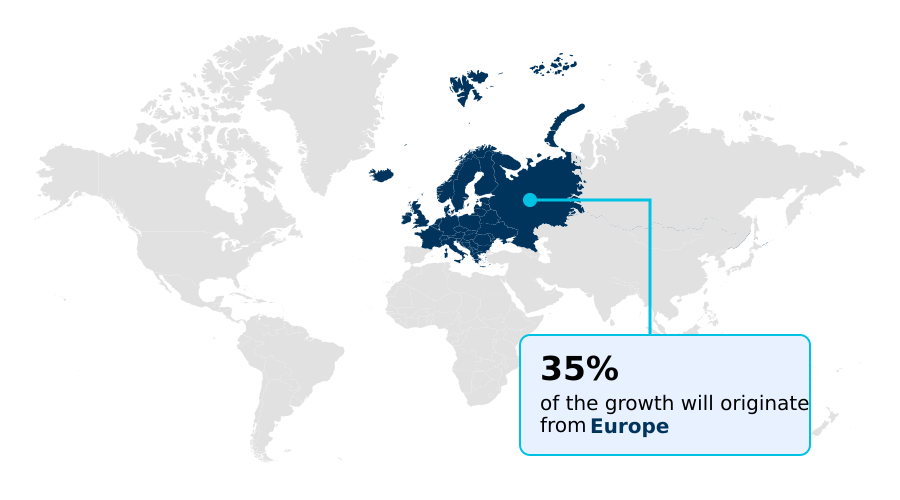

- Europe dominated the market and accounted for a 35.3% growth during the forecast period.

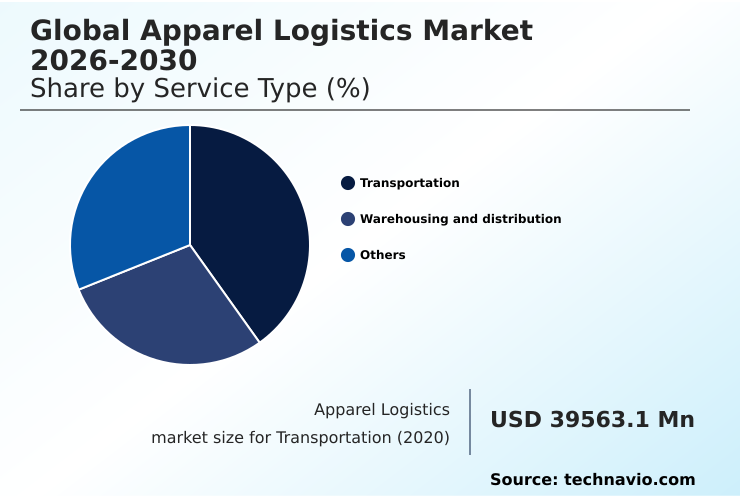

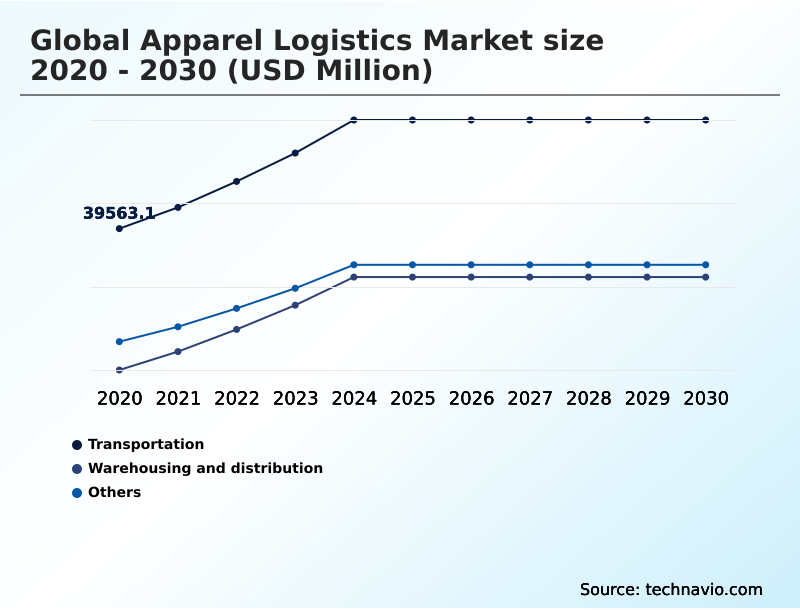

- By Service Type - Transportation segment was valued at USD 48.15 billion in 2024

- By Product - Pre-production segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 82.23 billion

- Market Future Opportunities: USD 52.35 billion

- CAGR from 2025 to 2030 : 7.1%

Market Summary

- The apparel logistics market is undergoing a significant transformation, driven by the dual pressures of fast fashion and the rise of e-commerce. Success in this environment depends on achieving a delicate balance between speed, cost, and sustainability.

- Key drivers include the adoption of omnichannel retailing, which demands a seamless integration of physical and digital sales channels, and the relentless pace of the fast fashion supply chain, requiring rapid inventory turnover.

- In response, logistics providers are investing heavily in distribution center automation and advanced warehouse management platforms to handle high volumes of stock keeping units (SKU) and complex order fulfillment.

- For instance, a global fashion brand must orchestrate a complex network to manage its e-commerce fulfillment, including efficient returns processing for online purchases, which can account for a significant portion of sales. This necessitates sophisticated reverse logistics capabilities. However, the industry faces challenges from supply chain complexity and volatile operational costs.

- The strategic implementation of technologies that improve supply chain visibility and enable agile responses to demand forecasting is no longer a competitive advantage but a fundamental requirement for survival and growth in a highly dynamic market.

What will be the Size of the Apparel Logistics Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Apparel Logistics Market Segmented?

The apparel logistics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Service type

- Transportation

- Warehousing and distribution

- Others

- Product

- Pre-production

- Trade logistics

- Mode of transportation

- Road

- Air

- Rail

- Water

- Geography

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Japan

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- Europe

By Service Type Insights

The transportation segment is estimated to witness significant growth during the forecast period.

The transportation segment is evolving beyond simple freight movement to offer sophisticated, value-driven services. Providers are delivering high schedule reliability through integrated networks, a crucial factor for brands managing tight production timelines and high inventory turnover.

For luxury goods logistics, specialized handling like garment-on-hanger (GOH) transport is standard, while sea-air combined transport offers a balanced solution for speed and cost. A key differentiator is the ability to manage a high diversity of stock keeping units (SKU).

The push toward sustainability is promoting green logistics solutions and the adoption of a digital product passport to meet regulatory demands. This ensures end-to-end supply chain visibility and supports a more resilient fulfillment operation.

The Transportation segment was valued at USD 48.15 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 35.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Apparel Logistics Market Demand is Rising in Europe Get Free Sample

The geographic landscape of apparel logistics is being reshaped by strategic shifts in sourcing and distribution.

In North America, the trend of nearshoring logistics is gaining momentum, with many brands moving production to Mexico to achieve significant lead time reduction and enhance supply chain responsiveness, supported by bonded warehousing and efficient cross-docking facilities.

Europe, which accounts for 35.3% of the incremental growth, is pioneering the sustainable supply chain through stringent regulations and investment in multimodal transportation. Here, logistics network optimization focuses on balancing efficiency with a lower carbon footprint.

Meanwhile, APAC, contributing 29.93% to growth, is transitioning from a pure manufacturing hub to a major consumption market, requiring sophisticated omnichannel distribution networks.

This global reconfiguration requires logistics providers to adapt from traditional full truckload (FTL) models to more agile, regionally-focused strategies.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the apparel logistics market is being defined by a strategic focus on operational excellence and technological adoption. The imperative for improving last-mile delivery speed is driving investment in advanced routing systems and urban distribution hubs.

- Simultaneously, automation in apparel warehousing is becoming standard practice for managing fast fashion inventory and handling high SKU complexity, which is essential for successful omnichannel fulfillment strategies. A key area of focus is optimizing apparel reverse logistics, as efficient returns management is critical for profitability.

- Reducing apparel logistics costs remains a constant battle, with the impact of fuel price volatility forcing a re-evaluation of transport modes, including a closer look at LTL vs FTL for fashion shipments and the benefits of sea-air transport for apparel.

- The successful implementation of RFID for inventory accuracy is directly linked to improving apparel supply chain visibility, a cornerstone of modern logistics. For high-end brands, specialized strategies for logistics for luxury fashion are crucial. As manufacturing diversifies, the nearshoring impact on logistics is significant, with some companies more than halving their lead times.

- The effective use of technology in apparel logistics, especially in warehouse management for e-commerce, and understanding the role of 3PL in apparel are vital. These efforts are complicated by cross-border apparel logistics challenges and the need for a sustainable apparel supply chain, particularly in apparel logistics in emerging markets.

What are the key market drivers leading to the rise in the adoption of Apparel Logistics Industry?

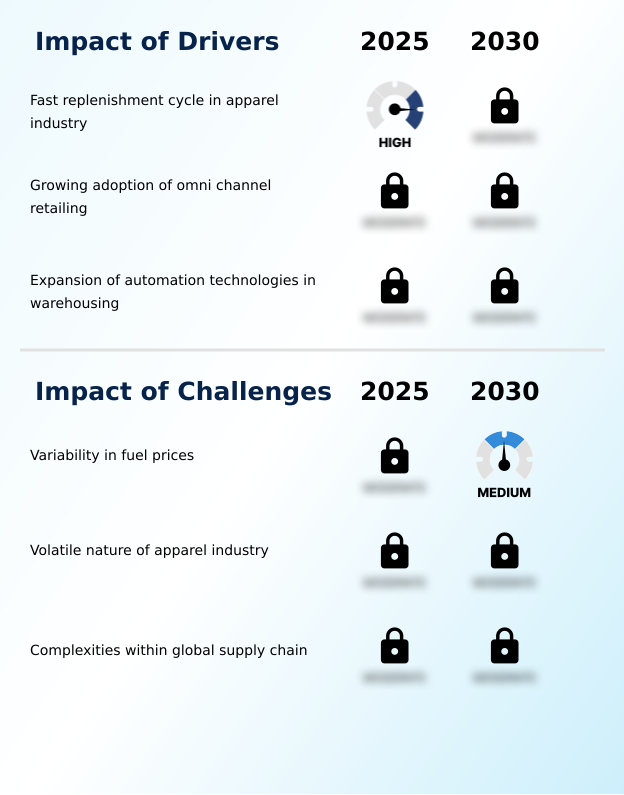

- The fast replenishment cycle in the apparel industry, driven by evolving fashion trends and consumer demand for speed, is a key driver for market growth.

- The primary driver of the apparel logistics market is the need to support the high velocity of the fast fashion supply chain and the complexities of omnichannel retailing.

- To meet consumer expectations for rapid delivery, companies are deploying networks of micro-fulfillment centers and leveraging digital freight matching platforms to optimize last-mile delivery.

- Sophisticated warehouse management platforms are essential for orchestrating e-commerce fulfillment, where effective demand forecasting can improve inventory placement and reduce stockouts.

- This focus on distribution center automation is not just about speed; strategies that enhance the omnichannel experience have been shown to boost customer loyalty by more than 15%.

- These drivers are pushing logistics toward a more responsive and data-driven operational model.

What are the market trends shaping the Apparel Logistics Industry?

- The growing adoption of RFID technology within the apparel industry is a significant market trend, enabling enhanced inventory visibility and operational efficiency across the supply chain.

- The apparel logistics market is increasingly shaped by technological advancements that enhance visibility and efficiency. The adoption of item-level RFID is a pivotal trend, enabling near-perfect inventory accuracy and providing the granular data needed for robust supply chain traceability. This technology, coupled with real-time tracking systems, provides a foundation for sophisticated returns processing, a critical component of circular economy logistics.

- As e-commerce continues to drive smaller, more frequent orders, the industry is seeing greater reliance on less-than-truckload (LTL) services and significant last-mile innovation. Furthermore, logistics providers are investing in automated sorting systems to manage the high volume of returns and prepare items for resale, which has been shown to accelerate the process by over 40%.

What challenges does the Apparel Logistics Industry face during its growth?

- The variability in fuel prices presents a key challenge to the apparel logistics market, directly impacting transportation costs and overall profitability.

- Navigating the apparel logistics market involves managing significant supply chain complexity and external risks. Volatility in operational expenses remains a primary concern, where effective logistics cost management is critical to preserving margins. Building supply chain resilience requires a robust transportation network with high schedule reliability to mitigate disruptions.

- In certain regions, ensuring shipment integrity necessitates secure convoy protocols and specialized freight forwarding expertise. Cross-border movements add another layer of difficulty, with customs brokerage becoming a key strategic function. Furthermore, the industry is under pressure for carbon footprint reduction, which can conflict with the demand for speed.

- Fuel costs, for instance, can account for over 25% of transport expenses, creating significant financial uncertainty for providers.

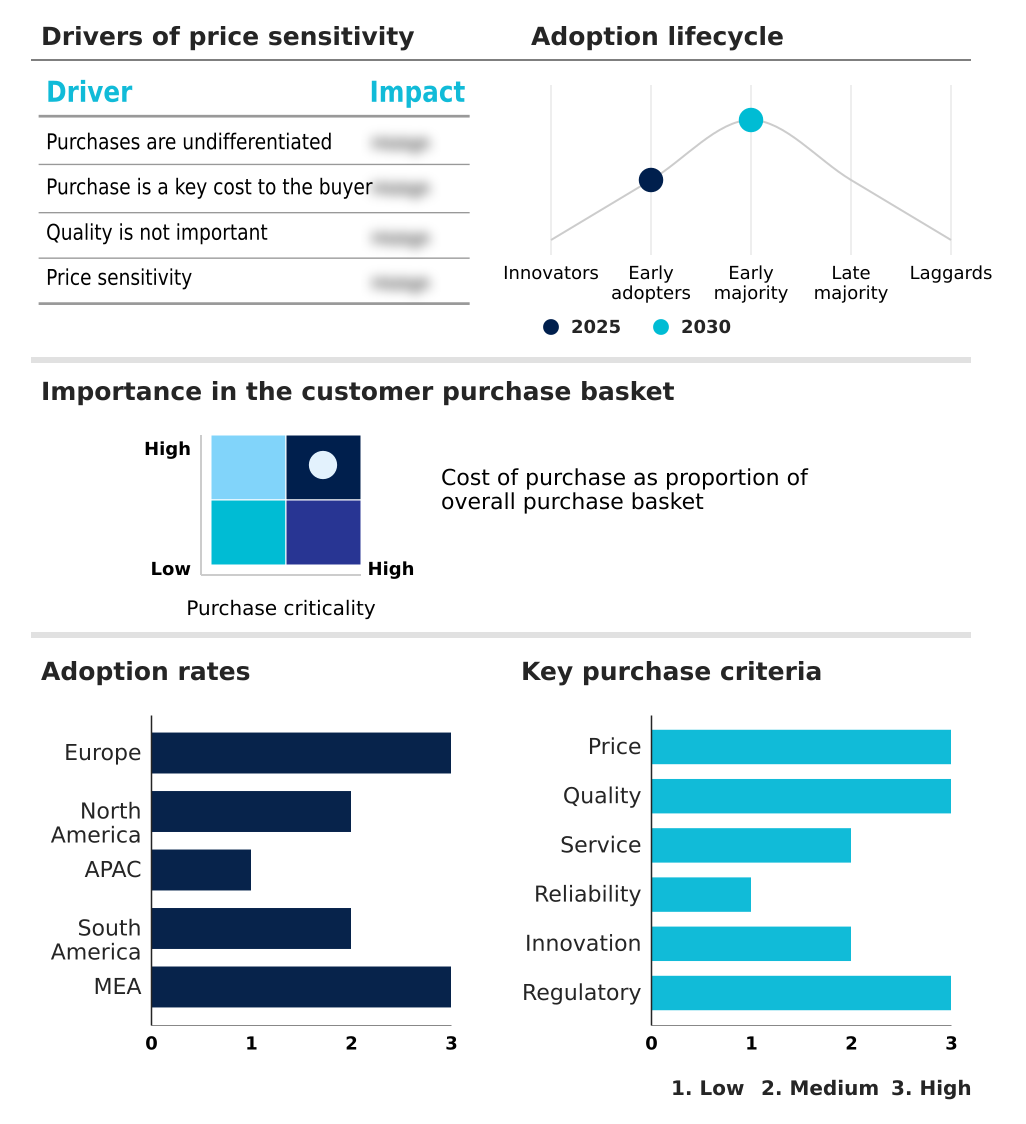

Exclusive Technavio Analysis on Customer Landscape

The apparel logistics market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the apparel logistics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Apparel Logistics Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, apparel logistics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Agility Public Warehousing Co. - Provides international-standard apparel logistics and warehousing solutions through global logistics parks, catering to multinational corporations, local markets, and small businesses.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agility Public Warehousing Co.

- Apparel Logistic Group Inc.

- Bollore SE

- CMA CGM Group

- Delhivery Ltd.

- Deutsche Bahn AG

- DSV AS

- Expeditors International

- Gulf Agency Co. Ltd.

- Hellmann Worldwide Logistics

- Kintetsu Group Holdings Ltd.

- Kuehne Nagel Management AG

- Logwin AG

- NFI Industries Inc.

- Nippon Express Holdings Inc.

- PVS Fulfillment GmbH

- Shipbob Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Apparel logistics market

- In February 2025, GXO Logistics expanded its partnership with sportswear brand Castore, taking over warehousing and transportation services across the UK, the US, and Europe to support the brand's global growth.

- In February 2025, the Gemini Cooperation, a strategic alliance between Maersk and Hapag-Lloyd, commenced operations, introducing a hub-and-spoke network designed to achieve over 90% schedule reliability for ocean freight.

- In April 2025, DSV AS completed its acquisition of DB Schenker from Deutsche Bahn AG, creating a logistics giant with expanded capabilities in global air and sea freight for apparel clients.

- In April 2025, the European Commission adopted the ESPR Working Plan, which establishes strict sustainability and digital traceability requirements for textiles, mandating digital product passports for goods entering the EU.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Apparel Logistics Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 289 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.1% |

| Market growth 2026-2030 | USD 52348.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.7% |

| Key countries | Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, China, India, Japan, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The apparel logistics market is defined by its intricate operational demands, compelling providers to master both freight forwarding and customs brokerage to navigate global trade. A primary boardroom focus is the shift towards a sustainable supply chain, where the implementation of a digital product passport and green logistics solutions are becoming key investment criteria.

- This is driven by both regulatory pressure and consumer demand. The rise of omnichannel retailing has made last-mile delivery and e-commerce fulfillment critical, with strategies like micro-fulfillment centers and digital freight matching optimizing urban distribution. Concurrently, supply chain visibility enabled by item-level RFID and real-time tracking is essential for managing the high volume of SKUs.

- The industry grapples with a high rate of returns exceeding 30%, making efficient reverse logistics and circular economy logistics vital for profitability. Providers are leveraging automated sorting systems and advanced warehouse management platforms to handle this complexity.

- Strategic sourcing trends, such as nearshoring logistics, are being adopted to shorten lead times, while specialized transport like garment-on-hanger (GOH) and sea-air combined transport cater to specific product needs. The use of bonded warehousing and proficient cross-docking further streamlines complex supply chains.

What are the Key Data Covered in this Apparel Logistics Market Research and Growth Report?

-

What is the expected growth of the Apparel Logistics Market between 2026 and 2030?

-

USD 52.35 billion, at a CAGR of 7.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Service Type (Transportation, Warehousing and distribution, and Others), Product (Pre-production, and Trade logistics), Mode of Transportation (Road, Air, Rail, and Water) and Geography (Europe, North America, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

Europe, North America, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Fast replenishment cycle in apparel industry, Variability in fuel prices

-

-

Who are the major players in the Apparel Logistics Market?

-

Agility Public Warehousing Co., Apparel Logistic Group Inc., Bollore SE, CMA CGM Group, Delhivery Ltd., Deutsche Bahn AG, DSV AS, Expeditors International, Gulf Agency Co. Ltd., Hellmann Worldwide Logistics, Kintetsu Group Holdings Ltd., Kuehne Nagel Management AG, Logwin AG, NFI Industries Inc., Nippon Express Holdings Inc., PVS Fulfillment GmbH and Shipbob Inc.

-

Market Research Insights

- The apparel logistics market is characterized by intense pressure to enhance supply chain resilience and optimize the transportation network. A critical focus is on managing supply chain complexity driven by the proliferation of stock-keeping units and the demands of omnichannel sales.

- Effective logistics network optimization has become paramount, with data showing that streamlined fulfillment operations can reduce last-mile delivery costs by up to 15%. Moreover, achieving high inventory accuracy, often reaching over 99% through advanced tracking technologies, is essential for supporting a profitable fast fashion supply chain.

- As online returns frequently exceed 30% of sales, sophisticated returns processing is crucial for logistics cost management and maintaining a sustainable supply chain. These dynamics underscore the need for continuous innovation in last-mile innovation and distribution center automation.

We can help! Our analysts can customize this apparel logistics market research report to meet your requirements.

RIA -

RIA -